(USTs 'under pressure' o/n, steeper on 'modest' volumes)while WE slept; "Bond Yields Rise at Fastest Pace Since Early 1980s" (BBG ... somethings gonna break)

Good morning … This morning, much is being made OF news flow from China past 24hrs …

Bloomberg- China Signals Zero Tolerance For Sharp Economic Slowdown With Rare Steps Reuters- China's measures to shore up a shaky economic recovery

… and rightfully so. The magnitude of the moment IS addressed a bit more by Global Wall Street (just below) … At the same time as the flow of macro economic and FISCAL support is (continuing to be) UNLEASHED to ease economic pain ‘over there’, it’s worth mentioning the data HERE yesterday was … MIXED — see what ever you wanna see …

ZH: US PMIs Print Goldilocks Surprise In October: Growth Expansion & Slowing Inflation

… and as you saw, that data combined with RATES / SUPPLY leading TO markets celebratory reaction …

ZH: Bitcoin & The Dollar Soar, Squeeze Saves Stocks As Yield Curve Re-Inverts

… it is worth noting rates did NOT rubber band bounce (technical term) back UP above 5% (Bill and Bill really are smart, aren’t they) and so, there may just be a reason to HOPE — cuz HOPE = strategy, right?

Speaking of HOPE, #Got5s? I HOPE you might like some especially after yesterday’s 2yr auction. It would suggest today’s 5yr auction will be < GREAT / mediocre / a train wreck > please choose one …

ZH: Solid 2Y Auction Prices On The Screws As Yield Drops For The First Time In 7 Months

One day after the biggest intraday reversal in Treasury yields following bullish bond commentary by the two "Bills", markets were closely watching today's 2Y auction to see how the sharp drop in yields would impact demand for short-end paper.

We got the answer moment ago when the Treasury sold $51BN in 2Y notes, in a solid auction which saw the first drop in the high yield since the March bank crisis, when yields tumbled from 4.67% to 3.93%, sparking widespread carnage among the "higher for longer" crowd. To wit, the High Yield was 5.055%, down from 5.08% in September, and priced "on the screws" to the When Issued, which was also at 5.055%, Curiously, this was the 2nd auction pricing "on the screws" in a row, a very rare occurrence.

The bid to cover was less impressive: at 2.636 it was down from 2.738 last month and the lowest since March (of course, it was below the six-auction average of 2.82).

The internals were also subpar, with Indirects taking down 62.1%, down from 65.0% and the lowest since April (vs six-auction average of 65.6%); and with Directs awarded 20.3%, or in line with recent auctions, the Dealers were left holding 17.6%, a big jump from September's 14.0% and the highest since April's 18.9%.

Overall, this was an average auction, with solid demand - especially by foreign buyers - despite some weak metrics here and there, something which wasn't lost on the bond market where the 10Y yield now trades back down to 4.83%, near the lows of the session…

AVERAGE they say. Okie Dokie, boys and girls. You know what to do … we’ll show THEM average. Get out there today and get those bids in early and often and lets make this one the best auction ever ? Ok, maybe not but … todays 5yr auction will go as < GREAT / mediocre / a train wreck > please choose one, and once again lead to another squeeze higher in stonks cuz, you know.

Bonds.

Forget it. Here’s a look at 5yy for some context …

I’d note momentum (stochastics, bottom panel) are now a ‘push’ … not indicating one thing or another and so, my eyes are once again attracted TO the TREND and I’ve attempted to highlight psychologically important round number (5.00%) doesn’t appear to be lost on anyone … at least not yet?

Bids in at 1pm please and while 5% may NOT be todays business, it’s worth keeping on one’s radar screen, at least in the shorter-term … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… Overnight Flows Treasuries were under pressure overnight with the 2s/10s curve steepening out to -21 bp. Overnight volumes were modest with cash trading at 74% of the 10-day moving-average. 5s were the most active issue, taking a 31% marketshare while 10s were a distant second at 23%. 2s and 3s combined to take 32% at 19% and 13%, respectively. 7s managed 8%, 20s 1%, and 30s 6%.

… and for some MORE of the news you can use » The Morning Hark - 25 Oct 2023 in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ (in a similar sorta way you’ll find content if you pay for ZH PREMIUM … except different … I think, as they seem to be selling others research and I’ve never been quite sure how they can do that … anyways, another time …)

ABNAmro- Global Monthly - Six urgent questions on China

The main driver of the global growth slowdown is the spike in inflation and interest rates, not China, but a sharper reopening rebound would have cushioned global growth more than it has. In this special Global Monthly, we tackle six urgent questions surrounding China's recovery and what it means for the global economy. Cyclically, the Chinese economy already passed the trough, but headwinds remain: from property sector woes, to post-zero-Covid scarring, and the global slowdown in demand for goods / rotation back to services, next to some other (structural) challenges. A silver lining of China’s slowdown is less inflation, but at the current juncture this effect is limited. Given how China-EU/US relations are evolving, we delve into how this is impacting tech/EV sectors.

… US: Mixed signals amid strong data

Activity data has been unambiguously strong over the past month. But the data has been prone to revisions due to falling response rates for preliminary data releases Meanwhile, the Fed's Beige Book suggests a much weaker economy than what the hard data is currently telling us The Fed is hedging its bets for now given the continued murkiness in the macro picture

… The Fed is – understandably – adopting a cautious, non-committal stance given the continued conflicting signals we are getting from the economy. The significant run-up in bond yields, with the 10y Treasury yield topping 5% this week, also represents a major tightening of financial conditions that is probably equivalent to a couple more rate hikes. Despite this, the pushback from Fed officials has so far been restrained. Still, the Fed looks fairly certain to keep policy on hold at next week’s FOMC meeting, and a December hike also looks unlikely, barring a major upside surprise to labour market and/or core inflation data next month. How soon the Fed pivots to more dovish communication will depend on how the conflict in the data and the qualitative read on the economy resolves itself over the coming months, with our base case continuing to see a substantial slowdown in Q4.

Apollo- Proxy Fed Funds Rate Is 7% (not much to add other than another look at how tight — FINANCIAL conditions — are)

The Fed has quantified what their forward guidance and balance sheet policy mean for the fed funds rate, and their estimates show that the proxy fed funds rate is 7% rather than the official 5.5%, see chart below and here.

In other words, comparisons with history and discussions of how restrictive monetary policy is should not only look at the level of the fed funds rate but also include forward guidance and balance sheet policies, including their impact on long rates.

Apollo- Restarting Student Loans Weighing on Households (not IF but when…?)

Student loan payments restarted on October 1. And the Census Household Pulse Survey for October shows a jump in the share of consumers saying they are having difficulties paying their household expenses, see chart below.

Looking at the Household Pulse Survey in detail shows that the difficulties with paying household expenses were concentrated among households with a college degree, making between $50,000 and $150,000, suggesting that restarting student loan payments is the source of increased financial stress for consumers.

BAML - Asset managers shift UST longs further in on curve, FI fund inflows cool (the ‘ole Curve-o-meter)

Moving in … CFTC data suggest that asset managers are shifting away from long UST positions further out the curve to shorter tenors. This is consistent with investors requiring more compensation to own duration given elevated inflation risks, USTs being less diversifying in portfolio construction, and an uncertain fiscal backdrop. We remain more confident in curve steepeners than duration

Barclays- Equity Strategy - Who Owns What: Positioning cleaner in equities...and bonds (positions matter as does watching what they SAY as well as what they are doing)

Defensive hedges mean de-risking has been orderly. Cleaner positioning, oversold technicals and better seasonals raise the chances of relief rally, with Europe and Cyclicals looking under-owned. But medium-term outlook is tricky and bonds look increasingly attractive to us post recent selloff, albeit more in EU than US.

DB - Refunding preview: Large borrowing needs in a high(er) term premium world (LARGE needs and … getting largER? a view…)

… We push back against the view that the Treasury might pause its coupon increases this quarter for several reasons: (1) the Treasury gave guidance of further coupon increases in August, and it is unlikely to violate its principle of being "regular and predictable" for short-term changes in the market environment; (2) the bill's percentage of total debt is elevated and still rising; and (3) the recent term premium repricing reflects an overdue recovery rather than an overshoot to the upside, and the move may not be fully finished yet, so delaying increases into the future could be counterproductive.

That said, we do expect the Treasury to be responsive to the recent market move. Our coupon size forecast entails a similar cadence of increases as announced in August but with a slight tapering in 10y to 30y maturities. We also expect potential upside to FRN increases, as well as the first 10y TIPS increase in more than a year….

A bill share of total debt that could exceed the TBAC's recommended range for a long period puts pressure for coupon supply to grow

A notable element of the rise in rates and curve-steepening over recent months is how steady measures of inflation compensation have been by comparison. Through early last week, 5y and 5y5y inflation swaps had traded in a range of 20-25bps since July, near their tightest 3-month ranges over this hiking cycle.

We saw more notable moves in the wake of Chair Powell’s remarks last week, which brought 5y5y inflation up to 2.8%, its highest level in a year. While that rise has since retraced, 5y5y still sits near its peak over the cycle, as shown in today's chart…

…Models and surveys don’t paint an entirely clear picture on this breakdown, and given the need to make an assessment and calibrate policy to it, there’s a chance the Fed gets it wrong. This could lead them to ease off on hikes when markets are in fact signalling the need to do more. In market pricing, this risk would show up in higher inflation risk premia and breakeven rates, and so breakevens bear close watching. That said, there are limits to how far 5y5y can go given a material move up should elicit hawkish pushback from the Fed.

DB - China Macro - Understanding the CNY1tr fiscal stimulus (important for those of us even far removed from the Far East to understand how far reaching consequences might be … re/reading)

China has just approved a new fiscal stimulus package. The government will issue an additional CNY1tr of CGBs for infrastructure investment, which will raise its 2023 annual budget deficit to 3.8%, exceeding the 3% implicit deficit ceiling. The government appears to be serious about boosting growth.

We look for modest rate cuts in 2025, followed by an equally modest boom in mortgage lending

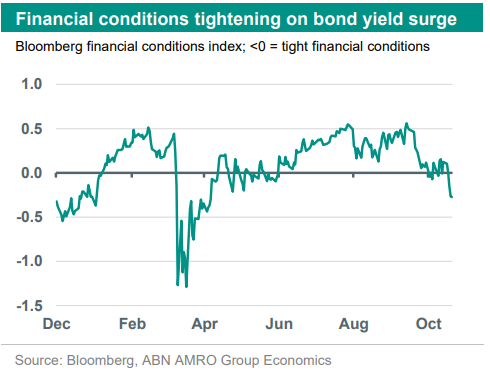

JPM - The J.P. Morgan View: Financial conditions remain a headwind (all the cool kids talkin’ about it … )

… Financial conditions remain a headwind: Tightening in financial conditions has continued largely unabated since 1Q22. Given that the impact from a tightening in financial conditions on GDP typically takes 1-2 years, the full effect of the severe tightening that took place last year has yet to be felt. And the continued tightening, albeit at a slower pace, during 2023 should add to this effect until well into 2024.

LPL- Treasury Term Premium 101 (I always say, ‘talk to me like I’m 2’ … this gets close to my level of understanding PLUS a longer term’ish visual helps)

… Economic theory suggests that each security on the Treasury yield curve can be thought of as the expected fed funds rate over the maturity of the security, plus or minus a term premium. The Treasury term premium is the additional compensation required by investors for owning longer maturity Treasury securities. The term premium, which is unobservable and thus has to be estimated, takes into consideration things like Treasury supply/demand dynamics, foreign central bank expectations and the potential for higher inflation in the future, to name a few. And since the end of July, which is when the last Treasury quarterly refunding announcement (QRA) was made that surprised markets because of how much new debt would be coming to market, the term premium has increased dramatically. The next QRA is October 30, so if the Treasury department surprises markets again with the amount of debt coming to market, we could continue to see the term premium move higher.

MS - November Refunding: Lower Coupon Supply (IF that were to happen it MIGHT be a somewhat less bearish development … staying tuned…)

With the recent rise in term premiums, we expect a slower pace of coupon increases at the November refunding meeting, with a higher share of funding via T-bills in the coming quarters.

We think the US Treasury's upcoming quarterly refunding meeting might deliver a surprise relative to market expectations – in which the Treasury might decide to increase coupons at a lower pace than what its "regular and predictable" strategy might have suggested in August. We expect more T-bills in lieu of coupons to make up a higher share of issuance through 2024.

We see an increase of $2bn in 2s, 3s, 5s, and 10s and $1bn in 7s and 30s, with 20s unchanged at the November and February meetings, a lower pace of increases vs. August - $3bn in 2s, 5s, and 10s, $2bn in 3s and 30s, and $1bn in 7s and 20s.

We see the recent sharp rise in term premiums being a key consideration for lowering the coupon path….

UBS - Tepid surveys today (leaning in to read all ‘bout it … maybe something to do with little bit of bid — want 5s little bit later on to accompany yer 2s? anyone?)

S&P Global flash manufacturing PMI still tepid… Richmond Fed manufacturing index little changed in October… Richmond Fed services index falls back… Nonmanufacturing activity remains feeble in the 3rd district too…

UBS - China to Issue Extra RMB 1 Trillion Special CGB (folks on sellside seem to be buyin’ in, drinkin’ the KoolAid China policy makers pourin’)

… A clearly more proactive fiscal policy signal Although Bloomberg reported earlier such issuance of special CGB and increase of headline fiscal deficit for 2023, today’s announcement may be still a positive surprise for many investors. 3.8% headline fiscal deficit in a post-Covid year of 2023 is well above around 3% in normal years and even higher than that in the Covid outbreak year of 2020 (3.7%), suggesting a clearly more proactive fiscal policy signal. Amid subdued local government revenue and restricted LGFV financing, additional CGB issuance and direct transfer should help ease local fiscal difficulties and support related public investment.

More policy support to come; maintain 2023/2024 growth forecast…

China has announced a fiscal stimulus, increasing the deficit limit from 3% to 3.8% of GDP. The money is focused on infrastructure spending. China was expected to meet this year’s growth target of around 5%. The rush to stimulate at this point in the year suggests concern about growth momentum in 2024, or a worry that living standard reality is not as good as the reported GDP figures imply…

… And from Global Wall Street inbox TO the WWW,

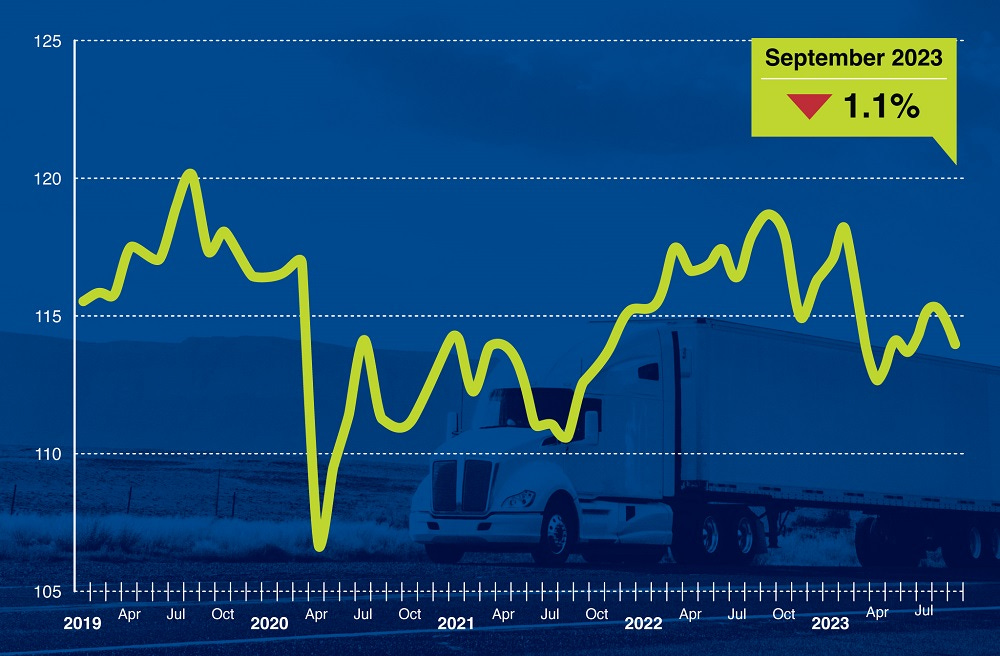

ATA- ATA Truck Tonnage Index Fell 1.1% in September (i’m sure this is fine)

Washington – American Trucking Associations’ advanced seasonally adjusted (SA) For-Hire Truck Tonnage Index decreased 1.1% in September after rising 0.2% in August. In September, the index equaled 113.9 (2015=100) compared with 115.2 in August.

Image

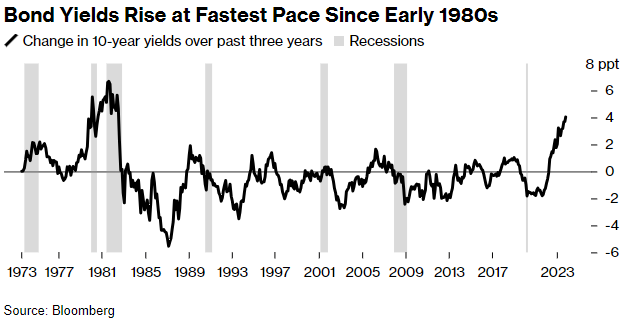

Bloomberg- The Last Time US Yields Rose So Much, It Sank the Economy Twice

10-year Treasury yield up over 4 percentage points since 2020

The biggest increase since double-dip recessions of 1980s

… The 10-year Treasury yield — a key baseline for the cost of money across the financial system — has jumped more than four full percentage points over the past three years, briefly pushing it this week over 5% for the first time since 2007. It’s the biggest increase since the run up in the early 1980s, when Paul Volcker’s efforts to slay inflation pushed the 10-year yield to nearly 16%…

… “A hard landing is sort of our base case scenario — but I can’t point to any data and say, ‘This is a clear leading indicator of a recession and look right here,’”said Priya Misra, a portfolio manager at JPMorgan Asset Management

“Conviction levels are low,” she said. Investors who had been buying bonds “have all been hurt,” she said.

Bloomberg- New Age for Treasuries Means 6% Yield Isn’t ‘Out of the Picture’ (sent out couple days ago but I just stumbled on it so …)

DoubleLine’s Whiteley: higher-for-longer ‘finally taken hold’

Brandywine’s Chen says ‘we are in a regime change’ for bonds

… The Federal Reserve may very well be at — or near — the end of its most-aggressive interest rate-hike cycle in decades. But at the same time, other forces have continued to push yields higher. The economy has remained surprisingly resilient. Inflation, stubbornly high. And the federal budget deficit is surging, testing the market’s ability to absorb a seemingly endless supply of new US government bonds.

The upshot is that some are sticking to their calls that yields may be near their peak as the impacts ripple through the cost of everything from credit cards to corporate loans, taking the pressure off the Fed to raise rates further. Others, though, say that yields have become untethered and another push higher is far from out of the question…

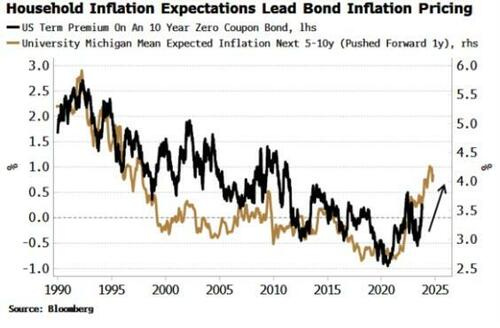

Bloomberg- Bond Yields Have More To Go As Retail Wises Up To Inflation

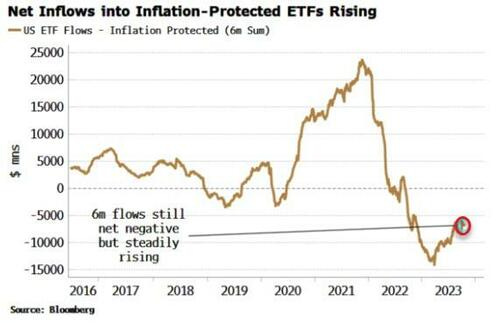

… In the wake of the initial burst of US inflation in 2021, there was a spurt of interest among both retail and professional investors for real assets and their proxies, such as commodities, as well as energy and industrial stocks. That has since waned somewhat, but inflation is unlikely to return to a low-and-stable regime anytime soon.

Households may be picking up on this, and are investing accordingly. Flows into the largest commodity ETFs have been rising this year. And flows into ETFs of inflation-protected securities, which peaked in 2021 then fell sharply, have also been steadily picking up.

Long-term inflation expectations of households (as measured by the University of Michigan’s survey) are markedly higher than what is expected by the Federal Reserve, or priced in by the market based off breakeven rates and CPI fixing swaps.

Typically, household inflation expectations lead bond term premium - which is mainly driven by the market’s expectation of inflation and inflation volatility – by around a year. Term premium has been following household inflation expectations higher this year.

But in this cycle, the sensitivity between inflation expectations and term premium is likely to be higher as the household sector becomes the de facto buyer of last resort of Treasuries.

They are the only sector absorbing USTs as the Fed, US financials and the rest of the world reduce their exposure.

As the marginal buyer, they’re likely to demand a higher yield than the market is currently offering to compensate for the greater inflation risks they foresee, and are beginning to hedge.

Well look who won the Speakership Prize, a real in the flesh MAGA. I really can't believe this. There's always Hope, says Gandalf, but perhaps there's far more than I ever imagined. Perhaps. As the great Kieth@Hedgeye says, "HOPE is NOT an investment (or Geopolitical) strategy".

Well look who won the Speakership Prize, a real in the flesh MAGA. I really can't believe this. There's always Hope, says Gandalf, but perhaps there's far more than I ever imagined. Perhaps. As the great Kieth@Hedgeye says, "HOPE is NOT an investment (or Geopolitical) strategy".

I'm wondering if there's a relationship between 4th Turnings and Interest Rates; or rate Volitivity. Just a thought, more research required.