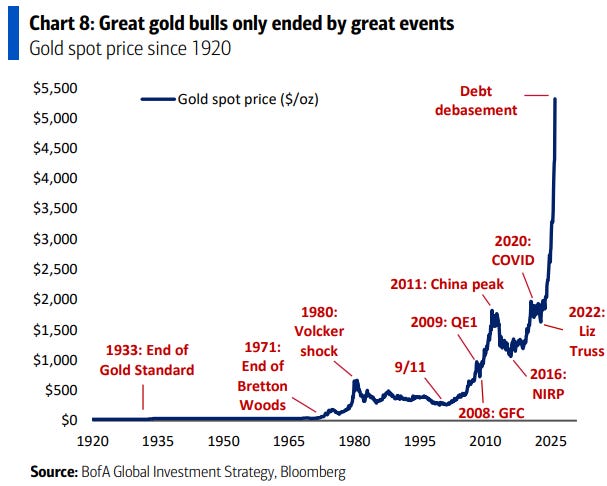

weekly observations (02.02.26): "Warsh and Peace"; #GotBONDS?; 10s coiling (ahead of bearish break?); welcome back, Kev; WEAK USD ok for USTs?

Jan 31, 2026

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note …

So many moving parts of the week that just was. Metals mayhem. A Fed that passed on cuts (surprising nobody, per CME FedWatch, currently showing large probability of an UNCH Fed rate until the JUNE meeting, where things start to get more nuanced and interesting). An official shadow Fed chair has won the beauty contest and now all things rest in his hands.

Folks love him or they hate him. I’m indifferent and don’t have as informed a view as all the pundits … Seems to me those who hate him think he won’t cut enough or fast enough and I’d push back on that as it’s NOT the job of the Fed to place bets with polymarket or kalshi on economic outcomes or levels of FedFunds (or snow in NYC, for that matter). Unfortunately, the INSTITUTION is to be independent, slow moving (by design) and currently has a dual mandate.

At the end of the day, haters gonna hate — here’s something for all the haters …

…The opening tape fit that inflation hawk narrative. Long-end yields moved higher. Equities declined, led by rate-sensitive sectors. Gold sold off sharply as real yields rose and the dollar firmed.

That’s the consensus reaction. It’s also shallow…

… He is not pursuing tight policy as an objective. He is pushing back on QE and asset-price management because they distort capital allocation and suppress productive investment. Wall Street calls that hawkish because it conflicts with a demand-stimulus, balance-sheet-first framework, not because it implies permanently restrictive rates…

…Trump did not select Warsh to shut down growth, and Bessent knows his record well. Claims that they were duped are lazy. They selected him to normalize policy without destabilizing a high-debt, dollar-centric system. The front end is already trading that distinction, even if the headlines are not.

Shallow. We’re all going to become experts now on Warsh and what he’s gonna do. We’re going to be told by those who know they know.

Fact of the matter is, it’s a far better choice than, say, the other Kevin, but who are we kidding? Whoever is in that seat has to be able to develop a consensus based on all the best information at that time.

Lets wait and hold judgement and see IF he’s confirmed (lot of moving parts there) and also how the data develops. Think BIGGER than the current and now known, shadow chair …

On THAT note, Gundlach was on CNBC after the FOMC, before WARSH was a thing … it’s worth a look / listen and I’m grateful for a reader — thank you, Steve — for having pointed this one out …

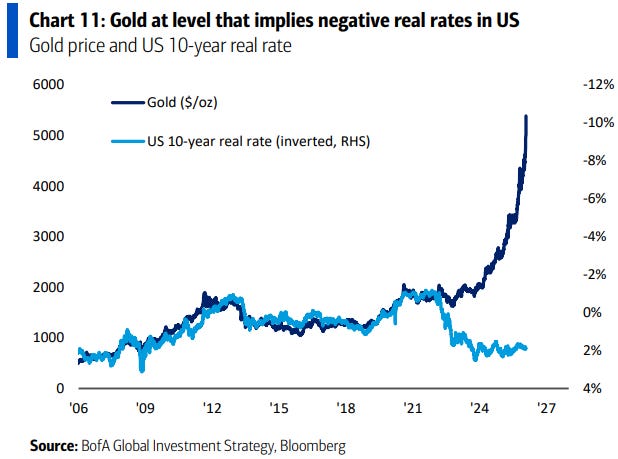

Jeff talks 2s on top of FF (so the front-end of the market ‘gets the joke’), talks REAL assets and GOLD price being the inverse of confidence in CBs. See BAML visuals below. Gundlach doesn’t necessarily like the longer end BUT if you stick with this short FOMC recap / victory lap, you’ll note some interesting commentary on how he hasn’t changed his bearish view of the longer-end BUT it’s what he’s thinking about, and why he MIGHT, leads me to follow the bond king and investing legend, Gundlach, with a mediocre view of bonds … Long bonds …

30yy WEEKLY: triangulating, flagging … where support up nearer 4.65 and resistance is down ‘round 4.00% …

… as momentum becomes stretched, overSOLD and appearing to have rolled over and cross bullishly favoring LOWER RATES …

#GotBONDS?

Tale of a couple markets or, should I say, timeframes … if you look at rates Friday, it would seem that nothing much happened further out the curve BUT there was noticeable BID for 2s.

If you look at structure of the curve and on a more broad, WEEKLY, view, it would seem to me that in the week just passed, well, rates were HIGHER and so, a vote of little / no confidence.

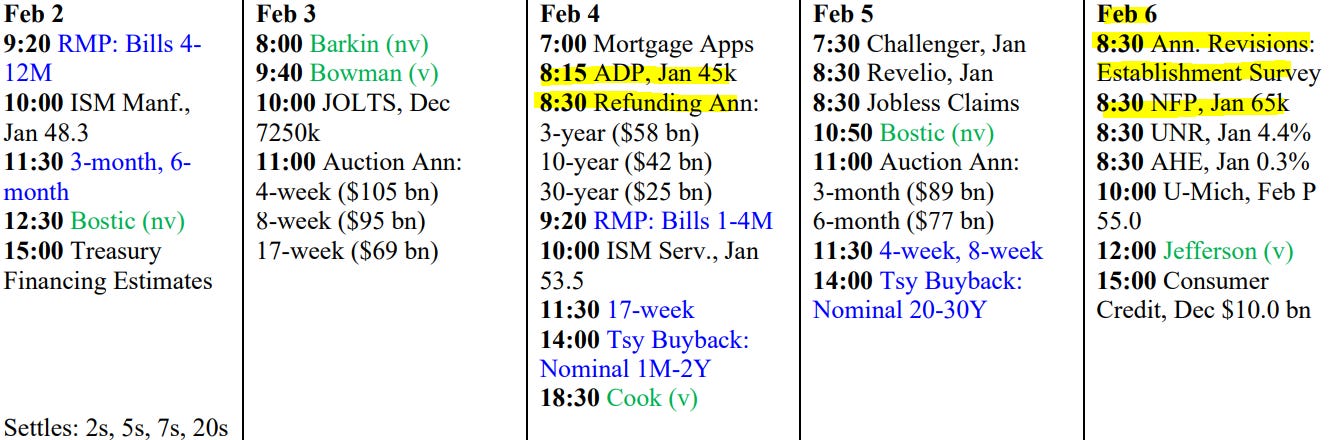

The week ahead there will be more data for our consumption. In as far as the day which just passed … for the incoming Fed (and the outgoing) …

ZH: US Producer Prices Unexpectedly Surged In December

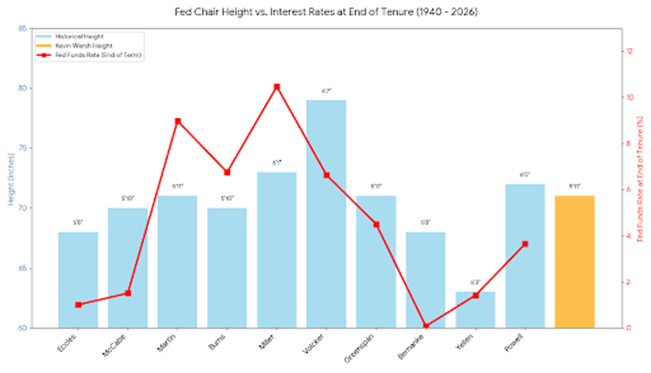

… I’ll continue to think ‘bout Warsh and currently have lots of space on the wall of shame so PLEASE reach out let me know if / when Kev’s spotted on cover of Time …

… … askin’ for a friend. Thanks …

… I’ll move on TO some of Global Walls narratives I’m still blessed to stumble upon one way or another. These are SOME of THE VIEWS you might be able to use … some of the ‘usual suspects’ with lots of WARSH notes sprinkled in …

From THE bank of our great land … a few more bearish TECHNICAL thoughts …

The View: US refunding and labor market in focus Trump to announce his Fed chair pick this morning; Warsh odds across prediction markets increased above 85%. We expect ECB and BoE to hold, RBA to hike, and no coupon changes at refunding. We are long EUR front end, in SONIA flatteners, sell terminal pricing in AUD, and long UST 20y on the fly as a hedge to refunding surprises.

Rates: Forest thru the freeze US: Any initial financial condition tightening on Fed chair decision should be faded; FX impact on rates limited for now. Core views: receive belly nominal & reals, steeper 5s30s, long spreads…

…Technicals: US 10Y yield coiling ahead of upside breakout US 10Y yield is rising in Q1, but it stalled this week between 4.20-4.27%. We anticipate a breakout higher toward 4.40% provided it remains above 4.13-4.15%.

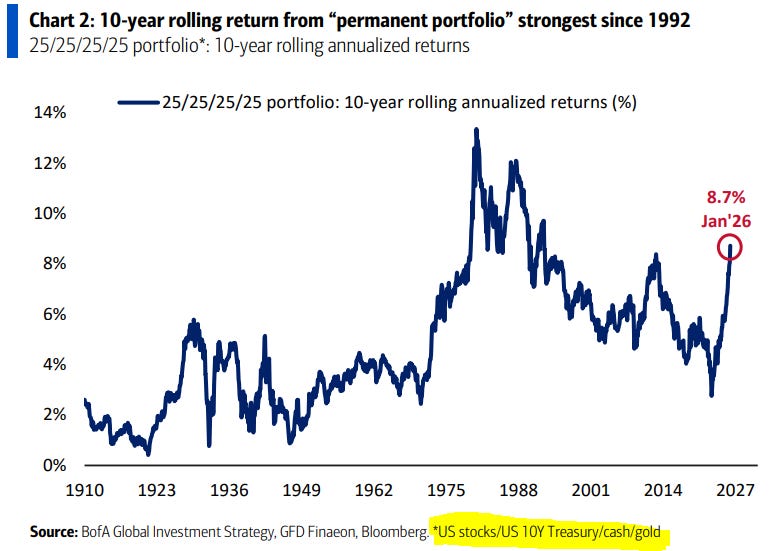

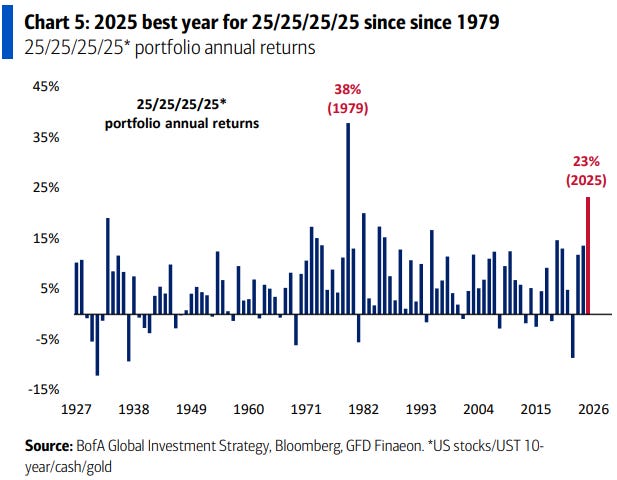

…The Biggest Picture: 10-year return from 25/25/25/25 stocks/bonds/gold/cash “permanent portfolio” = 8.7% (best since 1992 - Chart 2), follows 23% gain in ’25 (best year since 1979 – Chart 5); long gold was contrarian “pain trade” in 2020 for secular asset allocators…in 2026 it’s long bonds.

Large recent swings in the USD reflect hedging over geopolitical concerns, speculation over JPY-related intervention, and mixed communication from the US administration, including a new Fed chair nomination. The USD will remain in focus, alongside payrolls, the ECB, the BoE and Japan's election.

…US Outlook It’s Warsh We do not expect the transition to Kevin Warsh as Fed chair to alter monetary policy meaningfully this year, with the resilient economy, elevated inflation, and a divided FOMC limiting scope for easing. Revisions in next week’s payroll report should underscore that slow job growth is the new norm.

The president nominated Kevin Warsh to be the new chair of the Fed’s Board of Governors. Despite temporary roadblocks in the Senate, we expect him to be confirmed by May 15, the end of Powell’s term. In our view, attempts to forge consensus behind further policy easing will face resistance – both within the divided FOMC and given tension with Warsh’s own inclinations.

Although portions of the federal government face a Congressional funding deadline on January 30, any shutdown is shaping up to be partial and brief, with little disruption to economic data. This includes next week’s payroll report, where we expect another decline in the unemployment rate, despite benchmark revisions showing a prolonged slowdown in net hiring.

Data remain resilient and are consistent with a pickup in inflationary pressures at the turn of the year. Incoming November data on trade and factory orders helped narrow the shortfall between our Q4 growth tracker (1.9% q/q saar) and GDPNow (4.2%), with the latter likely overstated by shutdown-related effects. We are tracking December core PCE inflation at 0.4% m/m (3.0% y/y).

….Warsh probably still a hawk

…Communication likely to change

…Powell now more likely to step down as governor

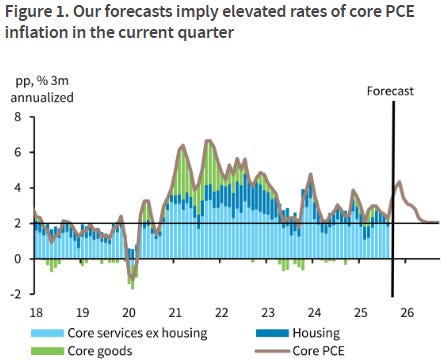

…The Fed will be weighing a firm December PCE price inflation print December PPI estimates looked firm, led partly by trade margins, a notoriously volatile category. Core goods PPI rose modestly from November, while core services PPI accelerated materially, to 0.7% m/m (+0.7pp). The services subcategory excluding trade, transportation and warehousing, which carries inputs for the PCE price index, also firmed. After folding in the PPI estimates, our core PCE forecast stands at 0.40% m/m (3.0% y/y), an elevated print following a run of subdued readings. This would imply Q4/Q4 core PCE for 2025 at 2.8%, 0.2pp below the Fed’s December projection in its SEP. We continue to anticipate higher inflation pressures in the coming few months (Figure 1), partly due to more tariff pass-through and partly from a payback to the PCE price index from missing October data. Altogether, we forecast Q4/Q4 core PCE at 2.8% in 2026, essentially unchanged from 2025.

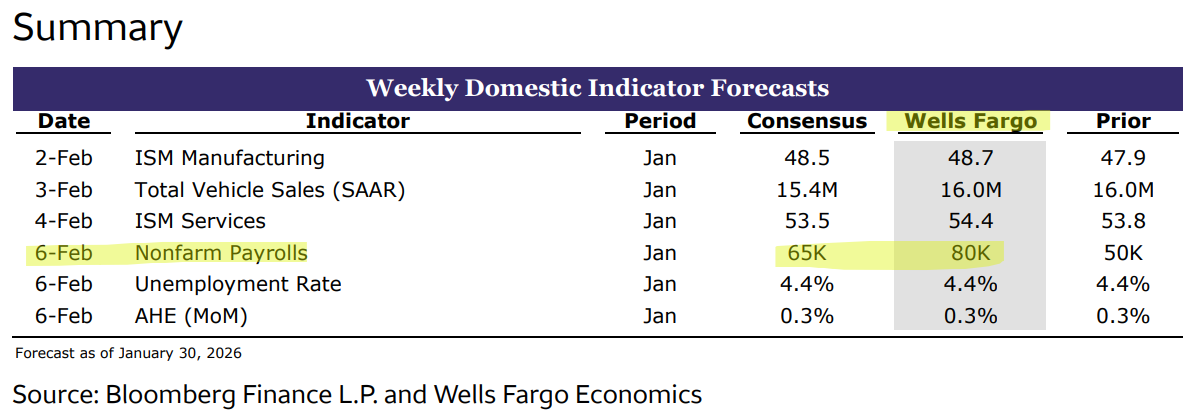

…We expect payroll estimates to show more of the same for job gains Next week’s highlight will be the latest employment situation report, which will include the incoming January estimates, as well as the 2025 benchmark revision. As we discuss in our preview, we expect January’s estimates to show gains in a overall and private nonfarm payroll employment of 50k, in line with December’s pace and the 3mma of private payroll gains during H2 25. In the household survey, we expect the unemployment rate to tick down to 4.3%, 0.2pp lower than its shutdown-distorted peak during November’s reference week.

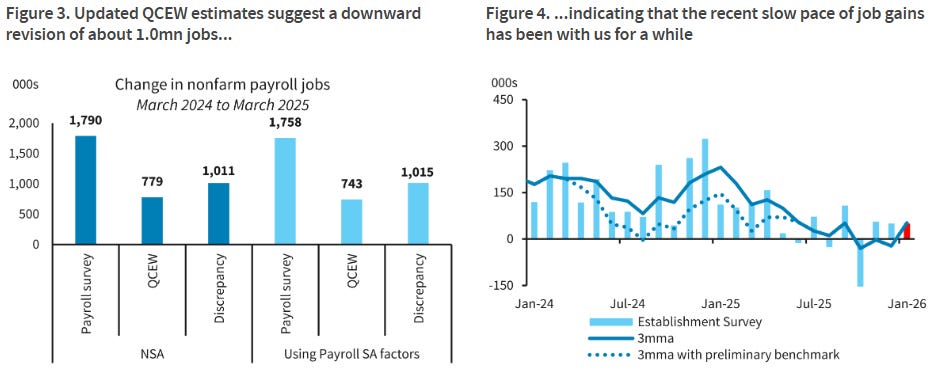

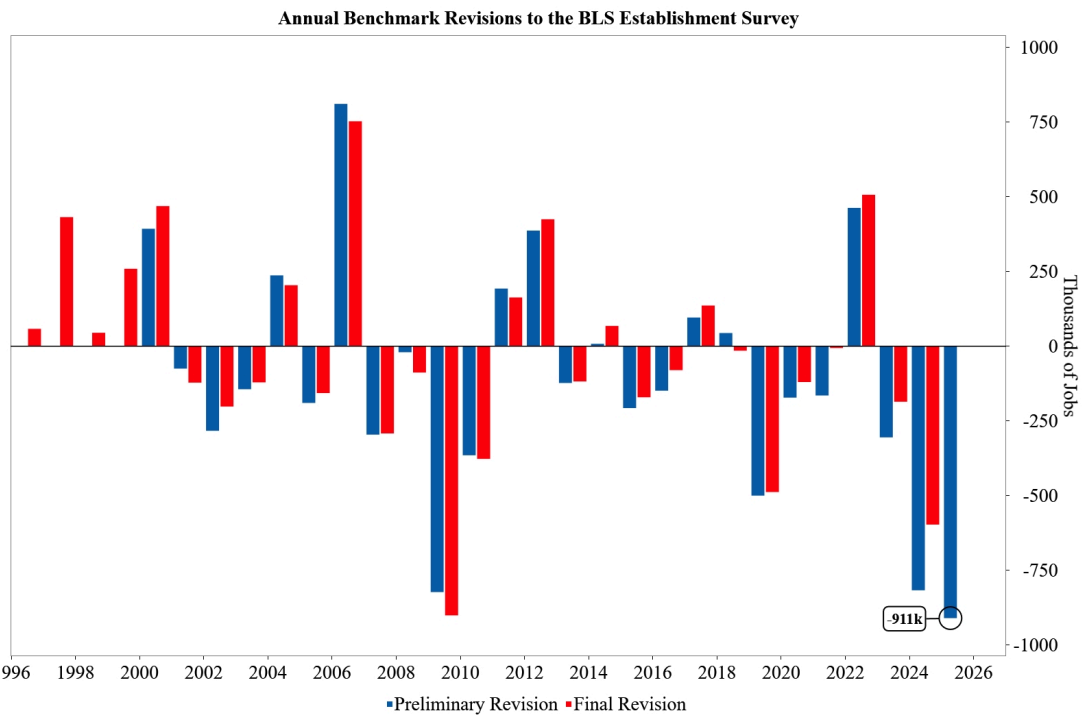

The latest jobs data will also factor in benchmark revisions and a methodological tweak This report will also feature the BLS’s usual benchmark revision, which will align the level of employment in March 2025 with the near-census counts from the Quarterly Census of Employment and Wages (QCEW). The BLS’s preliminary benchmark revision announcement in September suggested that the level of nonfarm payroll employment in March 2025 would be reduced by 911k, trimming average monthly gains from April 2024 to March 2025 by ~75k/m. Updated QCEW counts, which were released in December, suggest that the downward revision could, plausibly, be as large as 1.0mn (Figure 3). Anyway you slice it, the numbers will show that the job gains have been running at slow levels for quite some time now, beginning in mid-2024 (Figure 4).

With this release, the BLS will also update its estimates for April-December 2025, incorporating earlier updates of the birth-death adjustments to account for new QCEW information through Q2 25. Starting with the January estimates, it will also be amending its monthly birth-death adjustment methodology to incorporate more up-to-date information about employment gains from its establishment survey sample, under the (plausible) premise that job growth in the sampled firms is correlated with unobserved job gains from establishment births and deaths. Statistical work by the BLS following the Global Financial Crisis showed that this modification would have improved the real-time accuracy of the jobs numbers, albeit moderately. In principle, revisions to prior birth-death adjustments could be meaningfully downward, though we lack confidence to assess the magnitudes in question…

Brakout comin’ …? Staying SHORT 10s (tgt 4.35, stop 4.11), top of range still needing to be defined … alternatively, looking at BELLY (5s) vs wings (2s10s)

In the week ahead, investors face several key event risks as the market struggles to determine the next 15 bp in 10-year yields. Typical seasonal patterns suggest that higher yields should be the path of least resistance in the near-term, and as such, we’re open to renewed selling pressure that will steepen the yield curve. Powell’s message was clear – decisions will be made on a meeting-by-meeting basis and reflect the evolution of the economic data. Even with two dissents (Miran and Waller), the decision to keep rates steady offered investors evidence that Fed independence has weathered the President’s relentless critiques. Trump has announced that Kevin Warsh is the official nomination for the next Fed Chair, leaving Monday’s Punxsutawney Phil spring forecast as the next focal point for the betting markets. Warsh is a solid selection for Fed credibility, and while he’s viewed as less likely to use the Fed’s balance sheet to influence longer-dated Treasury yields, he will unquestionably be heading back to Eccles building with orders to lower policy rates. We maintain that the degree to which he’s able to deliver will be as much about the performance of the real economy as it will be his ability to build consensus and persuade the other FOMC members…

…Let us not forget that Friday is the scheduled release of the January payrolls report – which includes the BLS benchmark revisions. The market will use the employment update to further refine expectations for a March rate cut. Currently, the market-implied odds of a March rate cut are steady at 15%, which strikes us as a bit low given that the FOMC will have two additional payrolls reports before its next decision. It’s difficult to envision that there won’t be evidence of some economic headwinds in the interim that at least brings the odds to 1 in 4, even as the current sentiment toward the Fed is that wait-and-see truly translates into wait-and-wait.

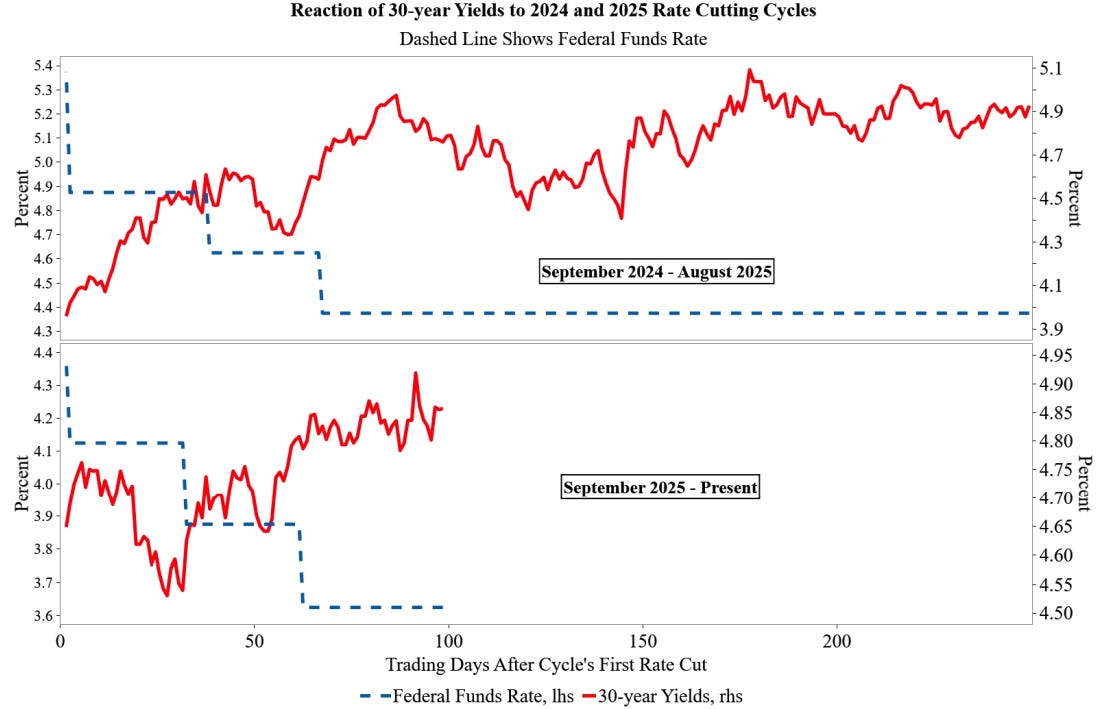

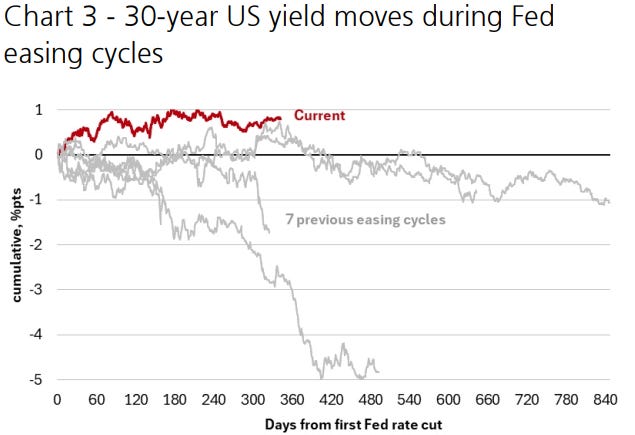

Charts of the Week Our first chart plots the reaction of 30-year yields to the 100 bp of rate cuts delivered by the Fed in 2024 (top pane), and to the 75 bp of rate cuts delivered in 2025 (bottom pane). In the twelve months following the start of the 2024 rate-cutting series on September 18, 30-year yields rose by as much as 120 bp. To put a finer point on it, 30-year rates went into the first cut of the cycle in September 2024 at 3.95% and, after 100 bp of cumulative cuts in 2H24, reached as high as 5.15% in 1H25.

After a period on-hold, on September 17, 2025, the Fed commenced another series of three consecutive rates cuts. 30-year yields went into the September 2025 cutting series at 4.65% and, after 75 bp of cumulative cuts, long bond rates have (thus far) risen by as much as 30 bp – as a 4-handle has been retained. Clearly, the long bond has been biased toward higher yields despite the 175 bp of rate cuts delivered by the Fed over the course of the normalization cycle. The reality is that moving toward a less restrictive policy stance implies upside risk for future inflation – putting upward pressure on longer-dated TIPS breakevens and term premium.

Our second chart plots the history of the preliminary and final benchmark revisions to the BLS establishment survey. Recall that the upcoming payrolls report will be accompanied by the final annual benchmark revisions to total nonfarm employment for the year ending March 2025. Recall that in September, the preliminary benchmark payrolls revision subtracted -911k from jobs growth for the 12-month period of April 2024 to March 2025. Framed differently, the revisions reduced the monthly payrolls prints in the reference period by an average of -76k per month.

Note that the final annual revision has come in higher than the preliminary one in all but one year since 2012. Moreover, over the last five years, the final revision has come in 119k higher than the preliminary one, on average. While we're looking for the upcoming final revision to once again be higher (less negative) than the preliminary estimate of -911k,we expect Friday's update to reinforce the assumption that monthly jobs growth has been meaningfully overstated by the BLS in recent years.

Unsurprisingly, Waller cited the looming downward revisions to 2025 jobs data when explaining his decision to dissent in favor of a rate cut at the last Fed meeting. Specifically, the Fed Governor said, "last year's data will be revised downward soon to likely show that there was virtually no growth in payroll employment in 2025. Zero. Zip. Nada."

Welcome back …

30 Jan 2026 18:52 GMT BNP US Fed: Welcome back, Kevin Warsh

KEY MESSAGES

We believe Kevin Warsh is committed to 2% inflation over time and to maintaining the Fed’s institutional credibility. His nomination to lead the central bank seems entirely consistent with our optimistic outlook for US economic growth over the coming years.

Regardless of who leads the Fed, we expect monetary policy to be determined by the economic outlook and by the Fed’s existing policy goals and framework. Given our outlook for robust growth and sticky inflation, we anticipate no rate cuts this year.

We perceive room for eventual agreement at the Fed on reducing the size of its balance sheet and moving it to a Treasury-only portfolio. However, these changes will probably take some time to implement.

A twist-steepening of the UST curve based on Warsh’s past comments makes sense to us for now, and a focus on AI-driven productivity and disinflation may further boost steepener trades. We continue to suggest 1s30s steepeners.

We expect a steady 4.4% unemployment rate in the US January jobs report, while nonfarm payrolls rise a solid 105k.

We continue to take a glass-half-full view of the job market alongside an above-consensus outlook on near-term economic growth.

The large downward benchmark revision to nonfarm payrolls seems unlikely to materially alter the Fed’s thinking on policy, with the unemployment rate still the key guide.

This next group of notes from a large German bank who’s writing about WARSH in various capacities …

30 January 2026 DB Fed Notes - What Warsh could mean for the Fed

This morning President Trump announced Kevin Warsh as his nominee to replace Jay Powell as Chair of the Federal Reserve. We build on a prior note to discuss what his nomination could mean for the Fed….

…Warsh’s Fed critiques During recent years he has been particularly critical of the Federal Reserve. His criticisms span short-term policy decisions – for example, continuing QT and rate hikes in late 2018 despite shaky markets and the 50bp reduction last September – as well as longer-term considerations for the central bank, which he outlined in a speech this year at an IMF lecture hosted by the G30 (see here).

Warsh has been consistently critical of the Fed’s active use of its balance sheet over the past ~15 years. This has earned him the label of a “hawk”, at least with respect to the Fed’s balance sheet. Although he supported the Fed’s initial foray into QE in response to the GFC, he cautioned that later programs were not appropriate, possibly raising inflation and financial stability risks, as well as moving the Fed away from its core duties and into credit allocation policies that could distort market signals. As he noted recently, “I worried mightily in the summer and fall of 2010-- a time of strong growth and financial stability –that the decision to buy more treasury bonds—would involve the Fed in the messy political business of fiscal policy. QE2 was announced. I disagreed with the decision, and resigned from the Fed soon after.”

While Warsh spoke out against QE2 at the November 2010 meeting (see transcript here), he ultimately did not dissent. At the time, he argued that he preferred to show consensus and support for Chair Bernanke’s decision to undertake another QE program – Warsh did not want to undermine the effectiveness of that program by publicly showing disagreement on the Committee.

Warsh has further argued that the Fed’s active use of its balance sheet may have brought about a period of “monetary dominance”. By artificially depressing rates for extended periods, Warsh argues the Fed has played an important role in enabling US government debt accumulation. This contrasts with the usual concerns around “fiscal dominance”, in which elevated debt levels make it difficult for the central bank to raise rates by increasing the debt service burden of the federal government.

Beyond the balance sheet, Warsh has levied a variety of criticisms on the Fed. For example, he argues that the Fed has been consistently too data dependent and not forward looking enough. At the same time, Warsh has been critical of the Fed’s regular use of forward guidance. He recently noted, “forward-guidance – a tool rolled out to great fanfare in the financial crisis—has little role to play in normal times.”

He also questioned various other aspects of how the Fed has set and/or justified monetary policy. Warsh has argued the Fed incorrectly believes: “monetary policy had nothing to do with money”, “black-box DSGE models were anchored in reality”, and “the surge of Putin and the pandemic were blameworthy for inflation rather than the surge of government spending and printing.” These criticisms imply that Warsh wants to put more focus on the Fed’s balance sheet size and money supply in the conduct of monetary policy and could also be open to overhauling the Fed research staff.

Finally, while he has described Fed independence as a “worthy” cause, he has also argued that the Fed has brought upon itself questions about independence. Warsh noted, “the Fed’s outsized role and underperformance have weakened the important and worthy case for monetary policy independence.” Further, Warsh denounced mission creep at the Fed, including considering issues related to climate and inclusion…

30 January 2026 DB: Warsh and the Fed balance sheet

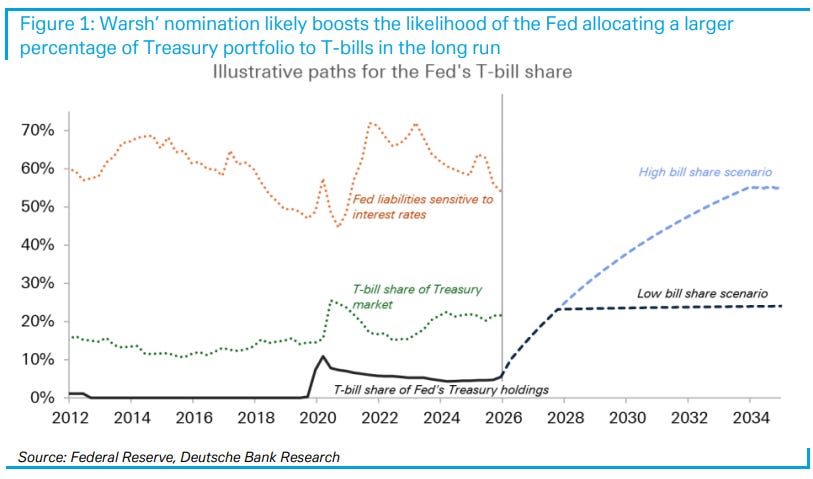

To help consider what a Warsh-led Fed could mean for the Fed’s balance sheet and its footprint in the Treasury market, we revisit a chart from November that outlines two potential paths for the Fed’s T-bill allocations…

…At first blush, the Fed confining its purchases to T-bills appears bearish for rates. However, the impact is less straightforward as it will depend on Treasury’s issuance response. If Treasury matches the Fed’s demand through increased bill issuance, less supply would then be needed further out the curve, offsetting the bearish bias in Fed purchases. However, until the Fed decides on the long-term composition of its holdings and lays out a clear plan on how it will get there, Treasury is also unlikely to respond decisively, leaving the future supply picture uncertain. In that context, a timely decision and clear communications from the Fed could prove more important than the decision itself.

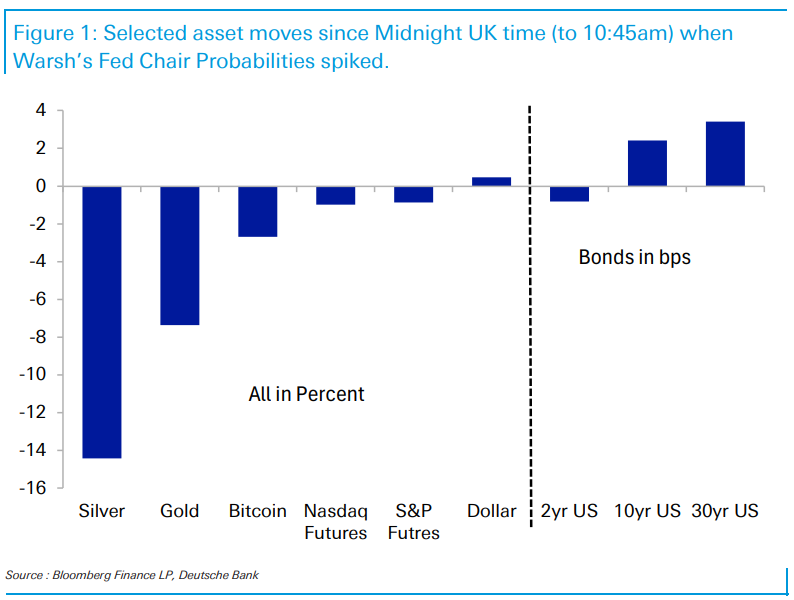

At around midnight UK time last night, the news broke that the Trump Administration would announce its nomination to lead the Fed this morning. Shortly afterwards, Kevin Warsh’s Polymarket odds began to spike and now sit well above 90%.

Today’s Chart of the Day shows how markets have reacted since midnight in the UK…

…There is still one outstanding question however. Any new Fed Chair requires Senate confirmation, and Republican Senator Thom Tillis (who sits on the Senate Banking Committee) has vowed to block any Fed nominees until the Justice Department resolves the current investigation into the Fed’s renovation. Tillis reiterated that yesterday, saying “DOJ’s got to decide when I lift those holds. It gets lifted the day that case is adjudicated or withdrawn”, and Senate Majority Leader Thune said “probably not”, when asked if a nominee could be confirmed without Tillis. So one to keep an eye on in the days ahead.

By the time you read this, prices in the chart will probably have moved again — but the market has clearly entered “new Fed Chair” mode. If it is Warsh, Matt’s primer is the quickest way to get up to speed and avoid wading through the inevitable chapter-and-verse on him… the kind that could give War and Peace a run for its money.

30 January 2026 DB: What you need to know for the week ahead

…Our forecasts for headline (+75k forecast vs. +50k previously) and private (+75k vs. +37k) payrolls reflect a mild uptick in the pace of net job gains relative to their three-month and six-month averages. If our forecasts prove close to the mark, we expect the unemployment rate to remain unchanged at 4.4%. Regarding other details of the report, we anticipate average hourly earnings growth (0.3% vs. 0.3%) as well as hours worked (34.2hrs) to both remain steady. The upshot of our establishment survey forecasts would be a slight uptick in the year-over-year growth rate of our payroll proxy for nominal compensation (4.5% vs. 4.3%).

It is important to remember that while the BLS will incorporate its usual annual benchmark revisions to the establishment survey, the adjustment to the population controls for the household survey has been pushed back to next month. Regarding the establishment survey revisions, recall that the preliminary benchmark revision of -911k (0.6%) to the level of March 2025 employment (for private employment the preliminary benchmark was -880k) was one of the largest on record. In addition to the typical re-estimations of the seasonal factors, the establishment survey will change the birth-death model by incorporating current sample information each month – a more frequent adjustment than the prior quarterly updates. It is impossible to determine exactly how the new higher-frequency adjustments to the birth-death model may impact the recent trends in the data. However, the purpose of moving to a higher frequency update to the birth-death model is to dampen the magnitude of revisions. That being said, January is typically the largest net job loss month each year on a non-seasonally adjusted basis, thus even a small change to the birth-death model could have a noticeable impact on reported seasonally-adjusted hiring.

Finally, we would point out that the final benchmark typically differs from the preliminary estimate because the QCEW survey – the basis for benchmark revision – is also often revised. Case in point was the 2024 final benchmark of -589k (-0.4%), which ultimately proved modestly less negative than the preliminary 2024 estimate of -818k (-0.5%). In short, risks around our January employment forecasts are elevated and market participants will need to monitor not only the headlines, but the potential impact (if any) of a higher frequency birth-death model adjustment as well as potential revisions to the preliminary benchmark…

…In summary, this week’s labor market data will be the starting point for debate between the hawks and doves on the Committee. While we continue to expect the Fed to remain on hold until Q3, any meaningful upside or downside surprises will undoubtedly impact market expectations for how long the Fed may stay on the sidelines.

THIS IS FINE …

30 January 2026 ING THINK Ahead: When a good place turns bad

Central banks from Washington to Frankfurt are telling us they're in a good place. And they have a point, even if that seems wildly at odds with *gestures at everything going on in the world*. Read on for James Smith's look at what could drag policymakers out of their happy place this year as the team looks ahead to another big week in markets …

…THINK Ahead in developed markets United States (James Knightley)

Labour market: A key takeaway from the 28 January FOMC meeting was the Federal Reserve sounding a little more upbeat on the jobs market. It removed the line that “downside risks to employment rose in recent months” while suggesting that there have been “some signs of stabilisation” in the unemployment rate. While the unemployment rate did dip lower in December, the jobs story in general doesn’t look particularly robust to us, nor to the market.

NFP (Fri): While we are not seeing much on the firing front, hiring remains lacklustre. Outside of government, leisure & hospitality and private education & healthcare services, the US has lost jobs in seven of the past eight months, and we suspect we will see a similar outcome for January when the report is published next Friday. Indeed, the market remains wary of what is happening in the jobs market and was unmoved by the Fed’s positive spin, continuing to price two 25bp rate cuts this year…

Jamie Dimon’s group on … things …

30 January 2026 JPM U.S. Fixed Income Markets Weekly

Cross Sector President Trump nominated Kevin Warsh to be the next Fed Chair. We look for the Fed to remain on hold for the rest of the year. Though the bar to restart QT is high, the Fed may opt for incremental steps to gradually reduce its balance sheet. We forecast a 75k gain in nonfarm payrolls and a 4.4% unemployment rate in January. Hold 5s/20s steepeners. Initiate 10s/30s maturity matched swap spread curve flatteners. We turn tactically neutral on short expiry volatility. In MBS, we continue to prefer the wings of the stack. We lean bearish on HG credit going into February. A look at bond fund flows data suggests limited selling of US fixed income.

Governments Fed chair nominee Kevin Warsh’s recent speeches indicate his policy rate view has shifted in a dovish direction, and we suspect he will at least initially advocate for easier policy, anchoring the front end. Warsh has consistently pushed back against the Fed’s balance sheet expansion; while the bar for restarting QT is very high, his confirmation could renew the Fed’s focus on the SRP, and rekindle the debate about the composition of Fed holdings, biasing the curve steeper on the margin. With growth expectations firming, front-end yields trading near local highs, and the broad curve flatter than local peaks, we hold 5s/20s steepeners, which offer a favorable carry profile versus outright longs and should outperform if Treasury disappoints versus expectations of more activist policies at next week’s refunding. With 2-year Treasury FRN DMs already too narrow to fair value, we expect DMs can widen modestly from here. Though breakevens remain cheap to our fair value model, many of the recent tailwinds that have recently supported breakeven performance are likely to fade or reverse over coming weeks, and we prefer to remain tactically neutral on breakevens at current levels…

…Treasuries Should we talk about the weather? Should we talk about the government?

Fed chair nominee Warsh’s recent speeches indicate his more monetarist approach to inflation remains ingrained, though his policy rate view has shifted in a dovish direction over the last year, and we suspect he will advocate for easier policy at least early on, leaving the front end well anchored

At the long end, Warsh has consistently pushed back against the Fed’s QE programs. While the bar for restarting QT is very high, his confirmation could renew the Fed’s focus on both increasing the efficacy of the SRP and reducing its stigma, alongside rekindling the debate about the composition of Fed holdings, biasing the curve steeper on the margin

With growth expectations firming, front-end yields trading near their highest levels since last summer, and the broad curve flatter than local peaks, we continue to recommend tactical steepening exposure, which offer a somewhat better carry profile than outright longs and should outperform if Treasury disappoints versus expectations of more activist policies at next week’s refunding

...Additionally, fiscal concerns in Japan should persist ahead of the election on February 8, which is likely to pressure long-end JGB yields higher near-term, likely helping the Treasury curve steeper. Hold 5s/20s steepeners

With 2-year Treasury FRN DMs already too narrow to fair value, we expect DMs can widen modestly as we see limited scope for further steepening in forward Fed expectations over the near-term and as positive net T-bill supply in February could place nearterm pressure on funding conditions

…At the long end, Warsh has consistently pushed back against the Fed’s balance sheet expansion, arguing in his G30 lecture at last spring’s IMF meetings that successive QE programs have led to the misallocation of capital and risks of bigger shocks in the future. Similar to the policy rate, a shift in balance sheet strategy would require a change to the Fed’s monetary policy framework; thus, the bar for restarting QT is very high. Nevertheless, his confirmation could renew the Fed’s focus on both increasing the efficacy of the SRP and reducing its stigma, which may allow banks to hold somewhat fewer reserves than they do now. Moreover, it could rekindle the debate over the composition of the Fed’s holdings and whether it should take a more aggressive approach to shortening the duration of its SOMA holdings. Governors Bowman and Waller, alongside Dallas Fed President Logan, have supported a SOMA with a shorter duration profile (see Good enough for government work, 11/22/24). On margin, this does bias the curve marginally steeper, particularly as the Fed’s balance sheet is a significant independent variable in our curve frameworks, indicating the 5s/20s curve tends to flatten by approximately 3bp for each 1% growth relative to the size of the economy (Figure 3).

WARSH … and USTs, the economy and inflation OH MY …

A Kevin Warsh-led Fed should lead to a steeper yield curve over time, assuming communication and balance sheet policy adheres to views he previously expressed. The potential for more monetary policy surprises and less consensus among investors about its future path should raise realized volatility.

Key takeaways

A Federal Reserve led by Kevin Warsh could allow for higher interest rate volatility and greater signaling qualities of macro markets.

A Fed that adopts a smaller footprint, both for its communications with the public and its balance sheet, should – all else equal – steepen the yield curve.

Until the Warsh Fed makes its intentions for the balance sheet known, investor speculation about a new approach could impact the swap spread curve.

Questions about how a Kevin Warsh-led Fed would change the SOMA portfolio outnumber the answers - opening doors to speculation and higher risk premiums.

We reveal takeaways from our reading of FOMC meeting transcripts between 2006-2011, which offer a historical perspective on Kevin Warsh’s views.

…Warsh on inflation Warsh looked at TIPS breakevens, commodity prices, and the US dollar when thinking about the drivers of inflation and inflation expectations, though he didn't see TIPS markets as perfectly embodying inflation expectations. He really spent a lot of time talking about commodity prices, the dollar, and import prices when referring to inflation. The weakness in the dollar as the Fed was cutting rates in mid-2008 made him more hesitant to keep cutting, given the perceived pass-through to inflation. He argued that:

...continued easing could well encourage the perception that the FOMC has a greater tolerance for inflation than is prudent.

Despite his concerns, Warsh probably learned from the “natural experiment” he spoke about:

...gauge whether changes in headline prices due in part to rises in energy and other commodity costs at a time of large central bank balances, at a time of an unsustainable fiscal picture, and at a time of debt limit discussions that are likely to preoccupy the floor of the U.S. Senate, whether all of that in a natural experiment finds its way into core prices or affects broader measures of inflation expectations.

…Warsh on markets Warsh didn’t like to keep the market beholden to the Fed’s view of growth, inflation, and monetary policy. He wanted the market to take its own view, both of how the economy is evolving relative to the Fed’s mandate and how the Fed should react to that evolution. He was comfortable with the market having a different view than the Fed, but he won’t necessarily reinforce the markets’ view if it differs from his.

He didn’t seem to mind the idea of disappointing market expectations, but was conscious about the “right time” to do it. He also gave markets credit for healing through their own means, and didn’t think Fed policies, while necessary, deserve “a disproportionate amount of credit”…

A Warsh nomination does not change our expectation for two further rate cuts, driven by disinflation, in 2H26. We expect that any shift in the Fed’s policy framework is more likely to occur gradually through balance sheet policy rather than the interest rate reaction function.

Key expectations

Economics: Kevin Warsh’s nomination does not materially alter our Fed outlook: we still expect two additional rate cuts driven by second‑half disinflation, with limited scope for a near‑term shift in the FOMC’s rate reaction function; any meaningful changes under a Warsh Fed are more likely to emerge gradually via balance sheet policy rather than interest rates.

Global Macro Strategy: Our global macro strategists think that a Federal Reserve led by Kevin Warsh should allow for higher volatility in and greater signaling qualities of macro markets. A Fed that adopts a smaller footprint, both for its communications with the public and its balance sheet, should – all else equal – steepen the yield curve. Regarding the Fed’s balance sheet, until the Warsh Fed makes its intentions known publicly, investor speculation about the Fed’s approach could also influence the shape of the swap spread curve.

Agency MBS Strategy: Kevin Warsh’s previously expressed views on the balance sheet have a negative tilt towards MBS investors, but we think this is countered by his preference for less regulation and reviews of the Basel Endgame proposal.

US Municipal Strategy:Few individual investors we surveyed list the Fed as their top concern; instead, we expect individual investors to continue to focus on inflation.

We exit long 10-year beta-weighted TIPS breakevens position due to the risks around the January CPI print; valuations are near mean reversion levels, and it tends to trade flat in the first week of Feb on average. We maintain 1y1y vs 15y5y CPI swap forward flattener.

Key takeaways

We exit our long 10-year beta-weighted breakevens position: valuations are close to mean-reversion levels, and it tends to trade flat in the first week of Feb

Jan CPI print usually surprises to the upside (residual seasonality), but the trend of misses in headline CPI in 2025 (8 out of 11) cannot be ignored

We continue to prefer 1y1y vs 15y5y CPI swap forward flattener, but raise the stop-loss of the trade

The trade benefits if 1-year fwd inflation expectations rise from here, metal prices pass through in CPI swap fwds, and if there’s a tightening in long-end BE

January core CPI fixing is at 42bp M/M, higher than our economists’ forecast at 40bp M/M and has tightened by 4bp from mid-January highs

Swiss view of the new Fed chair nominee (and NFP precap) …

…Considering the current make-up of the FOMC, and Warsh's past writings, and considering how other members of the FOMC might vote this year, we expect that replacing Jay Powell with Kevin Warsh as Chair of the Board is likely upside risk to our projection for two 25 bp rate cuts this year, which is also conditional on our current economic forecasts for inflation and the labor market. In other words, should this nomination move on to become Chair of the Board, this raises the odds in our view that the FOMC only lowers rates once this year…

30 January 2026, 17:23 UTC UBS: US Economy Stronger growth data delays Fed cuts to June. President Trump announced Kevin Warsh as his Fed Chair pick.

The timing of the next rate cut is likely delayed by stronger growth data and early signs of stabilization in the labor market.

Many Fed officials remain reluctant to look through tariff-driven goods inflation, reducing the likelihood of near-term rate cuts.

The ongoing DoJ investigation may indirectly slow a shift toward more dovish appointments to the Federal Reserve Board.

Nevertheless, the Fed’s guidance, including its latest forecasts, signals a strong inclination to continue lowering rates toward 3%.

By mid-2026, the path for rate cuts should become easier as 2H growth slows and goods inflation eases.

We now expect the next rate cut in June, followed by a second in September, bringing the policy rate range to 3.00-3.25%

30 January 2026 UBS: US Economics Weekly An unusual risk to rates

Economic Comment: a risk to front end rates The President announced via TruthSocial that he intends to nominate Kevin Warsh as Chair of the Board of Governors of the Federal Reserve. In most of his writing over the years, Warsh had been relatively hawkish on monetary policy and the use of the Fed's balance sheet. However, in more recent writings he has supported rate cuts. How influential any Chair might be over the setting of monetary policy depends also on convincing the rest of the 12 members of the Federal Open Market Committee. Considering the current make-up of the FOMC, and Warsh's past writings, and considering how other members of the FOMC might vote this year, we expect that replacing Jay Powell with Kevin Warsh as Chair of the Board is likely upside risk to our projection for two 25 bp rate cuts this year, which is also conditional on our economic forecasts. In other words, should this nomination move on to become Chair of the Board, this raises the odds in our view that the FOMC only lowers rates once this year…

The Week Ahead: January employment next We expect nonfarm payroll employment expanded 90K in January. Risks abound with annual revisions and new methodologies, which we explain on page 22. We expect the unemployment rate fell back to 4.3% and average hourly earnings rose 0.3%. We expect the annual revision to revise down the level of employment as of March 2025 by ~750K. Other labor market data sets to be released include the JOLTS, ADP's monthly estimate of private employment, and the monthly tally of job cut announcements. We may revise our projections for the employment report if anything surprises us. FOMC speakers include Governor Cook and Vice Chair Jefferson with both speaking on the economic outlook, and Vice Chair for Supervision Bowman will speak at a WSJ Invest Live event. We expect lightweight vehicle sales fell back to 15.1 million (saar) in January, probably not helped by the snow. We expect the ISM manufacturing composite rose 1.6 points to 49.5 in January, and the non-manufacturing composite likely continued to signal subdued growth…

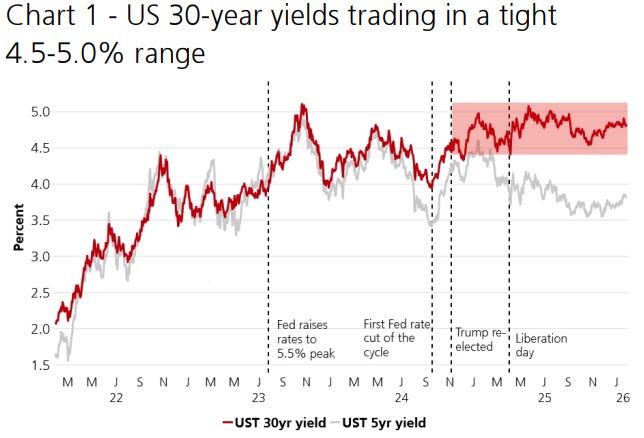

30 January 2026, 13:50 UTC Interest Rates Strategy Holding the line: Policy, premium, and the long end bond

2026 has started with some eye-catching market moves and events, but you wouldn’t know it by looking at longend bonds, which continue to trade in tight ranges with low volatility.

Instead of signaling complacency, we attribute the stability to three factors: (1) a valuation cushion after a multi-year curve steepening trend, (2) a strong resolve from policymakers to cap borrowing costs, and (3) for all the noise, little has changed on the US macro outlook and expected path of interest rates.

In the US, we continue to see modestly lower Treasury yields across the curve. Although 30-year yields should remain contained at 5%, we advise hedging against a breakout via option structures given low implied volatility.

The more profound implications may be outside the US as investors seek diversification. We prefer UK gilts and German Bunds over Japanese government bonds.

… The year has started with a flurry of geopolitical events that threaten to reshape the world order and the way capital flows across borders. Investors are once again asking questions about the US’s historically large fiscal deficit and the ability or willingness of foreign investors to fund it. Added to that, there are lingering concerns about central bank independence—all the while inflation has been running above target in many economies for more than three years now. Eye-catching market moves in the USD and gold prices have rekindled rhetoric around a “debasement trade.” Yet, the fixed income market, with the notable exception of Japan, has appeared unscathed, with longend bonds remaining in tight ranges and volatility firmly on a downward trend (Chart 1 & 2). For all the noise about US “debasement,” it is notable that breakeven rates on US Treasury Inflation Protected Securities (TIPS) have ticked up only modestly, while the nominal US Treasury yield curve has actually flattened…

…a historical perspective shows that this is the worst performance for the 30-year US Treasury bond during Fed easing cycles in the last 40 years (Chart 3). While the consensus and positioning still appears to lean in a bearish direction on the long-end, it is important to note that this underperformance on the curve has already gone a long way.

Affordability? Warsh’ll get it…

January 30, 2026 Wells Fargo: Kevin Warsh as Fed Chair

Summary We know from our many client discussions that there appears to be at least some degree of comfort with a Warsh led Fed vs. the other choices. But, we all should be mindful that there is also some degree of uncertainty associated with this pick if for no other reason than his public remarks on the economic outlook and the appropriate path for the federal funds rate have been fewer and farther between than the other finalists.

We generally expect Chair Warsh to support a more dovish stance on monetary policy driven in part by his optimism over productivity growth as well as his view of the need for lower rates to support “Main Street.” And of course, a dovish slant is what President Trump wanted. That said, Warsh has historically been among the most hawkish of the four finalists on President Trump’s shortlist. Warsh’s reputation as a hawk stems from his time as a Fed Governor and during his post-Fed career.

Although Warsh’s comments on the fed funds rate have been infrequent in recent months, he has maintained a belief that the Fed’s balance sheet is too large—a belief he has long held and another factor that has contributed to his hawkish reputation.

We think it is highly unlikely that the Fed will shrink its balance sheet materially under Chair Warsh given how entrenched the “ample reserve” operating framework is in the financial system. Stated differently, there are no reasonably plausible scenarios where the financial system would comfortably absorb a sharp change to this stance, no matter what the leaning of the new Fed chair may be. There is a high hurdle to altering this framework.

Where we think Chair Warsh could affect more change is by de-emphasizing short-term data dependence in favor of “trend dependence”, which we believe would lead to fewer, but more seismic, inflection points in U.S. monetary policy. We can also see him making a case for diminishing or even completely doing away with the Summary of Economic Projections and the Dots. We would not be surprised if he makes a case for less “Fed-speak”.

When it comes to Fed independence, Warsh has been outspoken about the need for the Fed to revisit some of its current governance policies and processes, but he has publicly maintained a belief in the importance of central bank monetary policy independence.

It is also important to remember that monetary policy decisions are a Committee decision. Seven governors vote at each meeting in addition to five of the 12 regional Fed presidents. This ensures some continuity in the makeup of the FOMC as it transitions. Accordingly, we do not anticipate making any changes to our fed funds forecast, although as we have stressed elsewhere, we continue to see risks to our call.

We would give you just two more things to consider. Warsh has some challenges that start almost right away. First, does he act as a shadow Fed chair? If he is going to second guess Powell at every turn or forcibly disagree with him, he may appease his new boss, but he runs the risk of alienating himself to the rest of the Committee. We think Warsh knows this and will tread carefully around that, but it’s a risk. And second, what kind of consensus builder will he be? Criticize Powell as much as you like (and yes, we have been critical of him at times), but he is one heck of a consensus builder, carefully crafting and selling his message to members ahead of meetings. This will be critical for Warsh. The expectation is he wants to cut, perhaps even more aggressively than market pricing. If that is indeed the case, he has his work cut out for him in building a consensus toward that when the expectation of the Committee at large is just for one more cut per the dots (where we think the hurdle is growing higher even for that).

For those that want to read on, below you’ll find more detail about his background and our analysis of his direct quotes over the years…

January 30, 2026 Wells Fargo: Home Price Appreciation Picks Up Real Estate Spotlight

Summary Home prices are once again on the rise. The Case-Shiller national home price index climbed 0.4% in November, the fourth straight monthly increase. The recent streak of gains represents a rebound from the string of monthly declines in the spring and summer of 2025.

Overall, the trend in home price appreciation has softened considerably compared to the post-pandemic boom years. However, the 1.4% year-ago change in November indicates that home price appreciation is still running in positive territory.

… Moving along TO a few other curated links from the intertubes. I HOPE you’ll find them as funTERtaining (dare I say useful) as I do …

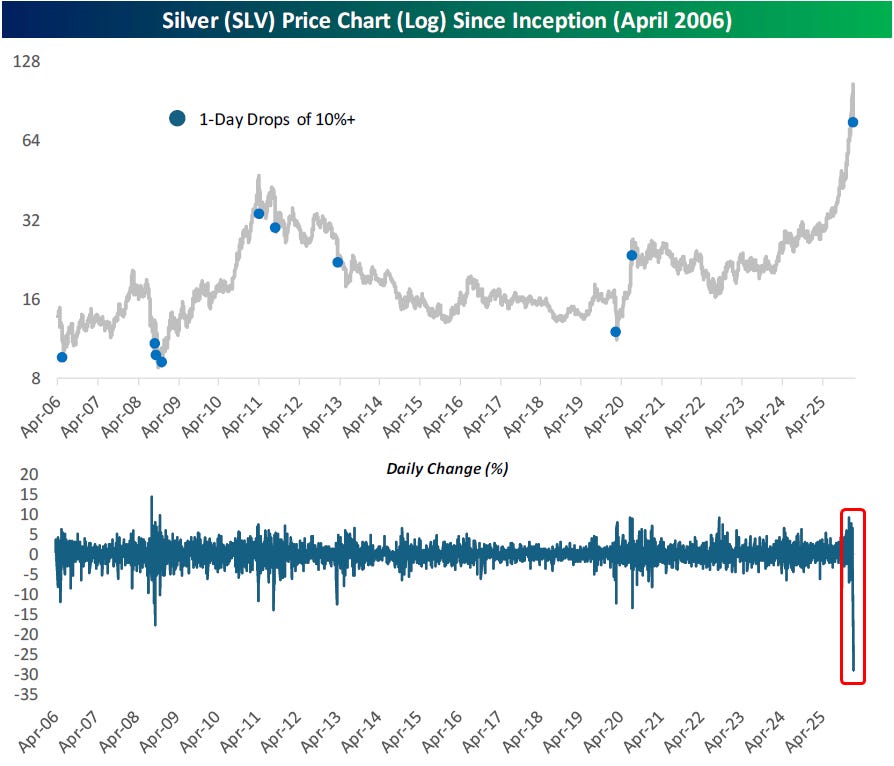

…After experiencing a parabolic run higher in the last few months, the silver ETF (SLV) crashed 28.5% today for what was easily its biggest one-day drop in history. The next closest was a 17.99% drop on 10/10/2008 during the worst week of the Financial Crisis when the Dow fell 20%.

CHARTS … I like ‘em … especially as EARL put into context of RATES …

POSITIONS matter and here it seems the evil speculators have gotten incrementally more short 10s …

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

Happy to read this next one as it REMAINS topical — dollar down means WHAT for bonds??

Jan 30, 2026 Shadow Price Macro: The falling Dollar won't hurt Treasuries

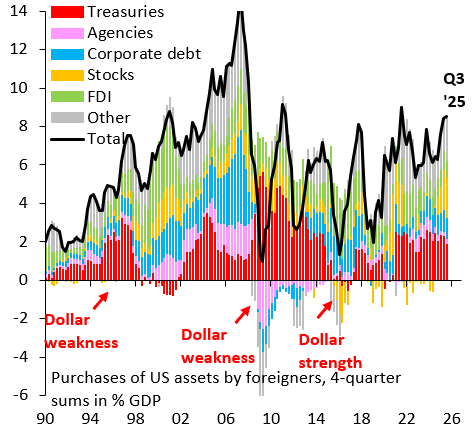

…One of the leading explanations for this conundrum was the weak Dollar. Foreign central banks, especially in Asia, were intervening to stop their currencies from rising against the Dollar. This meant they were accumulating Dollars, which they invested in US Treasuries. The theory at the time was that this additional demand for Treasuries was preventing yields from rising as they normally would. Academic work since then has found this “flows” effect to be robust and sizeable.

The chart above shows foreign flows into all US assets from the Fed’s flow of funds. The red bars are foreign flows into Treasuries, where I’ve used red arrows to denote periods of Dollar weakness or strength. The key regularity is that when the Dollar is falling or weak, foreign flows into Treasuries are strong. When the Dollar is rising or strong, foreign flows into Treasuries are weak. Intuitively, this lines up with the idea that foreign central banks are buying Treasuries when the Dollar is weak and selling them when the Dollar is strong…

…The bottom line is that a weak Dollar is good for Treasuries because foreign central banks turn into buyers. Historically, dysfunction in the Treasury market is associated with sharp increases in the Dollar, which is when EM central banks sell Treasuries, which upsets the basis and swap spread trades.

I’ve come to look forward to reading latest from Brent Donnelly and usually stumble on this, read couple times — especially for any / all comments on RATES — and have done AFTER listening to him and Alf on the Macro Trading Floor podcast. Perhaps it is a way to stay connected to that life. Whatever MY motivation, is fine by me if you don’t listen / subscribe / read cuz I will and will pass along whatever strikes them which then strikes ME … I’ll just say this, I spent past few days working more on setting up trailing stop losses of all sorts, related TO metals, then I ever would have imaged … That aside, on global macro (WARSH) & rates …

January 30, 2026 SPECTRA MARKETS Friday Speedrun: Silver Crash Silver has its 1987 moment

…This nomination cements my view that we get a consolidation/correction phase here for the USD and precious metals as the start of February is not a great seasonal window for precious, and pension fund USD selling is likely to cool once month end is over. Pension funds are less likely to be active USD sellers next week as they have just spent a busy week putting on USD hedges and early in the month is not their busy time.

I agree with the market reaction: The nomination of Warsh is a mild USD positive and precious metals negative as it takes a more rogue candidate like Hassett out of the picture, but in the end there was nothing much priced in for the Fed before and there will be nothing much priced in for the Fed now. The US economy continues to chug along fine and after six rate cuts, Fed Funds are in their happy place. You can see that expectations for the September 2026 implied rate have really not moved since Liberation Day as the market expects Fed Funds to land somewhere around 3.0%/3.25% at that meeting.

Here’s Alf’s take on Warsh, which is more USD-bearish:

“What Bessent and Warsh have in mind seems like a LatAM way of running monetary and fiscal adapted to the US.

Reduce interest cost on debt to optically reduce spending and redirect fiscal resources, but mostly lower rates enough so that the private sector can engage in productive investments and lead growth.

These policies argue for lower USD, lower front-end rates, steeper curves, much higher equities. Let me explain the last point on equities.

Reducing the Fed B/S does nothing to real-economy money, while lowering front-end rates makes policy looser and helps Bessent to redirect fiscal resources to the private sector if he keeps issuance focused on the short-end (At lower rates) saving interest costs and redirecting fiscal impulse to the real economy. All positive for equities.”…

…Here is a stupid chart I made:

…Interest Rates Bonds have stabilized as institutional money in Japan has started buying JGBs at the margin and there is enough weakness in equities to bring the odd bond buyer. The break of 4.20% was lackluster, but we’re still above. RBA next week is likely to hike, but it’s close enough to priced in…

Trump PICKS, mkts react … reflex … AND PPI jumped on services …

Jan 30, 2026, 7:29 PM WolfST: Markets’ Reaction to Warsh: Silver Collapses, Gold Plunges, Dollar Jumps, Treasuries Yawn, Stocks Drop, already Battered Cryptos Sink

Pulling the rug out from under the “debasement trade.”

Jan 30, 2026, 2:54 PM WolfST: Producer Price Index Jumps on Disconcerting Spike in Services PPI. Food & Energy Prices Fall

Core goods prices rise as companies distribute the tariffs amongst each other.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

Brent is a great read and funny as hell too! Strangley was telling a fellow metals investor on Wed the banks would luv to smash silver to $80 then short it to $60. Call me Jinx lol! Funny thing I feel BETTER after smackdown Friday, guess I'm paranoid of vertical up moves. Appreciate all the info on Warsh can't say I was paying much attention in 2006-2011. Xbox & Halo were much bigger parts of my younger life back then 🤣🤣🤣

Warsh & Peace.....that's classic...

(one reason why I enjoy this newsletter so much)

Mr Warsh sounds good on paper....

Quite a market reaction.....

Almost anything will be better than Powell...

Let's resume the rally in Stocks, Bonds and Bullion....

Brent is a great read and funny as hell too! Strangley was telling a fellow metals investor on Wed the banks would luv to smash silver to $80 then short it to $60. Call me Jinx lol! Funny thing I feel BETTER after smackdown Friday, guess I'm paranoid of vertical up moves. Appreciate all the info on Warsh can't say I was paying much attention in 2006-2011. Xbox & Halo were much bigger parts of my younger life back then 🤣🤣🤣