Good morning … really gotta admit I don’t care WHAT all the inputs are (Beige Book, US, EZ data, stocks, Fed) — many are touched on just below — as much as I care about and try to stay informed by PRICES. And with that in mind, 10yy holding OCTOBER 2022 levels (~4.33%) …

… the GOOD news is we’ve gotten oversold (stochastics, bottom panel) and it appears (bearish, overSOLD)momentum stalling and possibly on verge of a (bullish)cross. Suppose that it’s much easier to LIKE bonds here and now, especially as I thought were a ‘screaming buy’ … and in light of the Fed’s BEIGE book yest.

ZH: Ominous Beige Book Warns Consumers "Exhaust Savings" As Recession Mentions Soar To 5 Year High

AND … here is a snapshot OF USTs as of 706a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher and the curve steeper this morning, perhaps dragged along by the bull-steepening in the UK Gilt market this morning after weak housing data there. DXY is higher (+0.12%) while front WTI futures are lower (-0.65%). Asian stocks were lower (NKY -0.75%, SHCOMP -1.13%), EU and UK share markets are mixed while ES futures are showing -0.35% here at 6:55am. Our overnight US rates flows saw a pivot steeper in the curve with our desk seeing better real$ buying in the front-end out to intermediates. Overnight Treasury volume was about average overall with some elevated turnover seen in 2yrs (158% of ave volume).

… Treasury 5yr yields, weekly: Treasury 5yrs still respecting support derived by some weekly move highs in yields (~4.45% area) back in November. The bear trend in place since May is drawn in and while medium-term momentum still sits at 'oversold' levels, there is no hint yet of an impending bullish flip that could signal the beginning of a sustained push to lower rates. Simply, 5's appear stuck in a bearish vise: bounded above by range support and below by still-bearish trend conditions.

WATCHING … we’re all fishin’ in the same TA pond here and watching / waiting for participants to act LIKE the mkt is a ‘screaming buy’ … and for some MORE of the news you can use » The Morning Hark - 07 Sept 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Apollo - 31% of All US Government Debt Outstanding Matures within 12 Months (ruh roh, RelRoy)

One source of upward pressure on US rates is the $7.6 trillion in US government bonds that will mature over the coming 12 months, see chart below.

Recent incoming data for light vehicle sales, factory orders, and the overall trade deficit had positive effects on our Q3 GDP tracking estimate, which increased to 3.4% q/q saar. Implications across spending categories are mixed, with net exports and structures stronger, but consumer spending, equipment and CIPI weaker…

BlackROCK - Favoring short-term bonds long term (okie dokie … makes sense. enter the ‘build it and they will come’ Field of Dreams video now, please)

We up short-term sovereign bonds on attractive yields and downgrade credit in the long run. We stay cautious on long-term bonds even with the surge in yields…

… Sovereign bond yields have surged this year, with U.S. long-term yields hitting 16- year highs last month. We prefer short-term government bonds over credit. We go underweight high quality credit on a strategic view of five years and longer and trim our overall underweight to sovereign bonds. We still see investors demanding more compensation for holding long-term bonds given higher inflation, greater macro volatility and rising debt levels. We also like inflation-linked bonds.

We believe the new regime of greater macro volatility calls for more nimble and dynamic strategic views. Short-term government bond yields have risen alongside long-term yields due to rapid central bank rate hikes. That move has pushed shortterm U.S. Treasury yields (yellow line in the chart) near high quality credit yields (orange line), making short-term bond income comparable. We trim our overall underweight to developed market (DM) nominal government bonds to lean into short-term paper and reduce investment grade (IG) credit to underweight from neutral. We think high quality credit offers limited compensation for any potential hit to returns from wider spreads and sensitivity to interest rate swings. We prefer higher yields in private credit and see alternative lenders filling a corporate financing gap as banks curb lending…

… Bottom line: We evolve our views with the August update of capital market assumptions and strategic portfolios. We up our allocation to short-term sovereign bonds, trim our overall underweight to nominal government bonds and cut IG credit to underweight. We stay underweight nominal government bonds overall due to the risks we see in long-term bonds. We favor inflation-linked bonds. And we like equities in the long term. Their returns should surpass fixed income returns when growth rebounds from the near-term stagnation we expect – even if it muddles along due to the demographic hit ahead.

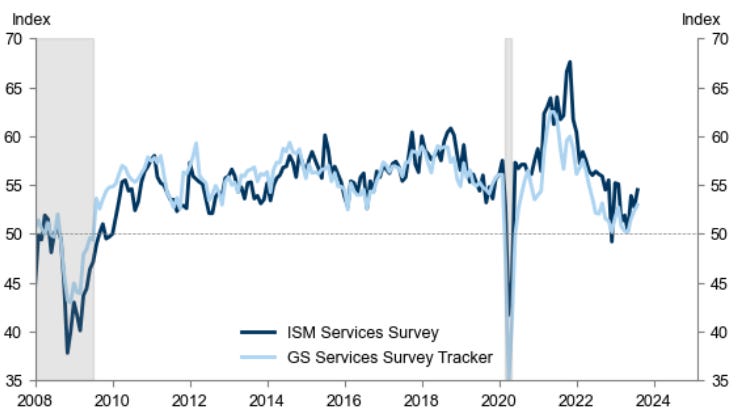

ISM Services in August outpaced expectations at 54.5 vs. 52.5 seen and 52.7 prior - the highest read since February. The underlying details were firmer as well with prices paid rising to 58.9 from 56.8, employment climbing to 54.7 from 50.7 (highest since Nov 2021) and new orders improved to 57.5 from 55.0. While the relevance of the data is diminished on the margin given the post-payrolls timing of the print, the services update is nonetheless relevant to persistent no-landing optimism.

The Treasury market responded in bear flattening fashion with 2-year yields returning to 5-handle territory while 10s crossed 4.29%. ISM services is the only top tier data of relevance this week, and once the dust settles we expect investors' attention will return to the corporate issuance calendar with the bearish implications that holds for Treasuries. We wouldn't look to fade the selloff until 4.32% 10-year yields given the momentum backdrop; that level is support as an opening gap from late-August which is just before the cycle high yield at 4.362%

DB - The top down case for a US recession (not mincin’ words here … rare these days rather than sellin’ the HOPIUM … or, runnin’ some real ‘career risk’ here but then again, seems entire firm behind this idea)

The US data has undoubtedly been stronger than expected. This has led many forecasters and the market to price a soft landing as the modal outcome. However, from a top-down perspective, a US recession remains more likely than not.

Given the inherent uncertainty around the level of the neutral rate and monetary policy lags, the odds of the Fed setting monetary policy exactly right are relatively low. As a result, the risk management choices made by the Fed should be relevant in determining the ultimate outcome. Given that inflation peaked significantly above target, the Fed should err on the side of tightening too much, rather than too little.

A soft landing could still be achieved if the Fed is "lucky". In the current context, luck would be defined as the economy experiencing a positive supply shock that reduces the risk management trade-off faced by the Fed.

In turn, the likelihood of a positive supply shock depends on the extent to which the post covid inflation was mostly driven by negative supply shocks, or by excess demand. The supply side did play a role in pushing inflation higher and some of these factors have normalised (supply chain bottlenecks and the participation rate). However, other supply factors are likely to be more structural (reshoring and the climate transition) and, more importantly, excess demand played a significant role as well.

Thus, it remains likely that bringing inflation back to target will require the Fed to depress demand below potential. Taking into account the risk management considerations, this tightening cycle should ultimately result in a more substantial increase in the unemployment rate. In turn, this implies that the trough in policy rates in the next cycle should be below rather than above neutral.

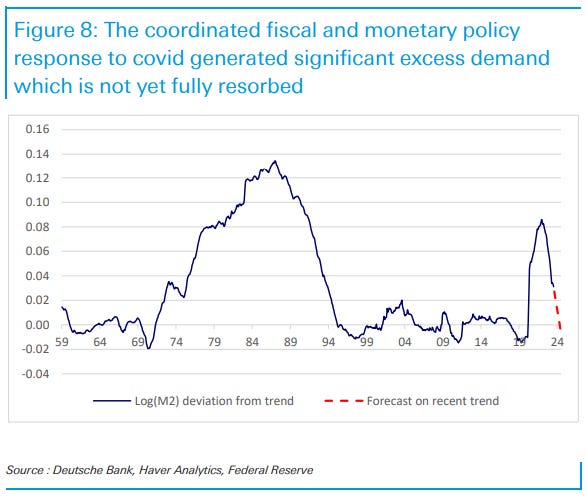

… The scale of the coordinated monetary and fiscal policies response resulted in the largest deviation of M2 relative to trend since the 70s. Since the Fed started tightening policy, the M2 overhang has been declining steadily, but the adjustment is not yet complete. On current trend, the M2 overhang would be reabsorbed by early Q2-24. If this is a correct proxy for "excess demand", it is likely that the pressure on the US economy would become more evident early next year.

In short, some of the negative supply shocks observed during covid have been unwound (supply chains and the participation rate). However, other post covid supply shocks are likely to be more structural (reshoring and the climate transition) and excess demand is likely to have been a significant contributor to the rise in inflation. Thus, it remains likely that bringing inflation back to target will require that the Fed depresses demand and brings GDP growth below potential. Moreover, from a risk management perspective, the Fed should err on the side of tightening too much rather than too little. Taken together, it remains likely that this tightening cycle will result in a more substantial increase in the unemployment rate. In turn, this implies that the trough in policy rates in the next cycle should be below rather than above neutral.

Goldilocks - USA: ISM Services Above Expectations (sure sounds like Fed who’s gonna have to CUT rates soon…? cuz, you know … services?)

BOTTOM LINE: The ISM services index increased by 1.8pt in August, above consensus expectations for a small decline. The composition of the report was firm, as both the new orders and employment components increased by more than the headline index.

Goldilocks - USA: Trade Deficit Below Expectations; Boosting Q3 GDP Tracking to +3.1% (sure sounds like Fed who’s gonna have to CUT rates soon…?)

BOTTOM LINE: The trade deficit widened less than consensus expectations in July. July goods exports were stronger than our previous assumption, and we boosted our Q3 GDP tracking estimate by 0.2pp to +3.1% (qoq ar). We left our Q3 domestic final sales growth forecast unchanged at +2.8%.

The US service sector ISM surprised to the upside in August and while not at very high levels is consistent with US growth accelerating in the third quarter. There are doubts as to how sustainable this will be, but the rise in the inflation component will keep hawks wary even if they do indeed go with the majority and vote for a pause on rate hikes in two weeks …

… Inflation concerns to keep the hawks wary amid data uncertainty The prices paid component rising to 58.9 from 56.8 is a concern though and is likely to keep the hawks wary even if there does seem to be a consensus amongst Federal Reserve officials that it can afford to pause in September and assess the situation again in November. Interestingly S&P's PMI measure for services, also released this morning, told a very different story. The headline index dropped sharply to 50.5 from 52.3, indicating barely any growth with its employment measure weakening and its prices measure recording their lowest reading since February. Just shows you how tricky it is to get a clear reading of what is going on in the economy right now and reinforces the view that a pause at the September FOMC makes sense.

■ The ISM Services PMI improved to 54.5 in August from 52.7 in July, coming in above the consensus of 52.5. This is the highest reading since February. ■ This series had been showing steady deceleration from the explosion of reopening activity in 2021 through the first half of 2023. The index dipped below 50 in December 2022, and also recently got close to contraction territory at 50.3 in May. The improvement since May shows some encouraging signs of a bottom, and evidence of a resilient economy.

… We still believe that much of the pressure that fuels inflation is rooted in sticky-high unit labor costs in the service sector. Lower skill, low productivity jobs used to be very easy to fill inexpensively with cheap labor. These jobs were becoming somewhat more difficult to fill in the years before COVID but the pandemic accelerated those trends as workers took advantage of higher-paying job opportunities offered by desperate companies seeking to meet reopening/revenge demand …

In one sense the global economic story is very clear—but is it obvious enough even Federal Reserve Chair Powell will notice? Cooling consumer goods demand is keeping disinflation pressures alive. China’s August export data showed another (expected) significant drop. The data is now consistent with counterparts’ trade data (unlike earlier this year when China reported exports no one seemed to be importing).

German July industrial production fell again, even with energy production flattering the data. Consumer goods production growth was negative. Of course (being German data), the previous month was revised, and was revised higher.

On the other side of the supply-demand balance, the Fed’s Beige Book of economic anecdotes reported cooling consumption, highlighting disinflation forces in manufacturing and consumer goods. US consumer durable goods prices have been in deflation since December 2022, one of the most dramatic reversals of inflation pressure in modern times.

US productivity and unit labor costs are due. Wage growth influences consumer spending power, labor costs influence either profits or inflation—the difference between the two is productivity (how hard people work). In real time this is an unreliable number. UK reported productivity just increased, not because people are working harder in reality but because there were significant revisions to GDP.

The fastest pace of rate hikes in a generation temporarily slowed activity in the service sector, but the ISM Services Index rose to a six-month high in August as the prices-paid measure climbed for the second-straight month.

From the intertubes,

CalculatedRISK: Fed's Beige Book: "Growth was modest during July and August"

AND finally, for the techAmentally minded and visual learners,

Brent Crude Oil has in our view established a medium-term base above key price resistance stretching back to Q4 last year at $86.49/89.37. This suggests the core trend has turned higher and we look for a more meaningful rally to emerge, with the next and initial resistance seen at $96.48.

Such a base in our view has significant and worrying cross-asset implications with CS Global Risk Appetite already holding a top to warn of further “risk off”, 10yr US Real Yields holding a large bearish continuation pattern and expected to rise further, and equity markets seen at risk to a more concerted downturn.

Please note the House View has Brent Crude Oil as most preferred on a 12-month horizon.

10yr US Real Yields continue to hold a large bearish continuation pattern following their break above 1.82% and we look for a further rise in yields to 2.15/2.21% next…

…with 10yr US Bond Yields expected to retest their long-term support at 4.36/4.46%.

The S&P 500 is expected to turn lower for a retest of support at 4,356/28. Below here and then 4,302 would be seen to mark a top to warn of a decline to test a cluster of supports at 4,195/4,167, including the 200-day average…

sorta why it bothers me when they talk 'bout hurricanes and the 'rebuild' ... not just cuz it was complete garbage and cuz I am in NJ (Sandy), but if death / destruction were so good for econ, they'd arrange them more often ... so friggin stoopid

If summer was boosted by concert and movies (ING), I guess it could be the same for thanksgiving/christmas :)

sorta why it bothers me when they talk 'bout hurricanes and the 'rebuild' ... not just cuz it was complete garbage and cuz I am in NJ (Sandy), but if death / destruction were so good for econ, they'd arrange them more often ... so friggin stoopid