Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

BAD (or less good) was GREAT … NFP missed, stocks went BID and bond yields dropped.

ALL is well in the world…IF you were long RISK for the trade…IF, on the other hand, you were short bonds — 2s with clues? — 2024 UPTREND certainly ‘at risk’.

Lets dive in and take a peak at what, if any, message from some of the on the runs …

2yy DAILY — sorry ‘bout switching from candles to bars BUT … close important

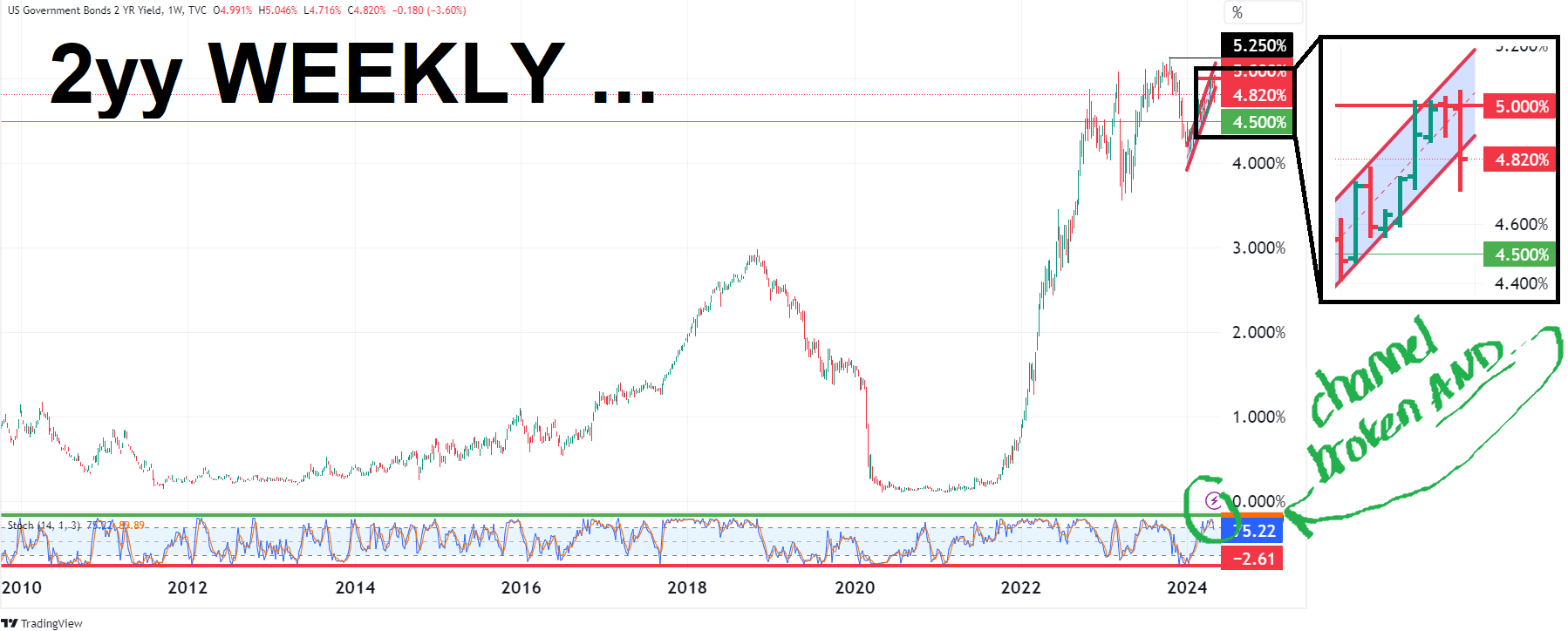

2yy WEEKLY — same story BUT perhaps a different ending (or we may just be at the beginning of this next BULLISH chapter …)

See what you want to see and Team Rate CUT certainly got some wind at their backs in to the week ahead — CPI and DURATION SUPPLY — all making front end of the curve a much / more / most interesting place to hide. I mean deploy capital.

As a friend once pointed out earlier on in my career … can’t buy / sell enough 2s on a DV01 basis to impact your bonus … um, I mean performance vs the AGG.

That said, when / if there is an interesting setup (divergence) and especially now that I’m so very far removed without need to risk life and / or limb out in the Land of the Big (DV)01s, well, I’ll just leave well enough alone…

And so, first UP lets deal with a couple / few things items from yesterday’s all important NFP report … Clearly the MARKETS are speaking loudly and with 2s closing AT < 4.82? based on my limited capabilities and per TradingView> and in context TO 2024 UPTREND — 4.865% noted HERE — well, there’s prolly little else needs to be added … BUT perhaps we’re getting some CLUES FROM 2s?

AND so, some links / recaps …

CalculatedRISK: April Employment Report: 175 thousand Jobs, 3.9% Unemployment Rate

ZH: April Payrolls Growth Unexpectedly Plunges, Biggest Miss Since 2021 As Unemployment Rate Rises

ZH: 'Buy All The Things' - Poor Payrolls Sends Rate-Cut Hopes Soaring

ZH: April Payrolls Debacle: Biggest Miss Since 2021 As Unemployment Rate Rises

ZH: ISM Services Survey Slumps In April - First Contraction Since 2022 But Prices Are Accelerating

… By days end when the data-dust and price action settled and the week now fully in our collective rear view mirror, it would appear Team Rate Cut has lots to celebrate …

ZH: Big Taper, Bad Data, & Buyback Bonanza Sparks Buying Frenzy In Bonds & Stocks

The markets took on a Dickensian dimension this week as while "it was the worst of times (for economic data), it was the best of times (for stocks)"...

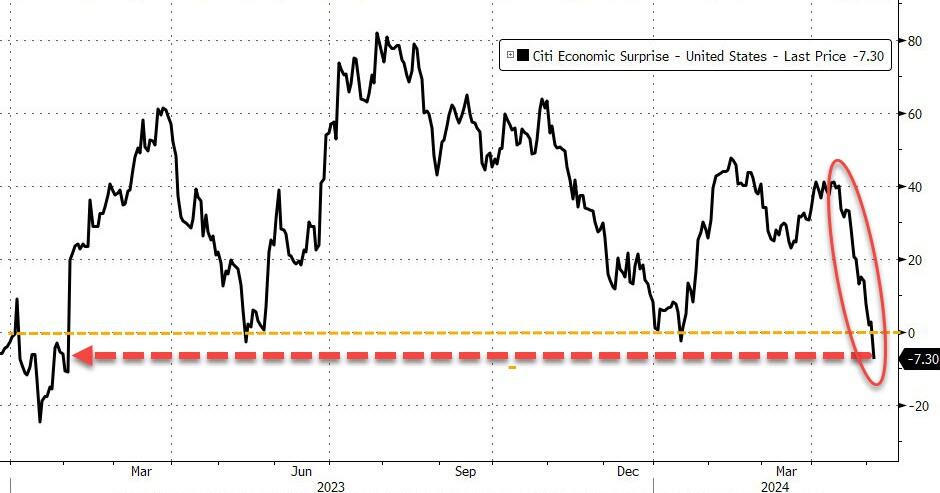

The US Macro Surprise Index continued its serial disappointment plunge into the red - the weakest since Feb 2023 (not helped at all by today's payrolls miss)...

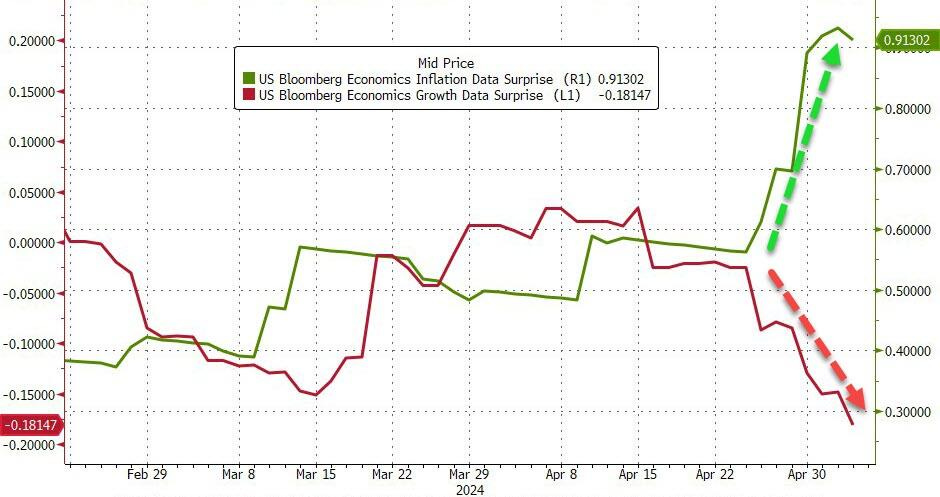

With growth data plunging while inflation data soared...

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES … some of THE VIEWS you might be able to use.

HEREyou are going to find many of the NFP recaps and victory laps we’ve all come to know and love … no matter what the data printed, we can ALWAYS count on these folks — Global Wall — to say they told us so and THIS WEEKEND is NO exception. Along with all that, a couple / few of the headlines / notes which stood out to ME …

BARCAP April employment: Gradual moderation back on course

BMO: Payrolls Disappoints - Bull Steepening Commences BMO Weekly, “A Distance to Pessimism” - booked profit long 2s, stopped OUT 2s5s flattener (small loss) and now buyer of 10s (4.60%)

Bloomberg BNP US April jobs report: Not weak enough to dissuade Fed patience

DB: Investor Positioning and Flows - Navigating Multiple Catalysts

… Buybacks return to full strength as companies exit blackout periods, while new announcements have risen massively, with the boom going well beyond the few high profile companies getting all the attention

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

AllStarCharts: Are Rates Ready to Drop? (ultimately sounds like they are watching USD)

…So far, the dollar-yen is playing its part with a little help from Tokyo.

Plus, interest rates are trending within a broader corrective wave, and momentum is posting a bearish divergence – two data points suggesting lower yields in the coming weeks.

But can we expect a more pronounced pullback that could last months?

… I can see the DXY and the 10-year yield following the same path as they did late last year, steering the markets into Q3.

If so, a weaker dollar and declining yields would produce a tailwind for the technology sector, consumer discretionary stocks, and the broader averages.

Apollo: CEOs Are More and More Bullish Despite Fed Hikes

CEO confidence continues to rebound, and there are no signs of Fed hikes weighing on how CEOs view current conditions, future business conditions, and expectations to the economy, see chart below.

In short, CEOs are becoming increasingly bullish on the outlook for their businesses and the economy. This suggests that r-star may be higher than the Fed currently thinks.

Bloomberg: Yields More Exposed To A Downside Miss In Payrolls (820a, b/4 NFP)

… 6 Conclusion We study the benefits and costs of leaning against the wind – that is, changing the conduct of monetary policy in response to a build-up of financial vulnerabilities – in a flexible, non-parametric model of the dynamic interactions between monetary policy, financial conditions, and macroeconomic outcomes. We find that downside risk to growth increases in response to a counterfactual tightening of the path of monetary policy, suggesting that LAW is detrimental even once one allows for rich nonlinearities, intertemporal dependence, and crisis predictability.

Our conclusions are subject to a number of caveats. First, we are using a reduced form model to predict the effect of changes in policy. In doing so, we are effectively assuming that a tighter path of policy is equivalent to a sequence of contractionary monetary policy “shocks”; our measure of the stance of policy is only one-dimensional, and we neglect the role of expected future policy or explicit forward guidance. Furthermore, we effectively identify the response of our variables of interest to a monetary policy shock using timing restrictions: we assume that within a period, rgapt reacts to zt , but not vice versa. This assumption is vulnerable to all the same critiques as in a linear VAR setting, especially since our system includes a financial variable (NFCI) which may respond contemporaneously to policy. Of course, in linear VAR models, the literature has considered various alternative identification approaches to circumvent this and other issues; we view our approach as a first step to studying monetary policy shocks in our rich nonlinear framework.

Second, the counterfactual exercises we conduct are subject to the usual Lucas critique. A monetary policy that systematically reacts to loose financial conditions would likely fundamentally change the relationship between monetary policy and downside risk to growth. For example, Adrian and Duarte (2018) consider the conduct of monetary policy by a central bank facing an economy in which financial conditions affect the conditional distribution of future real outcomes. In that economy, the optimal monetary policy rule always depends on financial vulnerabilities (as well as the output gap, inflation, and the natural rate), even when financial conditions themselves are not a target of monetary policy.

Finally, our estimates are subject to the usual caveats on the distinction between the effects of monetary policy surprises, realized monetary policy stance, and monetary policy rules. The overall conduct of monetary policy may affect the buildup of financial vulnerabilities through its impact on households’, firms’, and investors’ policy expectations and investment and consumption decisions made conditional on those expectations. Thus, for example, households in Grimm et al. (2023) are able to borrow more, with higher house prices, because monetary policy is systematically loose. Estimating the effect of changes in the conduct of monetary policy on the buildup of financial vulnerabilities, however, remains challenging due to the paucity of changes in the conduct of monetary policy, the simultaneous impact of an evolving regulatory environment, and the rare nature of financial crises.

… Since the trough in the unemployment rate almost exactly a year ago, the number of unemployed workers has now been increasing on an annual basis for 12 consecutive months. Going back to the 1940s, there has never previously been as prolonged a stretch of small but steady annual increase in the number of unemployed workers that did not precede or coincide with a broader recession. Perhaps the closest analogue is the mid-1980s – a period of stable but unspectacular economic performance.

After the tumult of the past half decade, a stable but unspectacular economy may well be welcome news for many firms and many workers.

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

ING: Weaker US jobs numbers boost expectations of a September rate cut

Job creation was weaker, unemployment higher and wage growth more subdued than expected in the April employment report. With Fed Chair Powell leaning dovish at Wednesday's press conference this has breathed new life into Federal Reserve interest rate cut calls

McClellan: Cattle Prices Have Outrun Grain Prices - Chart In Focus (didn’t ask BUT interesting to consider…)

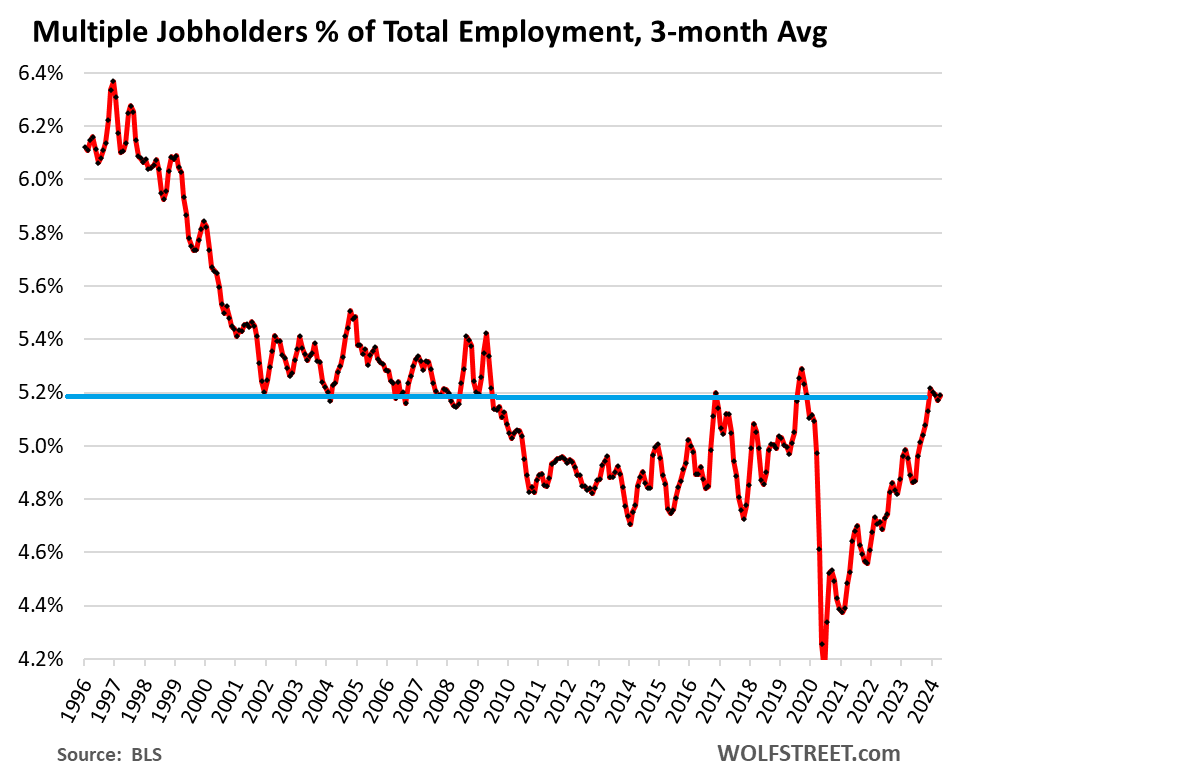

WolfST: Jobs, Wages, Mass Immigration, Full- and Part-Time Workers, Unemployment, Prime-Age Participation Rate, and Multiple Jobholders (who are they anyway?

But the undercount of mass-immigration distorts the household data.

… Who are multiple jobholders? They include: corporate employees with a side gig, such as consultant or being a landlord with some housing units (small landlords with 1-9 rentals own 11 million single-family houses for rent, so this is a biggie); university educators who also work as consultants; engineers with a startup side gig; restaurant workers with revenue-producing YouTube channels; restaurant workers working shifts at different restaurants; cops working off-duty as security; people working from home doing two full-time tech jobs before they get laid off by one of them; executives who also serve as paid member of the board at other companies…. We all know some of them. Multiple job holders span the spectrum.

WolfST: Which Industries Lost Jobs, Which Gained Jobs: Longer-Term Employment Trends in Charts

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

THAT is all for now. Lets Go NYY … quite a nice appetizer TO the fastest 2 mins in all of sport! Not a ponies guy so I’ll just be watching all the fanfare along with the masses!

Barchart: If rates remain stable over the next year, the U.S. will pay a total of $1.7 trillion in interest payments in the 12 months through April 2025.

Barchart: If rates remain stable over the next year, the U.S. will pay a total of $1.7 trillion in interest payments in the 12 months through April 2025.

Report: Biden Put Hold on US Ammo Shipment to Israel

https://www.newsmax.com/newsfront/israel-biden-ammunition/2024/05/05/id/1163544/

Biden is a man without Core Values.....other than being Re-elected and Holding on to Power...