A quick recap of week just past. Sunday evening - FDIC insures ALL deposits at couple troubled banks AND Fed weighs in with financing / bank rescue plan (BTFP) = 2yy down about 55bps. And THEN a couple days later CSFB gets 50bb from SNB and FRC gets 30bb from other larger banks. Last night we learn of the Fed’s discount window usage — finally — with a week lag showing there was in fact … interest,

The math (as twitted by WSJs Nick Timiraos),

NEW: Borrowing at the Fed this week

+$148.3 billion – net discount window borrowing +$11.9 billion – the new Bank Term Funding Program

Subtotal: $160.2 billion

+$142.8 billion – borrowing for banks seized by FDIC

Total: $303 billion

HEREis link to FED site with tables and details and last night, CNBC and others report,

And this on heels of 50bps HIKE by ECB … and all of this in mind, well, here we are … 2yy remain lower by about 70bps on the week,

I’m certain this means all is well … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher and off earlier lows after China cut banks' RRR by 25bp earlier this morning. DXY is lower (-0.2%) while front WTI futures are higher (+1.5%). Asian stocks were higher after yesterday's developments and stock market rebound in the US, EU and UK share markets are modestly higher while ES futures are showing -0.1% here at 7:05am. Our overnight US rates flows saw a relative and welcome calm during the Asian session with limited flows (2-way in the long-end) as 2's rebounded into the London crossover and then after into the NY open. Overnight Treasury volume looked very light (RELATIVE basis) at roughly 45% of the recent, ballooned average. Base effects in our volume sheet this morning.

… Our final attachment this morning looks at the freshly updated Bloomberg UST liquidity index. It measures the standard error across notes and bonds so a higher reading = less liquidity. Liquidity, by this measure, not quite as bad as it was near the end of last year nor as bad as it was during the March 2020 Covid panic. But it's still not great and this was backed up by discussions with the desk yesterday where some mentioned that the basis markets have been far more orderly (relative basis) than in spring 2020 and that they're able to offset most new risks in a reasonable timeframe still.

… and for some MORE of the news you can use can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

… The US has embraced recycling. As retail depositors have taken money from small banks to put into larger banks, larger banks are now taking money to deposit in smaller banks (or one bank in particular). This may stabilize the system in the near term, but in the longer term, some thought needs to be given to managing reputation risk in the social media age. For the economy, whether banks accelerate credit tightening is the key focus…

AND from a rather large French bank, an update of sorts,

Uncertainty in the near term: Although February’s NFP showed some cooling in wage growth and a slowdown in hours worked, the labor market remains tight with payrolls up by 311k, job openings still red-hot and unit labor costs revised higher. Moreover, core services ex-shelter remains hot in CPI and PCE indicators, while goods disinflation has slowed. Global inflation prints have also beaten estimates recently, and a reopening in China will likely spur growth, particularly in commodities. As such, we still expect the policy rate (UB) to reach 5.75% in July, with 2y and 10y UST yields respectively reaching 5.25% and 4.3% by Q2 2023.

However, the ongoing fallout at regional banks due to rapid deposit outflows have raised the prospects that the Fed could pause rate hikes as early as the next meeting. Given recession risks have increased as markets question whether this is a systemic issue across banks or not, the Fed could cut rates earlier than expected and steepen the US yield curve. Nevertheless, we believe the Fed’s Bank Term Funding Program will avert the need to alter the course of monetary policy (see US Banks: The macro and market implications of the SVB failure, dated 12 March 2023).

Once terminal fed funds is reached, let the rally begin: Given our forecast going into H2 2023, we see the 2s10s UST curve bull steepening back to 0bp by Q1 2024 (see Global Outlook Q2 2023: Unfinished business, dated 7 March). The Fed is likely to begin rate cuts in March 2024 and ultimately bring the policy rate back down to 4%.

In our view, the Fed will avoid simultaneously adding and removing accommodation by ending QT in Q1 2024. However, sticky RRP usage could bring this forward, or QT may extend through 2024 with policy still restrictive.

We also expect net US coupon supply, including QT and QE, to plunge in 2023. CBO deficit estimates have risen by an average of USD460bn for 2023-25. The debt ceiling precludes increased coupon issuance until late 2023, so we see the Treasury relying on USD1.2trn of net T-bill supply in 2023 before larger coupon increases in 2024. Absent a debt ceiling resolution, net T-bill supply should fall as extraordinary measures become limited ahead of the X-date. The T-bill curve is currently pricing a late August X-date, but it is still too early to tell given the uncertainty in April tax receipts (see US: Another year, another debt ceiling crisis, dated 14 February).

From rates TO shares (watchin RATES), a few words from Barclays,

Widespread de-risking across asset classes and the flight to quality borne out by an unparalleled drop in UST yields raises the possibility that financial stability concerns are taking precedence over other macro factors. The Fed's high-stakes decision next week will test the relative complacency of equity markets.

Stocks guys thinking / watching moves in rates … an actual STOCK related visual from Kimble,

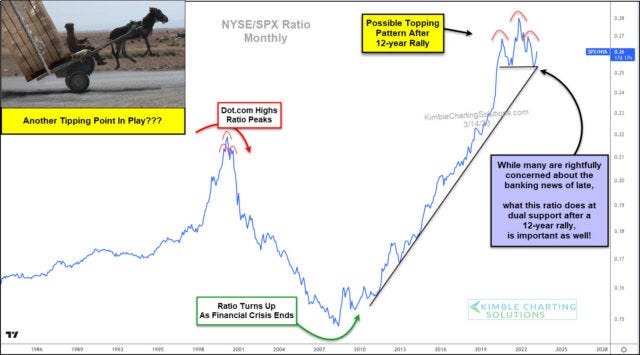

The New York Stock Exchange (NYSE) is a very broad measure of the stock market with over 2400 companies listed. So when the NYSE begins to underperform, market participants should pay attention!

Well, this has been happening over the past year… and it may be reaching a tipping point.

<ABOVE> is a long-term ratio performance chart of the New York Stock Exchange to S&P 500 Index. You can see how the NYSE has turned lower of late in a topping-like formation.

More importantly, we ask if this topping formation could be a head and shoulders pattern? The last head and shoulders pattern of consequence appears at the Dot.com highs. Yikes!

Currently, this pattern bounced off of 12-year uptrend support. But with the banking news of late, this ratio is still trading on thin ice.

If this thing tips over at this support level, it would send an important cautionary message to the broader market. Stay tuned!

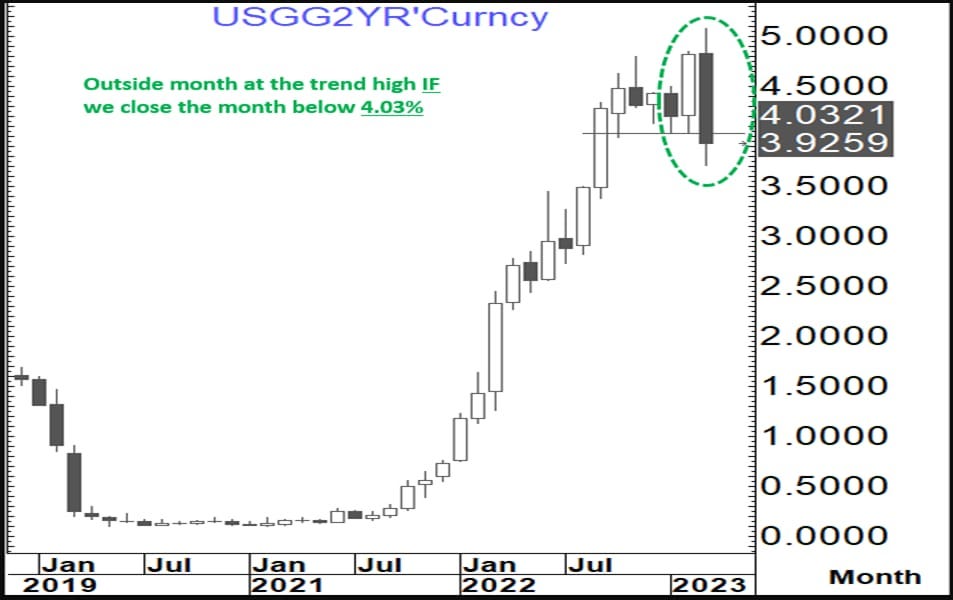

WATCHING … AND … back TO rates … from THE penultimate techAmentalists,

IF we close the month of March below 4.03%, we will post an outside month at the high of the trend confirming (in our view) the end of this interest rate cycle

This is what happened on the 5-year yield in November 2018 ahead of the final Fed hike on December 19th, 2018 (25 bp’s)

However, there are material differences here which are important

·That was a reversal on the 5 year yield which suggested it would lead the way lower ·This thereby suggested a bull flattening, which is what we saw ·At the time the yield curve was in positive territory, and this started the move lower to minus 15 by August 2019. ·This was the trend low in a low inflation world and led to a pre-emptive cut from the Fed and the start of the bull steepening.

This time around

·The potential reversal is in the 2 year yield suggesting it will continue to lead the way lower. ·The 2-year yield has a much stronger forward looking relationship to the Fed Funds rate . A basic rule of thumb in recent decades has been that if the 2 year yield inverts to between 120 and 140 basis points below the actual Fed Funds rate (upper band) then an easing is imminent. ·In 2019 the Fed was pre-emptive in that it eased rates both before the 2’s 5’s curve got to minus 20 to minus 25 bp’s (minus 15) and before the 2 year yield inverted so sharply to Fed Funds (It was inverted just over 90 bp’s) ·This development, if it takes place, would suggest a continuation of bull steepening which is much more closely associated with recession dangers and associated interest rate cuts. ·This is happening at a time when the 2’s 5’s curve just inverted to levels last seen in the 1970’s (inverted minus 77 in 1979)

Potential outside month at the trend high in the 2 year yield

Since it would appear I’m taking a VISUAL angle this morning, a large German operation offering SEVERAL CHARTS ‘from an unprecedented week in markets’ where the very first one caught my (and everyone else on Global Wall St) eyes

The 2yr Treasury yield saw its largest decline since 1982 on Monday… bigger than Black Monday 1987, 9/11 and the GFC…

These moves in yields ALSO come with updated Fed pricing,

Amid t all thi , we’ve een incredible volatility in Fed pricing… expectations of the December 2023 rate fell by 99bps in a ingle day on Monday…

With these moves — UNHEALTHY is putting it nicely — comes worsening LIQUIDITY in one of the deepest most liquid markets in the world. Back over TO Barclays,

Treasuries Worsening liquidity Treasury liquidity conditions are deteriorating as rate volatility has spiked, albeit unevenly across liquidity metrics. Spline errors increased at the front end, along with wider off-the-run bid-ask spreads. While on-the-run and CTD premiums did not rise by much, there has been a rising preference for futures vs. cash.

… Our markets dislocation proxy (Figure 1), which captures market variables sensitive to arbitrage relationships, show an increase in balance sheet stress and worsening liquidity. The proxy has generally coincided with the move in interest rate volatility, trending higher over the past year, given the Fed's aggressive hiking campaign and ongoing QT program. Over the past week, the proxy worsened, but not by as much as the rise in rate volatility would have implied. Rate vol has surpassed the level we saw after the UK LDI crisis last October, yet the move in the proxy was more benign.

Feel better? I don’t. It seems UST liquidity worsening and thematic … Finally, from our (unofficial)bank of the land, another FI related IDEA

… Long duration UST: top fixed income return potential; reduce credit exposure

Last month, in Bonds near the buy zone: 3.75%-4% 10y, we made the case for adding quality duration as the 10y yield headed into the 3.75%-4.0% range. Our preference was 30y UST. Ultimately, after briefly touching 4.09% intraday on March 2, the 10y yield quickly retraced lower, and now stands at 3.6% (Exhibit 8). Our new buy zone is 3.65%- 3.9%. The official BofA rates forecast still calls for a 3.25% 10y by year-end 2023. For the same reason that recession is likely to come sooner or in line with the BofA recession forecast, we think the risk to the rate forecast is to the downside and see a sub-3% yield as a distinct possibility. Moreover, the sooner than expected recession risk argues for a reduction of credit risk exposure. This means reducing exposure to our primary recommended sectors, floating rate bank loans and short duration high yield.

Recommendation: down in credit floaters + 30y UST; BUT reduce credit, increase duration. Value in fixed preferreds …

Safe to call the buy zone way above where we are here / now but hey, for us playin’ the home game with now broken brackets — THANKS Tigers — what else we got to think ‘bout? Hope YOUR brackets not as busted as mine …