ZH: Ugly, Tailing 7Y Auction Prints At Highest Yield On Record

#Got6moTBILLS?

Up 50bps on the year so why NOT just PARK IT and wait? (one reason perhaps NOT so evident as the page in the calendar turned TO 2023 was looming game of debt ceiling chicken) … here is a snapshot OF USTs as of 707a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly lower with the belly slightly underperforming after Japan's CPI made a fresh 41-year high while German and UK consumer confidence (GfK) scored upside beats. DXY is modestly higher (+0.17%) while front WTI futures are modestly higher too (+0.4%). Asian stocks were mixed, EU and Uk share markets are mixed this morning too while ES futures are showing -0.6% here at 6:40am. Our overnight US rates flows saw reports of some apparent futures block sales in TU's (2.57k) and FV's (8.04k) but we were too early for cash desk color. Overnight Treasury volume was about average overall with Japan back with 7's (195%) seeing some relatively high average turnover after yesterday's auction.

…Shifting out the curve, the daily chart of Treasury 30yrs is updated and it shows an elevated risk of a new, short-term momentum Buy signal being confirmed today with bonds continuing to hold support near 3.985%- a support level derived by their turn-of-year move high. Indeed, that last time bonds tried to press toward 4% we also had daily momentum at similarly 'oversold' levels before 30yr yields corrected almost exactly -50bp lower in the few weeks that followed. However, the difference today versus the start of the year is that weekly momentum was still guiding lower back then while today it guides bearishly. So -50bp might be a stretch and maybe today's short-term 'oversold' condition is partly relieved by a sideways chop around current levels??

Our next attachment looks at the daily chart of TLT's and it did show a close-confirmed daily momentum Buy signal yesterday (lower panel, circled). So back-end yields appear to be in a roundabout right now, wondering which exit to take...

Our next two attachments are Japan-related given the news this morning. First we show the full Bloomberg time series of Japan's CPI ex-fresh food an energy, YoY%. Ueda-san waxed confidently this morning that inflation would return to target but charts/trends like this must make him sweat a bit?

And our second Japan-related attachment looks at the latest MOF net foreign bond flow data which showed a huge/historic spike in net foreign bond purchases in the latest week. Note too that the 4-week moving average of Japan's net purchases is now back near 2021's multi-year high. Maybe 5%-handle front-end US paper are catnip for them too??

… and for some MORE of the news you can use » IGMs Press Picks for today (24 FEB— and STILL SPORTING THAT NEW LOOK!!) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

Upside surprises to activity data have reversed the rally in rates markets, with inflation fixings re-pricing higher.

Despite the rates market re-pricing being the consequence of better activity data, higher-beta assets have corrected lower, especially in FX.

US and core EUR yields are near our Q1 2023 forecasted peak. However, we are cautious about buying too soon.

The USD will be supported while Fed expectations adjust higher. But reduced recession risks make the eventual case for USD weakness compelling.

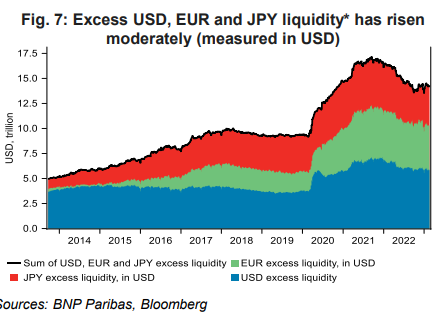

Increased excess liquidity in Japan has offset declines in the US and Europe, resulting in rising excess liquidity (in sum) in 2023. This is likely not a sustainable source of support to the everything rally.

… What about liquidity? One pushback we received to our 20 January note was that the everything rally was being driven by an expansion in liquidity.

USD liquidity has been contracting (at a slow pace), although there may be some expectations for an increase if the TGA is further drawn down.

When we sum excess liquidity* across Europe, Japan and the US (in USDs), we observe an increase in 2023 (Fig. 7). The increase is primarily driven by Japan. Part of the increase, in USDs, reflects USDJPY declining. However, in local currency, excess liquidity in Japan has started to increase since the middle of December 2023.

Furthermore, we note in the weekly flow data, around a similar time, Japanese investors have been buying foreign assets (both bonds and equities), contrasting with the 2022 trend (Fig. 8).

Looking ahead, given our expectation for a further widening in the BoJ’s Yield Curve Control band, it seems highly unlikely that Japan can be a source of increased excess liquidity to such an extent that it offsets the trend declines likely to be seen in the US and Europe over time.

Therefore, we judge that to the extent the everything rally was partly a function of improving liquidity, this is unsustainable..

Paul Donovan / UBS:

No holiday from inflation US personal income and consumption data is due, with strength expected in consumption (funded by savings and credit). Partly, this is due to the unremitting hedonism of the US consumer. Low unemployment will also help; while this has not translated into pay bargaining power, it gives a level of job security that reduces the need to save as an insurance against an uncertain future.

Attention will focus on the core PCE deflator as a measure of inflation. The forecast consensus is for an increase of 0.4% or 0.5%. Airfares will be part of this (the desire to go on holiday at any price is a factor). Seasonal adjustment may also boost the number—but what goes up in seasonal adjustment now, must come down later on.

Japanese consumer price inflation rose 1.9% y/y on the internationally defined core measure. Hotel accommodation was part of this move (the travel bug is a global phenomenon). Incoming Bank of Japan Governor Ueda suggested a “creative” approach to policy, hinting at some changes in spin without altering the accommodative substance.

German 4Q GDP was revised lower—as with the US revisions yesterday, this is a reminder that real-time data has become less reliable. Consumer spending was behind some of the weakness.

…AND in the category of I CAN RELATE,

More over the weekend BUT … THAT is all for now. Off to the day job…

https://www.citivelocity.com/siteminderagent/forms/login.fcc?isOnError=Y&errorMessage=REENTER_USER_AND_PASSWORD&TYPE=33554433&REALMOID=06-00015bc1-2064-1d0c-9b4b-8d099550f011&GUID=&SMAUTHREASON=0&METHOD=GET&SMAGENTNAME=-SM-1HxZr4fsP8iN8zyOwkUeTL5PDn4vPGiKyUnC8%2FJ7OlckSErk%2BjIa91ricnGbRsYbmvPeSObrpwn5guBRoUfzSrfx%2FWc9LkF9&TARGET=-SM-%2Fcv2%2Fsmartlink%2Fcommentary%2FAPIdc188f9b52dc4660870b766f1e5c1206%3FmenuCode%3DRATES_BILL_ED_RATES_CORNER&__prc=2&x-citiportal-requestid=4-03-CV-PCV6UFMMIEMRYC4AMKFYCCFJACAYGUG5477035902%406-7423678%2333