Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP there’s really no way in my current seat I can do the move in long bonds — WEEKLY — justice. Largest gain in yields since the 1980s but it certainly continues to be worthy of consideration …

30yy: 5.00% …

… psychologically more significant than anything else I’m currently able to figure and that in mind, momentum on a WEEKLY basis here not yet suggesting the move is over OR rentable … patience, then, remains the virtue?

… as far as contextualizing the move, goes …

Fri 11 April 2025 at 4:33 pm GMT Reuters: Trading Day: A crushing week for US bonds, dollar

… This Week's Key Market Moves

30-year U.S. Treasury yield rises 47 basis points, its biggest weekly rise since April 1987.

10-year Treasury yield surges 49 bps, its biggest rise since November 2001.

The S&P 500 rises 5.7% and the Nasdaq rebounds 7.3%, their best weeks since November 2023 and November 2022, respectively.

… As far as what’s helping shape shift the price of 30yr money just above … producer prices DECREASED …

ZH: Producer Prices Plunged Most Since COVID In March

… and consumer expectations soured BIGLY …

ZH: Americans' Expectations Plunge To 45 Year Lows As Democrats Send UMich Inflation Expectations Soaring

… Alrighty, then. I’ll quit while I’m behind for now …

I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox …

Here are a couple notes from a rather large British operation … First, thinkin’ MACRO and another economic look at the holiday shortened week ahead from a

US bond market behavior has been the most worrisome part of price action this week. Until Treasuries stabilize and start to behave normally, risk assets will struggle, in our view.

A pause of reciprocal tariffs only partially contained the financial fallout, as rising Treasury yields and a weakening dollar suggest flows out of USD assets. With an escalating US-China trade war adding to global growth fears, the focus is now on negotiations and potential central bank action.

…US Outlook A bad case of the yips With market jitters intensifying amid the escalation of retaliatory tariffs with China, the administration retreated from reciprocal tariffs. An abrupt upswing in bond yields was a key catalyst, reflecting prospects of crimped foreign capital inflows and less accommodative Fed policy.

…The president's reciprocal tariff shot landed well off the fairway for markets…

… The ball remains deep in the rough after taking a drop …

… No mulligan from us – we retain our stagflationary outlook While China's high tariff rate will encourage a shift of imports away from China and toward lower-tariff trading partners, we think the current situation still implies significant stagflationary pressures within the US. Although there is scope to divert imports of final goods to other trade partners, we suspect that it is more limited for intermediates and other inputs, which can have particular specifications that can be difficult to substitute. We also think this diversion could pose logistical issues in the near term that will likely prove challenging. Beyond this, even diversion will raise costs relative to the status quo, because of new tariffs on other countries and because this almost surely involves a shift to higher-cost production. At the same time, these countries will likely be somewhat reluctant to serve as intermediaries in rerouting Chinese exports to the US, for fear of higher US tariffs. All told, we still expect to see significant cost-push pressures on inflation through year-end…

… All told, we retain our outlook for activity, including our forecast that the US will experience a recession in H2 24 amid intensified uncertainty, deterioration in household purchasing power from cost-push inflation, and retaliation against US exports. Although we do not have strong conviction about the depth of the downturn, we continue to pencil in slowing of GDP in Q1 (1.0% q/q saar) and Q2 (0.5% q/q saar), then declines of 1.5% q/q saar in Q3 and 0.5% q/q saar in Q4. We retain our 2025 outlook for inflation, with core PCE price inflation expected to top out at 3.7% q/q saar, on a Q4/Q4 basis…

…Inflation came in under par in March..

…In our view, macro tensions helped push yields into the sand trap

…am LOVIN the (Masters) golf references … just me?

In the week ahead, the market will remain on edge and wary that the next social media post could further redefine the global trade landscape. We’d like to assume that the recent flurry of tariff changes and Trump’s 90-day pause on reciprocal levies implies a period of relative calm – alas, we don’t have a great deal of confidence that a trade war reprieve is in the offing. Instead, we’re anticipating that the price action will remain choppy and the quickly changing macro narrative isn’t likely to stabilize in the near-term. For the time being, the market appears content to approach the risks from a bond bearish perspective – as evidenced by Friday’s selloff which put 10-year yields above 4.50% despite two consecutive lower-than-expected inflation reports in the form of core-CPI and core-PPI. It isn’t lost on us that March’s core-PCE pace is now tracking at a 'low' +0.1% and Treasury yields have been pushing higher, not lower as one might otherwise have assumed. The reality is that Trump’s trade war is redefining global markets in real-time and investors have shifted to a reactive posture.

Treasuries sold off despite solid sponsorship for the 10- and 30-year auctions. Moreover, Bessent even commented on the 10-year auction that, "We had a lot of foreigners show up… showing that the US is still the best place to invest." The tone as the week came to an end would suggest otherwise, and we’re wary of what the holiday-shortened week ahead holds. At issue is the extent to which Treasury bears are emboldened by the price action and seek to push 10-year yields beyond the 4.65% mid-February peak. One notable development is that the recent selloff has pushed term premium in US Treasuries higher, a nuance that suggests that once the market stabilizes, dip-buyers could use the downtrade as an opportunity to add to core duration longs. Higher term premium won’t, in and of itself, be sufficient to stabilize the clear selling bias in US Treasuries.

The market is looking toward either Trump or Powell to blink in the near-term. We’re skeptical that either the President or Fed Chair will feel compelled to take action if the market drifts sideways from here. Intervention would require a larger selloff and/or another leg lower in the equity market. In light of how dramatically the trade war between the US and China has escalated, we struggle to envision that Trump has any intention of backpedaling tariffs or offering an olive branch to Beijing for the foreseeable future – unless there is another >10% downdraft in stocks. The President appears to be in wait-and-see mode in anticipation of Beijing reaching out to make a deal. The clock is running.

Powell is in a very difficult position at the moment. The Fed has the tools to calm the market, however, using them carries the risk of stoking inflationary pressures that we know are rapidly mounting. Not only are there the fundamentals – i.e. contributing to the inflationary potential – but monetary policymakers are undoubtedly worried that by stepping in at this point, the Fed would be effectively backing a trade war that could have serious negative ramifications for the US economy. In addition, the moves have been relatively orderly – or at least the sharp swings haven’t brought in any systemic risk chatter from Fed officials. While we're retaining our medium-term constructive bias on US rates, we’re increasingly wary of the potential for another leg higher in yields in the holiday-shortened week ahead if the market isn’t satisfied by the inevitable headlines over the weekend related to bilateral trade deals or any potential de-escalation of tensions between Beijing and Washington DC…

Charts of the Week

Our first chart shows the bid-ask spread in US 30-year bonds, a basic proxy of liquidity in the long end of the curve. According to researchby the Federal Reserve Bank of New York, the bid-ask spread is a "superior tool" for assessing the liquidity of Treasuries. It can "directly quantify the costs of transacting... the bid-ask spread [measures] the cost of executing a single trade of limited size." Further, the bid-ask spread historically tends to "correlate with episodes of reported poor market liquidity in the expected manner." The pattern has held in the current episode; the bid-ask spread has widened since ‘Liberation Day’ as the tariff turmoil has worsened, but not to levels of any true concern for monetary policymakers.

Over the last week, 30-year yields reached as low as 4.30% and as high as 5.02% in the span of just three trading days. The one-week moving-average of the bid-ask spread in the long bond surged to 0.562 bp as of April 11. This is the widest since March 2023, and nearly triple the 2024 average of 0.19 bp. Using this general proxy, liquidity in the long end has certainly gotten worse amid the tariff turmoil, but it hasn't yet reached the point of being as thin as it was in March 2023 (regional banking crisis) and March 2020 (pandemic), when the average spread widened as far as 0.838 bp and 1.002 bp, respectively.

A Financial Times article featuring comments by Boston Fed President Collins made the rounds on Friday. In keeping with the chart above, "markets are continuing to function well… we’re not seeing liquidity concerns overall." More notably, "We have had to deploy quite quickly, various tools [to stabilize markets in the past]… We would absolutely be prepared to do that as needed." …

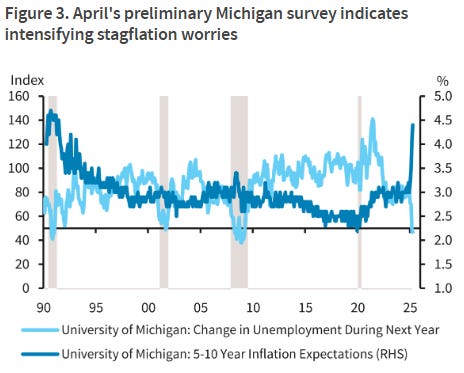

France callin’ … a note on UoMISSagain as a leading indicator …

11 Apr 2025 BNP: US: One man’s outlier is another man’s leading indicator

KEY MESSAGES

Long-term inflation expectations continue to rise sharply in the University of Michigan survey, and unusual recent asset price correlations suggest that some investors might be changing their medium-term assessment of the US economy.

Despite its insistence that inflation is well anchored, we think the FOMC is well aware that inflation expectations are rising and that it is awaiting clarity on whether these expectations will self-heal before deciding how to respond.

The FOMC appears to be trying to more evenly balance inflation and employment in formulating monetary policy, moving on from focusing primarily on employment and discounting “transitory” inflation. We think this leaves policy risks more equally balanced than many believe.

Here are a couple thoughts from rather large German institution … all sorts of nuggets here …

11 April 2025 DB: Investor Positioning and Flows - Caught Between Macro Concerns And Policy Relents

… Discretionary positioning is in the lower half of its usual range, caught waiting for the inevitable weakening in hard data that is yet to come, but mindful of a potential trade policy relent. Discretionary investor positioning is in the lower half of the usual band, clearly underweight but far from extreme (z score -0.66, 14th percentile). In the past, discretionary positioning has tracked hard data like GDP and earnings growth very closely, which is not surprising. Currently, discretionary positioning has moved lower well before any hard data has. It is already in line with a stall in GDP growth and outright modest declines in S&P 500 earnings. The reprieve this week on reciprocal tariffs saw positioning bounce a little. In our view, discretionary investors are unlikely to cut positioning too far, mindful of potential further relents…

… from a rather large German bank to one of the largest and most respected operations in the USofA …

11 April 2025 JPM: U.S. Fixed Income Markets Weekly

… Governments Treasury yields traded in a historically volatile range, with the curve bearishly steepening. Measures of term premium have moved higher, but the divergence of yields to our fair value model has been at current levels multiple times in prior years, and cross asset valuations appear fair. We think the moves this week were exacerbated by long positioning. Market depth has dropped sharply, but other liquidity metrics remain close to average levels. Following the tariff pause, we expect the Fed to resume easing in September, but retain our 2-year duration longs and 2s/5s steepeners against the backdrop of weakening growth and risks of a deeper easing cycle. We discuss the implications of foreign shedding of Treasuries on valuations. We expand our core bond fund model sample, finding active money managers are now near neutral on duration. We remain neutral on breakevens despite attractive valuations given the potential for further cheapening if tariffs remain in place…

… Treasuries The bond market has entered the chat

In a historic week for the Treasury market, the curve bearishly steepened more than 20bp and 30-year yields traversed a 70bp range, and this sort of volatility is not healthy...

...While it is hard to conclude we are in the midst of a crisis, it’s clear that investors now require more compensation to buy long-term Treasury debt with various measures of term premium moving higher. That said, the dislocation in yields from our fair value model is still below levels observed in the past and cross-asset valuations appear fair...

...We think moves this week were exaggerated by positioning metrics, with our Treasury Client Survey showing net longs near their most elevated levels. Meanwhile liquidity metrics provide a more mixed picture, but it’s hard to say that this is the sort of market that requires official intervention

Following the tariff pause we now expect the Fed to resume easing in September. Despite this delay in expected easing, alongside elevated inflation, we retain our 2-year duration longs and 2s/5s curve steepeners against the backdrop of sharply weakening growth and risks of a deeper easing cycle

Foreign investors own about 30% of marketable Treasury debt outstanding, nearly evenly split between official and private accounts. Foreign holdings are concentrated at the front end of the curve, and we estimate every $300bn decline in foreign official holdings of Treasuries would lead 5-year Treasuries to increase by 33bp …

…Thus, with investor positioning leaning historically long following the “Liberation Day” announcement this week, and concerns over the ongoing international support for the Treasury market on investors minds (see “Foreign demand and Treasury yields” below), it’s likely active investors used this week to pare back their duration overweights, contributing to the move to higher yields. Indeed, it appears that activelymanaged bond funds have reduced their duration exposure over the last week (see “Expanding our active core bond fund positioning model” below).

A couple notes from MS which are always TOP of the inbox for the week ahead … noteworthy, too, as they had been advocates of a ‘long duration’ stance and so, caught most of the move lower in yields, have shifted tone / tenor …

April 11, 2025 MS: Stay in UST Curve Steepeners, Turn Neutral Duration | US Rates Strategy

We no longer suggest investors embrace US duration after the large round trip in yields – much lower, then back to levels in place the week before "Liberation Day". We still suggest yield curve steepeners as we see them performing well in a variety of scenarios involving trade and fiscal policies.

Key takeaways

After April 2, yields fell dramatically, then rose as dramatically above our reassessment levels. We feel uncomfortable suggesting long duration again.

At the same time, the yield curve steepened just as dramatically as yields round-tripped. We continue to see a much steeper Treasury curve ahead.

The Treasury market experienced stress over the past week - particular vs. SOFR swaps, but the cash-futures basis was relatively well behaved.

We don't find enough stress in Treasury market prices to encourage Treasury to make more use of "liquidity support" buybacks than already planned.

Maintain UST 3s30s yield curve steepeners and term SOFR 1y1y vs. 5y5y steepeners as we expect the market-implied trough rate to reprice much lower.

April 11, 2025 MS: Crunch Time for Liquidity | US Rates Strategy

Significant risk reduction across broader macro markets led investors to make a dash for cash, sparking concerns about money market plumbing. Funding markets are far from true, liquidity shortage stress, but current pressures should linger with April tax collections next week; stay short SERFFJ5.

Covered wagon folk askin’ questions …

April 11, 2025 Wells Fargo: Weekly Economic & Financial Commentary

…Interest Rate Watch: What Is Going on in the Treasury Market? After an initial plunge following “Liberation Day,” longer-term Treasury yields have risen this week and are now higher than they were on April 1. What is going on in the U.S. Treasury market?

Like U.S. equity markets, the U.S. Treasury market has been incredibly volatile over the past week. The initial market reaction to President Trump's tariff announcement on April 2 was for a sharp decline in U.S. Treasury yields. On April 4, the 10-year yield finished the day around 4%, down more than 30 bps from the prior week. However, this week longer-term yields have jumped back up, and as we go to print the 10-year yield is 4.57%, which is above where it was on April 1. Some of this move may be attributed to the improvement in risk assets and general market sentiment after President Trump announced a 90-day pause on reciprocal tariffs, but we doubt that tells the whole story. What else is going on?

The culprit does not appear to be higher inflation expectations. Longer-term inflation expectations as measured by Treasury Inflation-Protected Securities (TIPS) have fallen since April 1. Interestingly, short-term inflation expectations as measured by market-based tools have increased over the same period of time. This suggests that markets are generally in agreement with the economic models that indicate the initial burst of tariff-induced inflation should not be long-lasting.

Some analysts have pointed to potential foreign selling of Treasury securities. The hypothesis suggests that some foreign investors may not want or need Treasury securities in the midst of a trade war with the United States. Data on foreign Treasury security holdings and FX reserves often comes out with a long lag, and it likely will take time before this hypothesis can be rigorously tested. That said, based on the data we do have, we are somewhat skeptical this was the main driver of the rebound in longer-term Treasury yields. The Federal Reserve holds roughly $2.9 trillion of Treasury securities in custody for foreign official and international accounts, and these holdings were roughly unchanged between April 2 and April 9 (chart).

A third possibility is an unwinding of “Treasury basis” trades. A deep dive into Treasury basis trades is beyond the scope of this short write-up, and we would encourage interested readers to learn more here. In short, Treasury basis trades typically involve buying a Treasury security, shorting a Treasury future and using leverage to amplify returns. Somewhat similar trades can exist in other structures, such as swap spreads. In times of significant market volatility, hedge funds and other basis trade investors may need to reduce their positions, a phenomenon that has led to rising Treasury yields in past episodes of market stress, such as March 2020.

Perhaps less discussed, but no less important, has been market views of the path for the federal funds rate. On April 1, fed funds futures were priced for roughly 76 bps of easing by the FOMC this year. Fast-forward to today and the market is priced for about 80 bps of rate cuts from the FOMC. The first 25 bps rate cut is not fully priced until the June FOMC meeting. Given the tremendous uncertainty and volatility over this period, the relatively small move in Fed pricing speaks to the tricky stagflationary conundrum facing monetary policymakers.

Ultimately, as financial markets eventually become less volatile in the months ahead, we expect slower economic growth and eventual rate cuts to put downward pressure on longer-term interest rates. We look for the 10-year Treasury yield to fall to 3.75% by the end of this year before rising to 4.15% by the end of 2026.

… Moving along TO a few other curated links from the intertubes, which I HOPE you’ll find useful …

Air travel as it reprsents both biz and leisure spend and clearly a(nother)feather in the cap of recession’istas, to be 100% clear …

April 12, 2025 Apollo: Arrivals at Top 10 US Airports Slowing

Daily data of the number of arrivals at the top 10 airports in the US has shown a rapid decline since late February, see chart below. This is likely a mix of declines in business travel, tourism, and government travel.

AND I always believe everything I read on the intertubes and have been talking with many folks about the worst week for long bonds since 1980s … here’s a couple relevant tweets for those — like myself — who are merely on the sidelines lookin in at those IN the game …

at MikeZaccardi

TLT’s 3rd-worst week this century. But easily record volume.

Apr 11, 2025 WolfST: PPI Pushed into Negative by Dropping Prices of Many Goods and Services

The Producer Price Index is where tariffs will show up first, whether or not companies can pass on those cost increases.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,