Good morning … As the dust settles, I might be watching the 5yy for some signals

I’ve etched in an UPtrending line and today, it is about 3.95% … a break BELOW would be of some importance, in the short run, IMO but for now there’s simply NO indication that is near term risk … We ARE oversold (stochastics) and trading near another inflection point just north of 4% … no signals yet there is any hurry to buy / cover and this, as an FOMC ‘hawkish PAUSE’ is almost completely in the rear view mirror and nearly buried by the news out overnight from CHINA.

ZH: Yuan Tumbles After Chinese Economic Data Dump; Youth Jobless Rate Hits Record High

… An ugly night of data from China tonight suggests the 're-opening' is not gathering pace:

China May Retail Sales disappointed, rising 12.7% Y/Y; Est. 13.7% - which is a flashing red indicator. Given the boost from the Golden Week holiday, May retail sales rising just 0.4% from April speaks to how consumer sentiment has yet to show any significant improvement.

China May Industrial Output slowed to a 3.5% rise Y/Y; Est. 3.5%

China Jan.-May Fixed Investment rose less than expected, up 4% Y/Y; Est. 4.4%

China Jan.-May Property investment tumbled 7.2% from a year earlier with the value of new home sales by the 100 biggest developers falling 14.3% in May.

And with that, China cut Medium Term Loan Facility rate by 10bp, first cut in 10 months…

Back to the here and now … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…A morning commentary titled, “4% Counterpoint”

… Overnight Flows After rising during the Tokyo session, rates pulled off the highs overnight with volumes at 146% of the 10-day moving average. 5s and 10s shared the title of most active issue with each claiming a 33% marketshare. Front-end volume distributions were fairly typical with 2s taking 13% and 3s claiming 11%. 7s managed 6%, 20s took 1% and the long-bond rounded out the curve with a 4% allocation…

… and for some MORE of the news you can use » IGMs Press Picks for today (15 JUNE) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

Before I jump in TO Global Wall St inbox and FOMC victory laps, how about that there PPI …

ZH: PPI Plunges More Than Expected - Lowest Since Dec 2020

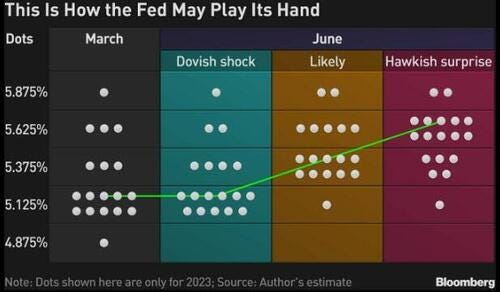

Putting paid TO aforementioned hawkish pause? But then, what of the DOTS PLOTS and 2 additional hikes??

Global Wall Street has plenty to say regarding the FOMC … sampling the victory laps

BMO FOMC: Hawkish Pause Delivered BNP US June FOMC: Are hawks flying higher and faster than Powell?

…Our official forecast remains for the terminal rate to reach 5.50% at the July FOMC meeting. We continue to believe that decelerating economic activity, lagged effects of previous rate hikes, tightening lending conditions in the banking sector and greater evidence of disinflation will show up more forcefully in H2 2023—and ultimately diffuse conviction for the second additional hike to 5.75% (presumably on either 20 September or 1 November)…

…In discussing inflation drivers, Powell stuck to his now long-standing assertion that wage growth needs to slow and this likely requires labor market easing. He described recent wage growth rates as still too high. Importantly, in response to a question, he appeared to dismiss a recent paper from the San Francisco Fed arguing that wages did not contribute much to inflation in favor of a direct reference to a recent paper by Bernanke and Blanchard that concludes that wages do ultimately drive inflation. Powell sounded optimistic that recent falls in indicators of rent would cut housing inflation in time, but also noted that housing had appeared to bottom and may be recovering….

DB: June FOMC: Little bit harder, a little bit more, a little bit further than before

…We maintain our Fed expectations in response to today's meeting. Our baseline remains for a final 25bp rate hike in July, with the Fed then remaining on hold into early 2024 in response to further evidence of labor market weakening and inflation falling somewhat faster than envisioned in the Fed's latest forecasts…

If the Federal Reserve were paying close attention to the money supply it would know that monetary policy is now tight…

GS June FOMC Recap: A Hawkish Surprise Raises Our Confidence in a July Hike

…We have not made any changes to our forecast of one additional hike in July to a peak rate of 5.25-5.5%. The combination of the hawkish surprise in the dots and the hint at an every-other-meeting pace strengthens our confidence that the FOMC will hike in July and makes a possible second hike more likely in November than September, though neither is in our baseline forecast….

…We have long been of the view that the Fed is done with rate hikes, but we will need to see some adjustments in Fed communication over the coming weeks to feel confident in that view. The message delivered today suggests that the markets should be pricing in a significant probability of a hike in July, and the Fed may be forced to follow through….

We continue to see a soft landing for the economy this year, with inflation and wages slowly easing,as well as job gains. Consistent with the economic outlook, we continue to look for the Fed to hold the peak rate at 5.1% for an extended period before making the first 25bp cut in March 2024. Our rates strategists see the market starting to underprice the risk of a weaker economy, cooling inflation,as well as bank crisis risks. They suggest beingneutral on duration for now…

RBC: Fed skips June hike but suggests more tightening to come UBSs Paul Donovan: Not the Fed’s finest hour

For somewhat more off The Terminal via ZH,

ZH: Fed's Dot Plot To Show More Tightening On The Cards Authored by Ven Ram, Bloomberg cross-asset strategist,

Investors are underpricing the possibility that the Federal Reserve will telegraph a higher peak rate with its new dot plot this week.

The median of FOMC members’ indications will show an additional one or two hikes, while a couple of them may pencil in more tightening than that. Should the median show more than one increase, Treasuries are bound to sell off.

The Fed will need to revise its dot plot to acknowledge that it isn’t done with its efforts to quell inflation that is still running well above its own estimates.

Interest-rate traders aren’t quite positioned for the Fed to keep tightening, with meeting-dated swaps assigning only about a 70% chance of an increase in July — and no hikes beyond then.

Over in Treasuries, front-end notes are trading at a rich premium. At the current level of around 4.60%, the two-year maturity is, based on historical correlations, trading as though the Fed is poised to cut its benchmark by about 50 basis points imminently.

The Fed’s benchmark rate is currently at the median rate indicated in its March dot plot. However, even back then, seven of 18 members thought a rate higher the current level would be needed to quell inflation.

Given that the Fed has adopted a slowly-slowly approach to guiding the markets toward a higher and higher benchmark rate, the median may well show the peak rate at 5.4%. This will prepare the markets for another increase in July. If any subsequent hikes are required, the Fed will rely on the September dot plot to do so.

If the Fed’s revised dot plot on Wednesday doesn’t show a shift, equities and Treasuries would almost certainly rally and the dollar would weaken on conviction that the central bank is done with its fight against price pressures. That would also suggest the Fed views its current rate as being sufficiently restrictive, meaning policymakers will adopt a cautious, calibrated approach from here given that the economy is losing momentum even in the face of a labor market that is pretty tight.

However, an application of the Taylor Rule shows that the restrictive rate for the US economy based on current inflation read-outs is 6.55%, a level that will make the bond market distinctly uncomfortable.

The Fed has successively raised its estimate of the peak rate that will be required for this cycle since September 2021. Back then, the Fed’s benchmark rate was 0.125% and the Taylor Rule recommended a benchmark of 5.38% — something the policymakers were acutely aware of. In other words, the monetary authority chose not to rattle the markets with the amount of tightening that would be required to cool inflation.

Even a modest tightening that is likely to be indicated in this week’s dot plot may still not be enough to get the job done on inflation. In the four months through April, core PCE has averaged 4.7%, way above the Fed’s forecast of 3.6% for this year.

Front-end Treasuries are still glossing over all this, and a hawkish dot plot may alter the trajectory of yields…

Think about that in context of 5yy above (and perhaps a move towards upper bounds of support — nearer 4.25% / 4.30% — is coming soon to a theater near you and me?

Point deserves a COUNTERPOINT and this one based on some MATH

CalculatedRISK Update: "Why Year-over-year Headline Inflation will Decline Sharply in May and June"

… The key point was that energy and food prices soared in May and June 2022, and as those data points are removed from the year-over-year calculation, the YoY change will decline sharply. However, core inflation does not include food and energy, so we won't see as dramatic a decline in core CPI and core PCE.

I posted this table showing the month-over-month changes that would be removed.

This shows the large increases in May and June 2022 for CPI and the PCE price index.

I've added the May CPI numbers, and an estimate from BofA for the May PCE numbers.

As the large increases in June last year are dropped from the year-over-year calculation, the YoY change will decline…

Now as that is off my chest — happy to hear any / all feedback as YOU choose a side, lets turn our attention TO … China

ABNAmro: China: Disappointing data, more easing BARCAP on China: Disappointing activity data to trigger more policy support GS China: May activity data slightly missed expectations, calling for more policy easing

More on any / all fronts later but … THAT is all for now. Off to the day job…

What's with these loaded contradictory phrases, such as Dovish rate increase, Hawkish 'skip', etc? But then Kissinger once said like 50 yrs ago, "when the American people believe up is down, the CIA's work will be done" (something to that effect). Thus, Men are now Women; Men, can get pregnant too. Happy Tuck week! Oops I most CERTAINLY meant Happy Pride Month yippie!!!!

What's with these loaded contradictory phrases, such as Dovish rate increase, Hawkish 'skip', etc? But then Kissinger once said like 50 yrs ago, "when the American people believe up is down, the CIA's work will be done" (something to that effect). Thus, Men are now Women; Men, can get pregnant too. Happy Tuck week! Oops I most CERTAINLY meant Happy Pride Month yippie!!!!

DDB keeps harking that China isn't leading the world out of the economic gutter this go-around....