I HOPE you all had a nice Thanksgiving break from this spammation and I am cleaning up the inbox as equity markets are to open for a shortened session AND because I have been up since 330a delivering ‘Thing 1’ TO Penn Station for his 5am trip TO Boston for the BC v Miami game later on today. He’s headed North to watch a friend and former roommate / team mate who now plays for BC.

Speaking of BREAKS…

Reuters: Ceasefire takes hold in Gaza ahead of hostage release, aid enters enclave

HOPE this works out and ALL hostages come home and forgive me if I sound skeptical as negotiating with terrorists NEVER seems to work out as one plans. HOPE may not be a strategy and its usually NEVER ‘different this time’ but …

I’m angling to keep this note short and will begin with a look at long bonds …

… Momentum here remains a BULLISH (lower yield) input and i’ve attempted to highlight what appears to ME to be reasonable targets (resistance) for IF this trade were to continue …

AND as far as some data from Friday Wednesday … helping to drive price action

ZH: 'Unadjusted' Jobless Claims Surged To 4-Month Highs, Led By California ZH: US Durable Goods Orders Plunge In October As War-Spending Sinks ZH: UMich Inflation Expectations Continued Soaring In November

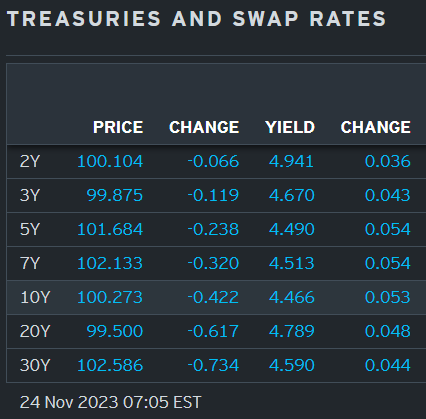

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower with the curve steeper after pretty decent sell-offs in Gilts and Bunds yesterday amid 'overbought' momentum conditions that we chat about below. DXY is lower (-0.25%) while front WTI futures are too (-0.4%). Speaking of Oil and OPEC... it appears that African nations, who want to increase production, may be a reason for the OPEC meeting delay? OED Asian stocks were mixed (China shares lower, most other markets higher), EU and UK share markets are modestly higher overall while ES futures are showing +0.1% here at 7am. Our overnight US rates flows saw a predictably quiet session where Treasury prices languished near their lows with real$ a seller of the long-end (10's and 30's) from the London open. 5yrs have struggled on curve with the Tsy 2s5s10s 'fly almost 2bp higher this morning. Overnight Treasury volume was ~90% of average overall.

We'll pick on Treasury 10yrs again to show how daily momentum (circled, lower panel) has begun to flip bearishly from a deep 'overbought' condition as 10y rates re-test their old bear trendline from below. This overall set-up is certainly a tactically bearish one with 10's deeply overbought near a major resistance level (4.34% area)…

… That said, the medium-term, weekly chart of 10yr Tsys still looks quite bullish in set-up, as you can see.

… and for some MORE of the news you can use » The Morning Hark - 24 Nov 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

During the pandemic, many households refinanced their mortgages at lower interest rates. As a result, 22% of mortgages today have an interest rate below 3%, up from 1% of all mortgages in 2019, see chart below.

The locking in of lower mortgage rates has weakened the transmission mechanism of monetary policy, and it is the reason why Fed hikes have not had a more significant negative impact on the housing market.

The bottom line is that Fed hikes are not having the desired effect because households have locked in low levels of mortgage rates during the pandemic. As a result, the Fed will have to keep interest rates higher for longer to slow down the economy and get inflation back to 2%.

UBS (Donovan): Discounting discounts, and durable deflation

US consumers are gearing up for the most important celebration on the national calendar; Black Friday sales. Increasing consumer awareness of profit-led inflation may shift focus from flashy headline discount numbers to the question “is this price lower than it was a year ago?”. Deflation of durable goods means that for big ticket items the answer is probably “yes”…

With US consumers consuming, the day ahead for markets looks subdued. ECB President Lagarde is speaking, but this is the fourth time in two weeks we have heard from Lagarde. It seems unlikely that she will add anything markets care to hear.

Japan’s October consumer price inflation was slightly lower than expected in spite of fading government support for utility bills. The trend amongst advanced economies is for inflation to surprise slightly to the downside. Japan did not have the profit-led inflation that has plagued Europe, the UK, and the US. Real wage growth remains negative in Japan.

German third-quarter GDP revisions offered no change to the headline, and quite a lot of churning around in the detail. The revisions to these figures are sizable enough that offering authoritative statements on the state of the German economy is difficult.

The unfortunate consequences of prejudice politics were shown in Dublin overnight, with what appears to be anti-immigrant rioting. Fear of economic uncertainty encourages scapegoat economics—it is reassuringly simple to be able to blame a single group for economic woes. The mantra for economic success in the fourth industrial revolution is “right person, right job, right time”; the rise of prejudice makes that impossible to achieve, fuelling further economic uncertainty.

We wish you a great Thanksgiving Day tomorrow with your family and friends. We thank you for your interest in our research service. We are thankful that 2023 has turned out to be a better year than 2022, as we predicted. The S&P 500 is up 18.7% ytd following last year's decline of 19.4%. We will be thankful if 2024 is another good year for the market, as we expect.

Today, the S&P 500 resumed its recent rally that started on October 27. It closed at 4556.62, which is smack dab on the downward resistance line connecting the January 3, 2022 record high and the July 31 high for 2023 so far (chart).

We are expecting an upside breakout above the resistance line as inflation continues to moderate led by falling gasoline prices (chart).

Oil prices fell today suggesting that November will be another month of moderating inflation. The OPEC+ meeting scheduled for November 26 was postponed to November 30, suggesting the cartel is having trouble agreeing on production cuts to stop the slide in oil prices since late September.

Meanwhile, today's report on initial unemployment claims showed a drop of 24,000 to 209,000 for the week ended November 18. The decline more than reversed the jump in the prior week, which had lifted claims to a three-month high (chart). So the labor market remains robust.

Also out today was October's nondefense capital goods orders which has been zigzagging to new record highs all year (chart). It edged down 0.1% m/m in October, which isn't bad considering the depressing impact of the autoworkers' strike.

End Game for Hikes Bonds extended this month’s stunning rally to wipe out losses for most major markets. Investors piled in as softer data spurred bets that the Federal Reserve and its peers would soon be cutting rates, instead of hiking them. Treasuries erased 2023 losses that had hit 3.3% in mid-October. Unlike earlier this month, an auction of longer-dated Treasuries went off smoothly to keep investors confident that the worst is behind bonds after two and a half very tough years. Japan’s longer-dated sale also proved popular.

Some of the biggest fund managers out there — DoubleLine Capital, Pimco and TCW Group — were emboldened to urge investors to stop squirreling away so much money in cash and start putting it into bonds. There’s also a darker side to all this — the FOMO vibe around bonds is built on strong expectations that the US economy is in for a hard landing. That message was underscored when the term premium, a gauge that measures how strong demand is for longer-dated debt, turned negative once more. That only makes sense if you think a recession is baked in.

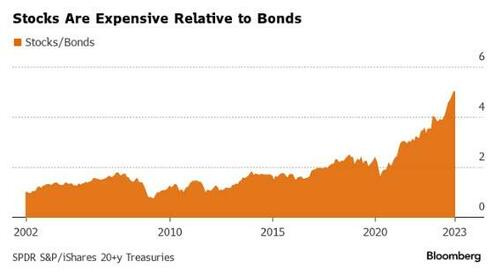

Bloomberg: Investors Have Never Been This Optimistic About Stocks Relative To Bonds

Never before have investors been this optimistic about stocks relative to bonds, a phenomenon that may have room to run before being upended by an economic downturn.

The net asset value per unit of the SPDR S&P 500 exchange-traded fund was $454.26 on Monday, more than five times that of iShares Treasury bond fund comprising residual maturities longer than 20 years.

That is the most elevated in their contiguous history spanning two decades.

The ratio has doubled since the end of the 2019, just before the pandemic struck, with the Federal Reserve’s 525 basis points of policy tightening since then wreaking havoc with bond valuations even as stocks have shrugged off the onslaught.

As of Monday’s close, the S&P 500 offered investors an earnings yield of just 19 basis points over 10-year Treasuries. That premium was negative as recently as last month, the lowest since 2002.

The melt-up in stocks is testament to their shrinking empirical durations in the current Fed tightening cycle. A few months into the cycle, stocks had demonstrated an empirical duration of 7.1 years, though the recent rally brought the S&P 500’s gain since the Fed started tightening to more than 6%. That means stocks have done enough to boast a negative duration — an asset that increases in value when interest rates rise.

Bonds, on the other hand, have copped it through this cycle. The Bloomberg Treasury total return index has incurred losses of about 9% since the Fed started raising rates.

Despite the recent rally in bonds, the outlook is still murky, with a host of factors weighing on sentiment: estimates that the neutral rate has risen considerably, a labor market where aggregate supply isn’t quite aligned with demand yet, and a disinflationary process that has further to run.

Interest-rate traders are betting that the Fed will start loosening policy around the middle of next year, but the resilience of the US economy has so far wrong-footed investors who have underpriced the policy trajectory through much of this cycle. Those factors explain why two-year Treasury yields have surged more than 100 basis points since the middle of the year to still hover around 5%.

While a chase for duration may have looked legitimate this late in the Fed’s tightening cycle, a surge in real yields has come back to haunt both 10- and 30-year bonds. Should that narrative continue to bedevil the markets, sentiment toward longer-dated maturities may stay subdued.

A turning point in investors’ attitude toward bonds relative to stocks will occur when we see an inflection point in the US economy. However, with the jobless rate still below 4%, a rebalancing of the economy is still not in sight, which may preserve the skew between the two asset classes.

KIMBLE: Are Technology Stocks Ready To Lead the Next Bull Market? (as goes tech so goes long bonds?)

StockCharts.com: The Stock Market In 3 Charts: Market Breadth, Bonds, Sentiment

… The Bond Market

The 10-year US Treasury Yield Index ($TNX) fell to its 100-day simple moving average (SMA), which is acting as a support level. The yield bounced off the SMA and closed at 4.42% (see chart below). Lower yields tend to be good for stocks.

CHART 2: 10-YEAR US TREASURY YIELD INDEX. The 100-day simple moving average could be a support level to watch.Chart source: StockCharts.com. For educational purposes.

Treasury yields move inversely to bond prices, so it's not surprising to see that the iShares 20+ Year Treasury Bond ETF (TLT) has been moving higher. If you've pulled out all your fixed-income investments, now may be time to start thinking about getting back in. But there's no need to rush, since TLT is still a long way for TLT to reach its yearly highs of around $106.

ZH: For The First Time Since The Covid Crisis, There Are More Global Rate Cuts Than Hikes

330am. Damn. You're a great dad. I wouldn't told him to get a Uber 🤣

Will read soon...

Want to post these two items: Zero Hedge and Danielle DiMartinoBooth

https://gettr.com/post/p2v77ew9c8b

https://youtu.be/eUoJQTDSrA8?si=SBrM7XB81rLS3bf9