(USTs lower, flatter on light volumes) while WE slept; YELLEN>JPOW; everyone agrees - the curve has now bottomed - let the cyclical steepening commence ... someone inform 3m vs 18mo fwd 3m bill crv

Good morning … due to travel schedule and having been mostly off the grid yesterday, this mornings update will be topical and sans opinion of my own. I do find it interesting waking up to news that SNB jacked rates — CNBC,

Besides all that — water under the bridge — it would seem to ME that JPOW and the Hobbit crossed their signals in as far as WHO was supposed to be making the news?

*POWELL: HARD TO SEE HOW BANK CRISIS HELPED SOFT-LANDING CHANCE

Rate CUT folks back to work pricing OUT Fed and so, a steeper curve it IS! Now then over to the Hobbit … ZH:

ZH then fleshes out Bill Ackman commentary who’s tweeting what everyone was thinking,

Yesterday, @SecYellen made reassuring comments that led the market and depositors to believe that all deposits were now implicitly guaranteed. That coupled with a leak suggesting that @USTreasury, @FDICgov and @SecYellen were looking for a way to guarantee all deposits reassured the banking sector and depositors.

This afternoon, @SecYellen walked back yesterday’s implicit support for small banks and depositors, while making it explicit that systemwide deposit guarantees were not being considered.

We have gone from implicit support for depositors to @SecYellen explicit statement today that no guarantee is being considered with rates now being raised to 5%.

5% is a threshold that makes bank deposits that much less attractive. I would be surprised if deposit outflows don’t accelerate effective immediately.

A temporary systemwide deposit guarantee is needed to stop the bleeding.

The longer the uncertainty continues, the more permanent the damage is to the smaller banks, and the more difficult it will be to bring their customers back.

AND ZH goes on all well worth time / point / click IF you (like ME) missed the markets food fight in / around the time both were speaking. For more on (if its) YELLEN (you must be SELLIN) comments, RTRS

“I have not considered or discussed anything having to do with blanket insurance or guarantees of deposits”… When a bank failure “is deemed to create systemic risk, which I think of as the risk of a contagious bank run…we are likely to invoke the systemic risk exception, which permits the FDIC to protect all depositors, and that would be a case-by-case determination.”… “To the best of my knowledge, we’ve never seen deposits flee at the pace that they did from Silicon Valley Bank”.

IF you were looking for a sellside I TOLD YA SO, ZH,

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower with the curve little changed as Treasuries underperform the UK and EU peer markets after a brace of central banks (see above) followed the Fed by hiking rates overnight. DXY is little changed while front WTI futures are lower (-0.65%). Asian stocks were mixed, EU and UK share markets are lower while ES futures are showing +0.55% here at 7:15am. Our overnight US rates flows saw a muted Asian session with curve steepening a feature (2s10s from -51 to -42.5bp before retracing some) during their hours. During London's AM hours we saw better net selling (mostly fast$ by the sound of it). Overnight Treasury volume was ~70% of average overall.

… After yesterday's 25bp hike, Powell's preferred 'recession curve,' the 3mo Bill versus 18mo forward 3mo bill rate, banged out a new century low- more inverted now than at the prior cycle low seen in 2000- which was just weeks before an official NBER recession began.

… and for some MORE of the news you can use over here at Finviz …

From some of the news to some VIEWS you might be able to use. Global Wall St SAYIN’ AND SELLIN’

MS on the moment having arrived,

FOMC Reaction: Inertia Amid Uncertainty The FOMC delivered a 25bp rate hike and we continue to expect a final 25bp hike at the May meeting. The Fed remains hyper-focused on inflation and maintained its "high for longer" rates message. Our strategists add 2s30s and 5s30s steepeners, and long SFRU3.

Key Takeaways

In line with our expectation, the FOMC hiked the policy rate 25bp to a range of 4.75-5.00%, acknowledged it is monitoring incoming information "closely", and believes further tightening "may" be appropriate. Also, there were no changes to the balance sheet program, nor was the possibility of a change even "discussed yet". Rate cuts are not in the FOMC "base case" and indeed the Committee sees half a cut less in 2024 compared with the December projection – a sign that the Fed "remains highly attentive to inflation risks."

There were competing dovish and hawkish elements throughout the statement and press conference, likely a reflection of considerable uncertainty around the effects of tighter credit conditions on the outlook for the economy and monetary policy. Weekly data on loan growth as well as deposit flows will be key in the weeks ahead.

We continue to expect a final 25bp hike at the May meeting, driven by another strong payroll print and sticky inflation. Needless to say, a surge in bank funding pressures could alter that view.

Our rates strategists think the FOMC meeting will keep momentum towards lower yields. Just like the Fed, the market will focus on banking system stresses and credit tightening for now, while inflation risks will continue to be a medium-term concern. They suggest a long duration bias expressed via 2s30s and 5s30s curve steepeners (or TY/WN steepeners). They also add long outright SFRU3….

THEY (MS) are not alone as a large German institution also offered,

The FOMC meeting and market reaction supported our recently entered 2s10s steepener. The Chair emphasized that recent turmoil is likely to tighten credit conditions and limit Fed hikes, the forward guidance was revised as we expected, and comments from the Chair (and Secretary Yellen) reinforced our view that a blanket bank deposit guarantee won't come preemptively. All told our conviction in the trade has steepened.

HEREis the note where they told us ‘bout steepeners (BEFORE FOMC).

This same operation but different desk stratEgerist … one of the fan favs (Ruskin) ‘splains,

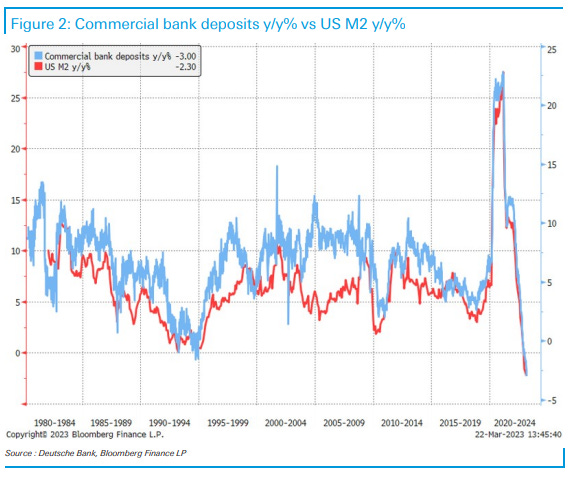

This piece looks at how two favorite leading indicators, the yield curve and money supply are deeply interconnected in a causal way, and at the nexus of current US banking sector tensions. The US is at the very bottom of a global ranking of wider M2 growth rates when compared to 40 countries (see Figure 7), which is consistent with the US being at the epicenter of this bank liabilities storm. The discussion is neither good for relative US risk, or the USD, with the EUR/USD bellwether (see Figure 3), tracking the relative performance of EUR vs US bank indices.

… As Figure 1 and 2 show, the fall in commercial bank deposits that make up the preponderance of M2 is unprecedented.

… Fortunately for now, the US deposit flows are said by Powell to have stabilized, but whether the distributional flows within the sector can be reversed is altogether another story. US bank deposit stabilization would probably encourage the market to think in terms of a worst case credit crunch, rather than a crisis. Much as there is little from the above that is good for relative US risk, it is also negative for the USD and it is not surprising to see EUR/USD tracking the relative performance of EUR vs US bank indices as per Figure 3…

AND there you have it … ‘fortunately for now’, deposit flows are said to have stabilised. Feelin’ better?

The memo has gone out and one SHOULD at least IF your biggest fear was further hikes (where my 6% terminal folks at again — are they now TRANSITORY cuz something broke?). A group from BBG who now represent a large FRENCH operation,

US March FOMC: Fed backs down as banks step up—one (more) and done?

Key Messages The most uncertain Fed rate decision in recent memory concluded with the FOMC hiking by 25bp and the official communique suggesting “some additional policy firming may be appropriate”.

Chair Powell expressed confidence in the overall health of the banking sector, but also repeatedly stressed that tighter credit conditions could do some of the Fed’s work—in his view, possibly the equivalent of 25-50bp.

Powell cautioned that it was too soon to understand the net impact of banking sector strains, but we agree with his general assessment that the Fed will likely need to “do less”. Therefore, we are putting our prior forecast for the terminal funds rate (of 5.75%)—which was established before the collapse of Silicon Valley Bank—under review.

In the nearer term, we think still-too-hot macro conditions and some encouraging signs that policymakers’ actions have alleviated acute stress among smaller regional banks could pave the way for additional Fed tightening. As such, from the current vantage point we think the Fed will raise rates by an additional 25bp on 3 May—but we stress that this is a low-conviction call which is highly sensitive to the evolution of financial and credit conditions in the interim.

Forgive me for bouncing all over the place and as I go from the ‘ivory tower’ folks TO one of the best desk strategists out there … an afternoon note,

* FOMC hiked 25 bp and the biggest takeaway from the statement was the shift away from “ongoing increases” to the policy rate to “some additional firming” as well as saying that the “U.S. banking system is sound and resilient.”

* Powell said “it’s still too early to tell how stress in the banking section will affect credit conditions,” and that if stress in the banking sector has a larger impact, then “monetary policy will have less to do.”

… The front-end of the US rates complex rallied >20 bp as 2-year yields declined as far as 3.91%. 10s rallied as well; although to a lesser extent reaching 3.453% intraday. Assuming this is the beginning of the Fed pivot, it will also mark the commencement of the cyclical resteepening of yield curve. 2s/10s at -50 bp might be a near-term equilibrium but we’re maintaining an initial target of -29 bp as the market adjusts to the new realities of the Powell’s stance. In the event the pendulum swings toward deeper inversion, -60 bp represents meaningful support. The benchmark 2s/10s curve has begun its climb back into positive territory. 5s/30s is leading the charge of curve normalization, reaching +15.5 bp after printing at -5.1 bp ahead of the meeting. From current levels, we’re targeting +24.7 bp as the first level at which we’d look to book profits with a nod to the potential for a >100 bp 5s/30s curve as investors make the logical transition from pricing in the end of the hiking cycle to a more dramatic cutting cycle in the years (if not quarters) to come…

From ivory tower views to narratives (following price action) I’ll end with some CHARTS as prices never lie (he says with very little conviction) … here are some weekly MULTI ASSET charts and themes from a large Swiss shop under pressure,

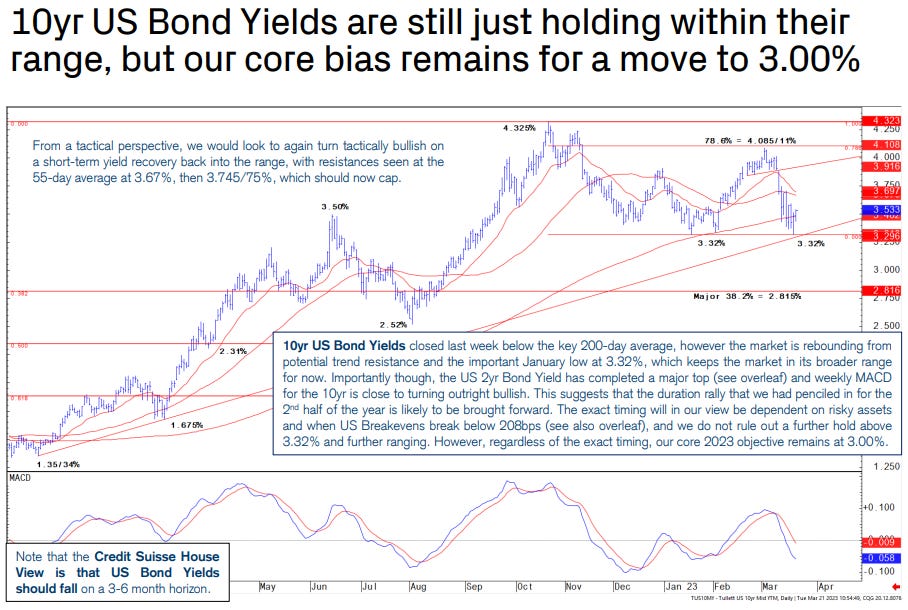

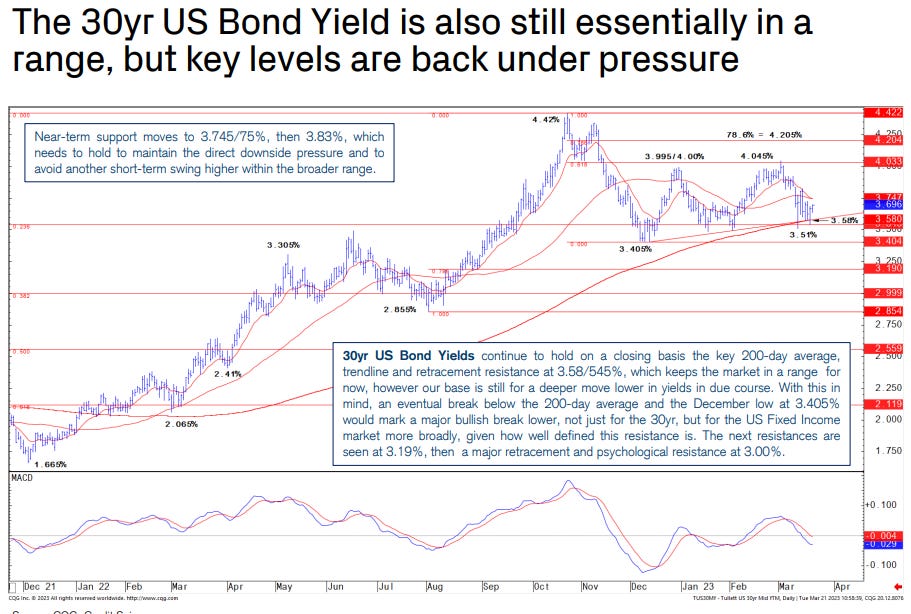

Government Bond Yields fell sharply last week as further signs of stress emerged in the global banking system, reinforcing our strategically bullish view on US Fixed Income for 2023. The US 2yr Bond Yield has now completed a major technical top in our view, which suggests a deeper fall in yields in due course to 3.175%. This is also seen likely to accelerate the move in the US 10yr Bond Yield to our core 3.00% 2023 objective although we may see the January low at 3.32% continue to hold on the near-term.

* Our bias for a fall in the US 2yr Bond Yield could trigger a deeper bull steepening phase in the US 2s10s Bond Curve, which historically tends to be bad for risky-assets…

I'd say she's more of a Smegal IMHO!

(i'd have to agree)