weekly observations (05.13.24): CPI of the tiger (BAML), ROUNDING error (BMO) and more on CPI; "High-Risk Options Bet on Bond Rally At Risk of Losing Millions"

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

It will be brief ‘ish and slightly different ‘format’.

Jumping in to where we left off when there was a time not too long ago where we were looking for and took ‘clues from 2s’ ….

… and it looks like the price action is, shall we say, inconclusive at the moment. This is despite or because of the (lack of)news in the week just past (more on UoMISSagain shortly) and ahead of inflation data which will be very telling in the week ahead …

First UP, yesterday …

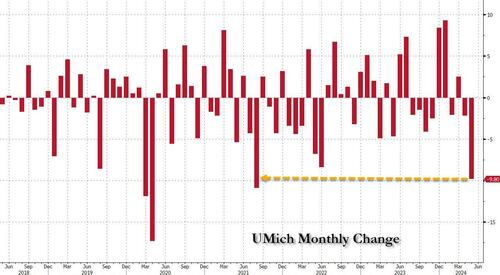

ZH: Bidenomics Implodes: Consumer Sentiment Unexpectedly Craters In Biggest Miss On Record As Inflation Expectations Surge

… Sentiment "unexpectedly" plunged from 77.2 to 67.4, the 9.8 point drop the biggest since August 2021...

… This a very nice combination with jobless claims and so, Team Rate CUT, for the WIN.

But then … Fedspeak and as we know, all opinions are created equally but some are simply more equal than others …

Bloomberg: Fed’s Logan Says Still Too Early to Think About US Rate Cuts

Evidence mounting that neutral interest rate level is higher

US economy’s resilience is surprising given high rates

… and by days end …

ZH: Stocks End Week On Muted Note As Stagflation Fears Mount

… Basically, an underwhelming week in rear view mirror will be greeted anxiously by all looking for an updated narrative post CPI.

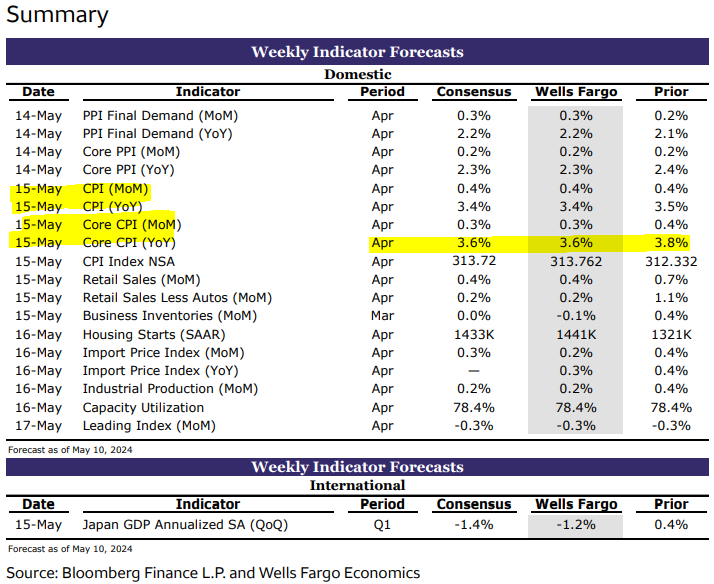

I’ll move on to a shorter format of what Global Wall is sayin and sellin this weekend. I’ll run through some VIEWS you might be able to use where lots of ink being spilled ahead of CPI …

… US: Shift in sentiment post FOMC has been expressed cautiously in UST exposures. Market on a holding pattern ahead of CPI. We see the balance of risks around the CPI print tilted slightly bullish rates.

… Bottom line: The market is in a holding pattern ahead of CPI, with 10yT c.4.5%, in between the c.4% yields consistent with soft landing scenarios, and the c.5% yields that exhaust no-landing scenarios. CPI has the potential to break the impasse and drive 10yT to the bottom of the 4.25-4.5% “nibble” range on a soft print, or the top of the c.4.5- 4.75% “bite” range on an above consensus print. Our economists are biased towards the soft side of consensus, and we see the balance of risks tilted to the downside in yields…

… Technicals: The buy zones Our technical process suggests the countertrend YTD rise in US yields is near an end. Buy zones: 2Y 5.00-5.25%, 5Y 4.75-4.98%, 10Y 4.70-5.02%, 30Y 4.85-5.06%.

… US Outlook Over-reading the signals With last week's signs of labor market slowing accompanied by deterioration in soft indicators, markets have become more optimistic that the FOMC might be inclined to cut earlier than its "higher for longer" messaging. We think this extrapolation is premature, with a firm inflation print next week a possible wake-up call.

BMO: US Rates Weekly: Rounding that Ruined the Day

… Before concluding that April’s data risks doing the same and erring on the side of pattern recognition, we’ll offer a quick glance at the unrounded figures of relevance. Core-CPI came in at +0.359% for March, +0.358% in February, and +0.392% during January. Said differently, it was a close call between +0.4% and +0.3%, and it was the rounding that ruined the day (at least for the Fed). Digging a little deeper, we see that the unrounded supercore numbers (core-services ex-shelter) were a bit more concerning at +0.681% March, +0.502% February, and +0.701% January. This trend undermines the argument that it was simply a January spike that moderated throughout the quarter; hence, the relevance of Wednesday’s data…

… , forward-entry long in the 10-year space did not reach our buy level as benchmark rates have remained well-anchored to 4.50% although we'll continue to play for more attractive entry points in the event yields stage a breakout back near the 4.60% level … For a new trade this week, we like fading the 2s/10s curve's kneejerk response to a consensus core-CPI move of +0.3%. Presumably such a print would be traded as a bull steepener, and given the distribution of estimates and recent tendency for core-CPI to surprise on the upside, we'll look to take advantage of an outsized market response…

In the attached Weekly we provide some thoughts about why CPI rents might be taking longer than usual to reflect more slowly rising market rents and we comment on Minneapolis Fed President Kashkari's essay about the stance of monetary policy and neutral interest rates. We also take the opportunity of a quiet week for economic data to step back and think about lower-frequency issues.

DB: Exploring bidding aggressiveness at 10yr auctions

In today’s chart, we build and examine an index to explore how aggressive bidders have been at recent 10-year auctions…

… The index highlights that end user bidding at 10-year auctions over the past 11 months has been consistently less aggressive. One notable aspect is that all auctions have had a negative index value since the first increase of auction sizes at last year’s August quarterly refunding, suggesting that the increased issuance may have affected how aggressively end users bid for Treasuries at auctions. Although this month’s quarterly refunding marked the end of auction size increases, the auction sizes remain at record highs, raising questions about investor appetite and bidding aggressiveness for 10-year notes at auctions going forward given the elevated issuance levels.

Goldilocks: UMichigan Sentiment Drops and Inflation Expectations Increase in Preliminary May Report

BOTTOM LINE: The University of Michigan’s index of consumer sentiment declined in the May preliminary report, well below consensus expectations for a smaller decrease. The report’s inflation expectations measures both increased above consensus expectations, with the year-ahead measure at 3.5% and the long-term measure at 3.1%. This likely reflects higher gasoline prices and the higher-than-expected price data reported so far in 2024.

The Treasury curve twisted flatter, with front-end yields rising 4-6bp and long-end yields remaining relatively unchanged, as data was mixed and the refunding auctions were digested without incident.

The decline in yields from their peak is largely due to mean reversion: 10-year yields had traded about 40bp too high controlling for the market-based Fed policy, inflation, and growth expectations, and that residual has been cut by 35%

We forecast core CPI rose 0.33% in April and this could alleviate concerns about reaccelerating inflation, but we do not think this is consistent with further progress toward the Fed’s 2% inflation target, justifying a later start and slower pace of Fed easing

We are hesitant to extend duration: with markets pricing the first Fed cut in early-fall and the curve still inverted, carry is punitive. Instead we would look to add duration exposure at the front end if yields retrace toward their recent highs: equi-notional front-end flatteners are attractive as they behave like low-beta duration longs with a better carry profile than outright longs

Risks to our view stem from further upward revisions to growth and inflation forecasts, which could push market-based Fed pricing in a hawkish direction. Powell’s comments indicate the bar for hikes is high and front-end yields would have limited room to reprice higher, while the intermediate sector would likely underperform, hurting our long-end steepeners. Meanwhile, a sharp weakening of the labor market, which could prompt the Fed to ease earlier and more aggressively, would support our steepeners…

MS Global Macro Strategist | SkiPPIng A Heartbeat Into CPI

Once again, the fate of government bond markets in most parts of the world will likely come down to the US inflation reports in the coming week. Fear of tariff announcements – before and after the US general election – could increasingly fray nerves in the absence of improvement in PPI and CPI data.

Earlier this year we made significant upward revisions to our GDP growth and unemployment forecasts while leaving inflation little changed. Slowly but surely, consensus is catching up to the idea of a bigger, not tighter economy. The Fed's June projections will likely move further in our direction as well…

… In a nutshell, we are forecasting more slack in the economy this year and next, and we think consensus and the Fed have more room to mark to our expectations. Markets have been whipsawed this year by volatility in the data releases, making it difficult to separate signal from noise. We have a strong, well-reasoned view that the reacceleration in inflation in 1Q24 was temporary, and have laid out arguments for lower rates of core inflation ahead – starting with core CPI next week…

Wells Fargo: Why Your Overseas Vacation Is Bad News for the Economy

Summary This report revisits some classic implications of a strong dollar on various sectors of the U.S. economy with an eye toward shining a light on an under-appreciated trade factor: foreign travel…

… A final and, in our view, more balanced way to think about it: a swing in the trade of travel services of $1.1 billion would represent a roughly 5% share of the overall trade surplus in services, or a 1.5% share of the total trade balance. That is roughly equal to the 1.7% average annual change in the trade deficit over the past three years. In short, growth in foreign travel may not be enough to wildly move the needle in any given month, but over time, it has scope to be a more consequential factor for net exports than presently appreciated.

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

Risk reversal has unlimited upside and downside payouts

Inexpensive position may be a hedge or a volatility wager

… The position starts to make money if 10-year yields fall below 4.35% and to take on water if they rise above 4.58%, but profit or loss accumulates quickly beyond those levels, Bloomberg analysis shows.

The trade has several possible motivations. If linked to an underlying position in Treasury futures, it could be a cheap hedge for a rally sparked by next week’s April inflation and retail sales data. It could also be a wager on implied volatility, where an increase would lift the prices of the options. In any case, the holder of the strategy should be able to mitigate losses by making adjustments or by exiting the position if yields start to climb.

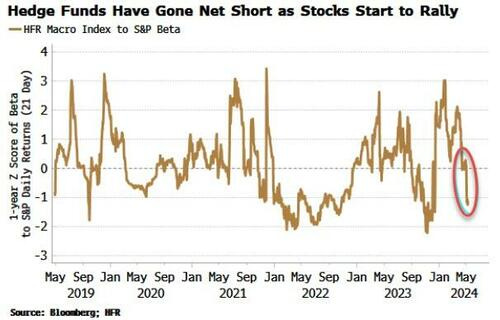

Bloomberg (via ZH): Hedge Funds That Sold In May Might Now Push Stocks To New Highs (positions lives matter)

… We can estimate how hedge funds are positioned in stocks by looking at the beta of hedge-fund indices (in this case HFR’s Macro/CTA index) to the S&P 500. As the chart below shows, it looks like funds are now short the stock market in the aggregate.

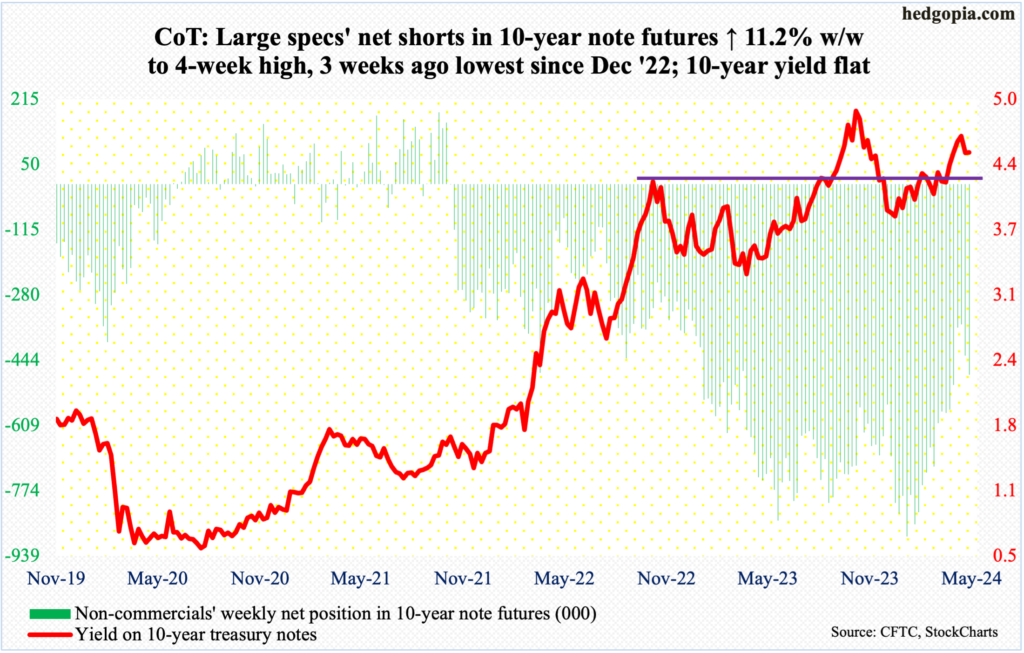

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

ZH: McDonald's Admits Consumers Are Broke With Planned Reintroduction Of $5 Meal Deal

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Fantastic work!!!!