(USTs MIXED on strong volumes)while WE slept; MATH: Bill + Bill = Bond BID? ; What FedFunds AREN'T tellin' us (Dudley); "Bill and Bill's Big Adventure in Treasuries Land"

Good morning … 10s have a peak peek over 5% and took a step back from the ‘edge of the abyss’,

Note the turn then cross of stochastics (bottom panel) which is something you’ll find I lean on quite a bit as I have learned ‘math’ from some of the best in the biz. Leading or lagging indicator — you can decide — it coincides with most recent attempt at / ABOVE 5% and combination of the math of the moment as well as psychologically important level obtained, well, someone(s) threw the ‘challenge flag’ and we pause …

MATH.

Bill Gross + Bill Ackman = BOND BID

Bloomberg- Bill Gross Sees a Recession By Year End

Bill Gross says he’s buying futures tied to the Secured Overnight Financing Rate and sees a recession in the fourth quarter…

Bloomberg- Bill Ackman Says He Covered His Short Bet on US Treasuries

Ackman disclosed bet against 30-year Treasuries in August

Long-term yields decline after earlier hitting 2007 high

… “The economy is slowing faster than recent data suggests,” the Pershing Square Capital Management founder wrote in a post on X, the platform formerly known as Twitter.

Ackman disclosed in early August that he was bearish 30-year Treasuries via options both as a hedge for his equity investments and as a stand alone wager. He said at the time that structural changes, such as deglobalization and the energy transition would fuel persistent inflation pressures. He added that a flood of bond supply to fund swelling US budget deficits could also push yields higher…

Add ‘em up and you get

Bloomberg- Ackman, Gross Abandon Bearish Bond View With Yields Bouncing Off 5%

Ackman covers Treasuries short, cites signs of slowing economy

Bill Gross buys short-term rates futures, predicts recession

NOW we’re coming up with BILL math as to WHY we traded LOWER? Thanks for that.

Now, am I going to sit here and hit SEND with a straight face and say that I wholeheartedly believe Bill and Bill equals BID?

No, not really BUT a few hours after we peek above 5% 10s , and the timing is, shall we say, suspect?

AND these two BILLS giving the world something to write and talk about so we’ve all got THAT going for us…

Someone out there buying and maybe it is, at days end, just a couple guys named Bill … perhaps it’s not even these two clowns but some others … Perhaps it’s someone(s) out there paying attention TO the technicals (stochastics) of the moment?

Whatever the case may / may NOT be, we’re still on verge of witnessing a ground incursion in Gaza that may once again invoke F2Q bid for bonds.

Until … it does not.

But it might … what I can say with somewhat more confidence is that despite or because of the ‘math’, bond yields dropped and stocks popped (until they once again DROPPED) and so

ZH: Stocks Soar, Yields Tumble After Ackman Says He Closed His Bond Short

AND then by days end,

ZH: Bitcoin & Bonds Bid After 'Bearish-Bill' Bails; Black Gold & The Buck Breakdown

… Equity markets soared as yields plunged, and we reminder readers that today marks the first day of the estimated open Buyback window period (which may have helped accelerate the exuberant BTFD move). Late day headlines on NVDA sparked selling in INTC and sent the majors lower with Small Cap and The Dow the biggest losers with the S&P swinging notably red (as we not.

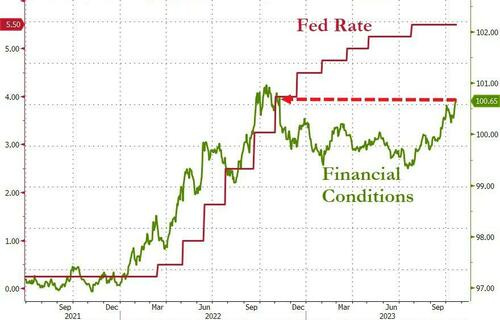

… Meanwhile, financial conditions continue to tighten...

...now near their tightest since The Fed began this inflation-fighting cycle. “Given that the impact from a tightening in financial conditions on GDP typically takes 1-2 years, the full effect of the severe tightening that took place last year has yet to be felt,” wrote JPM's Marko Kolanovic.

Meanwhile over in Japan,

Bloomberg - BOJ Wades Back Into Bond Market to Curb Rising Japan Yields

BOJ’s tolerance for higher yields challenged before meeting

Speculation of BOJ policy tweak continues to weigh bonds

The Bank of Japan announced yet another unscheduled bond-purchase operation to curb rising sovereign yields as traders challenge its resolve ahead of a policy decision next week…

BoJ BUYS and nobody bats as much as an eyelash? Perhaps they (or someone … anyone named BILL) might like some 2s which are on offer this afternoon,

Never mind … here is a snapshot OF USTs as of 705a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed with the curve pivoting flatter around an unchanged 20yr point ahead of this afternoon's 2-year Treasury auction. Treasuries have underperformed Bunds and Gilts this morning after some weak PMI readings and bank lending data (ECB; see links above) there. DXY is higher (+0.3%) while front WTI futures have seen a modest rebound (+0.5%). Asian stocks were mostly higher, EU and UK share markets are mixed while ES futures are showing +0.5% here at 6:45am. Our overnight US rates flows saw better selling in the long-end (10's-30's) from real$ during the rangebound Asian hours. During London's AM session we had receiving in 10's to support prices before that rally faded as the front-end was hit. Fast$ names faded the flattening by adding 5s30s and 10s30s steepeners. Overnight Treasury volume was quite decent at ~145% of average.

… and for some MORE of the news you can use » The Morning Hark - 24 Oct 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ (in a similar sorta way you’ll find content if you pay for ZH PREMIUM … except different …)

Apollo - Costs of Capital Rising for Small Businesses (um, small biz are a large part of the economy and so … waiting, watching for shoes to drop…HIMCOs watching …)

There are 33 million small businesses in the US, and the monthly survey from the NFIB shows that small businesses are now paying 10% interest on short-term loans, see chart below.

In other words, Fed policy is working as the textbook would have predicted, and companies are facing higher costs of capital.

The outcome is lower capex spending and lower hiring.

The recent spike in real yields was unprecedented for nearly 3 decades, calling current equity valuations into question. However, we argue that real yields are unlikely to trigger a major equity de-rating absent a larger macro shock. We see modest fundamental downside from here after the recent selloff.

… The recent spike in real yields has called US equity valuations back into question, in terms of whether stock prices are fairly reflecting both a higher discount rate as well as the likely increase in funding costs. For real yields, we are in fairly uncharted territory as modern markets go. Not only are real yields—based on 10Y UST less 10Y breakeven—starting to break out of the tight range (-1.5% to +2.0%) they have maintained since November 2008 (i.e., GFC's QE1), the magnitude of the increase over the past year (+3.5% T12M) is unprecedented since TIPS started trading in 1998.

…Looking further back in time, to better look forward Point-in-time data doesn't tell the whole story, and TIPS/Breakeven data extends only to 1998. To do a more thorough analysis while maintaining the forward-looking tilt that best aligns with equity valuations, we turn to the University of Michigan Inflation Expectation Survey, which has data going back to 1978. We calculate a longer-dated proxy for real yields (10Y UST less UoM Inflation Survey) and apply this measure to look for historical instances of real yields making a move comparable to what we saw over the past year (+3% T12M), finding only two: 1979-82, and 1993-94.

In both cases, equity valuations continued falling until real yields peaked, which may make it tempting to conclude that stocks today are heading toward a major reckoning if real yields maintain their current trajectory. Still, we think that the reasons behind these sharp moves in real yields are more important for equities than the magnitude of the moves themselves…

Bespoke- Who's Buying Treasuries? (um, BILLs? umm, nobody? for ALL complete diggin you gotta go behind paywall but do you really?)

Who’s Buying All The Bonds? With Treasury bills yielding more than 5% and coupon Treasuries in aggregate yielding 4.9%, some of the highest yields in a generation are on offer across the term structure. But those same elevated yields continue to climb as the market searches for someone to take duration risk. Of course, there are lots of transactions taking place. In the chart below, we show the net purchases of all Treasury securities across a range of investor groups. Through the end of Q2 (the latest data available), households and non-profit institutions serving households had in aggregate purchased $673bn more UST debt this year than they had sold.

That’s more than twice the pace of the next-fastest buyer of Treasury bonds. Foreign investors have bought more than $300bn in Treasuries on a net basis this year, while money market mutual funds are also notable buyers. That investor type is entirely spending at the front of the curve. The same cannot be said for longer-term asset-liability matchers like insurance and pension funds which have purchased $156bn this year. Of course, with aggregate supply up by $916bn in the first half, big buyers are needed…and that’s before the large scale selling that has hit banks (trimming duration to match deposit outflows) as well as the Federal Reserve (as part of the ongoing process of quantitative tightening).

We revised up our projection for US Q3 2023 GDP growth to 4.5% q/q saar (versus 3.5% previously) on the back of significantly firmer growth in consumer spending.

Q3 strength implies there could be enough momentum to lift our projections for Q4 as well – we now estimate growth in the vicinity of 1.5% q/q saar in Q4 (versus 0.5% previously). Nonetheless, we retain our forecast for significant deceleration in activity into year-end due to a confluence of strong headwinds hitting the consumer amid increased geopolitical and domestic political uncertainty.

The bulk of growth in Q3 will likely come from consumers splurging on both goods and services, as a narrowing trade deficit, surging residential construction and modest buildup in inventories will supplement growth in personal consumption.

CitiFX Techs - Watch for the bond turn (but wait, I thought it was BILLs)

Price action overnight indicates exhaustion in the US bond selloff. We are biased towards bull steepening in the medium term.

… Why bull steepening ?

Upside on US 10y yields looks increasingly limited. US 2y yields are on the verge of testing critical support again. In tandem, this supports a bullish turn for bonds.

2y yields are close to testing 55-day MA, the critical support level we have been watching (>45bps to formation indicated target)

10y yields are facing stiff resistance at the 5% psychological level.

While the bearish outside day on 10y yields has not historically been a good downside indicator, we think that the move back below the 4.88% handle (October 4 high) is a significant sign of resistance at 5%.

Addressing steepening: We remain firmly in the steepening camp (as we have been for some time)…

FirstTrust- Monday Morning Outlook - Growth Surge in Q3 Masks Weak Trend (we’ve heard this before … still worth noting / reading eventually gonna be right)

… Why do we still think a recession is coming? Because after the surge in money creation in 2020-21, monetary policy started getting tight in 2022. In the past year the M2 measure of the money supply is down 3.7%. Meanwhile the yield curve (we like to compare the 10-year Treasury yield to the target federal funds rate) has been inverted since late 2022 and is likely to stay that way for at least the next several months.

Higher short-term interest rates mean businesses have the ability to lock in healthy nominal returns on cash with minimal risk. In turn, this should lead to a reduction in risk-taking and business investment.

Meanwhile, jobs are still expanding rapidly. Payrolls are up 2.1% in the past year. During the economic expansion that happened before COVID (mid-2009 through early 2020), a pace that fast (2.1% or more) only happened when the unemployment rate was about 5.5%, which meant plenty of workers still available for hire. Now it’s happening when the unemployment rate is less than 4.0%. This suggests employers are out over their skis and vulnerable to any softness in demand.

The bottom line is that the economy grew rapidly in Q3 but Q4 and beyond are likely to be much slower…

… Add it all up, and we get a 4.7% annual real GDP growth rate for the third quarter. Look for much slower growth in the fourth quarter.

MS - US Economics: Ahead of the November FOMC: Our Monetary Forecasts

We participate in the NY Fed's Survey of Primary Dealers, which collects expectations about monetary policy and economic indicators in advance of each FOMC meeting. In this note we provide a snapshot of our responses to the survey.

UBS - Where to after 5%? (so, PEAK not just a peek)

… Where do we go from here? Our view is that we are at or close to the cyclical peak. We have not changed our view that policy rates are now restrictive, and that the transmission of these policy rates will continue to put pressure on inflation and growth…

… We still see value in the 1-10yr segment, particularly the 5yr point, as running yield and capital upside should quickly reverse recent drawdowns. YTD we have not seen the "Year of Bonds" as many had expected; however, despite nearly 100bps of moves higher, the total return on a 5yr high-quality bond investment is essentially flat, demonstrating how higher outright yields levels can protect against markto-market volatility with potential upside.

WisdomTree- Prof. Siegel: The Current Narrative Is Dominated by Bonds

The current market narrative is dominated by the action in the bond market, with the 10-year yield briefly touching 5% last week. Concerns about rates staying higher for much longer are keeping long yields ticking higher. I do think the recent high inflation that we’ve experienced is raising the premiums and compensation demanded to own bonds. This is not just a short-term phenomenon, but something that can last for a number of years.

Fed Chairman Powell spoke last week and confirmed what we’ve been saying for weeks—that the Fed is not going to move rates on November 1. The principal reason is what I just mentioned—the higher long-end rates are tightening conditions without the Fed raising short-term rates. It seems Powell has been very successful at getting unanimity and no dissent and the chorus from recent Fed officials hinted for another pause. It could also very well be that the last rate hike already occurred, and the Fed is now in permanent pause mode. The data over the coming months will dictate the rates, of course…

… How high will long-end rates go? Technicians have called for 5.1% to 5.2%. I would be very surprised if the 10-year goes above 5.25% because I don't see inflation moving up. The Middle East is a problem, and oil is a wild card, but other commodities are certainly being pressured by higher real rates and a stronger dollar. There have been momentum traders jumping on the “short bonds” bandwagon. If we get any weak economic data reports at all, I expect the Fed to cut rates.

Yardeni - Ackman's Big Short (but … but … what about the other guy)

“There is too much risk in the world to remain short bonds at current long-term rates,” Bill Ackman said in a post on X, formerly known as Twitter, this morning. “We covered our bond short.”

He first disclosed his Big Short on August 2 on X, one day after Fitch Ratings downgraded US Treasuries from AAA to AA+, and two days after the Treasury Department announced that the government would need to raise $1.0 trillion during Q3. It was a brilliant trade as the 30-year bond yield soared from 4.11% to 5.11% on Friday. This yield peaked at 5.18% at 6:00 am this morning. Ackman's announcement contributed to the rally in bonds today, as the yield fell to 5.01% (chart).

The "5" handle on both the 10-year and 30-year yields signaled a good place to take profits for the shorts since the two yields are back to their Old Normal levels, i.e., where they were from 2002-2007, before the Great Abnormal period from the Great Financial Crisis through the Great Virus Crisis…

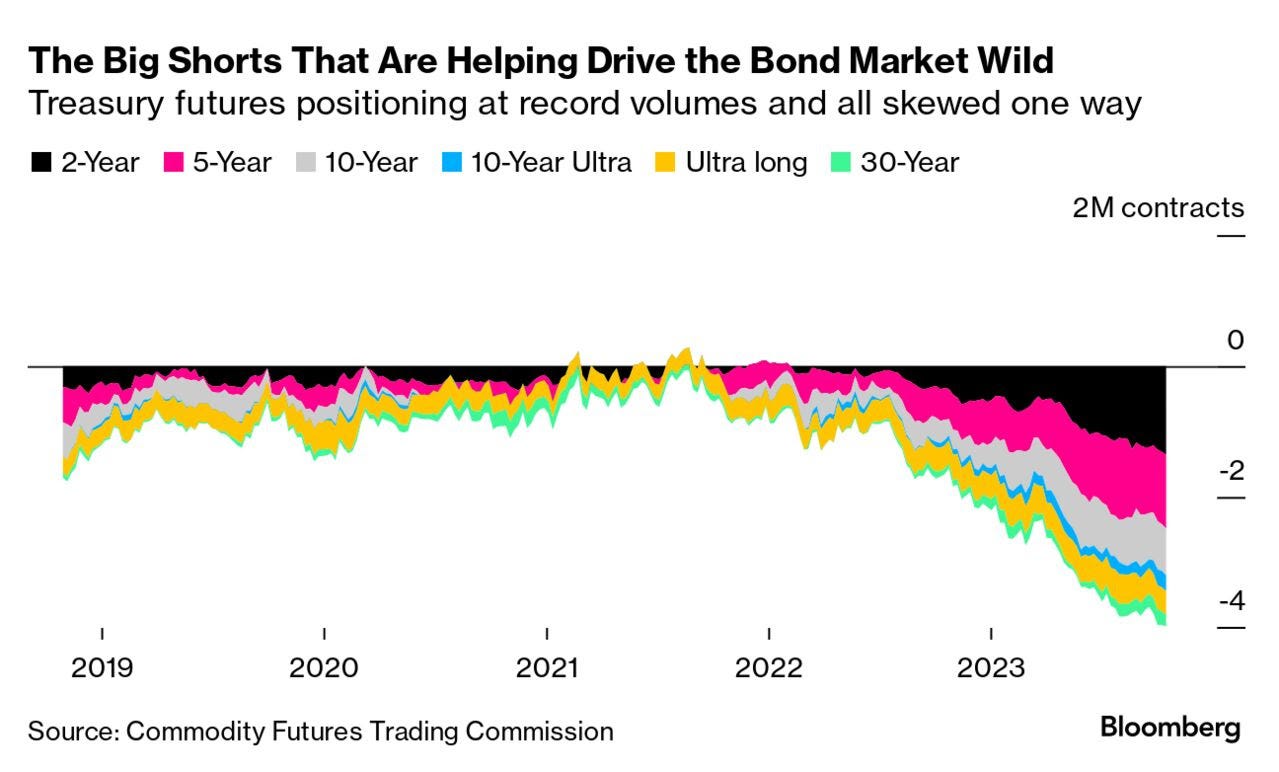

… Treasuries came roaring back in Monday’s US trading session in what looks like an epic episode of short covering. Futures traders had been massively overbalanced toward bets on further declines in US government securities, based on the latest data from the Commodity Futures Trading Commission. In the week that ended last Tuesday the net short across the six Treasury futures contract was almost 4 million contracts, way larger than the previous combined record of 2.2 million in mid-2018. Trader bets on declines outweigh those on gains for each individual contract and have done since June 2022, also an unprecedented stretch.

A large part of this setup appears to have been driven by an explosion in so-called basis trades — placed to benefit from the mismatch between the prices of futures and of the underlying bonds — but a short is still a short,. And when you have trades this crowded, the kind of wild swings witnessed in Treasuries seem almost inevitable.

That’s a problem for global markets given the key role Treasuries play as an allegedly risk-free asset and as a proxy for the cost of money. It also makes it very hard to be sure that this latest rally signals the worst has been and gone for bonds, or if this is just another wave of pain washing through the market.

Bloomberg- Long Bond Trade Hinges On Health Of The Service Economy (THAT LB trade as in buying dips … NOT to be trusted)

Authored by Simon White, Bloomberg macro strategist,

It’s hard to see what would drive a significant and sustained rally in bonds without a US recession. A downturn hinges on the services part of the economy, where the outlook is balanced.

Powell’s comments on Thursday gave fuel to hawks and doves. Bonds are oversold, but not yet at extremes, thus yields could easily climb higher in the absence of any flight-to-safety move.

But for anyone waiting to go long bonds, the best catalyst would be a US recession (even if yields would likely not fall as far as in a regular, non-inflationary downturn). However, that is looking less likely than not now, with US and global economies on the threshold of a cyclical upswing.

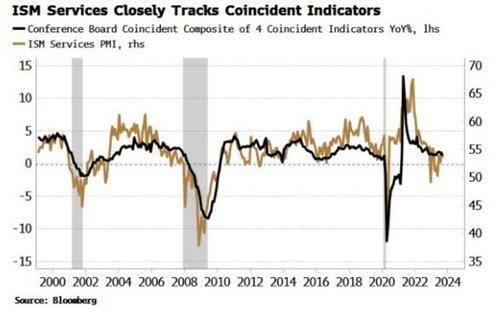

Leading indicators had been anticipating a recession earlier in the year. But that was not confirmed by coincident indicators. Both indicators have historically been contracting at the same time for there to be a recession.

There have been several false positives over the last 60 years where leading indicators have troughed but coincident ones have not (and only one where it was the other way around). The unique circumstances of the pandemic meant goods GDP was contracting from a high level – indicating recession – but services GDP was playing catch-up all the time. It’s looking like another false positive.

It hinges on services. The Conference Board’s Coincident Index is highly correlated to the services ISM.

The outlook for services is balanced. The ISM report is back above 50, but there is still some weakness in the S&P’s services PMI. However, the latter tends to revert to the ISM’s measure rather than the other way around. The strong retail sales report on Tuesday is another tentative sign the service economy is improving.

The US should avoid a recession as long as services does not worsen, as the highly cyclical manufacturing sector looks to have already turned the corner. Thus bonds are unlikely to experience any more than transient rallies, as the pull from rising nominal growth keeps yields elevated.

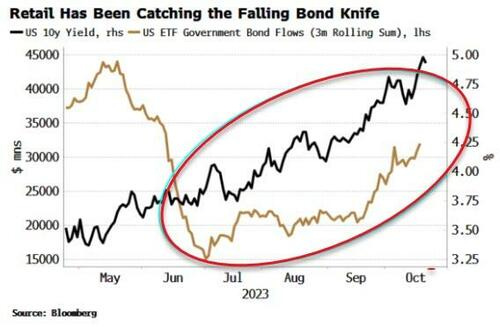

Bloomberg - Retail Getting The Message Stocks & Bonds Can Fall Together (about that LONG BOND trade …)

… While retail may thus face more stock losses, they have also had their hands bloodied by trying to catch the falling bond knife this year.

Using ETF flows as a proxy, they likely accelerated their net purchases of government bonds in the summer as yield rises started to pick up, and have chased prices lower ever since.

According to the AAII, investors have increased their stock and bond allocations this year, and reduced their cash allocations, despite very attractive cash yields.

That shows either enormous faith in financial assets to deliver fairly exceptional returns despite an elevated inflation backdrop, or that they have yet to adjust to the new financial order.

Bloomberg- What the Federal Funds Rate Isn’t Telling You (always funtertaining when X Fed spill their guts … were they telling us truths then or now?)

Broader financial conditions matter for the economic outlook. The Fed is right to focus on them.

Lately, Federal Reserve officials have been paying greater attention to financial conditions – that is, to the influence that market phenomena such as stock prices, bond yields and housing prices have on economic activity, above and beyond the effect of the short-term interest rates that the central bank controls directly.

This is a welcome development for monetary policy — and for me personally.

Nearly 25 years ago, when I was chief US economist at Goldman Sachs, my colleague Jan Hatzius and I created a financial conditions index as a tool for assessing the economic outlook and the appropriateness of the Fed’s monetary policy stance. While its construction has evolved considerably since then, the conceptual framework remains intact. Over the years, many others developed comparable indexes. This summer, the Fed introduced a new one of its own.

… The shorter lags are visible in the Fed’s new financial conditions index. The version that uses a one-year lookback window hit its point of greatest restraint last December, long before the federal funds rate reached its current peak. In contrast, the index was around zero at the end of September, indicating that financial conditions were providing no added impetus, up or down, to economic activity.

… I’m glad to see financial conditions finally getting the attention that they deserve. They should be viewed not as all-encompassing, but as one tool to help assess the stance of monetary policy and its likely evolution. To that end, they’re more valuable than mechanical guides such as the Taylor rule, which aren’t forward-looking and don’t consider how financial market developments influence the economic outlook and monetary policy.

Bloomberg- Bill and Bill's Big Adventure in Treasuries Land (Authers OpED)

… He went on to assert that there was “too much risk in the world” to remain short, and that the economy was “slowing faster than recent data suggests.” Ackman is a successful hedge fund manager who has built his fortune taking highly concentrated stakes in a few equities, and often agitating for them to make changes. Activist investing can work on a medium-sized company if you have the resources of a large hedge fund to deploy. Neither Ackman nor any other private investor has anything like enough money to move the entire Treasury bond market on his own. Pershing Square has assets under management of $18 billion. The total value of the Treasury market is about $24 trillion. But coming when it did, it certainly looks as though his intervention made a difference:

Bill Gross is a different case. Known as the Bond King for good reason, he founded and built Pacific Investment Management Corp. (Pimco) into the biggest bond investor on the planet, doing a great job of navigating the long bull market in bonds. However, it’s now nine years since he left Pimco, under something of a cloud after a big and unsuccessful bet that bond yields would rise after the financial crisis went bad. His subsequent venture with Janus Henderson didn’t work out. He doesn’t control money on a Pimco scale any more. While histake on Treasuries plainly continues to matter more than those of us mere mortals, it’s not obvious that opinion from him should make a difference. But it looks like it did. This is what he posted to X shortly are 11p.m.:

SOFR futures, for the uninitiated, are linked to the Secured Overnight Financing Rate. You can generally work out their value by subtracting the current fed funds rate from 100. They thus offer a very direct way to bet on imminent rate cuts by the Federal Reserve — and a look at the latest chart for SOFR futures does indeed make it look like there might be a buying opportunity there:

Reams of data on the US economy are available to all of us, of course, and most economists — of all political persuasions — entered this year confident that we would already be in a recession by now. We aren’t…

WolfST: Spectacle Ensues after 10-Year Treasury Yield Pierces 5%: Huge Demand Piles in, Yield Plunges 19 Basis Points in Hours (all the cool kids talkin’ 10s)

… As if someone had flicked a switch, human investors and algos that had apparently waited on the sidelines for just that moment jumped in, buying hand over fist at this signal, pushing up prices of those maturities, and thereby pushing down the 10-year yield by 19 basis points in a matter of hours, from 5.02% in early trading, to 4.83% currently, back where it had been on October 18 (hourly price chart by Investing.com):

Obviously, there was no such sudden change in sentiment about the US debt; and Congress hadn’t just voted this morning to drastically reduce the budget deficit in a bipartisan manner by cutting spending and increasing taxes in some equitable manner, LOL. It was a market reaction to one of the most anticipated key numbers: the 10-year Treasury yield hitting 5% …

At least we’ve got THAT going for us … which is nice. AND … THAT is all for now. Off to the day job…

Have heard Bill Gross on MacAlveny podcast a couple of times, always seemed very insightful. Have never heard about his Pimco & Janus adventures. I continue to relearn the lesson of giving some folks much too much presumed credibility. Amazing analysis & content, my day feels incomplete until I read my daily BondBeat, THANK YOU!

Have heard Bill Gross on MacAlveny podcast a couple of times, always seemed very insightful. Have never heard about his Pimco & Janus adventures. I continue to relearn the lesson of giving some folks much too much presumed credibility. Amazing analysis & content, my day feels incomplete until I read my daily BondBeat, THANK YOU!

Excellent article !!!!

Famous WS adage: " they don't ring a bell at the top"....but we did hear some famous Traders say

Enough is Enough.... as you describe so beautifully...

Thought I heard Bill Gross talk about some unspecified Economic data pointing to an imminent Recession......wonder what the were ???

I think back to Mr Lacy's video......

Do you ever watch the Credit Default Swaps on the Large and Regional Banks ???

Wonder how they are looking??? Rising ???

I don't know those symbols.....

Maybe 5 % will be significant resistance....

Heard another Money Manager..Sri something...talking about, even though the Fed doesn't

directly control the Long End of the Bond Market, they were in jeopardy of losing control of it.

He seemed pretty worried that if rates continued meaningfully higher, something was going to

break and soon.....

It seems strange to me that we can have a 4% GDP Q3 and yet slow meaningfully into Q4.

I can somewhat see post Christmas Q1 being slower.... but the economy appears to have some

momentum, with all due respect to Bill, Bill and Mr Lacy.

VERY UNCLEAR...

Glad the Bond Fever has broken, even if it's only TRANSITORY......Oops....