Good mornin’ … a couple things overnight worth mentioning before jumping in…

Bloomberg- Fed’s Kashkari Says Too Soon to Declare Victory on Inflation (VOTER)

Minneapolis chief says more data needed to assess economy

Kashkari says three months of good inflation data isn’t enough

… “Before we declare that ‘we’re absolutely done, we’ve solved the problem,’ let’s get more data and see how the economy evolves,” Kashkari said Monday in an interview on Fox News…

RBA raised interest rates 25bp to 4.35%, Michelle Bullock said“Inflation in Australia has passed its peak but is still too high and is proving more persistent than expected a few months ago”.

Bloomberg- WeWork Goes Bankrupt, Signs Pact With Creditors to Cut Debt (thinking a direct hit TO CRE and of importance next SLOOS reported…but hopefully by then we’ll have … forgotten?)

… WeWork’s collapse into bankruptcy is the culmination of a years-long saga for the company, which was once the biggest office tenant in Manhattan. Its sudden rise and precipitous fall have captivated Wall Street and Silicon Valley alike.

The firm’s undoing arguably started in 2019. In a matter of months, the company went from planning an IPO to laying off thousands and procuring a multi-billion-dollar bailout….

… Couple observations where FIRST it would appear 4.75% (March relevance) level appears to REMAIN relevant and in as far as momentum (nearer overSOLD) would suggest shorter-term (ie DAILY) caution warranted … rate cuts maybe but NOT today. Lets get concession (up nearer / ABOVE 4.75%) and go forward into 10s and 30s tomorrow and Thursday …

AND here is a snapshot OF USTs as of 703a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher after a 'dovish hike' by the RBA and weak Chinese export and German industrial output readings. DXY is higher (+0.43%) while front WTI futures are lower (-1.6%, see attachments). Asian stocks were mostly lower, EU and UK share markets are modestly lower while ES futures are showing -0.4% here at 6:45am. Our overnight US rates flows saw muted activity during Asian hours with real$ selling in 10's and fast$ interest in steepeners being a feature there. Overnight Treasury volume was quite solid at ~145% of average ahead of today's start of the refunding process.

… and for some MORE of the news you can use » The Morning Hark - 7 Nov 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

Apollo - Retailers Expect a Weaker Holiday Season (ruh roh, RelRoy)

Hiring for the holiday season is generally done in October, and adding up new jobs created in the BLS-defined holiday season retail sectors in the latest employment report shows that retailers expect a weaker holiday season, see chart below. This soft outlook is consistent with growing inventories at many retailers. The BLS defines holiday sectors as furniture, electronics, personal care, clothing, sporting goods, general merchandise stores, miscellaneous store retailers (e.g., florists, office supply stores, gift shops, and pet shops), and non-store retailers (e.g., online shopping and mail-order houses, vending machine operators, and direct store establishments).

Argus- Daily Spotlight (yest … an old shop around since 1934 and so lots of eyeballs on Global Wall Street reading … speaks TO those in recession or slower growth camp moreso than it does TO rate CUTS, at least in my view…)

GDP Growth to Slow in 4Q Our analysis of data that has been reported in recent weeks leads us to conclude that key parts of U.S. GDP are still expanding, despite the impact of inflation, high interest rates, and geopolitical developments. That said, growth is not consistent across all segments of the economy, and, in some cases, growth rates are slowing. While the Fed is on track to engineer a soft landing for the economy, recession in 2023-2034 remains a possibility, though we think that the odds are diminishing. After reviewing the latest economic data points, metrics, and trends, our forecast for GDP growth in 4Q23 is now 2.0%, a pronounced decline from the 3Q level. Our estimate for the full year 2023 is now 2.8%, up from our prior forecast of 2.3% due to the blowout 3Q report. Our preliminary forecast for GDP growth in 2024 is 1.8%, as the Federal Reserve, with its tool chest again full after hiking rates during 1H23, can contemplate lowering interest rates to recharge economic growth. Our estimates generally are in the range with other forecasters, though perhaps a bit higher than the consensus. The Wall Street Journal Economic Survey calls for GDP growth of 2.2% in 2023 and 1.0% in 2024. The Federal Reserve is now anticipating GDP growth of 2.1% for 2023 and 1.5% in 2024. The Philadelphia Federal Reserve's Survey of Professional Forecasters is calling for growth of 2.1% in 2023 and 1.3% in 2024. A recent GDPNow forecast from the Federal Reserve Bank of Atlanta was 2.3% for 4Q23.

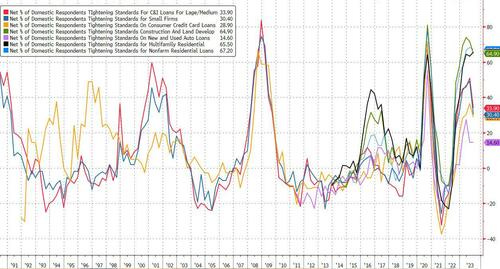

Barclays - October SLOOS: Lending conditions tighten again, but with less intensity (the good news IS the bad news is somewhat less bad in severity)

The October Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) showed a continued tightening in lending standards but with less intensity than in previous quarters, while the demand for loans remains weak.

The October Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) showed further tightening in lending standards for both businesses and households in the third quarter. However, the proportion of banks tightening lending standards declined.

At the same time, banks reported weaker demand for most types of loans.

While the reduction in C&I loan demand from large and mid-sized firms appears to be moderating, the decline in loan demand by small firms and households was somewhat more pronounced than in July.

China's exports remained stuck in contraction, missing marked expectation by a wide margin. We think slumping FDI, slowing global growth and contracting new export orders suggest any quick turnaround in exports is unlikely. Imports, on the other hand, beat expectations, thanks to strong rebound in cooper and chip imports.

October: -6.4% y/y for exports, and 3% y/y for imports (both in USD terms)

Bloomberg consensus (Barclays): -3.5% y/y (-5.5%) for exports, and -5% y/y (-5.5%) for imports

September: -6.2% y/y for exports, and -6.3% y/y for imports (both in USD terms)

Bloomberg BNP - US Q3 SLOOS: Banks continue to tighten loan standards

KEY MESSAGES

The Fed’s latest Senior Loan Officer Opinion Survey (SLOOS) supports the notion that past policy tightening is still filtering through the US economy, leaving intact our view that additional policy rate increases will not be needed.

The Q3 SLOOS indicated that banks continued to tighten lending standards (albeit at a slightly lower intensity) across loan categories. The data is consistent with the Fed acknowledging “tighter financial and credit conditions” as factors likely to weigh on activity and inflation ahead in its latest policy statement.

Consumer lending saw the most noticeable tightening in standards across categories, with demand for both residential mortgage and credit card loans deteriorating compared with Q2. Such worsening in consumer lending supply and demand will likely amplify ongoing deceleration in wage growth and rising interest expenses with respect to the impact on consumer spending, corroborating our projection for a sharp slowdown in Q4 GDP.

BNP- US equities: Fading the rally (rates mattering TO stock jockeys matters)

Rate-driven move? The regime of bad macro news being good news for risk assets was in full force for equities last week. Weaker ISM and payrolls prints and a benign FOMC meeting were the ‘positive’ catalysts. The macro newsflow resulted in US 10y yields falling 30bp last week. The SPX rally from 4150 to 4350 on 2024 EPS of 242.3 also implied a ~30bp increase in the earnings yield. We could attribute all of last week’s SPX performance to the rate move. However, this probably oversimplifies the case. The spread between equity earnings yield and US bond yields has not been stable but rather has been trending lower through the year (Figure 1).

Unwind of an oversold market: Away from the move in rates, an alternative explanation for the magnitude of last week’s rally might lie in a simple reversal of an oversold condition and short-covering. We flagged the risk of a rally last week (see US equities: Correction but not capitulation, dated 30 October). We also suggested a modest rally would be a move we would look to fade. Fundamentally, we see the trend into year-end for US equites as likely to be weaker. There is little in the recent macro data or Q3 earnings releases to support the 2024 earnings reacceleration implied by the consensus (SPX 2024 12.2% EPS). Post Q3, we have seen earnings downgrades, notably much more acute further down the market cap spectrum (SPX 2024 EPS -53bp, SPW -248bp). We expect to see forecast downgrades continue into year-end. In our view, this could trigger a retest of YTD lows. Our 2023 year-end target remains 4150, and we would consider fading rallies above this level.

… How monetary policy is passing through to the real economy is key to understanding this economic cycle. We have been arguing that one of the most important reasons behind the remarkable US growth out-performance this year is the exceedingly slow pass-through of Fed tightening. Transmission has been so slow that US companies have in fact seen interest expense decline by benefitting from higher returns on their cash holdings but fixed long-term liabilities thanks to a decade of zero rates (chart 1). QE effectively created an anti-bubble…

… Just when you thought it was safe to go back into the water and hoover up every bond in sight, yesterday saw yields do yet another 180 degree turn, something we've been used to seeing in recent weeks, even if last three days of last week was one way traffic. 2yr US yields led the way (+9.6bps). The S&P 500 managed to eke out a narrow gain (+0.18%) but US small caps (Russell 2000 -1.29%) suffered again with higher rates.

Diving in, the bond selloff perhaps came as investors began to wonder if last week’s narrative about rate cuts was overdone. For instance, market pricing for the Fed now implies a 16% chance of another rate hike, up from 11% on Friday. Moreover, the rate priced in by the December 2024 meeting was up +12.4bps to 4.47%. So there was a clear, albeit partial unwinding of last week’s moves. After the market close, we heard from Minneapolis Fed Kashkari, one of the more hawkish FOMC voices, who said that “we need to let the data keep coming to us to see if we really have got the inflation genie back in the bottle”. So some pushback against declaring victory over inflation.

For markets, this is hardly the first time we’ve seen expectations of a dovish pivot, and Henry pointed out yesterday (link here) that this is at least the 7th time this cycle where markets have reacted notably in response to dovish speculation. Clearly rates aren’t going to keep going up forever, but on the previous 6 occasions we saw hopes for near-term rate cuts dashed every time. Note that we’ve still got above-target inflation in every G7 country. With that in mind, next week’s US CPI release will be an important factor on that front, and our US economists expect core CPI to remain at +0.3% for a third consecutive month.

Two weeks ago, the yield on the 10-year Treasury Note was hovering around 5%, and the S&P 500 was in contraction territory, down over 10%. But last week, the 10-year yield dipped to 4.6%, while the S&P 500 saw a 6% gain. This market volatility is attributed to changing sentiments: 1) There was a belief that the Federal Reserve had lost control, but now, 2) it seems the Fed has achieved a "soft landing," bringing a semblance of stability.

While this may hold some truth, we remain cautious. If we step back and look at the US economy from a distance, things don’t really look so great. Our worries have roots all the way back in 2008, when the Fed altered its approach to monetary policy. The Fed shifted from a "scarce reserve" model to an "abundant reserve" model when it initiated Quantitative Easing, fundamentally changing how interest rates are determined…

… Today, US commercial banks carry an estimated $650 billion loss in their “held to maturity” assets…but they don’t have to mark them to market. Just imagine if this was 2008 and Treasury Secretary Hank Paulson, Fed Chair Ben Bernanke and FDIC Chair Sheila Bair were in charge. They would have insisted on mark-to-market and we would need TARP 2.0 to bail out the banking system.

What the Fed will do is pay these private banks and other institutions roughly $300 billion this year just to hold reserves. Without this payment from the Fed to the banks, profits would be much lower and the losses on their books would be more painful…

Goldilocks - Fewer Senior Loan Officers Report Tightening Credit Standards; Loan Demand Weakens Further (hey, thats great and / or terrible …)

BOTTOM LINE: The Federal Reserve’s October 2023 Senior Loan Officer Opinion Survey—conducted for bank lending activity over the third quarter of this year—reported that standards tightened at a slower pace versus the prior quarter. Demand weakened for both commercial and industrial loans for firms of all sizes and for commercial real estate loans. On the household side, banks reported tighter standards for all categories of residential real estate loans and for all consumer loan categories. They also reported weaker demand for all residential real estate categories and weaker demand for credit card, auto, and other consumer loans on net. Despite a major net share of banks reporting a worsening economic outlook as a reason for tightening lending standards, among banks that reported easing lending standards over third quarter, a more favorable economic outlook was one of the most frequently cited reasons.

ING - Bank caution to tighten the squeeze on the US economy

The Federal Reserve's Senior Loan Officer Opinion Survey shows banks have tightened lending standards further while households and businesses remain wary of taking on additional borrowing. Given how important credit flow is to the US economy it makes it all the more likely that the economy will continue to slow, helping to bring inflation back to target

Banks tightening lending standards points to outstanding commercial bank lending turning negative

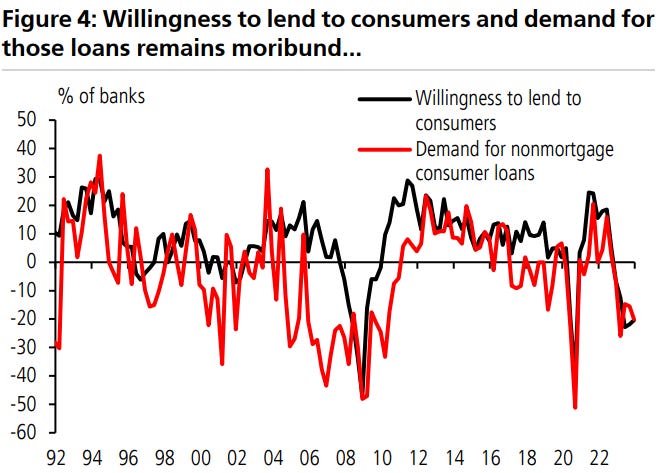

SLOOS indicates lending standards historically associated with recessions The Federal Reserve's Senior Loan Officer Opinion Survey continued to report widespread tightness in lending standards today. The net willingness to lend to consumers (make consumer installment loans) printed at -20.4 percent balance, little changed from the -21.8 reported in July and -22.8 in April. This net breadth has generally been associated with US economic contractions. Banks on net continued to report widespread further tightening of lending standards for C&I loans. The net share of banks tightening commercial real estate lending (summing together construction and land development, non-farm non-residential, and multifamily residential) eased a touch but remained high, reading in at 65.9 percent balance versus July's 67.8. Standards for consumer credit cards also loosened slightly but remained tight. Demand from households for credit card and auto loans was down relative to July and weak for an economic expansion. This report was consistent with our expectations last week: tightness in lending of a similar caliber to that seen in Q2 and Q3.

… In short, I am bullish on equities going into the end of the year and for 2024. Productivity growth is alive and well. This was one of the disappointing features of Powell’s press conference when people noted the surprising GDP growth in the third quarter—he did not attribute it to the surging productivity. Outside of the pandemic, this latest quarter’s productivity rate was among highest in the last two decades. This is partly a rebound after a very disappointing productivity fall in 2022 and I think more of this rebound can still occur.

Workers might be working harder so they cannot be laid off; the era of “do nothing, the boss can’t fire me" is over. I think a continued growth of productivity, that also comes from recent artificial intelligence applications, can offset the softening of demand and help us avoid a recession and support the profit outlook.

Last week was big for the markets. If the interest rate environment remains as supportive as I see it, we will see a continued bright outlook for equities.

Yardeni- SLOOS Shows Looser Credit Conditions (looser good or bad?

… Inflation seems to be to be mostly a transitory problem, after all, caused by the pandemic. Maybe labor shortages are stimulating a productivity growth boom. And, maybe retiring Baby Boomers are saving less and spending more. Perhaps, the Fed's Phillips Curve model is flawed. Solid economic growth is disinflationary rather than inflationary if it is productivity-based.

Even the credit markets aren't following the Fed's game plan. Today's Senior Loan Officer Survey (SLOOS) showed that credit conditions actually eased a bit in October's quarterly survey (chart). Last week's plunge in bond yields also eased credit conditions raising some concerns that the Fed may have to raise the federal funds rate if the Bond Vigilantes stop doing their heavy lifting in the bond market.

We are expecting that the FOMC will remain on pause and that the committee may conclude that growth isn't inflationary after all, but rather disinflationary because productivity is making a comeback. That's our story, and we are sticking to it.

… And from Global Wall Street inbox TO the WWW,

Barrons- Warren Buffett Isn’t Buying Bonds Even as Rates Surge

Berkshire Hathaway (ticker: BRK.A, BKR.B) CEO Warren Buffett, 93 years old, has long favored stocks over bonds. That is a smart view given the historical outperformance of stocks, and the surge in rates since March 2022hasn’t changed his view.

Just take a look at the enormous Berkshire investment portfolio that Buffett oversees.

At the end of September, Berkshire held about $340 billion of stocks; $157 billion of cash, mostly in U.S. Treasury bills maturing in less than a year; and just $22 billion of bonds. That is according to Berkshire’s quarterly 10-Q filing with the Securities and Exchange Commission, released on Saturday in conjunction with its third-quarter earnings.

And that bond portfolio is largely cash-like. About 75%, or $17 billion, matures in the next 12 months. Just 1% of the entire Berkshire portfolio is invested in bonds with a maturity of longer than one year. Berkshire’s bond portfolio is down about $3 billion since the start of 2023.

Berkshire’s investment portfolio has gotten even more equity-heavy with time. When 10-year Treasury debt yielded less than 1% in 2020, Buffett marveled at the willingness of bond investors to accept that paltry rate. Ten-year Treasury debt now yields about 4.6%, but Buffett is still holding back…

… Asked at the meeting about an insurance contract with American International Group (AIG) in which Berkshire took a $10 billion premium for insuring against $20 billion of long-term liabilities, Buffett said: “And when we take that $10 billion, we don’t agree to put it in 5-year bonds and 10-year bonds. We don’t even think that way.”

Buffett held a lot of cash when short rates were at zero in 2020 and 2021, taking that financial pain because he felt bond yields were terrible. He wouldn’t follow the example of banks like…

… Bank of America and some other banks now have huge paper losses because bond prices fall as yields rise. And Buffett is being vindicated as short rates have surged to over 5%, giving Berkshire ample returns on its cash.

The big news will come if Buffett ever decides to redeploy a chunk of the cash into bonds. Wall Street is still waiting for that, but it might take appreciably higher yields to entice Buffett.

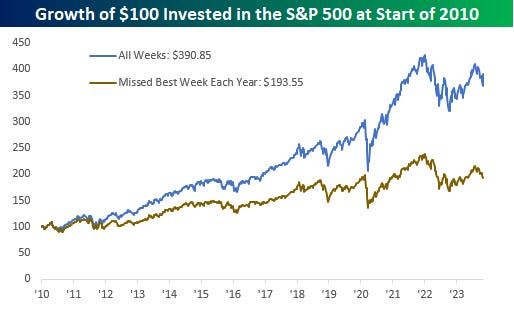

Bespoke- What if you miss out on the best week each year?

… The chart below shows the growth of $100 invested in the S&P 500 at the start of 2010 (dividends not included) on both a buy-and-hold strategy as well as if an investor missed out on the best week of each calendar year. The gap is enormous. While the original $100 is now worth $390.85 with buy-and-hold, had you missed out on the best week of each year, you would have less than half of that amount at $193.55. In other words, well over half of the gains since 2010 can be attributed to those 14 weeks. Admittedly, you could make the counterargument that most of the losses during this period have also occurred in a small number of weeks, but trying to successfully anticipate when these good weeks or bad weeks will occur is IMPOSSIBLE. As “KC and the Sunshine Band” advised in 1979, “Please Don’t Go”.

Bloomberg- Bombshells Are Already Landing in Election-Year Markets (Authers’ OpED)

… As for fiscal policy, the room for the Biden administration to do anything that would have a significant impact before the election is minimal. However, 2024 could provide an interesting taste of a new political reality in which both parties grasp that they can’t let the deficit remain unchecked. Jeannette Lowe of Strategas Research Partners predicts “more focus on offsets for new spending bills” (along the lines of Speaker Mike Johnson’s already much-ridiculed proposal to balance extra spending on aid for Israel with a cut in the enforcement budget of the Internal Revenue Service), especially as net interest costs on the national debt ramp up. She also pointed out that the total weight of the cost of servicing Uncle Sam’s debt was now almost back to its level from 1992, which led to the concerted action to reduce the deficit under President Bill Clinton:

These costs have surpassed 14% of tax revenues, historically the inflection point for a shift from fiscal accommodation to fiscal austerity. Essentially, tension is building up over how the federal government will pay for all the things that it's doing, especially if we're looking at even more spending for national security.

This chart illustrates the issue:

The big difference with the Clinton era, when deficit was turned into surplus and interest costs were halved, is that back then the Cold War had just ended and the peace dividend made it much easier to rein in the budget. That’s not the case now. On which subject…

Bloomberg- US Debt Interest Bill Rockets Past a Cool $1 Trillion a Year (it is election day … get out and vote … early and often…?)

Amount of annual interest payments has doubled in 19 months

Rise in issuance from 2020 will also need to be refinanced: BI

US Treasuries are set to face renewed selling pressure into the new year if the nation’s swelling debt repayment bill is any guide.

Estimated annualized interest payments on the US government debt pile climbed past $1 trillion at the end of last month, Bloomberg analysis shows. That amount has doubled in the past 19 months, and is equivalent to 15.9% of the entire Federal budget for fiscal year 2022.

The figures are calculated using US Treasury data which state the government’s monthly outstanding debt balances and the average interest it pays.

The worsening metrics may reignite debate about the US fiscal path amid heavy borrowing from Washington. That dynamic has already helped drive up bond yields, threaten the return of the so-called bond vigilantes and led Fitch Ratings to downgrade US government debt in August.

“There will be further increases to Treasury coupon auctions and T-bills outstanding going forward,” Bloomberg Intelligence strategists Ira Jersey and Will Hoffman wrote in a research note. “Besides deficits of over $2 trillion in the foreseeable future, climbing maturities following the increase of issuance from March 2020 will also need to be refinanced.”

Bloomberg- More Laid-Off Workers Got Severance During the Pandemic, But That’s Over Now

… Just 42% of global employers offered severance to all laid-off employees this year, a survey from Dutch recruitment firm Randstad NV found, down from 64% that did so in 2021. The current figure is also below the 44% of firms that extended severance back in 2019. US employers were the least likely to offer severance for all employees, with just one in four doing so. In the UK and Germany, about half of firms did so. It’s not a trivial matter, as more than 90% of the 430 firms surveyed said they plan some sort of workforce reduction in the next 12 months…

… More than half of companies surveyed said they’ve made changes to their severance packages in the past three years, and a third of those that hadn’t made changes said they’re currently tinkering with their plans. The most common tweak is offering so-called redeployment programs, where employees whose role is at risk of elimination have the opportunity to find an alternate position inside the organization. Four in ten respondents said they anticipate offering redeployment options over the next year.

That won’t help those who get laid off and aren’t eligible for severance. The most cited cause for layoffs, Randstad RiseSmart found, was companies over-hiring when times were flush. And that might happen again, as “many companies lack the learning curve to avoid this cycle in the future,” according to the survey.

CalculatedRisk: Fed SLOOS Survey: Banks reported Tighter Standards, Weaker Demand for All Loan Types

…The Strategy MBS are a particularly popular investment for Pension and Insurance (professional) portfolio managers because they offer a nice yield spread over USTs without the credit risk associated with corporate bonds. Unfortunately, except for large mutual funds or Index ETFs, it is challenging for civilians to gain access to MBS.

I often offer the -rosa line- spread of MBS to the 10yr rate as a measure of value. Presently, this spread, at nearly 175bps, is close to its all-time wide, and almost 100bps more than its long-term average of about 75bps.

However, this spread is a function of the 10yr rate versus the near-Par (100) priced MBS, not the spread to the MBS Index, which would be much tighter.

This Strategy offers civilians access to these higher-yielding MBS bonds in a liquid and transparent NYSE listed vehicle without the baggage of MBS Index-linked lower coupon MBS bonds…

WolfST- Highest-Ever Treasury Short Positioning by Hedge Funds into Last Week Was “Accident Waiting to Happen,” Massive Short-Covering Ensued, Pushed Down Yields. “Basis Trade” at it Again (highest ever ANYTHING warrants a bit more recon …)

The fireworks over the past few weeks in the US Treasury market involved, as you’d expect, highly leveraged hedge funds covering their massive short positions.

According to an aggregate of Commodity Futures Trading Commission figures going back to 2006, cited by Bloomberg this morning, hedge funds had taken on the most ever leveraged net short positions in Treasury futures trades by October 31.

Amid these short positions, the 10-year Treasury yield rose to 5% by October 23, and the rising yields mean falling prices in the cash Treasury market, and the Treasury-short bets were working, but that moment of 5% glory was followed by the insta-plunge in yields the same day, followed by further drops in yields. Dropping yields means prices rallied. And yet during that week, hedge funds continued to pile into this leveraged short trade until October 31.

And by October 31, the net short-positions in Treasury futures had reached the highest level ever, and this extreme positioning “was an accident waiting to happen,” Gareth Berry, strategist at Macquarie Group, told Bloomberg…

… Ken Griffin, CEO of the hedge fund Citadel which is up to its ears in the basis trade, pushed back against SEC scrutiny, and said that regulators should focus on banks and their lending to hedge funds, in order to reduce the risks to the financial system, he told the FT yesterday.

“If regulators are really worried about the size of the basis trade, they can ask banks to conduct stress tests to see if they have enough collateral from their counterparties,” he told the FT.

Meanwhile, back in the Treasury market, the massive short-covering that helped push down the 10-year yield last week seems to have run its course, and today the 10-year yield already jumped by 15 basis points from the low on Friday to 4.65% at the moment.

ZH: Senior Loan Officer Survery Shows Modest Improvement Even As Credit Remains Tight, Demand Weak

… Sure enough, moments ago the Fed reported that - as expected - in Q3 the SLOOS respondents "on balance, reported tighter standards and weaker demand for commercial and industrial (C&I) loans to firms of all sizes over the third quarter. Furthermore, banks reported tighter standards and weaker demand for all commercial real estate (CRE) loan categories."

… But while the big picture remains downbeat, with both supply and demand in tight/contracting territory, the silver lining is that the underlying measures improved somewhat compared with the second quarter, which is bizarre since rates are far higher now than they were in Q2.

Specifically, the proportion of US banks tightening standards for the all important commercial and industrial (C&I) loans for medium and large businesses fell to 33.9%, from 50.8% in the second quarter even as some 62.7% of banks are keeping lending conditions basically unchanged. Other notable categories also posted improvements:

The proportion of banks reporting tightening standards for small firms fell from 49.2 to 30.4

The proportion of banks reporting tightening standards for consumer credit card loans fell from 36.4 to 28.9

The proportion of banks reporting tightening standards for construction and lend development loans rose from 63.3 to 64.9

The proportion of banks reporting tightening standards for new auto loans was unchanged at 14.6

The proportion of banks reporting tightening standards for nonfarm residential loans fell from 68.3 to 67.2

Among the banks that reported easing lending standards, the most frequently cited reasons were an improvement in the credit quality of loans and a more favorable or less uncertain economic outlook.

In comparison to large banks, other banks more frequently cited concerns about deposit outflows, funding costs, deterioration in or desire to improve their liquidity positions, and concerns about declines in the market value of fixed-income assets as reasons for tightening lending standards.

For foreign banks, major shares reported that a less favorable or more uncertain economic outlook; a deterioration in customers’ collateral values; a reduced tolerance for risk; a deterioration in the credit quality of loans; and a reduction in the ease of selling loans in the secondary market were important reasons for tightening lending standards over the third quarter.

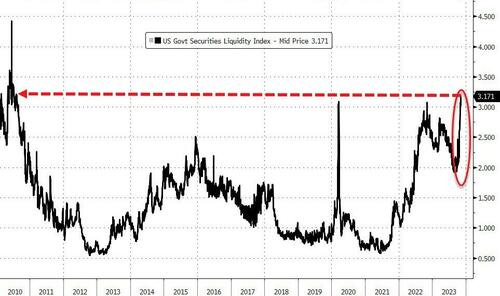

ZH: As Treasury Liquidity Evaporates, Last Week's Massive Bond Rally "Was An Accident Waiting To Happen" (specifically noting for these last couple visuals — really the very last one near and dear now that I cannot confirm or deny whatever conditions truly exist IN the marketplace but now, only as spectator well AFTER the fact …)

… One more thing of critical importance, after The Fed specifically highlighted the market's "tightening financial conditions" - doing it's job for it - last week saw almost one third of the tightening of the last three months removed as conditions eased...

Source: Bloomberg

This reflexive move - after Powell's comments - leads to the need for a more hawkish Fed to stabilize that over-easing of financial conditions which threatens to reignite asset inflation... and around we go.

And finally, this is a major problem - and maybe the canary in the coalmine of problems with the highly-levered basis-trade discussed above.

US Treasury Liquidity is at its worst since 2010 (worse than at the peak of 2020's yield collapse when The Fed stepped in specifically to ensure liquidity)...

I had NO idea Investing.com does multiple comics wkly. There's some REALLY good one's thanks!