Good morning … A new day and a new month begins and with that, a quick look at 5yy MONTHLY

I spy with my little eyes a peak in October as well as a turn in momentum (stochastics, bottom panel) and while todays FOMC meeting and presser could shake up the snowGLOBal macro a bit, lets circle back to this one as the days / weeks just ahead unfold … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly richer/flatter as we enter February, EGBs underperforming after EZ inflation saw another core beat/headline miss. Volumes were sub-par overnight, our Tokyo desk noting a quiet period for lifers, the JGB bull-flattening driven by foreign buyers ahead of next week’s expected announcement of a new BoJ Governor. A 4k FV buyer in pre-London saw the belly supported, a 450k TY-WN steepener after the London crossover modestly bull-steepening the curve pre-inflation data. Final PMI readings across Europe saw little nuance (save Switzerland’s sharp drop), while continental equity futures sit close to home (Dax +0.1%). S&P eminis are -12pts here at 7am, while Crude is +0.6% and the DXY is a bit cheaper at -0.2%. UST franchise flow was relatively mixed with better receiving in the short end but also better paying in 10y via outright and 5y5y structures. Spreads 5s to 30s are marginally wider across the curve.

… and for some MORE of the news you can use » IGMs Press Picks for today (1 FEB — and STILL SPORTING THAT NEW LOOK!!) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

ABNAmro on EZ:

Eurozone resilience won’t last Eurozone Q4 GDP came in stronger than expected, expanding by 0.1% qoq, whereas a 0.1% qoq contraction was expected. However, there was weakness under the surface and we still expect GDP to contract moderately during most of 2023, as most of the impact of past and upcoming rate hikes, and the tightening in financial and bank lending conditions, is still very much to be felt on the economy. Indeed, further evidence of the negative impact of interest rate hikes by the ECB on the eurozone economy was provided by the latest ECB Bank Lending Survey (BLS), which showed that banks tightened credit standards for all types of loans in Q4, while loan demand collapsed.

Well THAT isn’t so terribly optimistic … Let’s check in with UBSs Paul Donovan

Rates rise as inflation rates fall The US Federal Reserve is expected to raise rates, slowing the pace of tightening to a quarter point. Fed Chair Powell’s chant of “hike, hike, hike” seems to be running on autopilot. The press conference still suffers from Powell’s June policy errors, when forward guidance was trashed.Markets have less reason to believe forward guidance, forcing the Fed to be ever more implausibly shrill in its statements about future policy.

US labor market data comes with the release of JOLTS numbers, which include “vacancies”. The survey response rate for this data has collapsed, making the quality questionable. The vacancy number does not report actual vacancies, only externally advertised vacancies. Hiring rates are very high, suggesting a lot of the “vacancy” rise post pandemic has been about people changing company…

… Which assets saw the biggest gains in January? … Sovereign Bonds: After an awful 2022 performance, sovereign bonds have had a very strong start to the year, with gains for US Treasuries (+2.8%), Euro Sovereigns (+2.4%) and UK gilts (+2.8%). For US Treasuries, it marks their second-strongest monthly performance since the height of the pandemic in March 2020

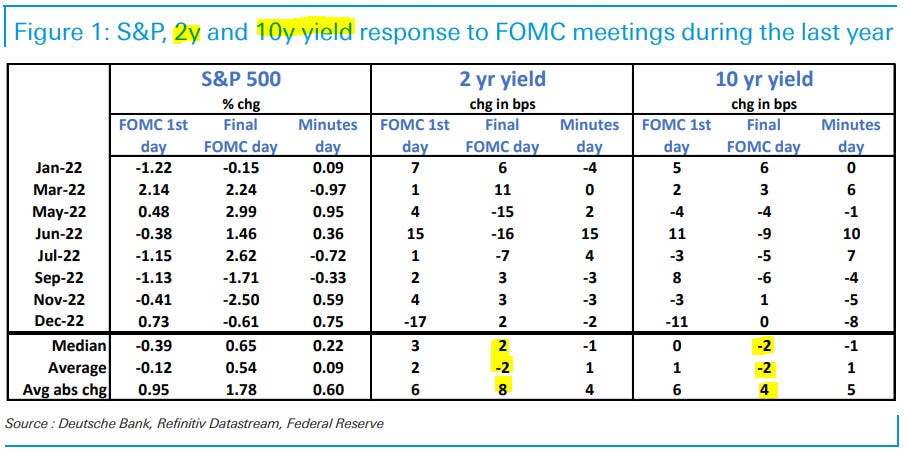

Same large German bank but a different stratEgerist thinking about FOMC later on today and offers some (visual) insight as to history of markets moves over past year

From trading the Fed to attempting to index or benchmark the current day Fed experience to various years of experience which have now gone by … the very same large German bank CoTD

… So, how do we benchmark current monetary policy relative to the past episodes of rising inflation, and how extreme the recent Fed hikes appear when viewed in a broader metric? The first logical step in that direction is to compare the current cycle with the Volcker’s Fed of the late 1970s. In many ways, the last 12 months of equity and inflation trajectories resemble the first year of rate hikes in 1977. When put side to side with each other, the extreme nature of the current cycle becomes visible both in nominal and inflation adjusted terms. We organize this in the Figure by displaying the trajectories of both inflation and S&P prices (indexed to the time of the beginning of each cycle) as a function of time from the first hike. We note that, while inflation trajectories in both cycles are practically coincident, the relative drawdown in 2022 is even more severe than in the late 1970s.

… In an adverse (low-probability) scenario of no-landing corresponding to persistent inflation and continuation of rate hikes beyond H1 of this year, equities are likely to continue to underperform with their correlations with rates pushing deeper into negative territory. We believe that equity/rates hybrid structures are the right hedges for this outcome.

Turning attention away from this large German operation and the Fed and pivoting (see what I did there) TO a Swiss operation and some (WEEKLY) charts,

… Reinforcing the case for a cap though is the failure for Nasdaq 100 to break the top of its range and the reversal back below the 200-day average, which points to another swing lower within the range …

… especially as the market remains highly correlated to 10yr US Bond Yields, which look set for a reversal back higher into their range after holding above the 200-day average at 3.33%, with a short-term base threatening and short-term momentum turning higher. However, in contrast to the equity market, we would use any backup in yields as an opportunity to increase duration exposure.

Aaaaaand … THAT is all for now. Off to the day job…