(USTs MIXED, mixed data o/n)while WE slept (and while I am still catching up with moves and responses TO data, central planners letters TO Santa, etc...)

ANSWER — LOTS. For starters, weaker than exp PPI (not a game changer for the FED), STRONGER ReSale Tales (clearly ALSO perceived to NOT be a game changer for the Fed), TONS of data out of China, ECB, BOE and, well, the FED so …

ZH: Core Producer Price Inflation Tumbles To 2.0% - Near 3 Year Lows

… This all seems like great news but we remind readers that the swing factor continues to be commodity prices, which in turn depend on how much stimulus China decides on, how much oil OPEC+ will pump and how much crude Biden will quietly dump to keep gas prices low into the election year.

ZH: Fed 'Dots' Signal Major Dovish Pivot For Election Year ZH: Fed 'Dovish Pivot' Sparks Panic-Bid In Bonds, Stocks, & Gold

Bloomberg: China Expands Cash Coffers With 13th Consecutive Loan Injection (and more than 2x what was expected…)

To be clear, I have been misinformed plenty over the past 3 decades and in as far as recency bias goes, back in March I might have ventured something (SVB) finally broke. The Fed has declared victory and was winning but then … it was winning TOO much and launched new funding initiatives and added liquidity (targeted) and re-saved the world. Something ‘bout firemen also being the arsonist?

Cycle forward to here and now, rate cuts depending on inflation cooperating and data ONLY slowing down NOT producing a stagflationary recession seems like a BIG ASK to me and it would appear by curve shape shifting (and persistent LONG END BID) counter TO 2024 being the year of the bull steepening … here we go again?

Dunno BUT a look at long bonds …

… overBOUGHT — ok fine but hasn’t seemed to matter much (‘til it does) and the downtrend remains in place. Being so close TO 4% — more psychological level as much as anything else technically significant — I’ll watch todays weekly close in and around proximity to this level … For now, here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed and off earlier highs set after German and French PMI disappointed for December. Japan's PMI was mixed and China's overnight data was mixed too (see above). DXY is modestly higher (+0.1%) while front WTI futures are too (+0.45%). Asian stocks were mostly higher, EU and UK share markets are mixed (SX5E +0.5%, FTSE 100 -0.5%) while ES futures are showing +0.25% here at 6:45am. Our overnight US rates flows saw a much more subdued trade with our London desk seeing early real$ buying in 2's-3's and then selling in 10's after Treasuries extended their gains after the European PMI prints. Overnight Treasury volume was …

… Here in the near-term, carry headwinds for 2-year Treasuries may be a reason why 2's have started to show some consolidation near June's [closing] move low in yields at ~4.34%. Our next attachment looks at the longer-term history of the Tsy 2yrs vs overnight GC rate spread. Yesterday 2yr yields pressed below -100bp through GC early in NY trading and seemed to run out of steam as soon as they did so. Keep in mind that the time series shown here is based on monthly closes so the intra-month push to the -135bp area for this spread during this spring's banking ructions... is not picked up. Anyway, we'd guess that the front-end faces stiffening [carry] headwinds here absent data that may lead one to assume a rate cut's imminent. Yesterday's claims, retail sales and Q4 GDP NowCast prints left no such vibe, certainly…

… AND this in addition TO taking look at bullish longer-term RESISTANCE for 5yy … and for some MORE of the news you can use » The Morning Hark - 15 Dec 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … and what follows is one (small)part PPI, ReSale TALES and FOMC … with a good chance I’ve missed something hopefully to be caught over the weekend …

Barclays: PCE inflation preview: Soft PPI data mark down PCE price forecasts (thats good, at least for rate cut ‘istas)

We estimate that PCE prices fell 0.1% m/m (2.7% y/y) in November, and that core inched up 0.02% m/m (3.2% y/y). The softening reflects a sharp deflation in core goods, as well as another month of soft core services. With a persistent wedge opening between PCE and CPI core inflation, we mark down our PCE inflation forecast.

Barclays: Federal Reserve Commentary: December FOMC: Open the flood gates

The FOMC kept the policy rate unchanged and softened slightly its tightening bias. The latest SEP indicates three 25bp rate cuts in 2024, in the face of softer inflation projections, and Powell fueled expectations of cuts, as they "come into view." We change our rate call and now expect three rate cuts starting in June.

Consumers fended off the Grinch in November, with strong online sales and robust food services propelling a stronger-than-expected 0.3% m/m gain. Even with downward revisions to October, today's numbers position consumers for another solid spending increase in Q4, with orderly slowing from the robust Q4 gain.

Barclays: November Atlanta Fed wage tracker suggests that wage deceleration has stalled

The unsmoothed October Atlanta Fed wage tracker print decreased, while the weighted 3mma measure showed no change from October. Our state-space model, which draws signals about the underlying pace of wage growth from available measures, shows leveled growth recently.

November data showed domestic demand took a further step down, with retail sales growth almost halving and most major housing indicators deteriorating. We think risks to our below-consensus Q1 and 2024 growth forecasts are tilted to the downside, given the CEWC fell short of offering clues on new or large-scale stimulus.

The overall tone of communication from the December FOMC meeting showed policymakers increasingly confident that they have achieved a sufficiently restrictive policy stance. The committee paid lip service to the prospect of further tightening, but it is evident that policymakers are starting to train their focus on the timing of cuts.

The dot plot signaled 75bp of cuts in 2024, but Fed Chair Powell emphasized that this is an amalgamation of forecasts and not a plan. Two participants saw no cuts, while the most aggressive forecast anticipated six cuts.

Powell repeatedly cautioned against premature declarations of victory in the Fed’s inflation fight, but provided only limited pushback on the substantial inter-meeting easing of financial conditions. He merely stated: “It is important for financial conditions to become aligned with what we want to accomplish … in the meantime, there can be back and forth … ultimately they will have to come along”.

Markets broadly saw the Fed communication as dovish and pushed the probability of rate cuts by January to 17% and by March to about 90% by the end of the trading session.

While we cannot rule out the possibility of earlier hikes relative to our baseline forecast of May, recent economic data gives us pause, including sticky wage inflation, upward surprises in CPI services and a still-resilient labor market. Downside surprises in the activity data, particularly nonfarm payrolls, or the aforementioned sticky inflation components could open the door to earlier action.

… Interest rate strategy: From a market perspective, today’s FOMC statement, the SEP and the press conference were more notable for what was absent. The material rally in rates and deepening in cut pricing had taken a breather since the start of the month, in part thanks to sufficiently firm data, but also amid trepidation around the risk that the Fed might strike a more hawkish tone given the extent of financial conditions easing. The absence of any real pushback today was taken as a green light to press on the asymmetry towards rate cuts, with real rates notably outperforming in the rally.

To the extent that the burden was on the data to deliver before, the repricing – with about 80% of a cut priced for March and nearly 6 cuts priced for 2024 as a whole – only underscores that further. We do, on a terminal basis, see room for short term rates to outperform the forwards into the middle of next year and beyond, and think the market’s inflation path – implying a swifter return to target than under the Fed’s (or our own) baseline – suggests the market is at least internally consistent and not misinterpreting the Fed’s reaction function. However, we think the environment is one where it is harder to sit in outright longs, and favors structures that seek to mitigate carry while retaining a bias towards bull steepening.

DB: December FOMC: Powell breaks out punchbowl early at the holiday party

The Fed held rates steady for the third consecutive meeting. Although the Committee maintained a soft tightening bias, the statement, Summary of Economic Projections (SEP) and Powell's press conference all skewed in a dovish direction, indicating that this bias could soon be dropped. Specifically, the statement softened the guidance language around "additional policy firming", the median dot in the SEP anticipated 75bps of rate cuts in 2024, and Powell indicated that early discussions about rate cuts have started.

In response, the market priced an even more aggressive cutting profile in 2024, moving further in line with our long-held view. While our baseline remains that the first rate cut is likely to come in June 2024 and that the Fed will reduce rates by 175bps next year, today's meeting points to dovish risks to this expectation (see “2024 Outlook: Fed WINs in ’24, but at what cost?”). We see heightened risks that rate cuts could come as early as March (see "How soon is too soon for soft-landing rate cuts?"). Earlier policy easing in the presence of more substantial disinflation would improve soft landing prospects.

DB: Decelerating inflation data drive dovish December surprise

As we wrote in our FOMC recap, yesterday’s FOMC surprised with dovish elements throughout the statement, dot plot and Chair Powell’s press conference (see “Powell breaks out punchbowl early at the holiday party”). The full embrace of a dovish tone, punctuated by a willingness to kick off the discussion about rate cuts, was the most surprising feature of the meeting.

A common question after this turnaround was: What changed relative to two weeks prior when Powell stated discussions about rate cuts were "premature"? We provide a perspective on this question in this brief note.

Goldilocks: FOMC Keeps Funds Rate Unchanged, Projects Three Cuts in 2024, Revises Inflation and Growth Forecasts Slightly Lower

BOTTOM LINE: The FOMC left the target range for the federal funds rate unchanged at its December meeting. The median dot in the Summary of Economic Projections showed 75bp of cuts in 2024, 25bp more than in the September projections. The median dot for 2026 was unchanged at 2.875%, modestly above the median longer run dot, which was also unchanged at 2.5%. For 2024, the Summary of Economic Projections showed lower core inflation (-0.2pp to 2.4%), slightly lower GDP growth (-0.1pp to +1.4%), and an unchanged unemployment rate (at 4.1%).

Golidlocks: December FOMC Recap: A Faster Return to the 2% Target Means Faster Cuts

■ The FOMC delivered a dovish message at its December meeting, but we learned more about the inflation outlook today than about the FOMC’s reaction function. The soft PPI report on Tuesday morning combined with downward revisions to prior months implies that core PCE inflation was only 0.07% month-on-month and—as Chair Powell noted in the press conference—only 3.1% year-on-year in November. By some measures, the trend is already at or near 2%.

■ In light of the faster return to target, we now expect the FOMC to cut earlier and faster. We now forecast three consecutive 25bp cuts in March, May, and June to reset the policy rate from a level that the FOMC will likely soon come to see as far offside, followed by quarterly cuts to a terminal rate of 3.25-3.5%, 25bp lower than we previously expected. We are quite uncertain about the pace, in part because it will depend on how financial conditions respond to rate cuts. Our revised probability-weighted Fed forecast is similar to both our baseline and market pricing.

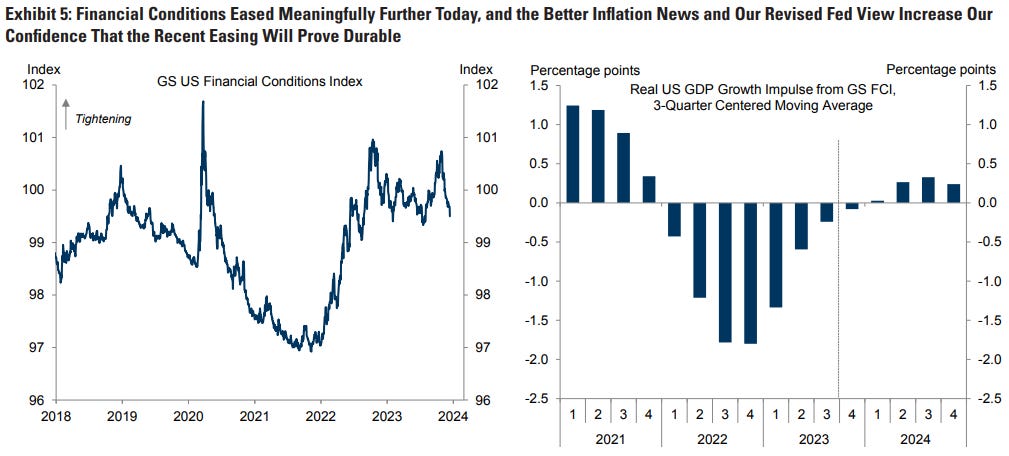

■ Financial conditions eased further today, and we are more confident that the large easing since October will prove durable now that the lower inflation path makes substantial rate cuts more likely next year. As a result, we are taking more of the easing on board in our economic forecast and bumping up 2024 Q4/Q4 GDP growth by 0.2pp to 2%, about double the consensus forecast and above the FOMC’s 1.4% forecast. We do not see our above-consensus growth forecast as incompatible with faster cuts because inflation is likely to be the main driver of cuts and Powell noted that FOMC participants are “very focused” on the risk of staying too high for too long.

Goldilocks: Retail Sales Rise but Prior Months Revised Down; Import Prices Decline; Initial Claims Fall Below Expectations

BOTTOM LINE: Core retail sales rose 0.4% in November, 0.2pp above consensus expectations and driven by a 1.0% rise in the nonstore category. However, the level of spending in October was revised down 0.2pp and pharmacy spending continues to be temporarily supported by Covid booster shots. November retail sales were above our previous expectations on net, and we will update our GDP tracking estimates following the mid-morning data. Import prices declined by less than consensus expectations in November, while import prices ex-petroleum increased. Following this morning’s import price data, we left our November core and headline PCE inflation estimates unchanged at +0.07% and -0.06%, respectively, corresponding to year-over-year rates of 3.11% and 2.60% respectively. Initial claims fell below expectations, while continuing claims were roughly in line with consensus expectations.

FirstTrust: Research Reports - Fed Declares Mission Accomplished

… The Fed didn’t change short-term interest rates today, nor did it alter the pace of Quantitative Tightening, but it made major changes to its projections for short-term interest rates. Not one policymaker on the Federal Open Market Committee thinks the short-term interest rate target will be higher a year from now than it is today, which is 5.375%. And while the median forecast from policymakers in September was one rate cut of 25 basis points in 2024, now the median projection is 75 bps. In turn, the median policymaker projects another 100 bps in rate cuts in 2025 and then another 75 bps in 2026.

…Moreover, the Fed should be focused on not cutting rates too aggressively and prematurely, which could re-ignite the inflation problem like the Fed did on multiple occasions under Chairman Arthur Burns in the 1970s. The economy is still growing for now, but we think it falls into recession in 2024 and that real GDP growth significantly lags the 1.4% predicted by the FOMC. Given that the Fed has now signaled 75 bps in rate cuts even in an environment of moderate growth, if we are right about economic growth it will be very difficult for the Fed to resist generating higher inflation in 2025 and beyond.

JEFF: FOMC Leaves Rates Unchanged For Third Straight Meeting, Signals End of Hiking Cycle

Key Points ■ The Fed left all target and administered rates unchanged, as expected. ■ The policy statement was relatively little changed from the last two renditions, but the subtle edits carry significant weight. The addition of the word "any" ahead of potential policy firming suggests less confidence that more firming will be needed. They also acknowledged the easing of inflation pressure and some evidence that growth has slowed from the robust pace of Q3. The statement also retained a reference to financial conditions potentially weighing on growth and inflation, despite the easing in financial conditions over the past month. ■ Powell and company do not want financial conditions to ease too much further, so they are keeping their options open for another hike as much as possible. However, given the recent progress in the data towards the dual mandate goals, it seems like the writing is on the wall for this hiking cycle.

The Fed is firmly on hold and now discussing the timing of cuts. Further downward surprises in core services inflation or pronounced deterioration in macro data would challenge our call for a June cut. Our strategists stay neutral on duration, and long agency MBS.

… Our rates strategists see limited risk-reward in pushing duration longs – with our economists expecting the first cut in June, and markets pricing a nearly 90% chance of a cut in March. They remain tactically neutral, and maintain long 10s on 5s10s30s fly, as a relative value trade.

This meeting revealed a much softer Fed emboldened by the recent fall in inflation. They are now thinking more about landing the economy softly than getting inflation all the way down to 2%. They have even started thinking about how to cut rates.

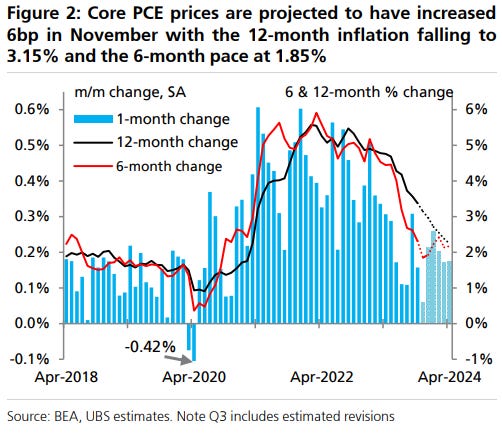

… Inflation still seems to be falling faster than they are projecting Translating the inflation data released this week (November CPI and PPI data) into estimates of November PCE prices, we estimate headline PCE inflation will fall to 2.6% in November. We estimate core PCE inflation is set to fall to 3.1%. As the graphs below show, the current 6-month annualized changes in core and PCE prices sat at 2.5% in the October data. Based on our translations of CPI and PPI data into PCE prices, those rates look set to fall to or below the FOMC's 2.0% target in the November data.

PPI implies 6-month core PCE inflation below the Fed's 2% target…

UBS: Core PCE tracking slower; claims fall as expected; retail sales look ok in November

Core PCE price tracking nudged down after import prices: now 0.05%…

Retail sales post decent November gain; prior months lower Retail and food services sales posted a decent 0.3% increase in November, better than the modest decline we and consensus expected. Sales at the control group of stores moved up a better than expected 0.4% too. However, the preceding months' sales for both headline and control group sales were revised down a cumulative 0.2% in the report undoing some of the sheen of the better-than-expected November outturn.

In yesterday's press conference Chair Powell picked up on a joke we had made… with all the strength in goods spending, residential investment looks resilient perhaps because people need space to put all this stuff. Within the details of the report, non-store retailers, which includes on-line purchases, posted a 1.0% increase in November. Sporting goods sales rose 1.3%, as hockey season ramps in earnest, and clothing sales rose 0.6%. Eating out did well too, rising 1.6% in November on the back of the 0.6% October increase. Declining gas prices weighed on sales at gas stations, down 2.9% in November. Sales of electronics, building materials and supplies, and at department stores all declined last month. Motor vehicle and parts sales moved up, again kind of out of sync with the lightweight vehicle sales reported by the BEA. Overall, the report will nudge up our Q4 GDP tracking which was at 1-1/4 percent (saar), but not a lot. We also get inventory data later this morning.

Initial claims fall in line with our expectations…

Import prices fall but ex-fuels stalls…

Wells Fargo: December FOMC: Dipping Dots—The Monetary Policy of the Future

Summary The doves won the day at the last FOMC meeting of 2023. The Federal Reserve left its policy rate unchanged at its December 12-13 meeting, a move that was widely anticipated. More important were the changes to the post-meeting statement and the latest Summary of Economic Projections (SEP). The new statement noted that inflation "has eased" over the past year, although still being elevated. The door was left ajar for additional tightening, but the "dot plot" signals that this was not the base case for most participants. The median projection in the dot plot called for 75 bps of easing in 2024 followed by another 100 bps of rate cuts in 2025. A more benign inflation outlook explains why the dots were revised lower for the first time since June 2020.

The job is not yet finished on the inflation fight, and the Committee will need to see additional data to confirm that the recent deceleration in prices is firmly entrenched. That said, the trend appears to be in place, and we expect the incoming data to confirm that inflation is gradually returning to 2%. After a period of nearly two years of rapid monetary policy tightening, a pivot to cuts next year seems like the most probable outcome. We expect the first rate cut of the easing cycle to occur at the June FOMC meeting.

Wells Fargo: Upside Surprise in November Retail Sales Signals Sustained Consumer

Summary The upside surprise in November retail sales is indicative of the continued staying power on the part of consumers. A decent holiday season looks to be in full swing, though we remain cautious if recent momentum can be sustained in the new year.

… In terms of total economic growth, it's this control group measure that matters because it aligns better with broader consumer spending in the GDP report. After adjusting for price growth last month, we estimate inflation-adjusted control group sales rose 0.9%, which suggests some slight upside risk to our 2% annualized figure for growth in real personal consumption expenditures in Q4 …

Yardeni: Bond & Stock Prices In Mini Meltup Over Soft Landing

Investors are obviously relieved that the economy may be on a sustainable soft-landing path and might avoid a recession (again) in 2024. They are especially relieved that Fed Chair Jerome Powell recently implied that he and his colleagues are relieved about this too and are talking more dovish now:

(1) Waller. For example, two weeks ago, Fed Governor Christopher Waller, in a November 28 speech titled, "Something Appears to Be Giving," said that if inflation continues to cool "for several more months—I don’t know how long that might be—three months, four months, five months—that we feel confident that inflation is really down and on its way, you could then start lowering the policy rate just because inflation is lower." He added, "It has nothing to do with trying to save the economy or recession."

(2) Powell. In his December 13 presser, Powell said: "I have always felt, since the beginning, that there was a possibility, because of the unusual situation, that the economy could cool off in a way that enabled inflation to come down without the kind of large job losses that have often been associated with high inflation and tightening cycles. So far, that's what we're seeing."

That sounds like a soft landing, and was confirmed as the consensus outlook of the FOMC participants in their latest Summary of Economic Projections also released on December 13. It implied three cuts in the federal funds rate (FFR) of 25bps each in 2024.

So there has been meltup rallies in both bond and stock prices in recent weeks. The 10-year Treasury yield has plunged from 4.99% on October 19 to 3.95% this evening. TLT is up 19.7% over this period (chart).

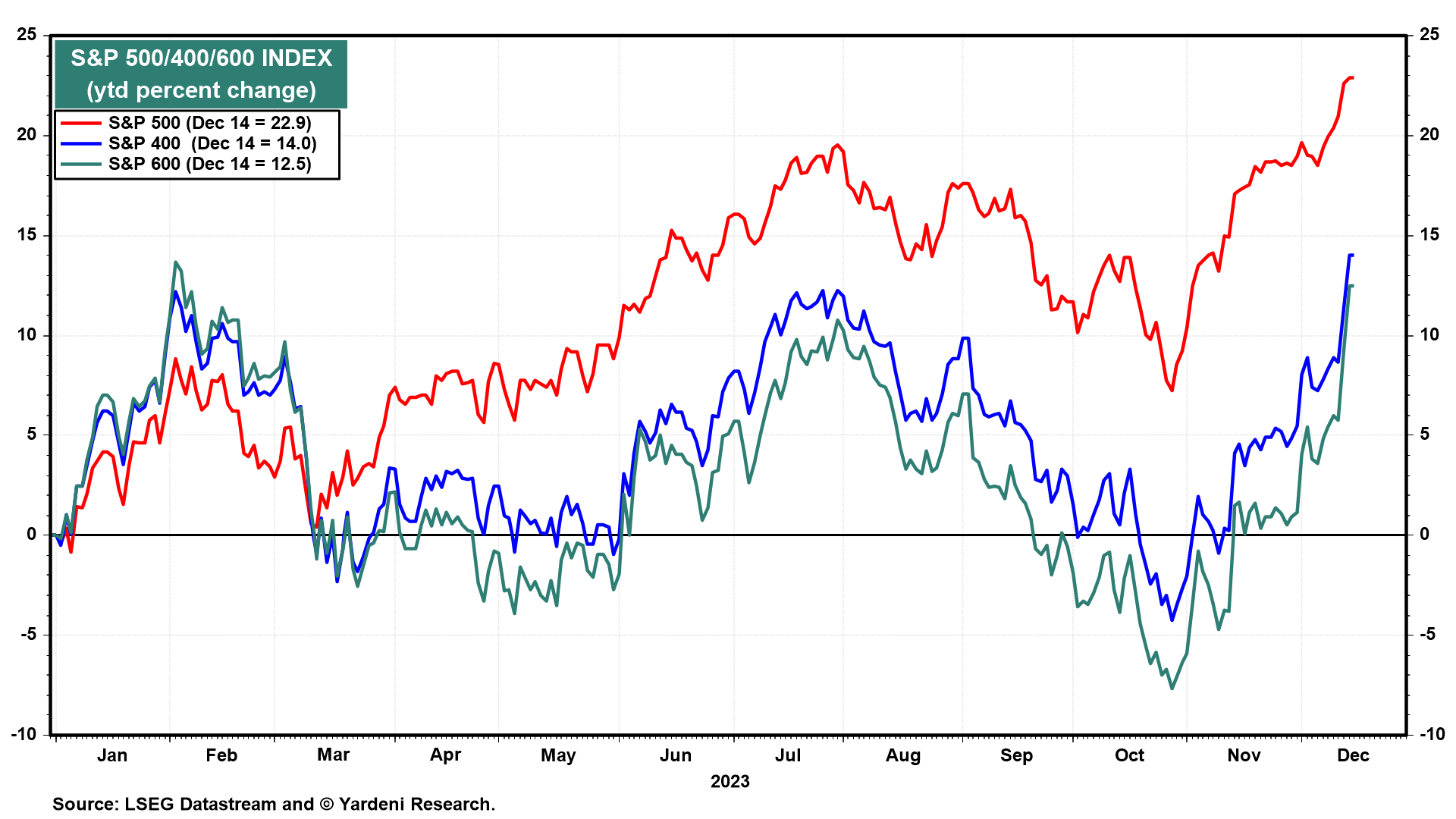

The S&P 500/400/600 are up 14.6%, 19.1%, and 21.8% since October 27 through today's close (chart).

The meltup relief rally is especially notable in the S&P 500 equal-weight index, which has been outperforming the S&P 500 market-weight index since November 13 (chart). The stock market rally is broadening now that investors are increasingly convinced that the Fed is done raising the FFR and might lower it next year, reducing the odds of a recession because inflation is moderating without one. That's been our forecast for a while. Happy holidays!

… And from Global Wall Street inbox TO the WWW,

Kimble: Rare Oversold Signal Could Send Russell 2000 Much Higher! (this caught MY attention … )

Nautilus Research: U.S. 10-year Treasury Yields Decline by -100 Basis Points

-100 BPS Swing Down from a Prior Swing Up Greater than 100 BPS, First Time in 1-year

On December 6th, we presented our analysis in a post titled 'Peak Short-term U.S. Yields.' At that time, U.S. 1-year yields stood at 5.05%, while U.S. 10-year yields were at 4.15%. In response to the Federal Reserve's shift towards a more dovish stance, we now observe rates of 4.82% and 3.94% for the same maturities this morning. This new weakness in 10-year U.S. Treasury yields represents a continuation of the downward trend since the peak in October, amounting to a significant “round number” of -100 basis points…

Nautilus Research: The "Magnetic" Attraction of Prior All Time Highs

SPX is Less than 3.50% Shy of its 1/3/2022 High, After Having Been in a Bear Market

The SPX is nearing its 1/3/22 high. Historically, when the S&P 500 approaches an all-time high after a bear market decline of at least -20%, there's a strong 90.90% chance of establishing a new high within six months.

Reviewing the data:

Within one month, the SPX reached a new high in only one of eleven instances (1982).

Extending to two to three months, eight of eleven times saw new highs with relatively limited drawdowns, except in 1971 and 1980.

In 1980, a -15.53% drop occurred but eventually led to a new high.

1971 was the only exception where a new high wasn't achieved within six months.

This history suggests the SPX's potential to rebound and set new all-time highs after significant bear market declines, providing insights into volatility and timing.

Finally, I hope to NOT ever prove this one out in theory OR in practice but …

AND back to markets and central planners … a couple letters TO Santa

big one today

Wow......Powell's Holiday Gift......Incredible!!!!

Soft Landing......Goldilocks???

Powell: Monetary Wizard or just Lucky ????

Powell is blessed with an extremely resilient Labor Market, partly based on Demographics.

(Older folks retiring early and creating opportunities for younger workers, Labor Pool Shrinks overall)

That's a petty Big Backstop....

It's been a LONG 3 YEARS.......

Hallelujah !!!!

Happy Hanukkah and Merry Christmas to all !!!!!