Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP, grateful I’m no longer tasked with trying to figure out direction of travel (outright / curve) as flow of news since Friday morning — more tariffs, FHFA talking ‘bout Fed chair resigning — certainly makes for nuanced trading / investing.

Here’s an updated look at long bonds. This as 10s continue to appear to ME to be home on the Rosie Range (with an albeit obvious bearish BREAK of medium term down trend) … I’ll offer this update recalling just a week ago, I was looking at a somewhat more bullishly leaning chart of bonds … how’d THAT work out?

30yy WEEKLY: 5.00 and 5.15 support vs 4.85, 4.75 resistance

… this time LAST week, momentum looked more bullish but now, price action has negatively impacted status and there appears to be room for rates to rise as the downtrend clearly broken … the UPTREND in place since … rate CUTS last year … has reasserted itself and that is VERY telling IMO …

For somewhat more on this, please see Jim Bianco’s mid-year update below as HE attempts to tackle why / how it could be that IF rates were cut, the bond market could (and has before) see it differently …

Fiscal concerns have NOT gone away and BlackROCKS Wei Li thoughts (equities favoured over USTs) remains as relevant and interesting today as they did HERE, just a week or so ago.

On THAT note, a couple of developments worth tackling … First up, from the FHFA director (at pulte) yesterday ‘bout 3pm, via X

… WTaF is going on?

Jul 12 2025 CNBC: Trump announces 30% tariffs on EU and Mexico, starting Aug. 1

… Trump revealed the new rates in letters to European Commission President Ursula von der Leyen and Mexico’s President Claudia Sheinbaum, which he posted on his social media site Truth Social…

… Alrighty, then. I’m really done. Anything BUT a quiet weekend in The Hamptons or ‘down the shore.

Good luck Sunday evening, y’all…

I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox

Ahead of CPI and ReSale TALES, a(nother)look at economic week ahead from across the pond …

Trade policy uncertainty has risen amid an extended negotiation deadline and new reciprocal and sectoral tariffs. Markets seem unperturbed, however, with US fiscal policy supporting growth and no negative tariff effects in economic data yet. Next week's US CPI is unlikely to change this narrative…

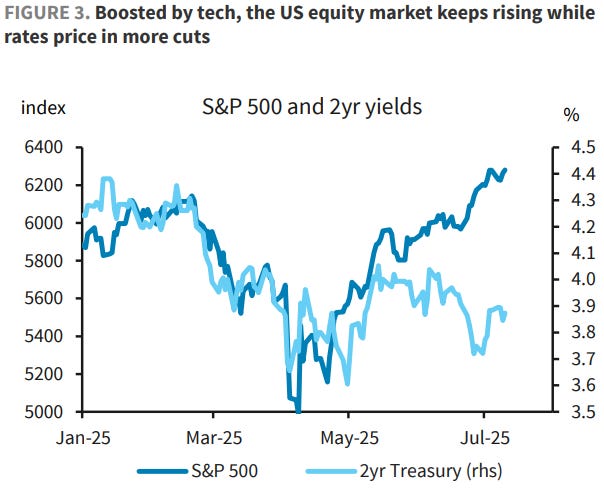

... and equity-bond market inconsistency Interestingly, the US equity rally was accompanied by a drop in government yields, including in 2y Treasuries. Hence, equity market's belief in robust economic and, thus, earnings growth goes hand in hand with the expectation for a reduction in Fed policy rates in the next two years. This is, in principle, not impossible, but it requires a very benign scenario where inflation continues to ease despite resilient domestic demand and much higher tariffs on imported goods. Disinflation in services prices and energy costs may provide some offset, but we would not assign a high probability to such a goldilocks growth-inflation combination. Hence, either equity or bond valuations may have to adjust.

We remain skeptical on both counts…

…US Outlook Strawberry letter 22 The president sent mixed messages on trade, extending the Liberation Day tariff pause until August 1 and sending letters to 22 countries threatening higher tariffs. As we await news about negotiations, we tweak our outlook to incorporate the budget act and some effects of the weaker dollar.

Even though the Liberation Day tariff pause was extended until August 1, trade policy uncertainty has re-intensified. The president sent out letters to 22 countries laying out tariff threats that, if realized, would push the overall trade-weighted tariff rate to levels following the Liberation Day announcement. We retain our assumptions but acknowledge risks of much higher tariffs.

With trade policy developments posing significant downside risks, we tweak our outlook to fold in an anticipated boost from last week's One Big Beautiful Bill Act and to give a nod to the weaker dollar. We think GDP growth will be slightly higher in 2025 and 2026, reflecting larger budget deficits in both years, and have also nudged up core inflation by 0.1pp this year.

The June FOMC minutes reaffirmed that voters are in no rush to adjust rates amid divided views on the outlook. Even so, "most" judged that a cut would be appropriate this year. Commentary stresses that only two voters are considering a cut in July, outnumbered by a contingent that favors no cuts at all this year. Re-intensified trade policy uncertainty is unlikely to hasten cuts.

…and the weaker dollar Our revisions also give a nod to the persistent weakness of the dollar so far this year, which runs against our prior assumptions. According to our translation of the Fed's FCI-g indicator (Figure 4), this weakness has contributed to a substantial easing of overall financial conditions in recent months. If sustained, this would stand in for rate cuts, implying an overall policy stance that is considerably more accommodative than the current target range for the funds rate would suggest. Our modeling also suggests that if the value of the dollar were sustained at current levels, core inflation would be 0.25pp higher than otherwise over the next twelve months and another 0.1pp higher in the following year.

In our view, dollar weakness is difficult to disentangle from downside risks related to trade policy, with markets hedging outcomes in which US growth is low in relation to foreign growth. Given that this would include adverse outcomes that are much weaker than our baseline, it implies that a fair bit of this dollar weakness would unwind if the outlook plays out as expected. Consequently, our revisions reflect only a modest boost to GDP growth in 2025 and 2026, as well as a 0.1pp upward revision to core inflation this year.

… same shop using a large language model to help garner some FOMC clues …

11 July 2025 Barclays FOMC Minutes NLP Analysis: Participants agree there is no rush to adjust, but upside inflation risks not broadly shared

Our NLP analysis suggests that FOMC participants remain on the same page regarding monetary policy and agree more broadly on the economic outlook. However, they are awaiting clarity on inflation, where views have started to diverge, with various takes on the upside inflation risks.

Best in show remaining IN 10s30s flattener and continues to look to add 2s10s as well as SFRM6/M7 steepening exposure …

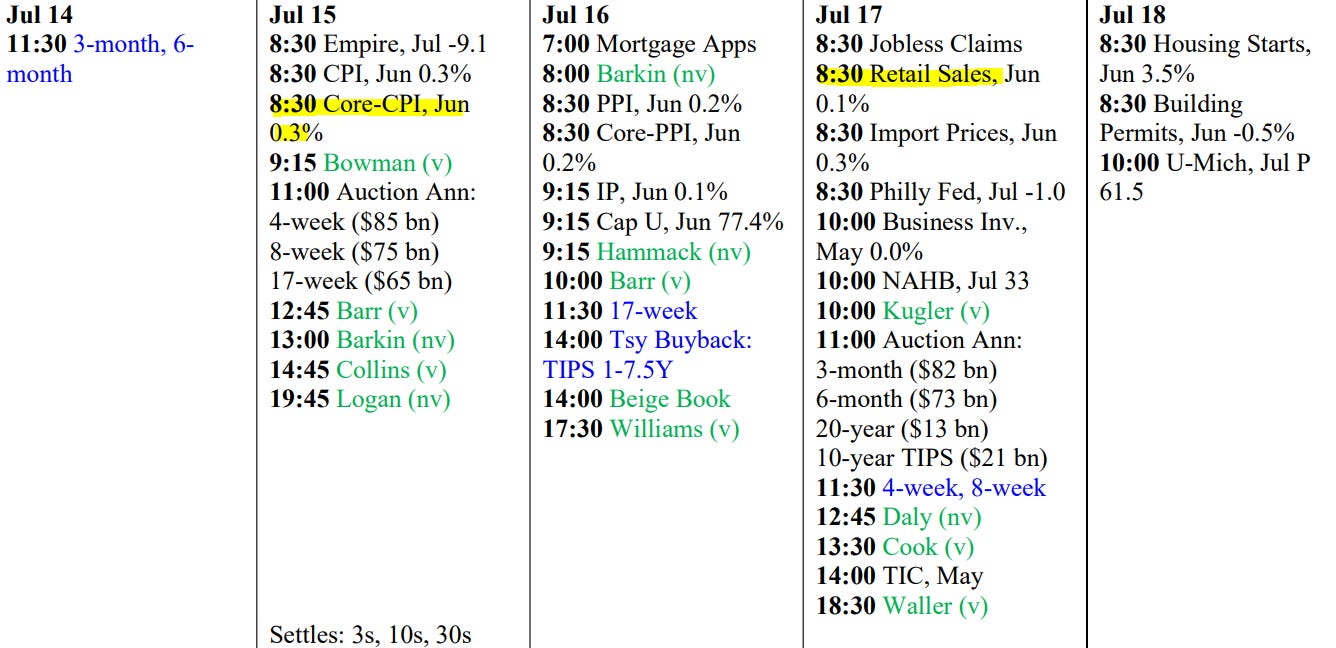

In the week ahead, investors will return to inflation watch. The combination of June’s CPI, PPI, and Import Prices will contribute to core-PCE expectations and provide an update on the Fed’s progress toward reestablishing price stability. As the current consensus is for a +0.3% core-CPI gain, we’re content with the characterization of an as-expected print as benign. Certainly, benign enough for the Committee to be comfortable with its success at reigning in inflationary pressures thus far in the cycle. Of course, it’s the numbers from August and beyond – when the full schedule of reciprocal tariffs apply – that will be the ultimate litmus test for the inflation complex. It’s not lost on us that during the second quarter, tariffs were meaningfully higher than prior to Trump’s Liberation Day announcements; even if they weren't as high as they will be later this summer – assuming that Trump follows through with his commitment not to further extend the latest round of levies…

…We’re tempted to view the market’s response to the budget deficit and implied forward borrowing needs as the archetype for responding to any future trade-war-driven reflation – sell the rumor, buy the fact. This would imply that the market has overpriced the upside inflation potential from the Administration’s actions. Let’s face it, it’s challenging for forecasters to estimate the full extent to which tariffs will pressure consumer prices – the wildcards being how much of the costs are absorbed by businesses via profit compression and what portion is ultimately funded by the consumer. Alas, we’re forced to rely on the passage of time for clarity on this issue.

As Q2 earnings come into focus, any indication of strains on profitability associated with the trade war will prove particularly relevant. As the FOMC Minutes highlighted, the last few months have seen such a rise in uncertainty that business leaders are waiting for clarity before making any major decisions. We’re certainly sympathetic to this approach; why would one commence any major undertaking while Washington is actively in the process of changing the rules? The upcoming earnings announcements and calls should provide further context for this concern. This all contributes to our range-trading thesis and reflects an investor base that is similarly waiting to see how the situation unfolds before establishing (or extending) any high conviction positions. Ultimately, we anticipate that the yield range will take on a downward-sloping skew – although not until the market has sufficient evidence regarding the full impact of the trade war and response of consumers. The latter point speaks to the importance of Thursday’s Retail Sales release. Watch this space.

…USD rates: Fed still on hold through 2025, flatter US curve Fed to remain on hold through 2025: Although a couple of Fed officials have hinted at a potential rate cut in July, Chair Jerome Powell indicated that the Fed could well stay on pause through the summer, with the next ‘live’ meeting coming in the fall.

We believe the FOMC is seeking conviction on which of two nonlinear risks to the US economy will require a response: a downturn requiring rate cuts, or entrenchment of high inflation into expectations requiring hawkish policy. While it waits, the FOMC is observing an economy that has proven highly resilient to a range of policy shocks, especially given the recent upside surprise in June payrolls. We think businesses have learned the lesson of past recessions: if they are overly proactive in laying off staff or pausing investment, these choices can be hard to reverse when the economy recovers.

Moreover, we think factors such as tariff collections, heightened recession fears and uncertainty over price hikes that induced a soft May CPI print are likely to fade heading into the June CPI print (0.34% m/m core). We continue to look for inflation to rise appreciably in the next release and maintain an elevated run-rate through the summer.

We stick to our long-held view that the Fed will keep rates on hold this year, resuming easing only in 2026 (four cuts).

Flatter US rates curve heading into 2026: We think rates markets will continue to focus on realized economic data on labor market or inflation, both of which have been relatively steady. While the FOMC dot plot suggested two median cuts in 2025, Powell repeatedly said "no one holds these rate paths with any conviction," moving the markets away from interpreting the dot plot or even the SEP too literally. Much like the May FOMC, Powell's remarks conveyed a sense of wait and watch, disappointing those who think the Fed is looking to actually deliver two cuts (or more) this year. Even with dovish comments from Governors Christopher Waller and Michelle Bowman, the overall cutting path through 2026 was little changed, as more cuts now would mean fewer cuts later.

By September 2025, we expect markets to have priced out all 2025 rate cuts, lifting 2y yields. We then see 2y yields tracking lower, ending 2025 at 4%, before the Fed delivers four rate cuts in 2026. The 10y yield depends more on the perception and news on deficits and supply– demand, and to a lesser extent on the economic backdrop. The upward drift in the Fed path (no cuts expected for 2025) and inflation (upward drift starting this summer) that we are expecting should be offset by a stable deficit trajectory and a bond-vigilant administration. We believe Treasury Secretary Scott Bessent will pursue a 'T-bill and chill' strategy by funding deficit needs with bills and leaving Treasury coupon auction sizes stable for the foreseeable future. The Fed also recently released bank regulation relief through lowering leverage requirements for some of the largest US banks, providing a backstop for long-end UST yields in the event another selling frenzy from bond vigilantes materializes.

A very senior member of the Trump administration yesterday sent a letter to Fed Chair Jerome Powell asking whether he misrepresented facts to Congress with regards to the costly renovation of the Federal Reserve headquarters. Some are arguing that this is opening up a legal avenue for President Trump to remove Chair Powell for cause. What if this happens and President Trump asks Powell to leave? We offer a few thoughts on market implications…

…So how large would we expect the market reaction to be? The empirical and academic evidence on the impact of a loss of central bank independence is fairly clear: in extreme cases, both the currency and the bond market can collapse as inflation expectations move higher, real yields drop and broader risk premia increase on the back of institutional erosion. Interestingly, the impact on equities has been far more ambivalent given they are ultimately a claim on real assets. We would point to the example of rallying equities in Turkey during the unconventional monetary policy period of the CBT.

It is hard to quantify the impact on FX and rates, but on the first 24 hours of an announcement of a Powell removal we would expect a drop in the trade-weighted dollar of at least 3%-4% accompanied by a 30-40bps sell-off in US fixed income led by the back-end. Similar to the experience in April, we would expect the correlation between the bond market and the dollar to turn sharply positive (both down), while we would also expect a widening in cross-currency basis as the market may worry about the politicization of the Fed swap lines…

…All being said and done, none of the above should be interpreted as lessening the significance of a potential removal of the Fed Chair for the market. At a minimum, we would expect a sustained and persistent risk premium to be subsequently embedded in both the US dollar and the Treasury market, with exceptionally high sensitivity to both the mix of data and the conduct of monetary policy in the subsequent months. But beyond that, we worry about the very vulnerable external funding position which the US economy currently finds itself in; this raises the risk of far larger and more disruptive price moves than the ones we have outlined here. In sum, we consider the removal of Chair Powell as one of the largest under-priced event risks over the coming months.

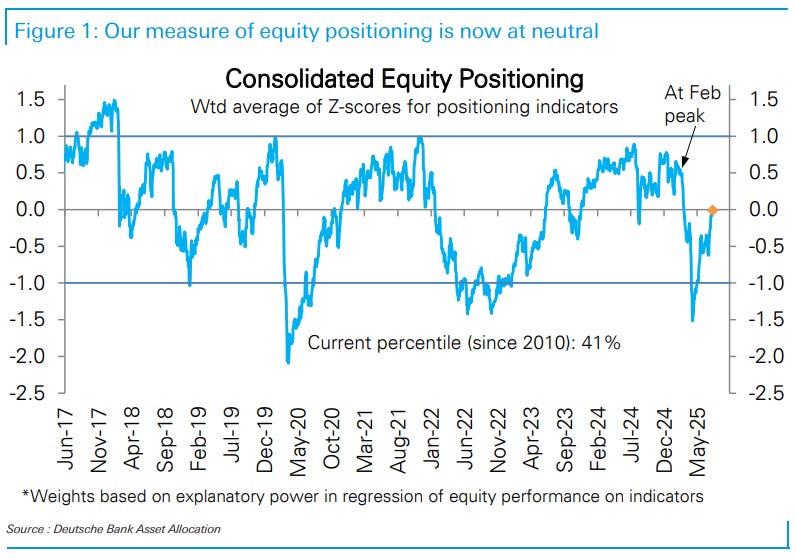

Equity position / flows update — finally made it up on TO the fence …

11 July 2025 DB: Investor Positioning and Flows - Neutral Positioning With Some Pockets Of Exuberance

Our measure of equity positioning is now at neutral. Against the backdrop of equities climbing to record highs, this read contrasts with the growing narrative of surging risk appetite and equity exposure, especially amongst retail investors. Why the disconnect?

While the record highs are impressive, the S&P 500 is just back to the middle of its post-GFC trend channel, where it was at the prior Feb peak. From a long-run perspective, the returns since the Feb peak (5% annualized) or even ytd (12.5% annualized) are about average at best outside of recessions and arguably even subpar.

Several measures suggest that there are some pockets of exuberance, but only some: our early-cycle basket of stocks has been rallying since the April bottom but tends to outperform in bursts and is approaching the top of its usual range; bullish option volumes remain within the range of the last 2 years and crucially have not been driven by small sized trades, unlike the 2020-2021 boom; a basket of stocks with the highest call volumes in the prior week has begun to outperform again over the last 2 weeks, a good indicator of rising risk appetite and momentum-driven buying in some pockets; similarly, certain stocks are posting eye-popping short-term rallies, but these have not sustained or gone wider; there is also no sign of exuberance in US equity flows, whether to funds overall, or into riskier products like leveraged and single-stock ETFs, with all largely seeing outflows over the last 3 months; crypto funds however have been receiving robust inflows.

Equity positioning at neutral means that it is still vulnerable to negative catalysts. The market has not treated the recent tariff escalation as a negative catalyst at all, as it was very predictable, with the expectation that a relent will come eventually. However, the lack of an equity selloff means other forms of negative feedback might have to be relied upon for a relent. This sets up a trip hazard and with positioning at neutral, a true negative catalyst will see equities react.

Same German shop offering an updated visual and tracker of tariffs …

11 July 2025 DB: Tariff tracker update: Letter by letter

In this piece, we update our tariff tracker with new actions by the Trump administration. Since our previous update, letters with country-specific rates have been sent to the heads of state of eight other countries, most notably Brazil and Canada, bringing the total number of letters to 22. In addition, President Trump announced a 50% tariff on copper to begin on August 1st.

The announcements this week bring our tariff tracker up to 20.7%, should those tariffs end up going into effect. Should remaining countries end up with country-specific rates close to those from April 2nd, this could rise to 24.4%.

On July 31st, the federal appeals court is scheduled to hold oral arguments regarding the Court of International Trade's previous ruling against the tariffs imposed under the International Emergency Economic Powers Act (IEEPA). Should that ruling stand, this would eliminate all the country-specific tariffs instituted thus far. In this situation, the administration would likely expand sectoral tariffs or turn to other powers (e.g. Sections 122 and 301) powers to achieve its policy goals.

In the unlikely event that Fed Chair Powell is removed or steps down before his term ends in May 2026, we would likely see a sharp steepening in the Treasury curve as markets price in cuts, inflation risks, and diminished Fed independence. That could create an even more toxic mix for the dollar than 'Liberation Day', with EUR, JPY and CHF best placed to benefit …

…Bond impact: a much steeper curve Such a deepening in interest rate cut expectations would filter directly into the front end of the curve. The 2yr yield is now at 3.9%. There’s a path to (sub-) 3%, based on a theory that, even if the FOMC does not react immediately with big cuts, the market discount could ultimately price the funds rate down towards 2%. It could, but there are challenges to that. The first would be the reaction of longer-dated rates.

So, how would the 10yr yield, now at 4.4%, deal with a downward lurch in short tenor yields? Usually, it would get dragged down too. But the long end of the bond market is a deeper thinker than the front end. It will be questioning the risks being added to inflation. Holding a 10yr bond means receiving fixed coupons and redemption, so factoring in long-term inflation is key to assessing the real return.

The long end already has an elevated fiscal deficit and upside to consumer price pressures coming from tariffs to worry about. Adding front-end rates that are arguably too low for the economy risks adding permanence to the higher inflation prints. The fact that front-end rates are in the 2-3% range is a relative value factor that’s not unimportant when framing where the 10yr yield should be. The aforementioned factors are in fact more important.

The outcome then is a much steeper curve, with front-end yields lower and longer-term yields higher. Think of a (sub-) 3% to 5% (2yr to 10yr) curve. A 300bp curve sounds ultra steep, but we had a 300bp term premium back in the 1990s, and 400bp in the 1980s (we even hit 500bp). These were different times for many reasons, but it’s not like we’ve not seen those types of levels in the not-too-distant past.

The 2/10yr curve has stretched towards 300bp in the past, and the 10yr Term Premium to 500bp

The 10yr Term Premium is effectively the 10yr market yield versus the market discount for a running bills exposure over the subsequent decade (rolling)

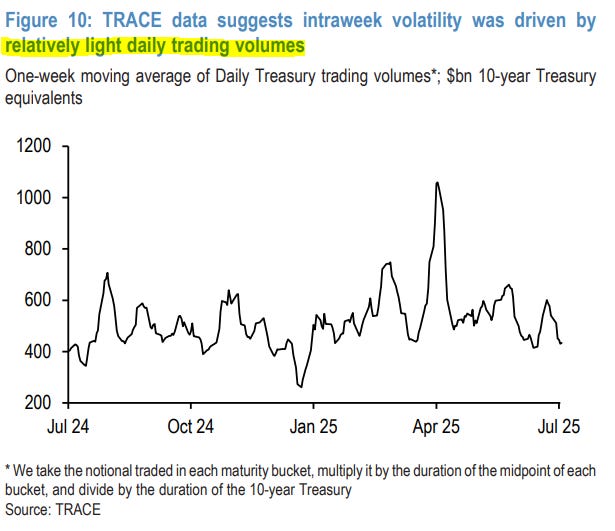

Jamie Dimon’s operation notes this past weeks (BEARISH PRICE ACTION) on ‘relatively low trading volumes’ … signal vs noise?

11 July 2025 JPM: U.S. Fixed Income Markets Weekly

…Governments With most of the curve near the middle of recent ranges, positioning relatively neutral, and 10-year yields fairly valued, we remain neutral on duration with an eye to trading the local extremes. Hold 10s/30s flatteners. Following the debt ceiling resolution, we project $629bn of net T-bill issuance over the current quarter. P-STRIPS outstanding declined $0.7bn in June. A re-escalation in the trade war has driven front-end breakevens sharply wider. We took profits on 5s/30s breakeven curve flatteners, but forwards in the 4Y-6Y sector remain cheap. Add synthetic 3Yx1Y BE wideners.

…Treasuries Range trading before focus turns fully to issuance

Looking ahead, we do not expect June CPI or retail sales to change the fundamental narrative next week, justifying a rangebound environment for Treasury yields

Given this backdrop, with most of the Treasury curve trading in the middle of recent ranges, positioning technicals relatively neutral, and 10-year Treasury yields appearing fairly valued, we remain neutral on duration with an eye to trading the local extremes...

...though we continue to favor 10s/30s flattener exposure as the long end remains somewhat steep after controlling for Fed policy and inflation expectations, Fed balance sheet policy and trade uncertainty …

… Importantly, while these crosswinds resulted in intraweek volatility for the curve, TRACE daily trading data reveal this was driven by relatively low trading volumes (Figure 10)…

Not QUITE the Rosie Range but … an excellent comment from an astute group who remains LONG 5s (3.97) and in 3s30s steepeners, among other trades …

July 11, 2025 MS: What Takes 10-Year Treasury Yields Above 5% or Below 4%? | US Rates Strategy

At current levels of term premium, a market-implied trough fed funds rate below 2.60% or above 3.90% would suggest a 10y Treasury yield below 4.00% or above 5.00%, respectively. But the prospect of higher tariffs risks a higher term premium, so stay in 3s30s Treasury yield curve steepeners.

Key takeaways

The April 2 "Liberation Day" and events that followed injected ~50bp of risk premium into 10y UST yields at its peak. Nearly 40bp remains in the yield today.

We estimate that over 75% of this term premium arose in term fed funds OIS rates, with the balance in Treasury securities.

Continued concerns over US administration trade policy could raise term premiums further, even though higher tariff revenues lower financing needs.

We don't see debt sustainability presenting upside risks to term premiums. Instead, issuance strategy and financing needs introduce downside risks.

Tuesday brings US CPI - a critical data point certain to influence how investors think about Fed policy this year. Stay in curve steepeners and long duration.

Earlier this week President Trump pushed out his deadline for the revised/negotiated reciprocal tariffs from July 9th to August 1st, allowing additional time to negotiate other trade deals. However, tariff rates were communicated to various trading partners, which without a trade deal would go into effect on August 1. For most trading partners the communicated tariff rates were higher than the 10% rate that had been levied since the week after Liberation Day. We estimate this week’s announcements would push up the average import-weighted tariff rate from around 14% to 16.7% though the entire impact from these tariffs has not been felt so far. Tariff revenue collected as a percentage of total imports remain well below the applicable rates. That to us suggests not all imports have been subject to tariffs so far, which may have kept a lid on the pass through to inflation.

Indeed, recent inflation prints have been constructive for the Fed’s inflation mandate. On a three-month annualized basis, both the core CPI and the core PCE cooled to 1.7% in May, down from around 4% at the beginning of the year. Moreover, the cooling was broad based with core goods and core services inflation each running below 2% (three-month annualized rate) in May. We wouldn’t be surprised by another benign core CPI print in June, despite some tariff pass through, which would beg the question as to will tariffs be enough to move overall price pressures higher.

We have long expected most of the potential impact from tariffs would begin to show up in inflation data over the course of the second half of the year amidst some knee-jerk reaction in specific price categories (e.g., used vehicles) immediately after tariff announcements. Our expectation for reacceleration in core inflation over the course of H2(25) due to tariffs hasn’t changed, as discussed below. We continue to expect the core CPI to rise to 3.5% y/y by December 2025 and core PCE inflation to rise to 3.3%y/y by December 2025. We expect core goods inflation to rise from 0.7%y/y in May to 4.8%y/y by December this year as tariffs feed through, which will be more than enough to offset the ongoing disinflation in the larger weighted core services prices (forecast 2.8%y/y in December 2025 from 3.3%y/y in May 2025).

Moreover, we believe the risks to the inflation outlook remain to the upside. The whipsawing of indicative tariff rates effectively translates to corresponding price increases even without a final effective rate in place, which would make their inflation impact more persistent. Additionally, further delays to potential reciprocal tariffs will push out the inflationary impact into next year.

… and same shop who was talkin’ tariff, also offerin’ CPI precap …

After a downside surprise in May, we expect both the total and the core CPI to resume trend-like clips of 0.2% each in June. Our unrounded core CPI estimate at 0.226% in June is not too far from its year-to-date (January-May) average gain of 0.219%. While we expect some pass through from tariffs to core goods prices (forecast +0.4% after +0.0%), core services prices likely posted another modest gain of 0.2%.

On a y/y basis, base effects will continue to push readings higher. We expect the total CPI to rise from 2.4% in May to 2.7% in June, as a flat reading from last June falls out of the calculation. Similarly, after having held steady at a four-year low of 2.8% in May, the core CPI could quicken to 3.0%, as a 0.1% reading from last June drops out. We also expect the June CPI NSA index to print at 322.526…

… and on rates …

11 Jul 2025 NatWEST: US Weekly Economic and Strategy Brief

…US Rates: The strong payrolls print last week has reduced the likelihood of Fed easing in the near term. Focus shifts to the potential impacts of tariffs given the deadline this week, while the US president continues to call for lower rates.

Switzerland callin’ …

11 July 2025 UBS: US Economics Weekly Tariff escalation

Economic Comment: tariff uncertainty to persist With equity markets and the inflation data failing to display much impact from tariffs, a new series of trade proposals were rolled out this week. The reciprocal tariffs at risk of snapping into effect this week were postponed again, to August 1. More than 20 trading partners appeared to be sent letters outlining new reciprocal rates that could come into affect August 1. Administration officials also commented this week on potential sectoral tariffs on copper and pharmaceuticals. It has been a busy week for tariff news, with little immediate impact, but potentially larger impact looming…

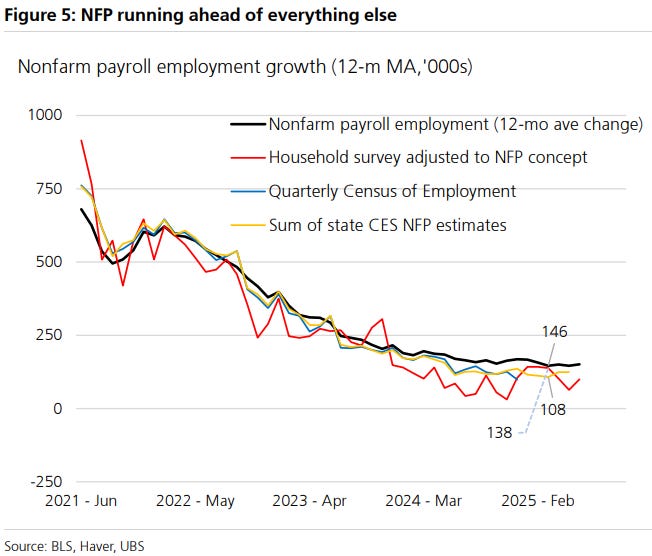

…Labor market mismeasurement Looking ahead to the next benchmark revision to nonfarm payroll employment (NFP), we expect the level of employment as of March 2025 to be revised lower by several hundred thousand. We estimate that the monthly establishment survey estimate of NFP has been overstating actual increases in jobs. In the household survey, we remain sceptical it reflects the labor market due to small sample sizes and problems weighting that sample to be representive of the population. For example, people seem to think immigration is slowing and thus US population growth. However, in the household survey, that is accelerating in 2025…

The Week Ahead: CPI and the end of month rush We expect the core CPI climbed 0.23% in June, held down importantly by what we estimate to be faulty seasonal adjustment. We project retail and food services sales fell 0.2% in June, held down by autos, light trucks and sales at gasoline stations. We expect sales at the control group of stores fared better. Real consumer spending has been relatively weak thus far this year, down year-to-date in real terms and running just 1.2% annualized over the last four months. Next week, we expect a rebound in multifamily activity pushes total housing starts higher, but single family activity slips further. The leading indicator in that report, single family permits, fell from a 992K annualized pace in February to 899K in May, declining sequentially in each of the last three months, pointing to weakness in residential investment. The week of July 20-July 26 is light on data, but June durable goods data that Friday will update whether orders are breaking up or down. Orders of non-defense capital goods ex aircraft were roughly flat from January through May, neither deteriorating due to policy uncertainty or caution, nor suggesting any acceleration either..

… covered wagons folks on dog days of summer AND FOMC (unch, for now) …

July 11, 2025 Wells Fargo: Weekly Economic & Financial Commentary

United States: Dog Days of Summer While it was a light week on the economic data front, there was still plenty of news to digest with tariffs coming back to center stage. Elevated uncertainty is beginning to creep into economic activity, leading us to revise down our estimate for Q2 real GDP growth…

…Interest Rate Watch: FOMC Remains in Wait & See Mode, at Least for Now The minutes of the June 17-18 FOMC meeting indicate that the Committee likely will not cut rates at its next meeting at the end of this month. However, we think conditions will warrant a 25 bps rate cut in September.

… The FOMC's assessment is in line with our own views. As we noted in our most recent U.S. Economic Outlook, we think the probability of a rate cut at the July 29-30 FOMC meeting is very low. Indeed, market pricing as of this writing implies a probability of a 25 bps rate cut at that meeting of less than 10%. By the time of the next policy meeting on Sept. 16-17, Fed officials will have received two more labor market reports (Aug. 1 and Sept. 5) and three more CPI inflation reports (July 15, Aug. 12 and Sept. 11). If, as we forecast, any rise in inflation in coming months proves to be a bump rather than a spike and the labor market softens further, then we believe the Committee will reason that a more accommodative stance of monetary policy is appropriate. We look for the FOMC to cut rates by 25 bps on Sept. 17 followed by two more similar reductions on Oct. 29 and Dec. 10 (chart).

… Moving along TO a few other curated links from the intertubes, which I HOPE you’ll find useful …

Immigration restrictions = INFLATION? May just be …

July 12, 2025 Apollo: The Economic Effects of Immigration Restrictions

If 3,000 unauthorized immigrants are deported every day, the labor force will decline by roughly 1 million people in 2025.

Lowering the labor force by 1 million will reduce the participation rate by 0.4 percentage points, which will lower the unemployment rate, lower job growth, and increase wage inflation, particularly in the sectors where unauthorized immigrants work—namely construction, agriculture, and leisure & hospitality.

In short, deportations are a stagflationary impulse to the economy, resulting in lower employment growth and higher wage inflation.

For more discussion and quantification, see this new working paper by Edelberg, Veuger, and Watson.

… Mom always said, be careful whatcha wish for, cuz you might just get it …

For MORE on this concept, this next note discusses how it may / COULD be that rate CUTS lead to higher longer-term yields …

On June 30, President Trump posted the following image to social media. It was a handwritten note to Jay Powell.

The market is looking past this view, as the Fed is unlikely to cut rates this drastically. But if Trump gets a Fed Chair to make 1% happen, how would the 10-year react?

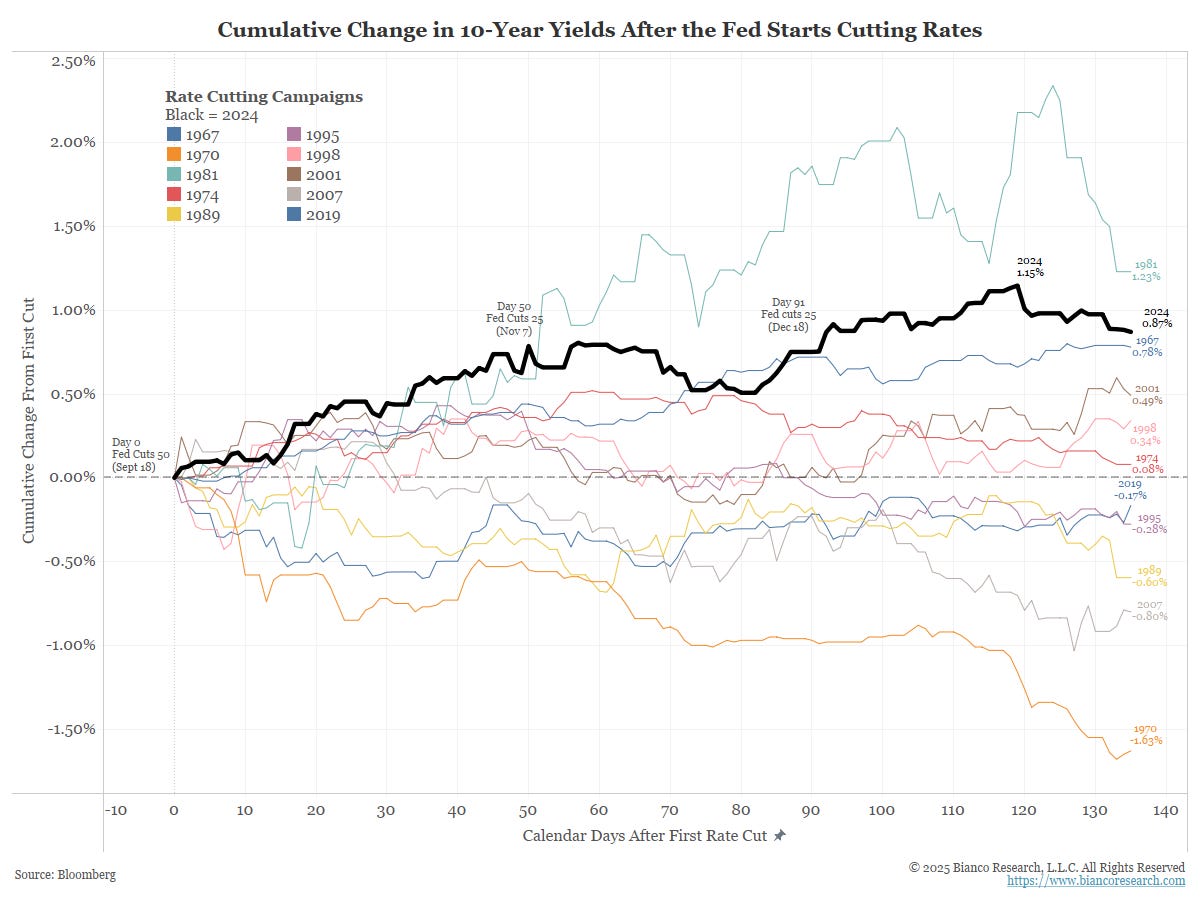

This is a reminder of what happened to long rates last year when the Fed cut rates (peach arrow) and the market did not think it was a good idea (cyan arrow).

Long-term yields “rejected” the rate cuts last year by rising. As the next chart shows, this was one of the largest in 60 years. Last year’s rise in the 10-year was the second largest in the previous 58 years.

Only the 1981 cut (which started in May 1981) saw a bigger rise in yields. But note that in 1981, yields were 13%. Therefore, we would argue that a move from 13% to 15% is not as significant as a move from 3.6% to 4.8%, which is what happened last year.

Why is Trump demanding rate cuts?

The problem with Trump’s argument is that he assumes interest rates are “made up.” So, he would like the Fed/Jay Powell to “make up” a lower interest rate.

He wants this so interest costs will fall. But see the chart above, the last time the Fed cut rates (last year), long-term yields soared, and interest costs rose.

This is because yield levels are not “made up.” Fundamentals such as inflation expectations, growth outlooks, and supply needs contribute to the fair value of yields, or nominal GDP, as detailed above.

Bond yields are not out of line with the economy. Cutting rates risks putting them out of line.

…. hmm that would suck …

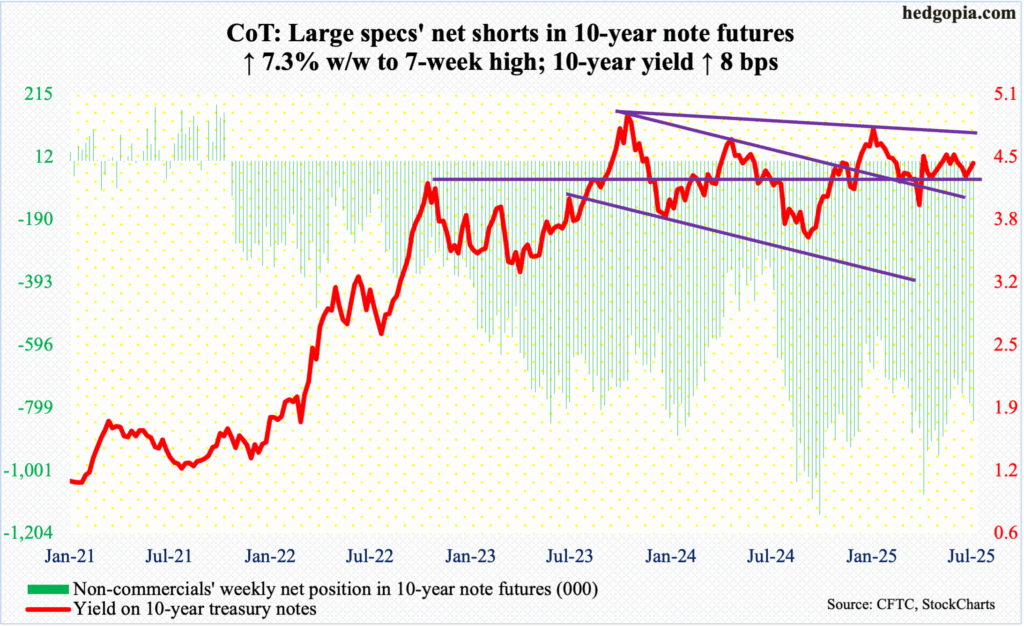

Positions matter … shorts are building once again …

12 JUL 2025 Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

Spectra and Brent Donnelly with a few words (visuals) of stocks seasonality and of rates … entire note worth a look but …

July 11, 2025 Spectra Markets: Rainbows and Lollipops There’s nothing left to worry about

…Here’s the typical path of US equities through the year:

As you can see, buying stocks on July 15 and selling them on October 15 has been a flat proposition over the past 25 years because August and September are lackluster months for the stonks. Hard to make a strong case for limit short here, other than seasonality and maybe sentiment. That said, we are entering earnings season, so if you were looking for a catalyst, I suppose that’s the one. I have no particular reason to think earnings will be bad, but you never know…

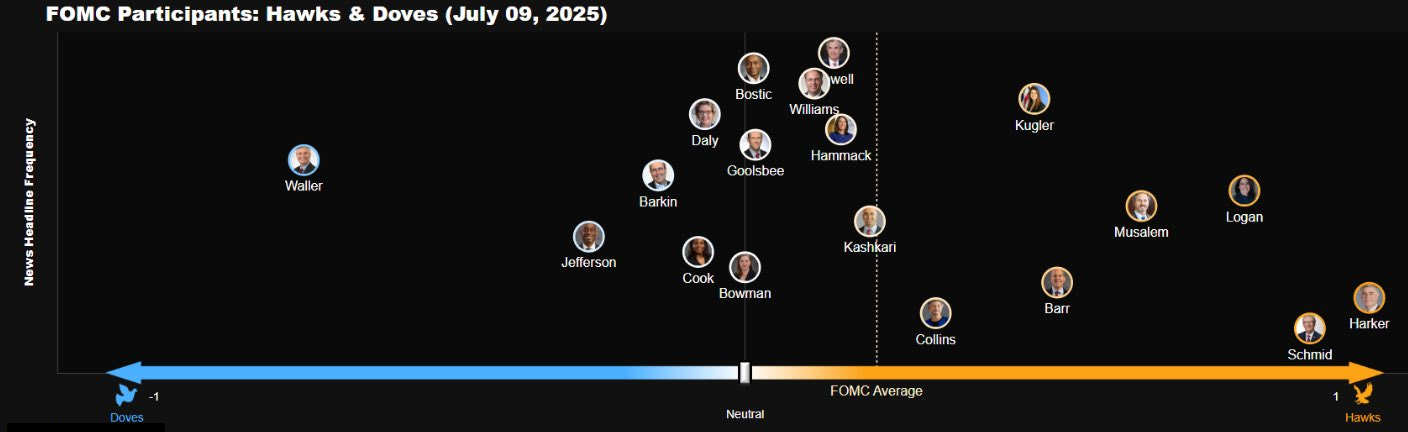

…Interest Rates The Fed is split into two camps, one led by Chris Waller and the other featuring a majority of the committee. This chart from Bloomberg illustrates it nicely.

The chart shows “news headline frequency” on the y-axis and “dovish vs. hawkish” on the x-axis. Nice little reference for Fed followers. Look at Waller way over there hanging out by himself. I would put Bowman closer to Waller on this thing, but otherwise it’s quite good.

Meanwhile, the bond vigilantes are out in the parking lot doing pushups and maybe we will see them again at some point. US and Japanese yields are creeeeeping higher again, but remain in familiar ranges. I bought some TMF puts yesterday (the levered bond ETF) because I think there’s a chance that CPI comes in wonky high on a snapback after the front-loading weirdness in last month’s release. That said, if there’s going to be an inflationary impact from tariffs, it could still be way too early for it to show up in the data. Still, I think the convex side if there’s a move in 10-year yields next week will be upward as we already got a strong rejection of the downside sub 4.20% on Canada Day.

… guess it is ok if I no longer have a Terminal as long as I can lean on folks like Brent to come through with excellent notes, if only weekly (for general public viewing…!)

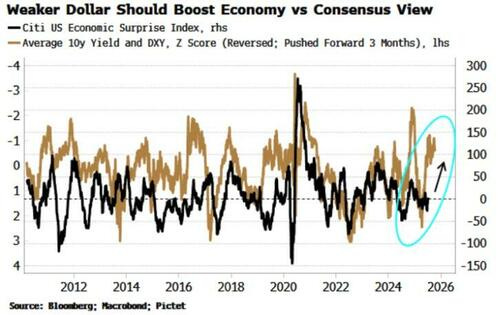

US recession (and so, rate cut(s)) coming? May be decided by ‘king’ dollar …

Bloomberg (via ZH): Can The US Avoid Recession? A Lot Depends On The Dollar

Near-term US recession risk is low, but there are pockets of weakness that could mutate into a downturn later this year. The weaker dollar, though, will be key to whether the US avoids that fate and stocks a significant decline.

For now, it’s gone quiet on the recession front.

Not long ago, there was febrile speculation that a downturn was imminent, despite a lack of support from leading data.

Since then, the clamour has died down, and that can make one a little uneasy. Not necessarily because we should be worried about an imminent recession, but it does imply the market is now less prepared for bad news, which increases the likelihood of a disproportionate impact on asset prices.

My Recession Gauge – an amalgamation of 14 separate recession indicators – has fallen and is well under the activation threshold. But there are areas of weakness in the economy that could trigger anxiety and cause stock markets to drop, at least temporarily.

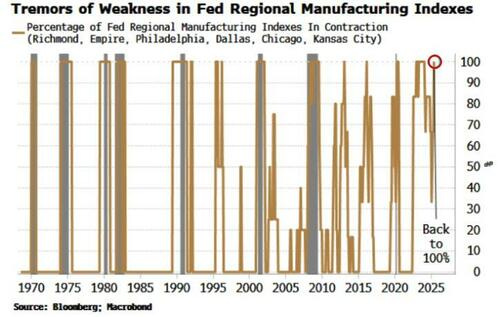

One notable point can be found in the Federal Reserve’s regional manufacturing indexes. Individually they are very volatile. But when they act in concert, they give a more reliable indication. The combined signal has recently jumped back to 100%, with all the indexes now in the contraction zone.

As we can see from the chart above, this particular data point has given a few false positives in the past, so it is not perfect. But equally it’s not something that should be ignored, as manufacturing is one of the most leading sectors in the economy. Moreover, recessions are pervasive. So a nationwide decline in manufacturing is best monitored.

We might also see other signs of economic weakness in the coming months. One point to focus on might be whether the rise in WARN (advance layoff) notices presages weakness in unemployment claims and the wider labour market. Another area to watch is the housing market, and whether that starts to become a wider problem.

None of these guarantee a recession however, especially if the weaker dollar eases financial conditions to keep a downturn at bay. The drop in the US currency should also translate into a boost for stock earnings.

More broadly, though, dollar weakness and (at least for now) relatively stable yields are typically consistent with economic data improving relative to the consensus.

There are more malign effects from the weaker dollar also in the pipeline such as higher inflation, but at least through the rest of this year, it might be enough to forestall a return of recession angst.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Back to topic du jour yesterday afternoon and which I led with above (and a few on Global Wall have commented, ‘What IF…’) …

at NickTimiraos

When people ask me about various internet rumormongering, my first instinct is to ignore it in the same way the TV cameras don't show the streaker running on the field at Yankee Stadium.

But for people who really do wonder about whether the Fed chair would do the opposite of what he keeps saying he will do (which is to serve out his term as chair, now just 10 months to go), I reflect on how Powell answered the question about getting in the life raft six years ago.

I included that answer in my book because it doesn't get any more absolute: “I will never, ever, ever leave this job voluntarily until my term ends under any circumstances. None whatsoever. You will not see me getting in the lifeboat.”

“It doesn’t occur to me in the slightest that there would be any situation in which I would not complete my term other than dying.”