Good morning … Especially if one is looking to borrow money in China as their big state banks CUT DEPOSIT RATES

China's biggest banks on Thursday said they have lowered interest rates on yuan deposits, in actions that could ease pressure on profit margins and reduce lending costs, providing some relief for the financial sector and wider economy…

We can / should consider what central banks are doing a bit more, just below BUT if / when this triangulated TLINE breaks …

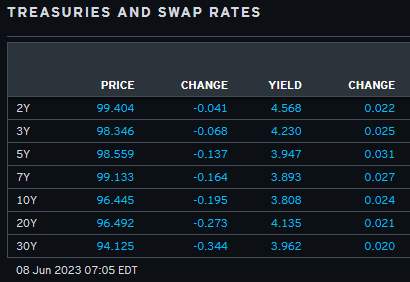

… I’ll be forced to find a thicker / newer / better crayon to redraw and MOVE the proverbial goalposts … but in the meanwhile … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower as the NY session opens with the belly showing a hint of outperformance on curve. DXY is lower (-0.25%) while front WTI futures are higher (+0.75%). Asian stocks were mixed (China up, most others lower), EU and UK share markets are modestly higher (FTSE 100 UNCHD) while ES futures are also UNCHED here at 7:07am. Our overnight US rates flows saw real$ buying in 10's to 30's during Asian hours, flattening the curve then. We got no other color and overnight Treasury volume was about average overall with 7yrs (131%) seeing some relatively active turnover overnight.

… Our last attachment shows the latest update of the MOF's net foreign bond flow from Japan. Contrary to fears of Japan putting hands down for Treasuries, the week ending June 2nd saw the 4th straight week of net foreign bond buying from the country with the 4-week moving average up to one of the higher levels seen in recent years.

… and for some MORE of the news you can use » IGMs Press Picks for today (08 JUNE) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

First, I’m wondering IF this is how the FOMCs ‘pause’ which refreshes is to end ..

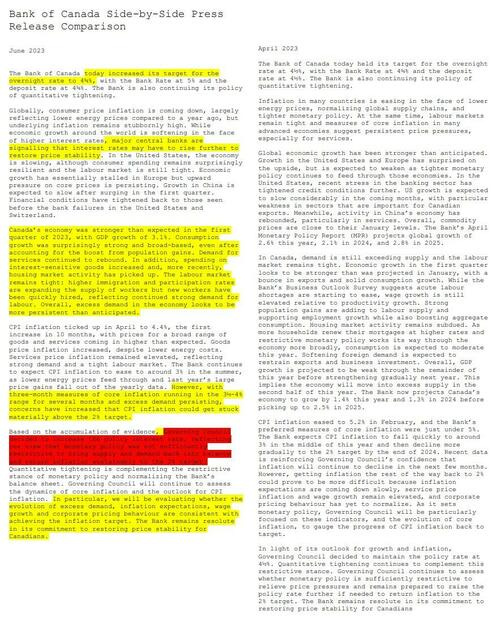

ZH: Bank Of Canada Ends "Pause" With Unexpected Rate Hike To 4.75%, A 22-Year High

… As Bloomberg reminds us, the Bank of Canada was the first and only Group of Seven central bank to pause its hiking cycle. Now it’s changed its mind, conceding that higher borrowing costs are still required to bring inflation to heel in an economy that’s proving more resilient than anticipated.

Understandably, the central bank also removed the April language about being prepared to raise rates further if needed. Here is a full redline comparison between the two most recent statements:

BoC chief Macklem and his officials pointed to elevated three-month moving measures of underlying price pressures as a key reason for their move. “Concerns have increased that CPI inflation could get stuck materially above the 2% target,” they said…

Perhaps some of the reason behind UST selloff? Canada. RBA … ? FOMC next? Askin’ for a friend (who used to be more intimately involved and aware of reasons for moves like these in US RATES.

Moving along then TO the aforementioned rate CUTS from China and in light of re hikes by Canada,

… China’s state banks have been reducing deposit rates. This might encourage consumers to put savings to work in the economy—but it depends on how money is being saved. If savings are being held as insurance against future uncertainty, rate cuts are less impactful. Rate cuts hint at some concern about domestic demand...

Speaking of troubled domestic demand, China’s not alone …

Wells Fargo: Export Flop Causes U.S. Trade Deficit to Widen to Six-Month Low

U.S. exports slipped by the most since pandemic-related lockdowns in 2020 in April, pushing the U.S. trade deficit to its widest in six months. Some one-off factors are to blame for the weakness, but the data continue to demonstrate an unusual volatility in trade flows. Net exports are tracking to be a meaningful drag on Q2 GDP growth.

It’s apparently a THING not specific TO any one country …

ABNAmro: Global industry and trade in the doldrums | Insights newsletter

Orders and production data for April illustrate that Germany’s manufacturing sector is suffering further from weak demand. China’s foreign trade data for May are a reminder of prevailing headwinds to Chinese and global growth.

All this may very well then add up to a Fed PAUSE but then … Bank of Canada tried that and along with RBA, provided some hawkish surprises … Perhaps here in the USA it will come down TO CPI

BNPs US CPI preview: April-fooled by “revenge spending”? May data to reveal true core services trend

KEY MESSAGES

We expect modest improvement in the May CPI report, with the headline rate ticking down to 0.1% m/m (consensus: 0.2%, prior: 0.4%) and core CPI slipping to 0.3% (consensus: 0.4%, prior: 0.4%).

The trend in CPI non-housing services inflation should continue to decelerate (to 5.4% y/y from 5.8% prior), but it remains well above a pace that suggests a return to 2%.

A turn in categories associated with “revenge spending” (such as airfares, hotels, event admissions and car rentals) drove most of last month’s improvement in non-housing services inflation and could do the same in May. The Fed’s target PCE price index also showed more limited progress on this front than in the CPI. Fed officials are likely to remain wary about sounding the all-clear for the key non-housing services inflation subset.

Looking beyond May, core inflation is likely to moderate as used vehicle and shelter cost inflation subsides. However, we continue to believe a more material weakening in the labor market will be required to return non-housing services inflation – and inflation more broadly – all the way back to target-consistent rates.

… The last bit is the hardest: In our view, this year’s key inflation theme is the distinction between improvement – easy to achieve – and returning fully to the Fed’s 2% target – a much harder task.

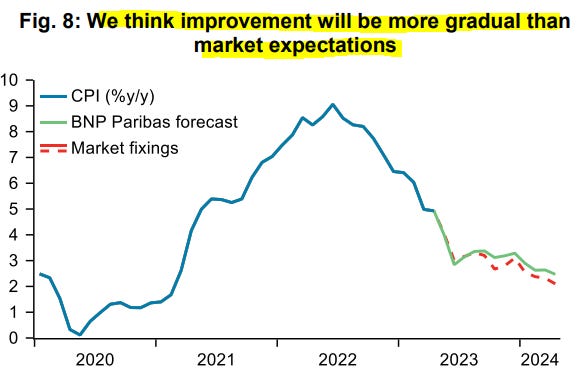

Indeed, even with the aforementioned factors helping to drive inflation lower over the next several months, at 3.2%, our 2023 q4/q4 headline CPI forecast remains well above the Fed’s target and solidly above current market fixings (which as of 5 June forecast 2023 q4/q4 headline CPI at 2.9%). Said differently, while we expect inflation to improve this year, we retain a view that inflationary pressures will prove more persistent and inflation progress more gradual than current market expectations (see Fig. 8).

We see no automatic path back to target inflation from here – to the contrary, our 2024 q4/q4 headline CPI forecast of 2.2% to a large degree is conditioned on recession that we envisage beginning in H2 2023 and extending into Q1 2024. Absent such a downturn and a corresponding loosening in the labor market, we think there is a good chance that inflation levels out at around these 3% levels.

From a CPI pre-cap and victory lap (?) TO an FOMC preview which ultimately awaits the CPI data next Tuesday,

MS FOMC Preview: June Meeting | US Economics & Global Macro Strategy

We expect the Fed to hold the policy rate steady at 5.1% while maintaining a tightening bias. We think the data will not meet the bar for a July hike, and the Fed remains on extended hold until the first cut in 1Q24. Our strategists stay neutral on US Treasuries, and maintain long USD positions.

… Our rates strategists see limited scope for markets to price any higher terminal rate or fade any of the current rate cuts at the upcoming FOMC meeting. They stay neutral tactically, waiting for the CPI print next week.

… The rates market prices nearly a 75% cumulative probability of one hike by the July FOMC, currently split between a 25% chance in June and 50% in July. The use of the word "skip" instead of "pause" by some FOMC members has introduced the idea for markets that no hike in June could simply increase the probability of a hike in July (see Exhibit 4). Our economists expectno hike in June, which ultimately translates to an extended pause through 1Q24.

… Overall, we see limited scope for markets to price any higher terminal rate or fade any of the current rate cuts at the upcoming FOMC meeting. We stay neutral tactically, especially as we wait for the CPI print next week. We think that the market is ripe for a bullish turn in the medium term (see our rates outlook) but prefer to go past CPI to evaluate the next trades in the rates market…

On THOSE FOMC dependent notes, here are some employment related thoughts… a few words from Eric

EPB: Where The Unemployment Rate Is Rising The Most

… When we dig down into the state-level data, we can see that almost 90% of states have an insured unemployment rate that’s higher today compared to one year ago. This looks clear-cut recessionary.

But, if we stick with the theme that 2022 was artificially low and look at the percentage of states with an insured unemployment rate higher than our 2018/2019 pre-COVID baseline, the number drops to about 30%.

Notably, the trend is rising in both cases. Only about 5% of states had an increase in the insured unemployment compared to the pre-COVID baseline at the start of 2023, a percentage that has increased steadily throughout the year.

So which states are leading the recession? Let’s start by looking at states with an insured unemployment rate higher than 2022. As we know, this is about 90% of states, but we’re going to find the worst states or the states with the largest increase in the unemployment rate.

The states that are most “red” are the states that are showing the largest year-over-year increase in the insured unemployment rate. At the top of the list, we have Massachusetts, Oregon, Washington State, and California…

…The percentage of states or the breadth of the change is increasing as well, which means the broader economy remains on the recessionary track.

If you enjoyed this post, join our email list for more articles and samples of our premium business cycle research.

Finally a couple of PICTURES for us visual learners and from professionals as mine above leave lots to be desired. First up a weekly macro chartpack,

… 10yr US Bond Yields ideally stay capped at 3.91/3.92%

US 10yr Bond Yields have settled into a range over the past week after recently backing away from key support at 3.91/92%, in line with our bias for a cap here. This zone included a cluster of retracement levels, a gap support and the downtrend from the 2022 high. With the market holding below this zone and particularly below the February high at 4.085%, the core trend is still pointing gradually lower in our view, with the market making “lower lows” and “lower highs” since October 2022. Going forwards, a sustained move back below the 200-day average at 3.645% should be sufficient to confirm that the prior correction higher in yields is over and that the broader, steady downtrend is resuming, with next resistance seen at the year-to-date yield lows at 3.29/265%, which could prove a tough barrier at first. Bigger picture though, we still expect yields to move lower in the 2nd half of the year and maintain our core 3.00% objective, especially as both Real Yields and Inflation Breakevens look as though they are forming negative patterns (i.e. both BEs and RYs have the potential to move lower over the medium-term in our view)…

… AND this next one is one I just stumbled upon and it was written / sent June 5, but related TO 10yy

… At present, the real 10-year Treasury yield is only 8 bps below where it was when bond yields peaked last October. Meanwhile, the 10-year TIPS breakeven inflation rate is 33 bps lower (Chart 1). With inflation now in a downtrend, the inflation component of yields is reasonably valued. For its part, the real component of yields will have a hard time moving higher unless the Fed leans into rate hikes in the second half of the year (something we don’t expect).

AND with all this Canadian smoke invading the NE, some are able to capture the moment and I’ll leave this here — a friend posted view of the amazing skyline from his window