Good morning … In addition TO what the sellside was selling and noted yesterday, well, there isn’t much in addition. In other words, it’s been a relatively quiet evening and so

… here is a snapshot OF USTs as of 654a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed and the curve flatter as investors digest Friday's data and the risks from tomorrow's election, Thursday's CPI print and China re-opening uncertainties. DXY is lower (-0.4%) while front WTI futures are slightly lower (-0.4%) though front-month Nat Gas prices are up nearly 10% as the weather maps turn chilly for much of the US. Asian stocks were solidly higher despite the "no" from Chinese officials on loosening Covid restrictions, EU and UK share markets are mostly higher while ES futures are showing +0.6% here at 6:45am. Our overnight US rates flows saw a quiet Asian session with real$ buyers in the long-end helping to correct the curve flatter after Friday's sharp reversals steeper. Overnight Treasury volume was ~70% all across the curve.

… The same is true with the Treasury 2s5s curve too where a new move low near -40bp on Friday was swift rejected with Friday's price action also tracing out a well-defined Hammer Bottom (2nd attachment, as highlighted) for this curve too. So we're thinking that both curves are currently suffering from flattening trend exhaustion right now.

… and for some MORE of the news you can use » IGMs Press Picks for today (7 NOV) to help weed thru the noise (some of which can be found over here at Finviz).

In as far as a couple / few OTHER items sitting in the Global Wall St Inbox and which did not appear where the sellside was selling things,

A few weeks ago, I said quantitative easing (QE) changed central bank balance sheets forever. But now, it is worth talking about the reversal—QT—for the Fed, the Bank of England, and the ECB.

… We think the Fed’s QT stays passive, with no active sales. The housing market has already turned down, so selling MBS could be overkill, and calibrating policy with rate hikes is hard enough. Will the Fed call an end to QT when they eventually lower the federal funds rate? In 2019, QT ended when rates were first cut, but because the Fed was already planning to end QT around that time, the timing was a coincidence. While we could see the same coincidence this time, the Fed sees the two policy tools as independent. Our forecast for the first rate cut is in December 2023. Our tentative guess is that QT ends the next year, implying the two tools moving in opposite directions for a time. QT might end early, though, if the economy goes into recession and the Fed is contemplating big rate cuts of 100bps or more. Similarly, if markets were dysfunctional along the lines of March 2020 or the recent episode in the gilt market, we would expect QT to end, at least temporarily.

Same firm and NOT economically speaking but rather, everyone’s favorite stock jockey getting warmed up for the week ahead,

Hanging Around; Consumers Still Spending But Looking for Deals Equity markets remained resilient in the face of a still hawkish Fed and strong labor data. This week presents another challenge with the CPI and mid-terms which could serve as further catalysts for lower interest rate vol and levels, at least at the back end. Stay bullish with tight stops.

… one of the reasons the Equity Risk Premium has defied logic is our view that the equity market is assuming rates will come down meaningfully next year as the Fed finishes its job and recession risk continues to rise into the danger zone (Exhibit 1)

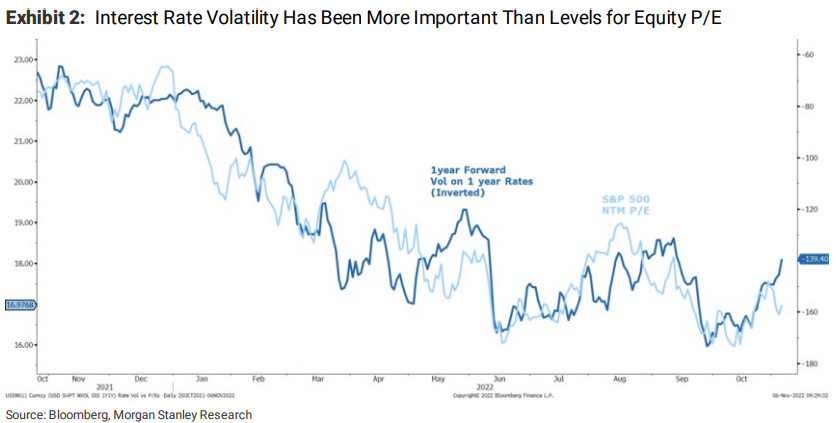

… we know that rate volatility has been closely linked to equity market valuations of late (Exhibit 2).

… we are willing to give a bit more wiggle room to our stop loss level for next week – i.e.,3625-3650 (Exhibit 4) and wouldn't be overly focused on that as much as the rates market.

Instead, if 10-year Treasury yields make a new high (4.35%), the odds of the equity rally trading to higher highs (>3950)goes down considerably, and we would advise clients to consider exiting bullish trades at that point. That doesn't mean we will necessarily plunge to new lows as we still think that will require companies throwing in the towel on 2023 EPS forecasts which isn't likely until 4Q reporting season (Jan/Feb). In short, the bear market rally is likely to hang around for longer than most expect if it can survive this week's test….

Rates matter to stock jockeys … For somewhat more and from a different shop,

U.S. Equity Insights: Pause and Effect The October hope trade was summarily unraveled by the Fed, exposing equities’ all-out focus on the elusive “pause.” Our analysis of prior hiking cycles, recessions and bear markets indicates that the Fed pause has indeed been a reliable buying signal for decades – but this time is different.

From stocks TO elections — which I’m told have consequences — WFC,

The 2022 U.S. Midterm Elections On November 8, millions of Americans will head to the polls to vote for their national, state and local political representation. In this report, we discuss the election and potential implications for our economic forecast.

… One possible election outcome scenario that could shake up the outlook would be if Democrats expanded their majorities in the House and Senate. Big chunks of President Biden's original American Jobs Plan and American Families Plan were left on the cutting room floor due to disagreements within the very small Democratic majority in Congress. More seats in the House and Senate could help revive some of these policies in a reconciliation bill, although this would take time, if it occurred at all. We also believe this election outcome would increase the probability of fiscal stimulus in the event the U.S. economy enters a recession in 2023.

Finally, since on the topic of 2023, here’s a note related TO what MSs stock jockey was keying in on above - consumption from Goldilocks

… Despite these downside risks, we believe that the most significant challenges to consumer spending are in the past and maintain a cautiously optimistic outlook for consumer spending in 2023. However, if strong real income growth leads to a notable acceleration in real spending, the Fed may be forced to hike more than expected, which is one reason why we continue to see the risks to our peak funds rate forecast of 4.75-5% as tilted to the upside.