Good morning … this mornings update will be short — I’ve taken the day off (Thing 3 ‘graduating’ 8th grade …) and so, today is as much about monetary policy report TO congress as it is about 20yy auction … but first,

ZH: Shocking Housing Starts Data: Economists Blown Away By 11-Sigma Beat After Biggest Monthly Surge On Record

AND about those 20s,

Seems to me that 4% or thereabouts is a level of ‘resistance’ one should be watching into / thru JPOW testimony later on … while momentum appears to be bullish input that might work against the process of a concession and in light of the overnight impulse (bearish from UK CPI somewhat muted by decent long end supply process in Germany) it is, as usual, anyone’s guess … a reminder of why I then should be thankful to no longer be forced to guess?

… here is a snapshot OF USTs as of 735a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly weaker and flatter, now recouping losses from the overnight bearish shock of unexpectedly higher UK Core CPI (7.1%YoY, highest since 1992). A strong 30y bund auction has seen long-end EGBs buoyed, risk-assets generally heavy with APAC indices souring on the ‘slow play’ of China stimulus measures (ChiNext Index -2.6%, HSI -2%, KOSPI -0.9%). The BoJ Minutes and Adachi statements out overnight were dovish-tilted, resulting in NKY (+0.6%) outperformance and a slightly weaker JPY (-0.2%). SOFR Flows were depressed (50% 20d ave) ahead of Fed Powell’s testimony today, cash/swap volumes not much better (~75% 30d ave) with better receiving seen post-UK CPI from RM in the belly. Some fast$ paying in 5s10s30s as well. S&P futures are showing -1.5pts at 7am, the DXY is +0.1% and CL futures are flat.

… and for some MORE of the news you can use » IGMs Press Picks for today (21JUNE) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

I’ll begin with something from a rather large German institution,

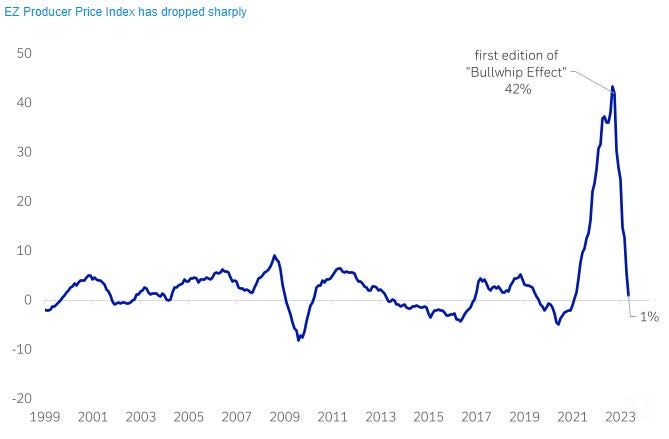

We turned from bears to bulls in November of last year when we published the first edition of the Bullwhip Effect. The Bullwhip concept describes how supply chain disruptions can lead to overstocking and subsequently to an oversupply of goods. Next to better supply in goods, we had passed the peak in energy prices and accordingly the risk of a severe energy-induced recession in Europe. Our hypothesis was that combined with weakening demand, this should lead to lower headline and goods inflation, improving investor sentiment, rising equity markets and an outperformance of the services versus the goods sector.

It worked. Since then, Eurozone PPI, which we highlighted in our first edition, has dropped from 42% to 1%. The EURO STOXX 50 has rallied 14% and we are witnessing the biggest divergence in services vs manufacturing PMIs in history. Our preferred services sector, Travel and Leisure is up 29% ytd.

And moving right along then a few more items of interest ahead of JPOW and 20s,

BBGs John Authers: If greed is good, when does 'greedflation' turn bad?

… In other words, the issue may be the very reverse of greedflation. Companies face a battle to maintain margins, and this will mean taking measures that hurt. Corporate margins haven’t had a great effect on the rise in inflation to date. They could have a profound effect on the way the economy moves next. And for stock pickers, companies that actually have the ability to maintain margins are likely to grow much more attractive.

BBGs Ed Harrison: US Inflation’s Minsky Moment Will Last Even as Rates Stall

When the Great Financial Crisis was raging some 15 years ago, it was described as a “Minsky Moment”, a phrase that has been used to capture the ideas by late economist Hyman Minsky on the genesis of major financial crises. His hypothesis on how excessive levels of debt can combine with inflated asset prices to destabilize the financial system has proved particularly prescient not just for the 2008 episode but also the 1998 financial crisis that originated in Asia. There’s a similar prescience for Minsky on inflation that might help us discern what comes next on that front. In the meantime, investors can lock in some returns offered by the higher yields.

…If you prefer to measure monetary policy by using shortterm rates, and do not think they’re high enough yet to bring inflation down to 2.0%, then you should also believe rates may go significantly higher from here. And yet markets are currently pricing-in a much more benign story for the months ahead.

The effects of monetary policy are long and variable, as Milton Friedman said many years ago. Right now, some investors may be drawing conclusions about its future path and effects way too early.

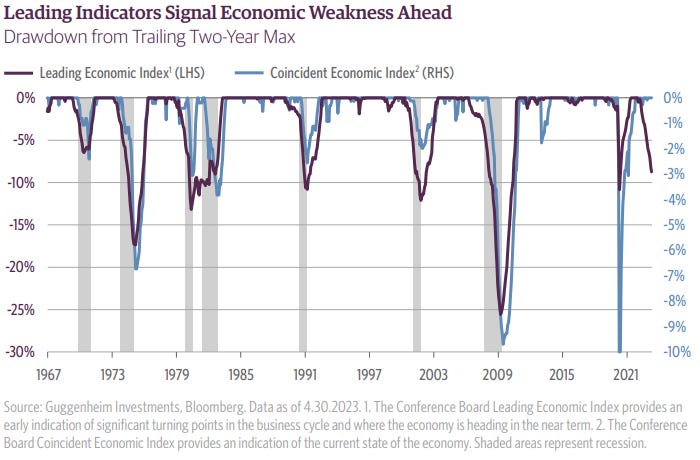

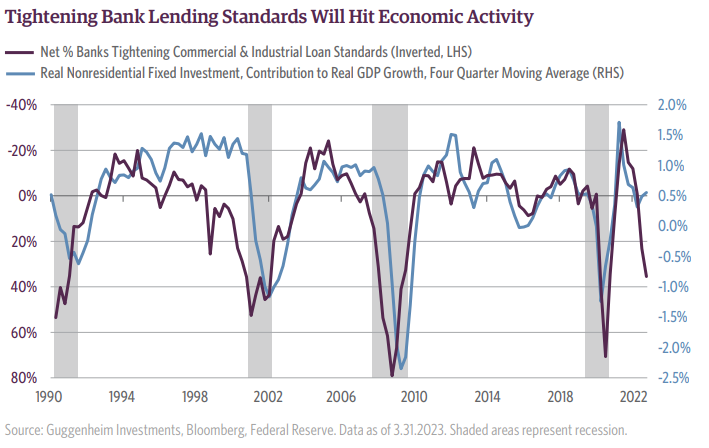

Chart of the Week Exhibit 1: We Lowered Our China GDP Growth Forecast to 5.4% for 2023 (vs. 6% Previously) on Persistent Property Market and Export Weakness

Quarterly Macro Themes, a new quarterly publication from our Macroeconomic and Investment Research Group, spotlights critical and timely areas of research and updates our baseline views on the economy. The work of this Group is a key input in our distinctive team-based investment process, which is designed to make better investment decisions in actively managed portfolios.

Each theme, drawn from current topics of focus for our investment team, is explained in short text and charts. Among the themes discussed in this issue:

A Fed-induced recession is still in the pipeline.

Tightening bank lending standards point to potential funding gaps.

Industry trends and labor market rebalancing suggest a more moderate recession severity.

Equity analysts, still expecting a “no landing” outcome, are in for a surprise.

The dollar’s status as the preeminent reserve currency remains secure.

Federal Reserve Chair Powell makes his semi-annual testimony to Congress today. There is more than a suspicion that the June pause in policy was part of a compromise to appease the Fed’s factions—with the promise of a hike in July the quid pro quo. Powell has tended to be reactive, focusing on current inflation rather than considering where inflation is going.

Given partisan divisions in the US, the questioning of Powell is likely to be made with an eye to political constituencies (with a focus on the causes of inflation). What economists would love to hear (but almost certainly will not) is an explanation of how Powell thinks inflation will contain profit-led inflation. Retailers’ profit share of retail GDP has risen from an average of a little over 14% in the pre-pandemic years to over 21% at end-2022.

Finally for those of use ‘visual learners’ a weekly macro chartpack,

• Despite equity strength seen in the US and Japan, European equities remain capped at key resistances and with glaring weekly bearish momentum divergences in place we maintain our defensive outlook.

• We thus continue to look for the Euro STOXX 50 to stay capped below key resistance from the 4,415 high of 2021 and for a more concerted correction lower to emerge, with a break below the 4,211 May low needed to mark a near-term top.

• Please note the House View has global equities as least preferred in a portfolio context on a 12-month horizon.

• The brief move to a new high in the DAX has been quickly reversed and with weekly RSI momentum posting another lower high we continue to look for a correction lower to emerge.

• FTSE 100 remains seen under pressure in its broader converging range and we look for a retest of key support from its uptrend from October, now at 7,502.

• In the US the strong move higher in the Nasdaq 100 has extended to our next target and what we see as tough resistance at 15,265/15,411 and we continue to look for this to cap and for a correction lower to emerge.

• 10yr US Bond Yields are expected to continue to hold key support at 3.85/3.91% and we maintain our bullish outlook, with a break below 3.58/56% needed to mark a near-term top to add weight to our view.

…A sustained move back below the 55-day average and June low at 3.58/56% is now seen needed to mark a near-term top for a test of resistance at the year-to-date yield lows at 3.29/265%, which could prove a tough barrier at first. Bigger picture though, we still expect yields to move lower in the 2nd half of the year and maintain our core 3.00% objective.

Above 4.085% though would suggest we have instead seen a significant break higher, opening the door to a move back to the 4.325% high of 2022, although this is not our base case

OUT … likely NOTHING from me tomorrow due to business travels and hopefully back Friday. AND for now, THAT is all for now. Off to the day job…

I wonder if I can get away with calling my nieces things #1 & #2! LOL that is hella creative and FUNNY, any man that can refer to their child as "thing" is alright by me!

enjoy your time off

I wonder if I can get away with calling my nieces things #1 & #2! LOL that is hella creative and FUNNY, any man that can refer to their child as "thing" is alright by me!