(USTs modestly steeper on light volumes)while WE slept; stress UP, nothing without consequence, debt ceiling and are safe havens still safe? Is it different this time?

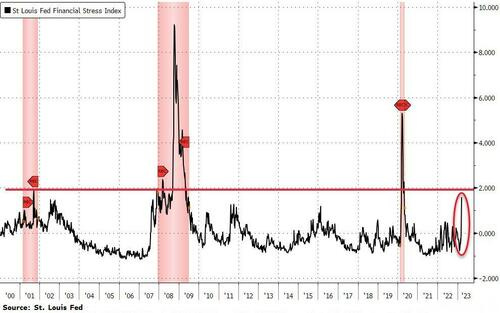

It’s not just the credit markets that are sending out a signal of distress. A key barometer that the Fed watches, the St. Louis Fed Financial Stress Index, is telegraphing a similar message about the state of the US economy.

While the spread between high-yield and investment grade debt captures one major variable, the Fed’s gauge comprises a host of yield spreads, interest rates and other indicators, making it a veritable one-stop-shop.

The average value of the index is intentionally meant to be zero, capturing a moment in time when the financial markets are in a “normal” state, with values above indicative of heightened stress…

Be that as it may, there was still some — not GREAT — appetite for 7yy yest,

ZH: Mediocre 7Year Auction Tails For The 5th Time In The Past 6 Months

AND so a mediocre day it was and is likely (hopefully?) to be today and so … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly steeper after a quiet overnight session, volumes still running light (60-70% 30d ave). There was limited fundamental inputs on offer overnight, the release of Germany’s NRW CPI prompting a minor rally across core EGBs. Initially, our desk saw better receiving going through from a mix of RM, Gamma and some clips from FM in belly of the curve. With spreads opening better offered in London, FM and RM treasuries bought on ASW. Flows out the curve were subdued, but in the very front end there continues to be some demand in short-dated bills (real$). Desk liquidity metrics indicate 85/100 despite tepid volumes as markets likely turn attention to the extension tomorrow. S&P futures are +23pts here at 7am, the DXY -0.3%, and CL +0.9%.

… and for some MORE of the news you can use » IGMs Press Picks for today (30 MAR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

Barclays offering an economic update and outlook whereby,

Global growth is being supported by China's reopening, the easing of Europe's energy crisis and US consumer resilience, but underlying price pressures persist. Banking turmoil complicates central banks' responses, but we expect wider crises to be avoided and policy rates to stay elevated once hiking cycles conclude in Q2.

China's reopening and the easing of Europe's energy crisis have led to a rebound in global momentum thus far in 2023, while US consumption remains supported by a buoyant labour market.

Tighter credit conditions should slow growth in H2, when we expect the US to enter recession, but global annual growth is predicted at 2.7%, including China (5.6%), US (1.2%) and Europe (0.5%).

Headline inflation has been moderating globally as energy-price effects fade, but core inflation dynamics in advanced economies have remained much more persistent.

We expect the Fed and ECB in 2023 to reach terminal rates of 5.0-5.25% and 3.75%, respectively, and to keep them unchanged through year end as they balance inflation risk against financial stability concerns.

And as the firm discusses how central planners are expected to do whatever it is they’ll do and bring inflation back down, they also discuss a theme I’m a forever fan of — namely how nothing happens without a consequence,

Monetary policy: Transmission impossible? Higher rates set to bite

The transmission of monetary tightening through the financial system is still playing out, but long and variable lags and a number of offsetting shocks are masking its effects on activity and inflation. The recent banking stress will accentuate the tightening pressures, but will not lead to a severe credit crunch.

Although interest rates have risen sharply and lending flows have slowed, monetary policy transmission to inflation and activity in the US and the euro area appears to have been more gradual than many had expected.

Potential reasons differ across jurisdictions, though some commonalities stand out. These include lingering supply and demand effects of shocks related to COVID and the Russia-Ukraine war that have overshadowed the effects of monetary policy, the likelihood that the unusually aggressive tightening will still play out with a lag, and the fact that monetary policy settings were initially well below neutral.

We suspect that recent banking stress will intensify the effects of the ongoing monetary tightening, rather than trigger a broad-based financial crisis and a severe credit crunch, which we view as unlikely.

Our econometric results suggest that this stress will contribute to lowering the level of real GDP after one year by0.25-0.5% in the US and 0.5-0.7% in the euro area. These would be substantially smaller than the effects that occurred during the Global Financial Crisis and the European Sovereign Debt Crisis, when the tightening in lending conditions was much sharper.

As a result of these additional effects, we believe both the Fed and the ECB are likely to raise policy rates by less (between 25bp and 50bp) than they would have otherwise done.

Carrying along with this theme of nothing happening without a consequence, MS chimes in with a different course of action will reap some … consequences?

Bottom Line: DC’s bank failure concerns don’t appear to have improved the chances of a timely debt ceiling resolution, keeping policy risk live for investors. Consider: 1) some Republicans have linked government spending to banking sector challenges, drawing a line from spending to the increase in interest rates that drove mark-to-market losses in bank portfolios; and 2) some lawmakers perceive the Fed and Treasury's telegraphed 'reassurances' as a signal that the government might be inclined to step in and prevent a full-blown default in the event of a missed payment. Taken together with the pre-existing incentives for both parties to not compromise early around the debt ceiling, this suggests enough lawmakers may see value in a drawn-out debate linking the debt ceiling to government spending.

Market attention could swing back to this issue soon: Tax receipts will roll in and offer clarity on the actual X date, giving lawmakers and investors something to focus on. Right now, that date is still a moving target within a range – between mid-June according to the Treasury's estimate, and later in August, according to our own – but should be narrowed down as we receive tax data. As we noted back in February, receipts and refunds will determine exactly how much cash is available in the TGA, possibly moving up or pushing out the date by which the Treasury's extraordinary measures will be exhausted.

Watch the t-bills market, which tends to be first to show signs of this debate being priced in: Observing a decade of debt limit episodes, one of the most common market reactions is the sell-off in T-bills that mature around the date by which the US Treasury is expected to run out of extraordinary measures and become unable to meet its obligations. T-bills have already begun to show these signs, with kinks emerging in the curve around the dates that investors have narrowed down to the possible dates by which a default becomes more likely. For now, the 'red zone' is appearing in August, but we expect it to narrow as we get more information on tax receipts in April.

AND so as the world turns and we’re all watching TBILLS (confirmed one cannot turn anywhere without having this conversation in most casual settings … more and more each day), begs the next question posed by Rich Bernstein

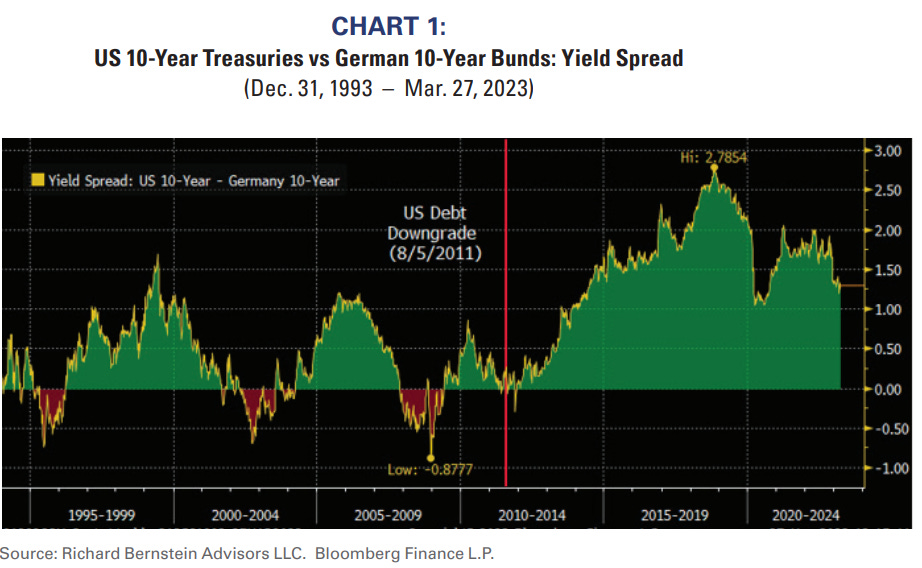

Is the safe haven still safe? Treasury bonds have long been considered the financial markets’ “safe haven” asset. That remains generally true, but investors should appreciate the risk of default is causing the financial markets to re-assess Treasuries’ superiority as a safe haven relative to other assets…

… The risk of a US default should nonetheless be fully appreciated. The markets re-priced Treasuries to account for the downgrade of US debt by Standard & Poors in 2011. The cost to the US government has more consistently been between 100-200 bps higher yield relative to German Bunds than it was prior to the downgrade (see Chart 1)

In other words, the 10-year T-note yield has carried a consistent risk premium to German Bunds since the downgrade of US government debt in 2011. Because all US debt prices off US Treasuries’ yields, the downgrade and subsequent increased risk premium means US corporate, municipal, and mortgage debt has also had an imbedded risk premium and higher associated interest costs…

… The US government 1-year CDS spread (i.e., insuring against default in the forthcoming year) is now higher than it was when US debt was downgraded in 2011 (see Chart 2), which suggests the markets feel the risk of default is higher than it was in 2011, and another US debt downgrade would likely further increase interest costs to the US government and to the overall US economy.

… The notion that 2011’s near-default was a non-event has proven totally false. Of course, financing costs would have been much higher if there actually had been an extended government default, but the US economy has nonetheless paid higher interest costs and experienced slower growth because of 2011’s fiasco.

Investors should appreciate another near-default or actual default could similarly result in a meaningful secular relative increase in US relative interest costs and slower US relative economic competitiveness and growth.

We remain overweight long-term Treasuries based on our view that US nominal growth will slow through time, as a hedge against more economically-sensitive equities, and the structural difficulties of holding German Bunds.

However, US Treasuries are clearly not the same safe haven asset they were prior to 2011’s downgrade of US debt, and we fully recognize a US government default could not only further jeopardize Treasuries’ status, but could also result in still higher relative US interest costs and the associated further loss in global competitiveness.

We’re also reminded by a rather large German bank how … it’s different this time (?) … and here are,

G7 core inflation peaked at 5.5%, a level not reached since the early 80s. This is in stark contrast with the past 25 years during which G7 core inflation never exceeded 2%. Most notably, underlying inflation in Japan is above 4% and still rising. We discuss the market implications of this simple observation and five ways in which this time is different from the past 25 years.

1- A hard landing should be base case… 2- It will require a bigger growth shock for central banks to ease policy. inflation is not far from target, slowing growth could be enough for central banks to expect inflation to be soon at target and the market to anticipate easier monetary policy. However, if inflation is significantly above target, there should be a "longer fuse" between slowing growth and a central bank pivot. As a result, growth signals won't be enough to dictate the duration view. For instance, traditional growth and cross-asset proxies of UST10y would have wrongly suggested being long duration almost a year ago and are currently consistent with sub 2% UST10y.

3- Once initiated, the easing cycle should be deeper 4- Risk parity is on shaky foundations 5- Japan moving out of deflation will have significant implications.

Clearly I’m drawn to #s 2 and 5 the most but … then that would be agreeing it IS in fact different this time and, well, we all know how that usually works out … THAT is all for now. Off to the day job…