Good morning … shorter than short note as I’m just back in seat and going thru inbox.

Jumping right in … here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries have been led modestly higher by intermediates to start the new week with bank earnings and ratings actions appearing to be top-of-mind alongside debt-ceiling X-date handicapping (see Wrightson's latest update in text below). DXY is lower (-0.17%) while front WTI futures are little changed (-0.2%). Asian stocks were mixed (Chinese and China-linked exhanges lower), EU and UK share markets are little changed while ES futures are showing -0.22% here at 6:40am. Our overnight US rates flows saw yet another sideways session during Asian hours with some buying in intermediates seen at the start of the week amid very weak overall volumes. It was a similar story in London's AM hours with Treasuries in a 2bp range. Banks were a light buyer, on balance, with real$ continuing to pick away at the shortest maturity Bills, avoiding the X-date window maturities. Overnight Treasury volume was ~60% of average overall.

Treasury 10yr yields, daily: About all one can say right now is that sellers emerge near 3.33% and buyers emerge around 3.60%, as drawn in. Momentum studies are generally signal-less except in long-term momentum which still shades bullishly.

TLT's (20+-year Treasury ETF), daily: Had to add this one because the channel that TLT's have trafficked in since late last year is so well-defined. TLT's look like they're tring to re-fill the opening gap higher from March 10's employment report.

… and for some MORE of the news you can use » IGMs Press Picks for today (24 APR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

KEY MESSAGES -Although we remain structural USD bears, our quantitative indicators point toward increased risk of a squeeze. -To protect the portfolio, we like owning FX and equities vol at these levels. -The main data catalyst of the week is Q1 ECI on Friday; we expect it to show sturdier wage growth than implied by AHE.

As we await ECI and then we all know to be mindful of SLOOS, Goldilocks on

… We have estimated the impact of tighter credit on growth using four approaches centered on the effects of reduced lending volumes, tighter lending standards, a decline in bank capital, and a higher deposit beta. Projections by regional banks are consistent with our assumption that deposit betas will rise more than usual, reducing bank profits and lending. Our central estimate is that tighter credit will reduce 2023 GDP growth by 0.4pp, leaving demand growth closer to the desired below-potential pace than it appeared to be in the first months of the year.

Broadening one’s scope to a more WORDLY view … well, one doesn’t have to because Seth Carpenter of MS has his you can share …

The EM versus DM theme we have been highlighting has become even more compelling. Asia is expected to outperform, while the China reopening story remains solid. Meanwhile, the US economy is slowing, and we believe risks are to the downside.

And from a WORLD view to one of the FOMC — without, dare I say, any Fedspeak ahead … whatever are we to do? Enter Wells Fargo,

We expect the FOMC to raise the target range for the fed funds rate by 25 bps on May 3, bringing it up to 5.00%-5.25% from 0.00%-0.25% only 14 months ago. We also anticipate that the Committee will continue quantitative tightening (QT) at its current pace.

Stress in the financial system related to the failure of two regional banks in early March has eased over the inter-meeting period, alleviating concerns over a rapid tightening in credit conditions. The jobs market is cooling only gradually, and the unemployment rate is still near historic lows. The trend in inflation remains uncomfortably high, as evidenced by core CPI advancing at a 5.1% clip over the past three months.

However, we believe the statement and press conference likely will signal that May's hike may very well be the last of this tightening cycle. In March, the so-called "dot plot" showed that 11 of the Committee's 18 participants viewed a fed funds rate of 5.00%-5.25% or lower at year-end 2023 as the most likely outcome, a view that has not seemed to have been swayed by the latest data.

If most officials see the May meeting as likely to be the final hike this cycle, then we would expect the statement to no longer include the phrase that "some additional policy firming may be appropriate."

That said, we do not think the statement will fully close the door on further rate hikes, given that inflation remains well above target. Rather, the statement likely will include an acknowledgement that further adjustments in rates are possible. The outlook will be based on the Committee's assessment of cumulative tightening of monetary policy, the lags of policy on economic activity and inflation, and economic and financial developments.

If, as we expect, the statement signals that additional increases are less likely, but not fully off the table, then dissents among voting participants are likely to be avoided.

We do not think a technical tweak to the Fed's overnight repurchase agreement (RRP) facility is forthcoming, and in the final section of this report, we dive deeper into this tool in the central bank's toolkit.

…Markets have noticeably calmed down this month relative to the frantic ups and downs of the first quarter of 2023. That’s at least partly due to a much clearer picture of what central banks are going to do, at least when it comes to interest rates. Sure, the Federal Reserve is among those now expected to deliver at least one rate hike, maybe even two, but the era of steep increases in borrowing costs has come and gone and investors are confident that a pause is very close, and that a pivot to lower rates may also come by year’s end.

There’s another side to central bank policy that now looms as a potentially bigger threat, though — liquidity. Stocks and bonds plunged in 2022 when rates rose and balance sheets shrank rapidly from record highs in the trillions of dollars. And assets turned around before the hikes stopped, but after those balance sheets stabilized. As Matt King, Citigroup’s global markets strategist, pointed out recently, we are likely to face fresh reductions in liquidity provisions now the banking crisis is waning. And that stands as a threat for investors across assets.

AND for something else worth your while, John Auther’s latest on

… Fiona Cincotta, senior financial markets analyst at City Index, describes the ceiling as a “dance which happens and then it all gets sorted out anyway,” and admits she struggles to view it as a factor that should have an impact on the market. She agrees, however, that if this were the time when the debt ceiling didn’t rise, the negative implications would be profound. Put slightly differently, the debt ceiling offers a classic example of a “black swan” event — extreme but very low-probability. Markets are notoriously bad at pricing them, and for most of this year the attitude seems to have been that it’s not worth the effort of even trying.

That changed last week. The clearest tell came in the Treasury-bill market, for bonds with less than a year to go before they mature. These are the safest, and therefore among the least interesting, investments that exist. But the spread of the yield on three-month bills compared to one-month notes has suddenly shot up:

This only makes sense if investors are worried that something bad might happen to Uncle Sam’s ability to pay up at some point between one and three months from now. That’s when the debt ceiling situation is likely to come to a head…

Finally, a couple of more EQUITY related notes for our inner stock jockeys. First from a rather large British operation,

With 1Q earnings set to address many unanswered questions over the next couple of weeks, we revisit some of the themes, sector and style/factor views that we have featured in this series over the last several months, checking in on what has played out in equity markets as of late and where we are likely to go from here.

And finally, few words to help get week in equities kickstarted,

Weekly Warm-up: Will the Fed Continue to Tighten into a Growth Slowdown?

So far this earnings season, stocks have traded more in line with fundamentals. This is different than the past few quarters and the beginning of what we think is a reset on expectations for a 2H EPS recovery. The Fed seems determined to fight inflation even if a more significant slowdown arrives.

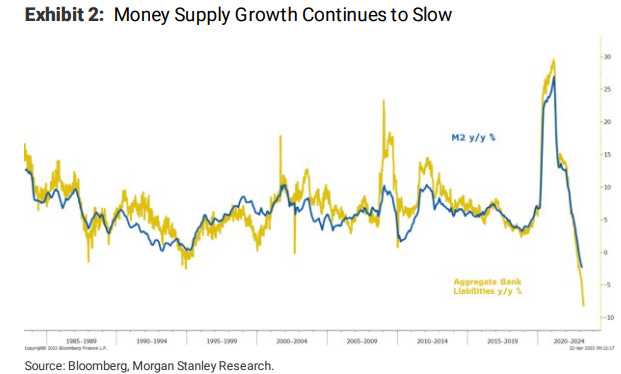

… In short, the irony of the bank stress experienced in early March is that ithas kept asset prices higher than they would have been otherwise (via this perception is reality liquidity dynamic)even though, in our view, there will be a negative impact on growth as capital availability is ultimately constrained (Exhibit 2).

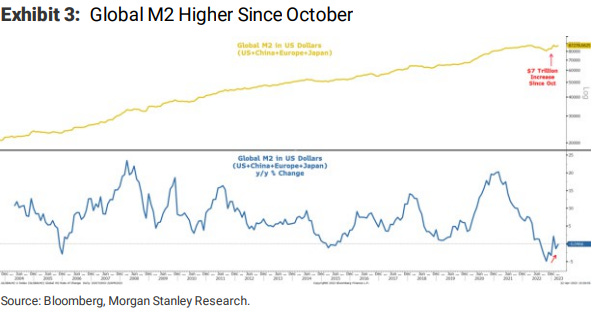

The other positive driver of asset prices has been the global liquidity offset to the squeeze we had seen in the US to start the year. We like to look at global M2in USD as a proxy for global liquidity and on that score, we've seen a major improvement since last October when stocks bottomed globally (Exhibit 3). Most of this improvementhas come from China and Japan adding more liquidity. The other big factor has been the much weaker dollar (Exhibit 4).

Still sifting through my inbox… THAT is all for now. Off to the day job…