China’s official mfg PMI jumping TO 52.6 was the highest monthly read in 10yrs clearly helping equities overnight (HSI up OVER 4%) and leaking into this mornings US futures bid … Chinese data visual by Goldilocks,

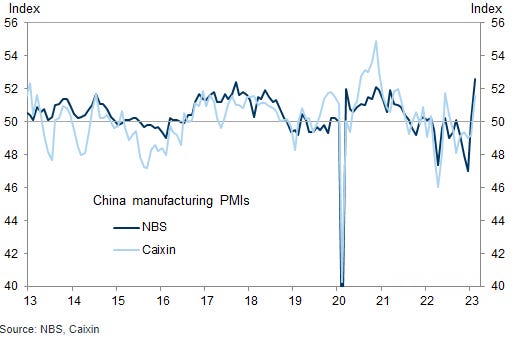

Exhibit 1: NBS manufacturing PMI and Caixin manufacturing PMI rebounded in February

More just below but for now, here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed with the curve slightly flatter. Treasuries were lower earlier (2y yields hit a new move high of 4.855% earlier this morning) after China's robust PMI data but a sharp rally in UK Gilts seems to have dragged prices back toward last night's closing levels. DXY is lower (-0.6%) while front WTI futures are too (-1.0%). Asian stocks were mostly paced higher by China-linked exchanges (Hang Seng +4.2%), EU and UK share markets are all modestly higher while ES futures are showing +0.3% here at 7am. Our overnight US rates flows saw another quiet Asian session despite a sharp rally in Aussie bonds (see links above). We had some real$ buying in the long-end and 2-way action in 10's. During London's AM hours, the desk noted how Treasuries first followed bunds lower and then rallied through most of their morning, following Gilts. We saw better selling in the uptick (mostly 10's) though they added that the demand for front-end paper remains robust. Overnight Treasury volume was decent at ~145% of average overall, led by 2's (207%) and 10's (169%), matching our flows.

… But earlier this morning it was all forgotten as China's sharp manufacturing/services rebound in February (see links above) and a sell-off in Bunds had pushed Treasury 2yrs yields to a fresh move high just above 4.85%. FLASH: after writing that, front-end Gilts have seen a sharp rally (UK 2's -11bp) which have brought 2's back to their closing level yesterday. Anyway, in our first attachment this morning we once again show how we've derived next-support levels (above 4.80% that is) for twos somewhat out of the air: at ~4.99% (January 2007 high) and then more solid near 5 1/8% (2007's high yield print, 2006's monthly closing high).

… and for some MORE of the news you can use » IGMs Press Picks for today (1 MAR— and STILL SPORTING THAT NEW LOOK!!) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

I’ll begin with a review of the month just past …

DB: Feb 2023 Performance Review After a very strong start to the year for financial markets, February saw that go into reverse, with losses across equities, credit, sovereign bonds and commodities. That came amidst growing concern about the persistence of inflation, which in turn led investors to ramp up their expectations for central bank rate hikes. With all said and done, this meant it was an awful month for bonds, with Bloomberg’s global aggregate bond index experiencing its worst February performance since its inception in 1990…

…Which assets saw the biggest losses in February? Sovereign Bonds: The prospect of higher inflation and more rate hikes was bad news for sovereign bonds. US Treasuries (-2.4%) and Euro Sovereigns (-2.3%) gave up most of their January gains, whilst gilts (-3.3%) are now in negative territory on a YTD basis.

… Worst Feb since 1990? With 2yy up nearly 55-60bps on the month, well yeah I guess so. From worst to FIRST … sorta. Chinese data overnight — PMI best in a decade via Goldilocks,

Bottom Line: The NBS manufacturing PMI jumped to 52.6 in February from 50.1 in January, the highest reading since April 2012. The Caixin manufacturing PMI also rose to 51.6 in February from 49.2 in January. The NBS non-manufacturing PMI increased markedly to 56.3 in February from 54.4 in January, driven by an acceleration in both construction and service sectors. Both the NBS and Caixin manufacturing PMIs pointed to improvement in the manufacturing sector in February, as firm operations and customer demand recovered in February after the LNY impact dissipated and the post-Covid recovery gathered steam.

Exhibit 1: NBS manufacturing PMI and Caixin manufacturing PMI rebounded in February

From worst to best and lots in between. More on the WORST (ie BONDS),

LPL: Bonds Are Back… But it May be Bumpy And That is Normal

Bond investors experienced the worst year ever for core bonds last year (as per the Bloomberg Aggregate Bond Index), -so the prospects of another year like 2022 could be hard to fathom. The good news is we don’t think we’ll see another year like 2022 anytime soon, but despite the higher starting yield levels, we could see periods of negative returns. In fact, after a strong January for core bonds, unless yields fall dramatically today, February returns will be negative. But that is normal. Since inception of the index in 1975, over a third of the monthly returns have been negative and close to 25% of quarterly returns have been negative. Bonds trade daily and interest rates change throughout the day as well, so that means the market value of a bond will change daily as well…

… For holding periods as short as five years or as long as ten years, starting yields explain approximately 94% to 95% of returns for the index. That relationship breaks down over shorter periods though with only approximately 40% of 1-year returns explained by starting yields—there is much more variability (noise) over shorter horizons. But if you buy and hold a fixed income investment, the short-term volatility you experience due to changing interest rate expectations is just volatility. It has very little bearing on the actual total return if held to maturity (or if held to the average maturity of a portfolio of bonds).

After the historically awful year for fixed income investors last year, it may be disheartening to see another month (or more) of negative returns. We would advocate for a longer-term perspective though. Current yields within many fixed income markets are at generationally high levels. Investors can take advantage of these high starting yields but only if they stay invested and look past the (normal) short-term volatility that happens on occasion.

And that, they are, as investors continue to pile IN to the front-end of the curve … not sure why but this in and of itself, strikes me as something worth thinking about a bit more as we all know, when everyone stands on the same side of the boat, it normally tips.

For now, sans Terminal, I’m relegated to more topical process of thought as I sift through mountain of ‘research’ and things like this from Invesco,

Invesco Insights: Inflation vs. the economy: Recent reports defy expectations for both

Recent data points suggest US inflation is more persistent than expected. On the other hand, recent reports indicate that the US economy is stronger than many expected. What matters more?

… Conclusion So markets are currently pricing in additional rate hikes and a further tightening of financial conditions, and this could of course lead to a continued near-term retracement of previous gains. However, I don’t expect actual tightening to be dramatically higher than what was expected back in January. Ultimately, I expect inflation to moderate and the Fed to end its tightening cycle, creating an improved backdrop for risk assets.

However, it might be a bumpy road over the next several months before we get there, with more defensive components of the market performing better. But keep in mind that as quickly as sentiment changed over the last several weeks, it can change again. That’s life in a data dependent world. Buckle up and stay diversified.

From theory and ivory tower topical process of thought TO actual (if somewhat delayed) data … TRADE data … because, you know …

As goes global TRADE so goes the <please enter something that sounds snazzy HERE>, an interesting note (visual(s)) from NWM in their updated TRADE TRACKER

Global trade volumes continue to decline with forward-looking indicators signalling ongoing weakness in Q1. World trade volumes contracted further, by -0.9% m/m in December, following a fall of -1.7% in November. Global trade volumes slowed to -2.1% q/q in Q4 (following +1.3% in Q3). Forward-looking survey data suggest global trade will remain in the slow lane in early 2023.

I used to follow this data set more closely and believe it’s widely disseminated on CPB Netherlands site for those may be interested … World Trade Monitor (Dec 2022 is most recent update …)

And from the other day, a note which shouldn’t slip underneath ‘the radar screens’,

JPMs (Kolanovic) View: Fade the bond-equity divergence

… Risk markets are misaligned with policy and cycle. Duration is back to being attractive: The long and variable lags in monetary policy could leave room for some continuation in the uptick in activity data, especially as China reopens and Europe keeps benefitting from lower energy prices, but we remain of the view that the cycle is moving towards the end. Evidence of stronger growth and resilient labor markets have triggered a reassessment in market expectations for G4 central banks. This adjustment has opened up a notable disconnect between OIS markets and risk markets. We are currently slightly OW Bonds, but in our view the recent repricing is opening up opportunities to add further to duration risk.

And finally for those of us who are ‘visual learners’ and enjoy some technicals every now and again, 1stBOS weekly

I have broad shoulders and mediums like this and twitter no place for the weak ... please don't EVER worry about any sorta feedback (its the silence which is deafening!!) ... appreciate your stance. respect ALL decisions -- my opinions are that, not facts just a personal choice., NOT right or wrong. everyone's got a right to a view just not their own set of facts (interesting how NOW it's coming to light about lab leak!) ... DiMartino Booth one of best in the biz. I met her former boss (Dick Fisher) briefly at a conference and really do appreciate how they handle things down there in TX ... and to be honest with you, I'm still learning each / every day. Now my capabilities limited given i've been without a BBG terminal for just over a year now ... lotta great resources out there on the intertubes. keep on keepin on ... again, appreciate any / all feedback. whats that saying -- keep friends close, enemies closer? no, well you know what i mean... stay safe...

I know I gave you shit the other day (I'm an unvaxxed bitter CA state employee waiting to retire or be fired!), but want you to know how impressed w/your knowledge, and ability to crank out a lengthy daily note of this high quality. Can't say I understand ALL of it, but I do believe in learning via repeated exposure, among other methods. I can't thank DiMartina Booth enough for turning me on to your Substack. I'm really learning a LOT (really impressed by that chart of BBB & 3 mo T-bill spread!) and can't thank you enough. Cheers!

I have broad shoulders and mediums like this and twitter no place for the weak ... please don't EVER worry about any sorta feedback (its the silence which is deafening!!) ... appreciate your stance. respect ALL decisions -- my opinions are that, not facts just a personal choice., NOT right or wrong. everyone's got a right to a view just not their own set of facts (interesting how NOW it's coming to light about lab leak!) ... DiMartino Booth one of best in the biz. I met her former boss (Dick Fisher) briefly at a conference and really do appreciate how they handle things down there in TX ... and to be honest with you, I'm still learning each / every day. Now my capabilities limited given i've been without a BBG terminal for just over a year now ... lotta great resources out there on the intertubes. keep on keepin on ... again, appreciate any / all feedback. whats that saying -- keep friends close, enemies closer? no, well you know what i mean... stay safe...

I know I gave you shit the other day (I'm an unvaxxed bitter CA state employee waiting to retire or be fired!), but want you to know how impressed w/your knowledge, and ability to crank out a lengthy daily note of this high quality. Can't say I understand ALL of it, but I do believe in learning via repeated exposure, among other methods. I can't thank DiMartina Booth enough for turning me on to your Substack. I'm really learning a LOT (really impressed by that chart of BBB & 3 mo T-bill spread!) and can't thank you enough. Cheers!