… HEREis what this shop says be behind the price action overnight…

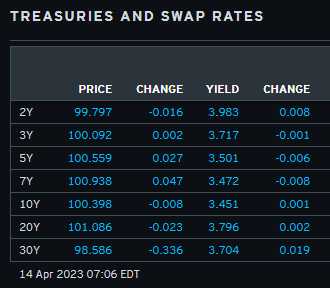

… WHILE YOU SLEPT Treasuries are little changed and the belly richer this morning ahead of bank earnings and a brace of tier#1 and #2 data releases. DXY is little changed while front WTI futures are modestly higher (+0.35%). Asian stocks rallied, EU and UK share markets are all modestly higher while ES futures are showing -0.15% here at 6:55am. Our overnight US rates flows saw yet another subdued Asian session with ongoing fast$ selling in the belly noted. Overnight Treasury volume was ~110% of average overall with 30yrs (181%) and 2yrs (162%) seeing some outsized turnover this morning.

… Our last attachment updates the US 1-yr CDS level, now well above 2011's peak. No wonder T-Bill investors have crowded into the shortest paper, avoiding the now-much-cheaper ~3mo cusips-- if this picture accurately reflects debt ceiling worries/sentiment??

… and for some MORE of the news you can use » IGMs Press Picks for today (14 APR) to help weed thru the noise (some of which can be found over here at Finviz).

In addition to all the news, something(s) from ZH which wasn’t mentioned above BUT which may very well impact the Fed, you and me personally,

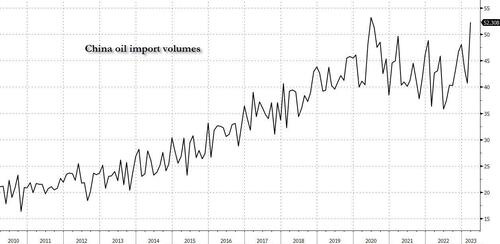

… Crude imports in March totaled 52.3 million tonnes, or 12.3 million barrels per day (bpd), according to data from the General Administration of Customs. This compares with 10.1 million bpd of crude imported in March last year Reuters noted.

Total crude imports for the first quarter stood at 136.6 million tonnes, a 6.7% increase over 127.9 million tonnes in the same period last year.

Um … hope you enjoyed lower’ish ‘earl prices and so, prices at the pump, while they lasted? Moving along then, I’m glad Yellen’s dept of Treasury was able to sell duration this week and yesterday’s 30yr wasn’t all that bad …

Read ZH for somewhat more but again, a look at 30yy daily and I’ll highlight the TLINE added just before sending YESTERDAY … it would appear to me, at least, to be of some relevance …

… until it breaks. What’s that saying? Trend is your friend until it bends? Momentum IS still pointing higher, perhaps more of an equity and ‘earl driven, ummm, ‘concession’ still in the offing?

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ … Starting with Paul Donovan of UBS

Yesterday’s US producer price inflation rate slowed, consistent with the profit-led inflation narrative. The transitory demand-led consumer durable goods inflation and the supply-led energy inflation have both receded into disinflation; both matter to producer prices. Profit-led inflation occurs more frequently at the end of the supply chain, affecting consumer prices more than producer prices.

March US retail sales test the rule “never short the hedonism of the US consumer”. There are concerns tighter lending standards will slow consumption, but there is little evidence of accelerated tightening so far. Because most credit cards will still have unused credit available, tighter standards do not immediately stop spending. This creates the Wile E. Coyote effect—consumers use this spare credit, and continue running off the edge of the cliff before economic gravity sets in.

Consumers in developed countries are switching consumption away from goods and towards services. Services like leisure travel are not fully captured in retail sales. However, the ongoing transfer of money from consumers to profit margins should have some dampening effect.

From a cartoon’ish take to a look at one firms measure of BIZ CONDITIONS … MS out last night noting,

Business Conditions: Credit Conditions Slump Worries over tighter credit conditions weighed heavily on sentiment in April - and were concentrated in services. Cost management initiatives such as layoffs and hiring freezes remain a key focus among companies in response to increased macro uncertainty.

Exhibit 1: Tighter Credit Conditions Begin to Bite as Firms State it is Moderately/More Difficult to Access Credit

In the first MSBCI survey since recent funding pressures emerged in the US banking system, credit conditions weighed heavily on business sentiment in April. The underlying details show that the deterioration in sentiment was concentrated in service sectors. The April survey was conducted from April 10 to April 13.

The Morgan Stanley Business Conditions Index (MSBCI) fell for the first time in three months, dropping 19 points to 44 (+50 = Expanding). This marks the largest month-over-month drop in the index since March 2020 when the index fell 23 points. 1 In the underlying details, the Services Subindex fell 42 points to 25, plummeting to a level not seen since November last year. The Manufacturing Subindex showed continued resilience rising to 67 from 63 - in line with our call that the ISM PMI bottomed in March.

Exhibit 8: MSBCI and the MSBCI Composite: Recent Performance

Turning from a biz condition index TO a rather large French bank and a (monthly) view of all sorts of things … here are some thoughts / excerpts from THE REPORT on US RATES,

USD rates: Fed to pause in June, curve to steepen in 2023

Base case is for a 25bp hike in May as the distribution of risks widens: The Fed is currently stuck between a rock and a hard place with an extremely wide distribution of risks, in our opinion. In just one month, Fed OIS pricing has gone from a 5.75% terminal rate with no cuts in 2023 to a 5.25% terminal rate with over 50bp of cuts priced in for 2023. SFRZ3 options-implied probability is pricing in “fat tails” in either direction with contracts showing a 90% probability that end-2023 rates will fall between 1.5-6.5%. Inflation and jobs data remain resilient with core services ex-shelter still at 8% y/y. The Fed has also persistently warned about the consequences of a premature pause − hence why we expect another 25bp hike in May (see US: Hike in May, then go away, dated 30 March 2023).

Pause in June and steeper US yield curve, data suggest: However, risks around the front end of the curve are asymmetric and we think the US rates market is moving into a steepening environment. The main focus falls on cooling economic data and lingering concerns about the banking sector. March payrolls were in line but showed a decline in average weekly hours, a deceleration in services-sector hiring and the first negative print in goods-sector hiring for almost two years.

Moreover, ISM manufacturing and services data missed estimates last week, with the ISM services new orders’ subcomponent down a whopping 10 points. As for banks, H8 data for the week ending 29 March showed that deposits have fallen by almost USD500bn in the last month and that banks continue to rely on the Fed’s emergency lending facilities, with H41 data showing BTFP + discount window usage at USD149bn last week. To us, this looks like a tightening credit impulse from banks and the economy is cooling in the right direction for the Fed to start thinking about pausing rate hikes in June.

Technical signals point to slower growth, steeper curve: We have revised our forecasts and now see a decent steepening of the curve this year where 2s10s reaches +10bp by the end of 2023, with the 2y at 3.3% (see US rates: Market-based rate cut signals accumulating, dated 4 April 2023). As regards technical indicators, the Fed’s near-term forward spread (NTFS) indicator is at around -160bp. Whenever the NTFS has reached -75bp before cutting cycles, the first rate cut has typically happened one to two quarters after. This signals that rate cuts could begin as early as Q3 2023.

Moreover, a 50% retracement in 2s10s inversion is typically followed by a structural resteepening of the curve when looking at prior hiking cycles. 2s10s reached peak inversion of - 108bp on 8 March which has now re-steepened by ~50%. Finally, a rotation from high-strike payers to low-strike receivers throughout a hiking cycle is quite common. 3m1y OTM receivers have now become much more expensive than OTM payers, which has previously presaged the last two recessions. Overall, we see a material steepening of the curve into Q3 once the terminal rate is reached in May.

From the PAUSE that refreshes camp and somewhat more in as far as PPI being the wind in the de / dis inflation’ista’s sails, a few words from all people — Dr Ed Yardeni

Could it be that the spike in inflation over the past two years was one of the many shockwaves caused by the pandemic? Is inflation turning out to be relatively transitory after all? Goods inflation is certainly looking transitory (chart). Services inflation has been much more persistent, but is likely to moderate during the second half of this year along with rent inflation. Wage inflation may remain troublesome, but less so if productivity makes a comeback from the adverse impact of the pandemic on the labor market.

This morning's release of March PPI data continues to support our disinflationary outlook for the rest of this year into 2024. The PPI for final demand fell to only 2.7% y/y, down from a peak of about 11.0% early last year (chart). PPI goods inflation has dropped from over 17.0% to 2.0% over this period. PPI services inflation (which does not include rent) fell from about 9.0% to 2.8% since early this year.

… I WANNA believe, really I do and so, HOPE as a strategy? Inflation in the rear-view mirror WOULD then be bullish for bonds, right?

Semi related and for us visual learners, the self—proclaimed ALL STARS of charts,

Despite another CPI report and the latest job numbers reflecting easing inflationary pressure, markets are a mess!

Indecision and uncertainty are running high. Investors simply aren’t able to get a read on the economy and the Fed’s next step.

I don’t blame them.

If you’re focusing on the Fed comments du jour or lagging economic data that will likely be revised in the future, confusion and pain are the higher probability outcomes.

That’s why we study price.

Let’s check in on the charts to clear things up…

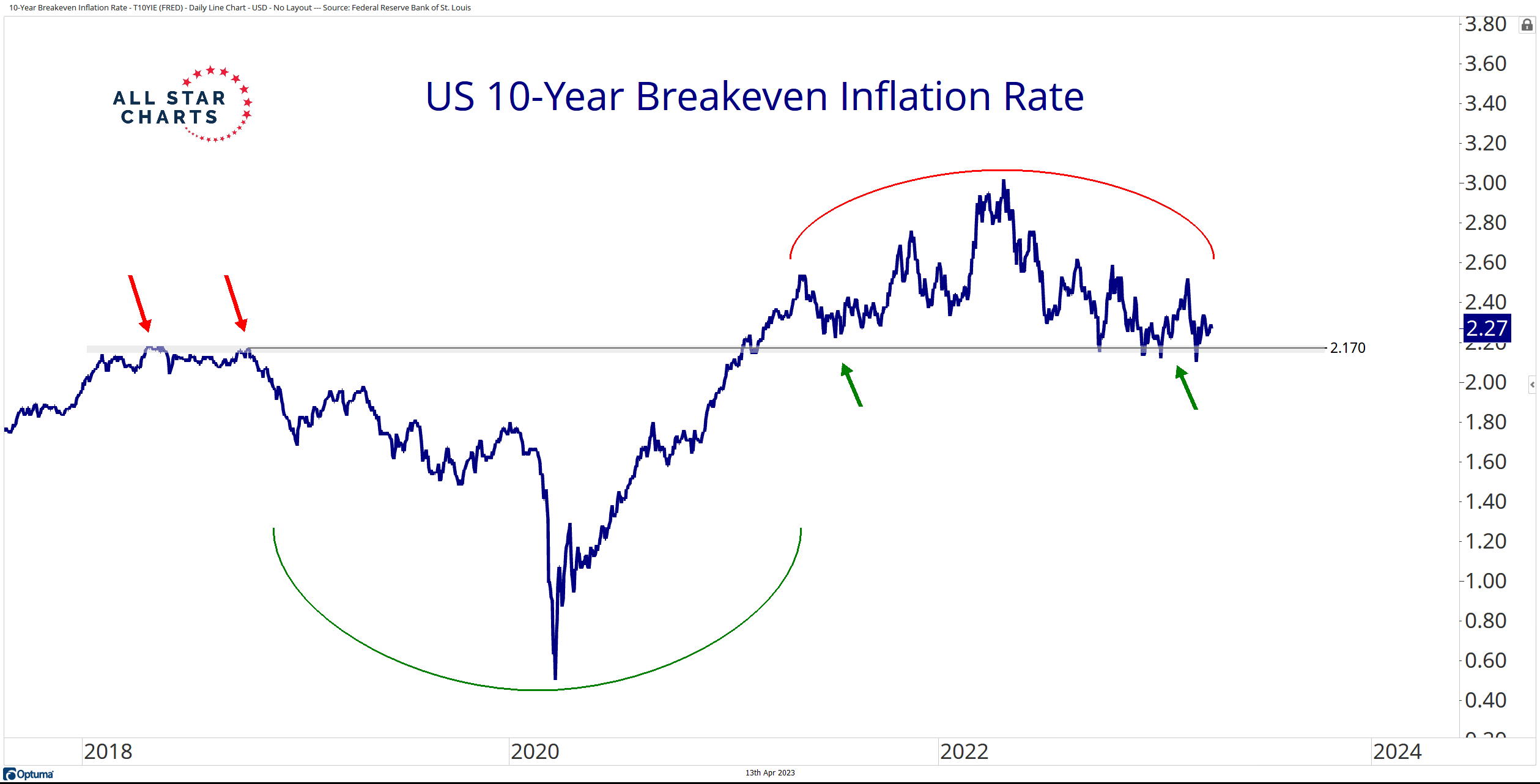

Here’s the US 10-year breakeven inflation rate:

This chart shows the difference between the 10-year nominal bond yield and its corresponding TIPS Treasury yield, gauging inflation expectations (or the real return on a 10-year Treasury bond).

While the chart doesn’t reveal direct buying and selling pressure, both yields are based on the bond market. And, as is the case for global risk assets, the former 2018 highs (the prior-cycle peak) are significant.

It’s hard to argue that disinflation is upon us if the 10-year breakeven inflation rate holds above those former highs. The same reasoning applies to inflationary assets, especially crude oil.

Check out the overlay chart of the US 10-year breakeven inflation rate and crude oil futures:

They move tick-for-tick over longer timeframes. I don’t want to make the bet these charts resolve in opposite directions.

With crude oil reclaiming its respective 2018 highs earlier this month, the commodity and bond markets — unlike the Fed — are sending a clear message: Inflation is not dead!

Sure, we can call it “sticky.” That’s fine as long as we understand we’re still in a rising rate environment and inflation remains elevated.

The charts tell the real story – a narrative that you can follow and trust.

Um, no … well, yea maybe … narratives always follow price and simply knowing that fact … well, I suppose then that qualifies one to be an allstar, too?

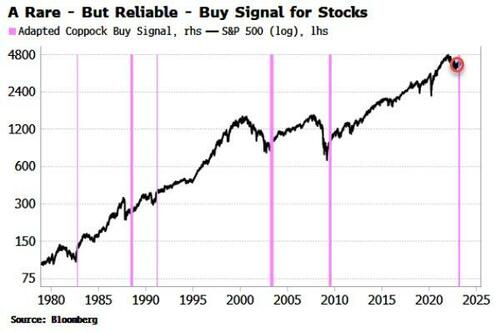

Lets give our collective selves a pat on the back?? Moving along then and for our inner stock jockey, some relief in form of a ‘rare buy signal’ — BBG via ZH,

A purely price-based signal suggests the bottom is in for stocks despite several lingering risks.

This is a hard column to write. Deposit flight, poor liquidity, weakening earnings, a credit crunch, recession – it would be much easier to list reasons why equities should be lower.

But that doesn’t necessarily mean it will be so. As anyone who has spent enough time in markets understands, they have a habit of being “anti-utilitarian”: causing the most people the maximum amount of pain.

It thus always pays to consider the other side of the case. But even with the best will in the world, it’s hard to fully let go of one’s biases. That’s why technical analysis can be so powerful.

Some call it voodoo, but using market data to identify trends is as old as economics, dating from the 18th century when Japanese rice traders used candlestick patterns to predict price movements.

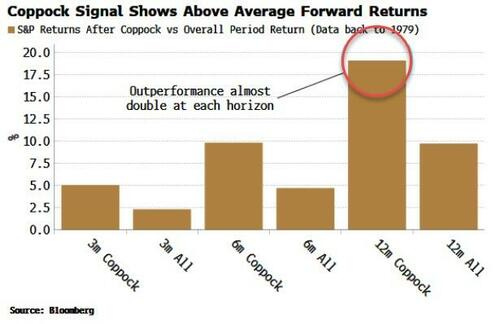

Recently, one very rare, technical-based buy signal called the Coppock has triggered, suggesting the long-term outlook for US stocks is constructive, and the bottom is potentially already in.

The Coppock is at base a momentum oscillator, which triggers when medium and longer-term measures of momentum begin to turn up on a persistent basis.

Based on adapted parameters, it triggers only rarely, but the times when it has done – e.g. October 1982, August 1988, April 2003, August 2009 – are a catalogue of generationally good buying opportunities. It outperforms the average S&P return over 3-month, 6-month and 12-month horizons, with the greatest absolute outperformance over 12 months (19.1% versus 9.7%).

The great appeal of technical signals is their simplicity. The Coppock uses only the S&P’s closing price on a daily basis. No economic data, no political inferences, no opinion – it is fixed and unemotional.

This also means signals such as the Coppock can trigger at very counter-intuitive times – a signature of contriarianism and a hallmark of many of the best buying opportunities.

The Coppock has previously triggered well before the Fed had started to hike again, when the ISM was under 50, and while the unemployment rate was rising. As the signal is not trying pick absolute bottoms, the S&P is generally already off its recent lows.

Similarly, today does not appear to be a good time to buy with economic data weakening and credit tightening, but if we were to listen only to the signal it is telling us to “buy and close your eyes”.

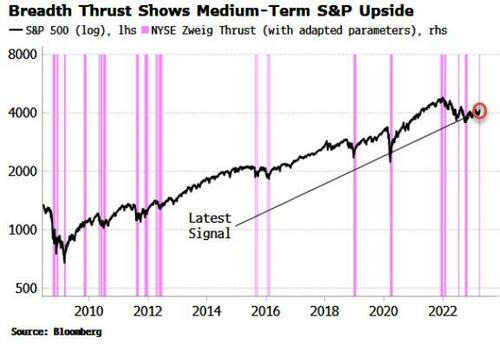

Another reliable signal, the Zweig Thrust, has also recently triggered. The Zweig activates more often and has more false positives than the Coppock, but it is a good gauge of the medium-term trend of the market.

The signal goes off whenever breadth (defined as the net number of stocks rising on the NYSE) rapidly goes from being very weak to very strong (i.e. “thrusts” higher). It shows good, above-average returns over the next one, three and six months.

If technical signals’ strength is their simplicity, it is also their weakness. No trader or investor could ever take a decision based purely on them (unless part of a more sophisticated quant strategy). It would be tricky, to say the least, to explain to a client or your CIO that you went long purely because one arbitrary moving average passed above another.

On the other hand, it pays to incorporate them into one’s view. In today’s case, the message is that despite everything pointing toward weaker stocks, the price action is whispering that that just might be wrong.

As already said, this was a hard column to write, and stocks could very well go on to make new lows before they exceed last year’s high. But great buying opportunities only look elementary in retrospect, and it would be remiss not to point out that this may be one of them.

Now not ALL is GOLDEN in as far as stocks and this BUY signal goes. At least not as far as Chris Kimble might be concerned. He is out with a chart which is showing how GOLD > dow,

Yesterday, the Federal Reserve (Fed) released the minutes from its March 21-22 Federal Open Market Committee (FOMC) meeting. In the section summarizing staff projections, to the surprise of some, the staff explicitly forecasted a recession:

“Given their assessment of the potential economic effects of the recent banking-sector developments, the staff’s projection at the time of the March meeting included a mild recession starting later this year, with a recovery over the subsequent two years.”

Three important things to keep in mind with this:

A projection is only a base case scenario. The consensus base case for Bloomberg-surveyed economists has also been that a recession is more likely than not in the next year for some time, so the call by the Fed’s staff should be no surprise.

Having a recession as a base case is by no means saying it is a “lock.”

The staff play an important role in supporting policymakers, but they are not the policymakers themselves.

As for Fed policymakers, they have been more careful about how they talk about the likelihood of a recession. But without saying it directly, even their projections imply a recession may be more likely than not over the rest of the year. FOMC participants’ median forecasts for 2023 economic growth and changes in the unemployment rate, last updated in March, both remain consistent with a recession in the second half of the year (although the dot plot is not).

With recession risks getting more attention in the wake of the FOMC minutes’ release, today we highlight some important characteristics of market behavior around recessions and some unusual features of the current market if a recession were to be on the horizon. Most of these points can be seen in the table below, which summarizes some key historical S&P 500 behavior around recessions.

After reading through market behavior and in context of 1937 onward, the firm lays out their 6 points of light, if you will … I’m jumping straight TO conclusion,

…We are wisely often warned that the most dangerous words in the industry are “this time it’s different.” In the current context, that phrase has often been used to caution a recession would likely come with a new market low. The problem with this argument is that this time has already been different. Saying we may not hit a new bear market low, even if we get a (mild) recession, is simply paying attention to those differences.

The risk of a new bear market low certainly increases if we get a recession and economic uncertainty remains elevated. But for now, our Asset Allocation Committee’s base case is that well telegraphed recession risk has already been meaningfully priced into markets and market participants may look past a mild recession as inflation continues to fall.We have recently reduced our recommended equity overweight on the combination of market gains and increasing risk, but still remain overweight overall.

Have cake. Eat it too. Whatever happens, we’ll see in future hits that THEY — LPL — told us so? WTaF!? Talk about economic workbenching and narratives following whatever the price action may be …

Welp, these folks are talking to US for a living and NOT the other way ‘round SO clearly I’m doing it wrong and so … Hope to have something over the weekend but THAT is all for now. Off to the day job…