(USTs lean green, belly leads thanks to Germany all on light volumes)while WE slept; revised yield f'casts (higher); 'more Powell-Bell' and "Lower Risks, Higher Rates"

Good morning … SURPRISE where overnight the RBA unexpectedly hiked 25bp as “Recent data indicate that the upside risks to the inflation outlook have increased” even as “inflation… has passed its peak”.

Another SURPRISE(s) from Germany where factory orders unexpectedly fell (-0.4% MoM) in April, weighing on the outlook for Europe's largest economy BBG Sliding German butter prices raise hopes for lower food inflation FT Eurozone retail sales were UNCHD in April- BBG.

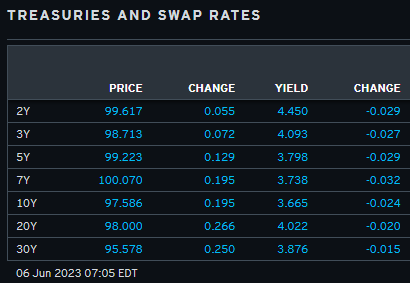

AND … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly higher with the belly outperforming; dragged along by an outperforming German Bund market this morning and despite a surprise (to most) +25bp RBA hike earlier. DXY is modestly higher (+0.12%) while front WTI futures are lower (-2.0%) despite the Saudi production cut. Asian stocks were mixed, EU and UK share markets are mixed-lower (SX5E -0.4%) while ES futures are showing -0.12% here at 6:50am. Our overnight US rates flows saw bear flattening in Treasuries during Asian hours as the RBA's 25bp hike set the tone then. Asian session Tsy volumes were decent (~90%) but desk activity was limited to real$ buying in intermediates. In London's AM hours, Tsy prices followed German bonds higher and we saw some long-end selling into the pop higher amid much lower turnover in their AM hours (~55% of average). Overnight Treasury volume was ~85% of average overall.

… and for some MORE of the news you can use » IGMs Press Picks for today (06 JUNE) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

First UP would have to be any time a firm (even those domiciled in France) are out with an updated dart throwing exercise and results. To whit,

BNP: US rates: Forecast reassessment

Evidence that the US economy is withstanding elevated policy rates better than expected can support further upward pressure on yields across the curve.

We accordingly revise our US yield forecasts higher, looking for outright cheapening in the coming months before transitioning to a bull steepening environment by year-end. We now project 2y yields at 4.05% and 10y yields at 3.85% for end-2023.

We see a greater probability that the Treasury yield curve remains somewhat sticky around current levels of inversion for the near term, given the Fed’s apparent resolve to re-engage with tightening if needed.

We close our standing 6m forward 2s10s curve steepening and long 10y TIPS recommendations.

We prefer to express a near-term short bias via 3m10y 1x1 payer spreads.

While we think our outlook supports tactical outright shorts, we prefer taking a limited risk approach given uncertainty over the summer, particularly as liquidity draining amid the TGA rebuild gets under way.

… The determination that more tightening is needed because of underlying economic momentum carries important information for the rates market. Continuing the cycle despite a policy stance perceived as significantly restrictive should prompt markets to reassess the level of rates that the economy is equipped to tolerate.

While that outcome may result in policymakers taking short-term rates higher, it also argues for upward pressure on intermediate and longer-term yields. Historical behavior has borne this out, with 5y5y rates typically being dragged higher as the trailing average of short rates converges from below (Figure 1).

Further, despite a very different economic cycle and much-reduced drag from global rates on Treasury yields, intermediate and longer-term forward US yields have not priced a material premium above where they were when the Fed stopped hiking in 2018. The passage of time without a severe recession should see further upward pressure on yields across the curve as the anchoring to the experience of the last cycle diminishes…

Good calls. Bad calls. UPDATED calls and everything in between … How’s about that service related ISM …

BMO: ISM Services Misses, Prices Paid Lowest since May '20

ISM Services in May fell to 50.3 from 51.9 compared to the forecast for a 52.4 read - the second lowest read since May 2020. The details were broadly softer as well, prices paid fell to 56.2 from 59.6 which is the lowest since May 2020, new orders declined to 52.9 from 56.1, and employment dropped below 50 to 49.2 from last month's 50.8. Overall, a weaker read from the service sector that, when taken with the manufacturing gauge released last week, adds to the narrative that the data is holding up well, but cooling at this point in the cycle….There is very little on today, or the rest of the week's calendar in terms of data, and with the Fed's pre-meeting quiet period underway, we expect cross asset correlations and technical considerations will play an outsized role in driving the price action.

And from a very narrowed view of the US data flow TO a more worldly outlook where a large German shop released a global outlook,

DB Research has just released our latest World Outlook (link here), featuring our updated views on economics and markets. We’ve called this edition “The Waiting Game…” becausewe maintain our call for a US recession in Q4 as the lags from tighter monetary policy really start to hit. As we've felt for a while, you have to respect the lag and be patient. Markets on the other hand are anything but and want instant gratification. That's what makes it an interesting time now and for the next few months ahead.

To recap we think this hard landing is the logical next step in a succession of alltoo foreseeable events since the pandemic: the biggest increase in the money supply in decades, followed by the highest inflation in decades, and then the most aggressive series of rate hikes in decades. A hard landing is just the next phase of this. If you're looking for hope we are optimistic about the prospects of AI changing the nature of our economies in the years ahead. We desperately need a new source of growth given weak productivity and poor demographics. And although AI is unlikely to help us out of this cycle, its promise is a hope we cling onto as we move deeper into the 2020s after a very challenging start to the decade.

The firm goes ON to detail the USA situation and specifically, on the Fed

… With recession looming, increasing focus has been on the timing and extent of future rate cuts. The modest adjustments to our forecast – primarily the delayed rise in unemployment – argue for a somewhat later start to the cutting cycle. If the economic outlook evolves as we now anticipate, with the unemployment rate around 4% by Q4 2023 and 4.5% by Q1 2023, we now see the Fed cutting rates in March 2024, one meeting later than our previous expectation. We then see the Fed undertaking 275bps of cuts over the year, coming primarily through 50bps increments. This would lower the fed funds rate modestly below our view of longer run neutral, which is currently around 3% nominal.

Rate CUTS then it is, as ones base case … This is, again, an excerpt of a WORLD outlook. For a more US-centered look,

Outlook update: The only prescription is more Powell-bell

Over a year ago, we argued that the most likely trajectory for the US economy was for a recession to occur by end-2023. We maintain that baseline view and continue to anticipate a moderate recession beginning Q4 2023 in which real GDP falls about 1.25 percentage points over three quarters.

With the labor market remaining resilient so far, our updated forecasts now see a somewhat delayed rise in the unemployment rate, which is expected to average just above 4% in Q4. This is down from our prior expectation of 4.5%. The unemployment rate then peaks just above 5% in Q2 2024, below our prior peak near 5.5%.

Inflation has remained sticky at elevated levels and the composition of recent elevated prints has challenged the prevailing narrative that focus need only be on core services ex-shelter. We continue to forecast well above target inflation through year-end, with core CPI and core PCE around 3.5% in Q4 2023. A recession and looser labor market will contribute to a steeper decline in inflation next year, where we see inflation ending 2024 modestly above the Fed's 2% target.

With the labor market so far proving more resilient than expected and inflation showing slower progress than hoped, we now see the Fed raising rates one more time in July, bringing the terminal rate to 5.3%.We have nudged the first rate cut back to March 2024, one meeting later than our previous expectation, and expect the Fed to slash rates by a cumulative 275bps next year. This would lower the fed funds rate modestly below our view of longer run neutral, which is currently around 3% in nominal terms.

As always, predicting the timing and shape of a recession is not a simple task. There remains considerable uncertainty around the precise quarters of negative growth and when the labor market will begin to soften. The latter has in particular been a consistent source of upside surprises. As such, relative to our baseline of a recession starting in Q4 2023, we see the risks skewed towards an economy that remains more resilient, takes longer to slip into a downturn, and requires more Fed tightening.

Now another strategist at the same firm offers something which doesn’t necessarily fit with the rate CUT base case…

Post the debt ceiling resolution, the massive TGA rebuild and bill issuance expected has sparked a scare that it will drain liquidity and hurt equities. We expect a substantial portion of the net issuance to be absorbed by money market funds and foreign central banks as they shift their holdings out of Fed repo programs to avail of the more attractive t-bill yields, reducing the impact on the popular measure of Fed liquidity, the Fed’s balance sheet adjusted for the size of the reverse repo and the TGA balances. See last week’s report for more details (Life after debt ceiling: TGA rebuild, bill supply outlook, and liquidity reshuffling, Jun 1 2023).

More broadly, we are skeptical of the liquidity narrative for equities. Contrary to the popular narrative, most of the gains in equities since the GFC and over the last 3 years are easily explained by fundamentals, leaving very little for the role of liquidity. The correlation between Fed liquidity and equity performance looks strong recently but is very inconsistent going back in time, which in our view suggests it is spurious. In contrast, the correlation between equities and measures of macro growth is strong, intuitive, and consistent, over the last 3 years as well as spanning several decades historically.

Hmmm so on the one hand, 88% correlation seems pretty tight to me but then, it’s only a very limited snapshot of history so … perhaps it will be different this time.

The game of narrative tennis shall, then, continue and I’d ask what YOU think … Back TO yesterday’s data, for example,

The US may be adding jobs in huge numbers but the key ISM business surveys cast serious doubt on how long this can last. The manufacturing ISM index is already indicating recession and the service sector will soon join it unless order books turn around dramatically

On that note of US recession FEARS, macro backdrop is remaining top of mind on Global Wall Street,

We see the market’s focus returning to higher-for-longer rates and sticky inflation after a U.S. debt ceiling deal. We prefer an up-in-quality portfolio.

U.S. stocks hit 2023 highs after the debt ceiling deal. Yields rose amid the specter of rate hikes after Friday’s payroll report showed a jump in new jobs.

China macro data is in focus this week. We trim our growth view slightly as the economic restart loses steam and policy reactions remain uncertain.

…Bottom line: The U.S. debt ceiling deal removes near-term uncertainty – we now expect markets to focus on the macro picture. We see higher-for-longer rates, so we keep our quality tilt in equities and bonds and prefer income for now. We like short-term Treasuries, emerging-market local currency debt and inflation-linked bonds.

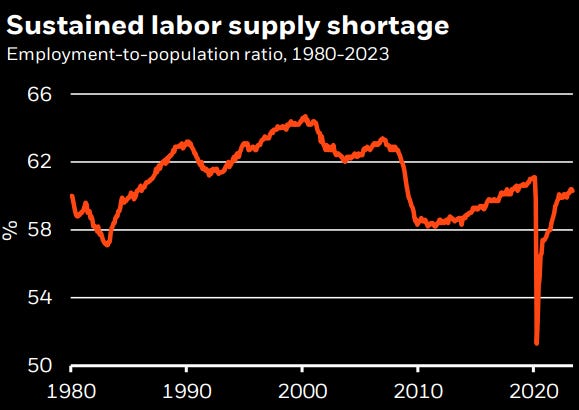

… Macro take Last week’s U.S. jobs report showed 339,000 new jobs were created in May, way above expectations of 195,000. Unemployment rose to 3.7% from 3.4% but the employment-to-population ratio – the share of the total population in work – was little changed. See the chart. That means labor supply hasn’t increased. The worker shortage doesn’t appear to be easing.

The labor shortage persisting means pay growth isn’t slowing down either. Average hourly earnings grew by around 4% in May, still too high to see inflation come back down to the Fed’s 2% target. But this measure doesn’t adjust for the pandemic’s impact on the services sector. The employment cost index (ECI) measure does, and it shows wages rising even more quickly.

This is still a very tight labor market, beset by shortages, and this report leaves the possibility of further Fed hikes firmly on the table, in our view.

We have used the word “unprecedented” to talk about the economy during and after COVID. We have never before locked down economic activity, while printing trillions of new dollars to help finance trillions of extra government borrowing to pay people not to work. But now, it’s all over…the Federal Reserve has lifted rates, M2 is falling, and we’ve stopped paying people not to work…

… Now that we are getting back to pre-COVID levels it is hard to imagine where more growth will come from. If people normally go to three baseball games or two movies a year, they aren’t likely to double down to make up for what they missed during COVID.

In other words, the economy may be finally seeing the end of COVID distortions, but the data suggest that growth is getting a lot harder to come by. Many companies have likely been hoarding workers and if GDI is sending the correct signals this can’t last.

We still expect a recession starting sometime in the next twelve months, but with productivity falling that recession may not be the long-term fix for inflation that many seem to believe. This is hard for us to say, but the market seems to be ignoring a whole lot of economic problems and pain that aren’t really that hard to see.

And so, the NARRATIVE tennis game continues … One last volley and I’ll crawl back underneath the rock from which I came,

We have cut our judgmental probability that the US economy will enter a recession in the next 12 months back to 25%, undoing our upward revision to 35% shortly after the SVB failure. There are two reasons for this change. First, the tail risk of a disruptive debt ceiling fight has disappeared. The bipartisan budget agreement to suspend the debt limit will result in only small spending cuts that should leave the overall fiscal impulse broadly neutral in the next two years. Second, and more importantly, we have become more confident in our baseline estimate that the banking stress will subtract only a modest 0.4pp from real GDP growth this year, as regional bank stock prices have stabilized, deposit outflows have slowed, lending volumes have held up, and lending surveys point to only limited tightening ahead. Meanwhile, the economy is getting a sizable boost from the recovery in real disposable income and the stabilization in the housing market. This leaves us with a 2023 growth forecast of 1.8% (annual average), well above both the private-sector consensus and the Fed’s view.

Shit who cares what I've got to say on the matter, listen to DDB w/Charles Payne yesterday: "the BLS could declare that we're already in recession at ANY time now" (If I've confused the alphabet soup agencies my bad you get the point!).

understood and yea, all kinda nonsensical BUT ... always a big BUTT, listening earlier this morning to Neil Dutta of RenMAC and he's committed optimist and very convincing ... he and Riccodana were going back and forth a bit i'd LOVE tro see Dutta and Rosie in a room right now both very well spoken and a command of facts. Better might be Dutta and Eric Basmajian (EPB)

Shit who cares what I've got to say on the matter, listen to DDB w/Charles Payne yesterday: "the BLS could declare that we're already in recession at ANY time now" (If I've confused the alphabet soup agencies my bad you get the point!).

understood and yea, all kinda nonsensical BUT ... always a big BUTT, listening earlier this morning to Neil Dutta of RenMAC and he's committed optimist and very convincing ... he and Riccodana were going back and forth a bit i'd LOVE tro see Dutta and Rosie in a room right now both very well spoken and a command of facts. Better might be Dutta and Eric Basmajian (EPB)