(USTs lower, flatter on light volumes)while WE slept; "The Great US Treasury Bond Rout Is Far From Over" (10yy going TO 4.50%, Dudley), "Rate Hikes Will Continue Until Morale Deteriorates" ...

With THAT in mind, and month / QTR END (demand) just ahead, a look further OUT the yield curve …

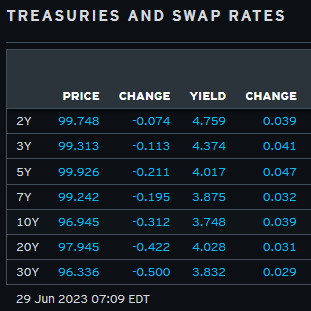

For more on DUDs 4.50%, continue scrolling down but for now … here is a snapshot OF USTs as of 709a:

… HERE is what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower with the curve generally flatter as Tsy 5yrs vacillate around 4% amid a thin news morning (German state inflation is coming firmer than expected- see link above about base effects from transit prices there). DXY is unchanged while front WTI futures are modestly higher (+0.5%). Asian stocks were mixed, UK and EU share markets are mostly higher (SX5E +0.55%) while ES futures are showing +0.3% here at a tardy 7:20am. Our overnight US rates flows saw a 'noisy' Asian session with a dip during their hours bought in intermediates. In London hours, real$ bought the 5bp cheapening in 10's during Asian hours in what the desk suspects might be partly month-end-related flow. Overnight Treasury volume was modest at ~80% of average overall...

… Our last attachment this morning looks at the updated MOF net foreign bond buying out of Japan. Japan looks like they were a decent buyer of foreign bonds into the recent back-up in rates but during the latest week those outflows appear to have cooled...

… and for some MORE of the news you can use » IGMs Press Picks for today (29 JUNE) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

Before I begin with I can’t help but share in my complete surprise when late yesterday afternoon, we all learned,

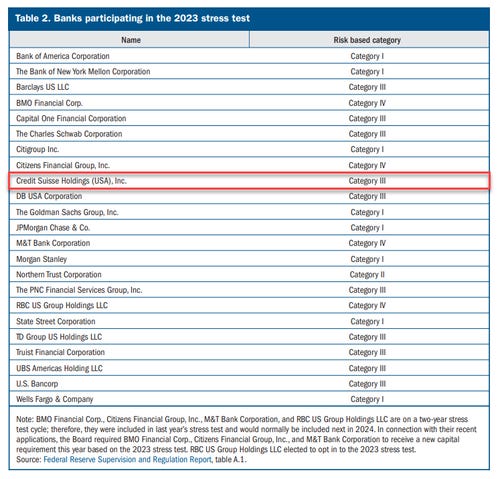

ZH: Surprise! Fed Says All Big Banks Passed 'Stress Tests', Face $541 Billion Losses In 'Adverse' Scenario

… In late breaking news that will shock absolutely no one, The Fed reports that the 23 largest

US

banks passed their annual stress tests.

Including Credit Suisse...

Read ALL the snark you’d like and then PAUSE before celebrating like the NYY last night

HOW can the Feds stress tests have credibility after CSFB passing? Clearly NOT a bank analyst here and so, jumping in TO the inbox, you’ll find actual serious ‘analysis’ like this one,

New Stressed Capital Buffers (SCBs) suggest higher required capital ratios at COF, CFG, TFC, C. Lower at JPM, BAC, GS, MTB, PNC, WFC. All banks have sufficient capital in our models under the new reg mins. No change to EPS, as tougher Basel III Endgame rules are up next…

… Multiple scenarios coming next year. This year included a non-binding alternative scenario for the GSIBs. The Fed noted that the trial provided further evidence that the use of more than one scenario can expand the Federal Reserve’s view of risk exposures. We believe this means we will likely get multiple scenarios for all banks in next year's test.

What's next? Post market close on Friday June 30, expect banks to disclose one or more of the following: announcement of the actual SCBs which could be marginally different than our estimates (+/-20bps), dividend hikes and potentially revised board share repurchase authorizations, if last year’s pattern holds.

Exhibit 1: MTM of securities book (OCI) benefitted capital ratios more than the tougher test hit earnings at Category I and II banks

Ok, putting banking aside for now, a few OTHER items from the inbox. A large French bank on longer-term yields — worth a look in light of yesterday’s 7yy auction and ahead of month and QUARTER end …

BNP US rates: A lasting reset in longer-term yields

We see factors supporting higher intermediate and longer-term forward US yields.

These risks leave us cautious on adding duration longs despite cyclical considerations that would seem to support doing so.

Risk/reward favors hedging upside to forward yields, in our view. We prefer to do so via a 1y5y5y midcurve payer butterfly.

In US Rates: Forecast reassessment (5 June), we raised our targets for UST yields across the curve. A resilient labor market and a sustained period of elevated short rates can drive further yield upside in our view.

On anchors and averages: We previously highlighted two factors that have helped explain the behavior of intermediate forward rates:

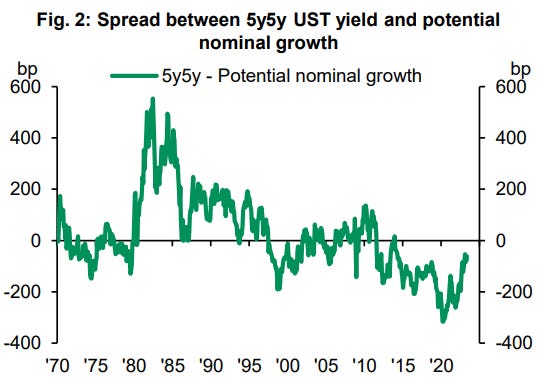

Potential nominal growth (for which we use the sum of the Congressional Budget Office’s real potential growth and the 10y CPI inflation expectations from the Survey of Professional Forecasters) appears to have provided a reasonable anchor level around which 5y5y rates have oscillated. Meanwhile, periods where the trailing average of short term rates have meaningfully exceeded or persistently undershot longer term rates have tended to see 5y5y rates dragged along (Figure 1).

In this note, we focus on the difference between the 5y5y UST yield and potential nominal growth (Figure 2). This spread can be thought of as a risk premium of sorts, albeit one where the “expectations” component relies on economic projections alone (rather than incorporating term structure or forecast-based estimates)

… Domestic and global duration demand The availability of and demand for duration supply are also relevant factors for driving the level of yields. There are domestic and global dimensions to these considerations…

… Overseas vs. US growth expectations: Finally, we consider the global backdrop, using the relative level of global versus US rates as a proxy.

Since the 1980s, it has been relatively rare for the average of German, UK, and Japan yields to trade meaningfully above US yields. Periods where foreign yields have set at a significant discount to US 10s tend to see forwards in the US priced at a deeper discount to potential nominal growth (Figure 8).

This is admittedly a simplistic measure, as it doesn’t capture potential considerations (such as FX-hedging costs) that may influence the spillover from foreign demand onto US duration.

Still, when we consider the recent experience with negative interest rate policy outside the US, for example, that rate regime likely incentivized foreign investors to allocate substantially more towards US rates than they would have otherwise.

Though US yields are still comparatively higher, we think the shift in the eurozone yield environment diminishes the incentive for European investors to go overseas (see Global flows 2.0: Part I, 22 May). On top of that, the potential widening of the Bank of Japan’s YCC band to +/-100bp—something we expect at the July meeting— can help to support further repatriation by Japanese longend investors. On balance, these flow dynamics suggest to us that the foreign yield picture should wane as an anchor onto US yields, even if there isn’t full convergence of yields abroad.

From global growth and DURATION DEMAND, this same outlet discussing central planners and looks towards the stars, '

The resilience of global growth over recent quarters despite the magnitude and synchronisation of policy tightening by major central banks bolsters our conviction that neutral interest rates have moved higher than in the past decade.

That said, signs of deteriorating economic activity, slowing inflation and recent turbulence in the banking sector likely signal that policy rates are now in clearly restrictive territory.

While we are sceptical that banking-sector issues mean policy rates have hit a so-called financial stability real rate, risks of over-tightening have become more prominent and central banks are likely to remain cautious.

The key implication of a higher r-star is to limit the scope to cut interest rates without excessively stimulating the economy, while policy rates are likely to stabilise at considerably higher levels than in the past decade.

…R-star 101 Stars are aligned: The equilibrium interest rate, also known as the neutral rate, the natural rate and (in more academic settings) r-star or r*, is the short-term interest rate that would prevail if the economy is operating in equilibrium – i.e. with inflation at target and the gap between actual and potential output equal to zero.

The equilibrium rate is typically referred to in ‘real’ terms – in other words, with inflation removed. Adding the inflation target (i.e. 2% in most cases) back on to the estimate of the real rate would give an estimate of the neutral ‘nominal’ rate, which would be the relevant guide for the policy rate…

From one esoteric concept TO a shop soon to be an esoteric memory,

CSFB: Global Economy Notes: Tighter policy, slower growth in 2H

We maintain our forecast for global growth momentum to slow in the second half of the year.

Global industrial production momentum appears to have peaked in May and should drop to close to nil by 4Q. If this comes with the slowing inflation we forecast, it may increasingly challenge risk appetite and benefit government bond yields.

The Fed, ECB, and BoE have signaled further hikes in the coming months. The now more aggressive stances of the ECB and the BoE are closing the gap with the Fed and making policy tightening more coordinated globally. The risk of overtightening is increasing.

In the US, we expect weaker employment and wage growth to increasingly curtail consumption growth as well as rein in the recent bounce in housing. Fed tightening, Treasury rebuilding of the TGA, and stagnant credit should swing broad liquidity from excessive to tight by 4Q.

… The Fed still seems likely to hike 25bps in July Some of these disinflationary forces should appear in July data, but probably not to the extent that they stop the Fed from raising the Fed Funds rate another 25bps to 5.25-5.50% at its July 26 meeting. What will be key will be whether disinflation is sufficiently advanced by September to prevent another hike to 5.50-5.75% that would increase the likelihood of recession.

In any event, we expect disinflation to be sufficiently advanced by year-end to create room for the Fed to begin cutting rates early next year, if not possibly in December if necessary.

Less positively for risk assets, the combination of falling inflation and slowing real growth implies slower nominal GDP growth. We expect nominal GDP growth to fall from 7% in 1Q to about 3% or less in 4Q. Figure 19 shows this implies a significant further fall in corporate margins. This drop in margins is likely to come with weakening volume growth and higher financing costs.

Additionally, what has been an economy with excess liquidity is likely to become increasingly liquidity tight. Broad money supply M2 to nominal GDP should swing from pandemic-era excess to below-trend levels by 4Q, largely because of the contraction in money supply. (See Figure 20.) Bank reserves and M2 are already falling. Fed quantitative tightening, Treasury rebuilding of the TGA account at the Fed, and tighter credit standards are likely to lead to reserves, bank credit, and broad money to contract in the coming quarters.

Inventory correction has put euro area manufacturing into recession, but rising real income growth should allow services to keep overall economic growth at a run rate of 0.5-1.0%. Yet, increased ECB hawkishness and potential spillovers from slower US activity imply downside risks to growth.

We continue to forecast below-consensus Chinese GDP growth of 5.2%. Policy appears unlikely to target a large acceleration in Chinese growth that works to offset developed market weakness.

The question of when the Bank of Japan will finally begin tightening remains open, but risks now appear to be for later rather than sooner.

So, as some who passed the stress tests believe a 25bps hike coming in July, a former Fed insider translates what any / all this MAY mean for the bond market.

Bill Dudley BBG OpED: The Great US Treasury Bond Rout Is Far From Over Rising yields and falling prices will wreak more havoc — and perhaps refocus attention on the government’s troubling fiscal trajectory. June 29, 2023 at 6:00 AM EDT

Yields on long-term US Treasury securities have risen, and prices have fallen, farther and faster over the past few years than at any time since the 1980s. This has wreaked no small amount of havoc — contributing, for example, to the recent demise of several regional banks.

I have what might be disconcerting news: It’s not over.

Since last fall, the 10-year Treasury yield has remained in a narrow range near its current level of 3.75%. There’s little reason for it to stay there, and many reasons to expect it to move considerably higher.

First, with the economy still strong, the labor market extraordinarily tight and inflation stubbornly high, the Federal Reserve will probably be taking short-term interest rates higher for longer. In their most recent projections, two thirds of officials on the policy-making Federal Open Market Committee saw at least two more 0.25-percentage-point increases this year, while the median forecast was for the federal funds rate to remain above 4% at the end of 2024. They also appear to be increasing their estimate of the “neutral” rate that neither restrains nor boosts the economy, suggesting that a higher fed funds rate will be required to combat any given level of inflation. This makes sense: With baby boomers spending down retirement accounts, the government running large budget deficits and vast capital investments required in supply chains and green technology, higher rates will be necessary to balance demand for borrowing with a shrinking supply of savings.

Second, over time, average inflation — a key component of bond yields — will almost certainly be higher than the Fed’s 2% target. The central bank’s monetary policy framework is asymmetric. When inflation is too low, it wants to compensate by aiming above 2%, lest inflation expectations decline and erode its ability to stimulate growth (if, for example, inflation expectations fell to zero, taking interest rates to the zero lower bound would have little stimulative effect). But when inflation is too high, Fed policymakers merely aim to get back to the 2% target. Over time, the result should be more upside than downside misses.

Third, the bond risk premium — the added yield the government pays over expected future short-term rates — is likely to move higher. For one, investors will demand more compensation for uncertainty about future inflation. Also, given the dim prospects for any political agreement to get the US government’s unsustainable budget deficits under control, the Treasury will be issuing vast amounts of debt — at a time when the Fed will be reducing its Treasury holdings by $60 billion a month, and when international sanctions have led some central banks (notably China and Russia) to reduce their appetite for US Treasury securities.

How high, then, might Treasury yields go? Let’s put together the pieces. Suppose the Fed’s short-term interest-rate target, adjusted for inflation, averages about 1% over the next decade. Inflation averages 2.5%, and the bond risk premium is one percentage point. In sum, this suggests a 10-year Treasury note yield of 4.5%. And that’s a conservative estimate: Given historical neutral short-term rates, the recent persistence of inflation and the troubling US fiscal trajectory, all three elements could easily go higher.

To some extent, this is what the Fed needs to happen, to slow the economy and get inflation under control. That said, it’s been so long since long-term rates have reached such heights that further havoc is all but guaranteed. There’s just one possible silver lining: With any luck, a reawakened bond market might force US politicians to finally get the country’s fiscal house in order. The sooner the better.

With these sage words of wisdom and local recon in mind,

… Look out if you thought central banks were done tightening the screws! That’s the message broadcast loud and clear from the Portuguese town of Sintra. Policymakers sound frustrated that their economies are far too sluggish to respond to the steep interest-rate hikes imposed over the past year or more, and their limited toolbox means they’re ready to take borrowing costs higher, even as concerns fester that the outcome will be a series of recessions.

Federal Reserve Chair Jerome Powell and his peers (excluding Japan’s Kazuo Ueda) said they have a ways to go. They’re also likely to keep rates high for longer. Sticky inflation is a key dynamic here, but so is the resilience of their economies. While supply shocks continue to play a part in cost pressures, central banks have made it clear they have to focus on reducing aggregate demand via rate hikes. Looking at global expectations for activity among purchasing managers, we can see those climbed back to levels signaling expansion this year, despite all the central bank moves. That helps explain both sticky inflation and central bankers’ willingness to keep using that sole tool by raising borrowing costs.

Finally, in the DONT WORRY BE HAPPY camp, a few words on M2 from Calafia Beach

… Chart #3 compares the growth of M2 with the rate of CPI inflation lagged by one year. The chart suggests that there is approximately a one-year lag between changes in money supply growth and changes in inflation. Given the dramatic decline in M2 growth which began early last year, the chart suggests we will see a similar decline in inflation over the next 6 months or so. As I've argued for months, the decline in inflation is well underway.

… For the past 18 months the Fed has been raising short-term interest rates in an attempt to bolster the demand for money. If they hadn't done that, plunging money demand would have pushed prices even higher. In effect, they were trying to prevent the public from rapidly spending all the excess money that accumulated in the 2020-2021 period. And it has worked. The May pickup in M2 suggests there has indeed been a slowing in the decline in money demand.

Chart #5 shows nominal and real yields on 5-yr Treasuries (red and blue lines), and the difference between the two (green line), which is effectively the market's expectation for what the CPI will average over the next 5 years. Inflation expectations today are about 2.1%, which is very close to what inflation averaged in the 20 years leading up to the 2020 Covid crisis. In effect, the bond market believes the inflation problem has been solved. The yield curve is very inverted these days (i.e., short-term rates are much higher than long-term rates), which means that the bond market expects the Fed to lower short-term interest rates dramatically over the next year or two—because the market believes the Fed will eventually realize that the inflation problem has been solved…

… Summary: There is nothing to fear from the behavior of M2; money and liquidity are still abundant and key indicators such as swap and credit spreads tell us that the economy's fundamentals are still sound. The source of our inflation problem has dried up and inflation is on its way back to normal. The Fed was slow to react to all this, but they have not yet made a significant mistake. It's therefore not surprising that the stock market has been creeping higher.

LOL as if 15 yrs of ZIRP & MMT-QE weren't MISTAKES! Didn't the recently imploded banks also pass their "Stress Test"? When I hear, "the big banks all passed their stress tests...yada yada" I thinks, "be warry of the next bank IMPLOSION". Today's dish was mucho-extra SPICY thanks!

LOL as if 15 yrs of ZIRP & MMT-QE weren't MISTAKES! Didn't the recently imploded banks also pass their "Stress Test"? When I hear, "the big banks all passed their stress tests...yada yada" I thinks, "be warry of the next bank IMPLOSION". Today's dish was mucho-extra SPICY thanks!