(USTs lower ahead of supply BUT relatively LIGHT volumes)while WE Slept; Chinese deflation over weekend, higher rates here to stay (Barrons) and S&P 6000 in 2025 ... plenty inbetween

In addition TO a better-late-than-never weekend edition with a look at 10yy ahead of this afternoons double - header auction (nearing TLINE support), thought it worth pausing a moment to consider this mornings 3yy …

… Cutting to the chase, TLINE ‘support’ mentioned above appears to ME to be up nearer 4.60% than not …

AND with that, we’re off and running in TO the week ahead and before recapping the weekend data outta China, lets pause to consider this past weekend, in case you missed (I did) and were unaware, BARRONS …

Even as inflation eases, global changes including less trade and growing government deficits will keep rates higher than before…

… One concern is that higher rates could throw sand in the gears of the housing market by exacerbating affordability problems. In the U.S. especially, where many homeowners locked in 30-year mortgages in recent years at rates below 4%, there is an incentive to stay put rather than move, given how much more expensive the next loan would be. As a result, prospective home buyers are facing not only higher mortgage rates but also less housing supply, since fewer existing homes are coming on the market than in the past …

… NOT all bad, though as some BENEFITS (to savers) from said HIGHER-FOR-LONGER structure of rates but still, maybe NOT what rate cut ‘istas were hoping for. On the other hand, perhaps it’s just another for the Magazine Cover curse group…

A study explains the business magazine cover curse

… Whatever you think you think, those still with the power of a Terminal at their fingertips (and capable of economically workbenching just about anything to prove a point) it all and always comes right back to your view on … CUTS / HIKES? 10yy and cuts / hikes priced via #finTWITs

More on this ‘stratEgery’ a bit below (HINT: MS has an even better graphic inclusive of stocks…) … FIRST

Reuters: China CPI fell at fastest pace in three years, -0.5% versus forecast -0.1%, while PPI also fell more than expected, -3.0% vs -2.8%.

… here is a snapshot OF USTs as of 706a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower, under-performing foreign bond markets ahead of a concentrated wave of Treasury supply today. DXY is a touch higher (+0.07%) while front WTI futures are lower (-0.65%). Asian stocks were mostly higher, led by the NKY (+1.5%) while EU and UK share markets are mixed and ES futures are showing -0.05% here at 7:00am. Our overnight US rates flows saw better buying in intermediates from real$ during Asian hours with a block FV-WN flattener posted during their hours too. In London's AM hours the desk reported a relatively quiet session ahead of supply, CPI and the Fed. Overall flows were mixed with some reported real$ selling in 3's and 10's ahead of today's auctions of the same. The 5yr sector saw better buying today although RV-types continue to fade belly strength in hope of reloading belly longs at better levels. Overnight Treasury volume was ~75% of average overall with 3yrs (111%) seeing the highest relative average turnover ahead of this morning's auction.

… the Treasury 5s10s30s 'fly sits near 1+-year range highs going into this afternoon's unsized (+$2bn) re-opening. One might guess that 10's are cheap enough on curve to fill Treasury's needs ahead of CPI and the FOMC??

WEATHER or not 10s cheap enough … well, only TIME will tell but for some MORE of the news you can use » The Morning Hark - 14 Aug 2023 and IGMs Press Picks (who CONTINUES to be sportin’ that new, fresh look) in effort to to help weed thru the noise (some of which can be found over here at Finviz).

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … in addition TO what all was noted over weekend HERE

Barclays: China: November deflation worsened (hey, that’s GREAT …)

Larger-than-expected deflation prints for the CPI and PPI added more evidence of weak demand in Q4. We expect the CPI to remain stuck in deflation in December-January before turning to inflation from February onward, while PPI deflation is expected to continue through to mid-2024 despite low base effects.

November: -0.5% y/y for CPI, and -3% y/y for PPI

Bloomberg consensus forecast (Barclays): -0.2% (-0.2%) y/y for CPI, and -2.8% (-2.7%) y/ y for PPI

October: -0.2% y/y for CPI, and -2.6% y/y for PPI

CitiFX Techs - H1 2024 outlook: Winter is coming (…and while 2s COULD drop 100bps, one should expect, “A slower drop in 10y and 30y yields”…)

WHAT COULD HAPPEN:

Bull steepening yields

US 2s10s could steepen to +26bps

US 2y yields face a quick slide to 3.55%

Soaring stocks, but caution warranted

All time highs are in sight for S&P 500

Watch closely for signs of a downturn

The de-throned Dollar

4.5% slide in DXY on the cards

98.8-99.6 will be the key support level

WHAT COULD GO WRONG:

200bps retracement in US 2y yields

30% drawdown in S&P 500

4% slide in USDJPY

DB: Mapping Markets: 5 hurdles for nearterm rate cuts

… But as in 2023, there are still some hurdles before we get to that point, particularly since we’ve just had the most serious bout of inflation in several decades. Indeed, even after the rapid rate hikes of 2022, market pricing at the start of 2023 still underestimated the extent to which central banks would remain hawkish…

1. The background context is very different to recent cycles, since we have just had the most serious bout of inflation since the early 1980s.

2. Unlike previous occasions when rates have been cut, there isn’t as obvious a reason for starting to cut rates right now. This is not to say there isn’t a case for easing policy, but the arguments appear less compelling compared to when previous pivots took place.

3. All this speculation about rate cuts has eased financial conditions considerably, and paradoxically is making rate cuts less likely.

4. This isn’t the first time in 2023 that markets have priced in rate cuts this soon.

5. There is a difference between central banks saying they won’t deliver any more hikes, and actively talking about rate cuts.

The first is leaving policy on hold, and the other is actively easing. So far, the Fed and others haven’t even gotten to the first point, and are still talking about the risk that they might need to do more hikes, rather than earlier cuts. Clearly that could change, but for the time being, the discussion has mostly been about whether hikes are done, rather than when cuts are moving into consideration.

Goldilocks: December FOMC Preview: Sooner but Not Soon

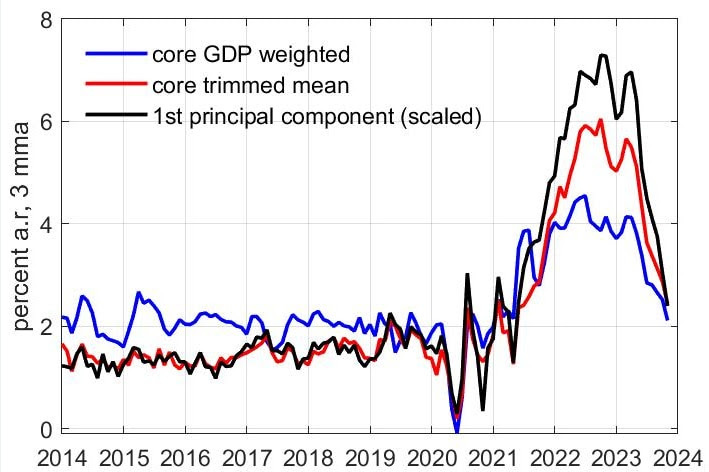

Recent inflation data have been an encouraging surprise even to our optimistic expectations, and our forecast path for year-on-year core PCE inflation has fallen somewhat as a result. Healthy growth and labor market data suggest that insurance cuts are not imminent, and with core CPI likely to print near 27bp on Tuesday and wage growth still too high we do not think that normalization cuts in response to a decline in inflation are either. But the better inflation news does suggest that normalization cuts could come a bit earlier than our previous forecast of 2024Q4.

We are therefore pulling our forecast of the first cut forward to 2024Q3. The change does not reflect any major shift in our thinking but rather that the rough thresholds for cutting that we have given previously are now reached earlier. It is hard to be too confident in the timing of the first cut, both because even modest surprises to our inflation forecast path could change the timeline and because our forecast of inflation in 2024 is flat enough that even if it were realized exactly, the FOMC could plausibly deliver the first cut either a bit earlier or a bit later than Q3….

Equities have traded well as Fed cuts have been priced into the bond market. Will the Fed push back on these expectations with the labor market and inflation still not cooling enough to declare victory? Meanwhile, soft earnings revisions vs. strong liquidity is a key debate for investors.

… Friday’s jobs data was important in this regard with the stronger than expected release taking 10-year UST yields higher by a modest 8bps. The 135 bps of Fed cuts that were priced into the bond market a week ago through YE 2024 were reduced to 110bps as of this past Friday. This reaction makes sense to us and there may be more to go in the near term if the CPI release this week comes in a little hotter than consensus expects. Of course, the Fed is also meeting this week and will have taken notice of the data as well. With the unemployment rate falling by almost 2-tenths in November and inflation data potentially remaining bumpy over the next 3-6 months (based on our economists' view), could we see the Fed push back on the bond market's pricing of rate cuts at this week's FOMC meeting? Meanwhile, as noted, our interest rate strategists are now neutral on duration post the significant move in rates over the past month and Friday's payroll report.

The market has revised its view of the Fed's policy path. We look into whether the policy adjustments of the 1990s can provide insights for the current debates.

… While history rarely repeats it often rhymes. We have 100bps of rate cuts priced in for next year, but as is often the case, the market has extrapolated. Our rate cut forecast is predicated on slowing real economic activity and falling inflation. Friday’s nonfarm payrolls print confirmed the down trend is in place. But from here, markets will clearly react—possibly in both directions—to data that will invariably be noisier than the forecast. We have one cut penciled in for June, and then from September, we see a cut at every meeting. Relative to our forecast, the market has gone from thinking we are too dovish to thinking we are too hawkish, with over 50bps of rates priced in by the June meeting. So, what might make our forecast wrong?

To the dovish side, the easiest answer is if the economy grinds to a halt and starts to contract. Friday’s nonfarm payrolls means that we would have to see a very surprising shift in trend over the next three months of data to get a cut at the March meeting. On the inflation side, a faster-than-expected fall in inflation might not suffice if it is driven by goods deflation, which the Fed will see as temporary. And perhaps more to the point, we actually forecast a rise in core inflation next week, driven by services inflation, especially for hotels and medical insurance.

What about on the hawkish side? For now, that outcome is hard for us see, but it was the market baseline not so very long ago; just last month, the market was pricing in only 2 cuts next year instead of the almost 5 it is pricing now…

… With all the available data, we stick to our baseline forecast as the best modal forecast. Our US team’s inflation forecasts have been particularly good this year, and the economy is slowing like we had anticipated. While we recognize that the path to a hard landing goes through data that will look like a soft landing, the data to date remains far from recessionary. After the volatility in recent quarters, I remain comfortable in our base case, though I have an even higher conviction that the market narrative will change at least once more before the Fed cuts rates. If I could give one piece of advice to the 1990s version of myself, it would be to forecast early … and be ready to revise.

UBS: Global inflation - receding as fast as it increased (dare I say, transitory?)

Global inflation is falling as fast as it increased, with 82-96% of the monthly 'run-up' in momentum of core inflation now reversed.

Global core inflation - monthly annualized run-rate

Friday’s US employment report was stronger than expected, but the surprises could be revised away in the coming months (US data quality has deteriorated, meaning more revisions). However, Federal Reserve Chair Powell’s failure to articulate an economic thought process and consequent mantra of “data dependency” has left markets at the mercy of high frequency data releases of dubious quality…

… Central bank meetings take place this week; “they would say that, wouldn’t they” seems an appropriate summary. Central banks are likely to try to reduce expectations of rate cuts through rhetoric. Markets are likely to look at the ending of profit-led inflation and price in rate cuts anyway…

Yardeni: A Christmas Market For The Bull? S&P 500 At 6000 In 2025? (paywalled BUT…)

… Along the way, we trimmed our year-end target to 4600. On July 19, we wrote: "The S&P 500 is now almost at 4600 [well ahead of schedule]. It closed at 4556.27 on Tuesday. Rather than raise our year-end target, we are raising our expectations for what the bull market could deliver through the end of 2024 and beyond. We think that 5400 is achievable by the end of next year. If that happens, then 5800 would be our target for the end of 2025. In other words, we think that the bull market has staying power." (By the way, in our November 1, 2023 QuickTakes, we wrote: "It's possible that the S&P 500 bottomed today.")

We are now raising our yearend 2025 target to 6000 assuming 2026 earnings at $300 per share and a forward P/E of 20. That's because we are seeing more reasons to believe in our Roaring 2020s scenario.

On Friday, the S&P 500 closed at 4604.37 (chart).

… And from Global Wall Street inbox TO the WWW,

Hedgopia: CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

Project Syndicate: Kenneth Rogoff: Higher Interest Rates Are Here to Stay (apparently he read Barrons this weekend :) just kidding as this was written 12/05 SO perhaps Barrons read THIS)

The long-standing economic consensus that interest rates would remain low indefinitely, making debt cost-free, is no longer tenable. Even if inflation declines, soaring debt levels, deglobalization, and populist pressures will keep rates higher for the next decade than they were in the decade following the 2008 financial crisis.

Sam Ro from TKer: The economy has gone from very hot to pretty good

Barron's gave Gold their Kiss of Death too. No matter fully expected that Gold self-off last Monday. Gold's my Pet Rock and Shield and it WILL shine again!

Great work !!!

Bond yield likely to regress, a little....

Must watch the 10 yr auction, today...

"pretty hot, to pretty good"

Powell & Co.....Very Happy.....

I'm ready for some "Roaring 20s"...Let's go !!!!!!!!!

Barron's gave Gold their Kiss of Death too. No matter fully expected that Gold self-off last Monday. Gold's my Pet Rock and Shield and it WILL shine again!