(USTs higher, curve steeper, EZ PMIs disappointed) while WE slept; as the world turns ... rates vol echoing '08, margin debt and vigilantes are being sought

Good morning … I’d normally ask what’d I miss but then, I never really miss a day (but often miss much) … There’s been so much going on past couple / few days and over the weekend and via Blonde Money,

Boris pulled out of the Conservative leadership race.

South Korea last night fired warning shots after a vessel from North Korea crossed the maritime border.

China GDP Q3 grew 3.9% yoy vs f/c 3.3%; Retails Sales growth slowed to 2.5% vs f/c 3%; IP rose 6.3% vs f/c 4.8%.

There was more suspected ¥ intervention by Japanese authorities overnight as the currency jumped 4 yen to 145.28.

this mornings update will (once again) be cut short due to travels. It appears not much has changed since I left … The bearish TREND, generally speaking (until this morning) has continued — at least here in the USA,

Meanwhile, in the UK where apparently political turmoil is a BOON to it’s 2yr debt, down 33bps on the morning (so far)

Ok … back TO my lane and so, here is a snapshot OF USTs as of 708a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher and the curve has pivoted flatter (UK and EU PMI's disappointed), maybe somewhat dragged along by the sharply bull steepening UK curve with UK 2's rallying an eye-watering -40bp this morning. DXY is higher (+0.33%) while front WTI futures are lower (-1%). Asian stocks were mixed except in Hong Kong (Hang Seng -6.4%, HS China Ent -7.3%), EU and UK share markets are all higher (SX5E +1.3%, FTSE 100 +0.25%) while ES futures are showing +0.35% here at 7:15am. Our overnight US rates flows saw the post-Daly bull steepener continue into Asian hours despite block-selling in FV futures. We saw long-end selling from fast$ and profit-taking of steepeners added last week perhaps. During London hours we had a choppy morning with TY and FV block sales fading the Asian hours strength. 10's hit 4.20% when EU real$ and fast$ names bought after the UK and EU PMI misses. Overnight Treasury volume was ~140% of average all across the curve.

… Treasury 5y yields, daily: Switching to duration now, the bear trendline for 5yrs pretty well defined, as illustrated. Yields remain above it but.... A) there is evidence of evolving bullish divergence (lower highs in momentum and higher yield highs) and B) 5yrs appear to be tracing out an Ascending Wedge (drawn in) which suggests a 'petering out' (Edwards and Magee) of selling interest. Bulls will want to see that bear trend taken out by a close and we believe such a bullish breakout would/will be a 'go-with' event.

… and for some MORE of the news you can use » IGMs Press Picks for today (24 Oct) to help weed thru the noise (some of which can be found over here at Finviz).

In as far as a few items / things / links from Global Wall St inbox, well, I’ve no idea where to begin, to be honest.

(this seems blatantly obvious and a feature not a design flaw sponsored, at least in part, by fiscal follies and a misinterpretation by stonk market of, well, nearly everything — see the very next link)

Barclays weekly MACRO view: Running on empty. Data and earnings surprise on the upside, pushing further out a potential policy pivot … In the US, it is still early to fade the rise in long-term rates, as the data do not suggest that a meaningful slowdown in the labour market or inflation is imminent — or that an accompanying bond market rally is around the corner. In the UK, political turmoil piles pressure on the Treasury to deliver a fiscally responsible budget on 31 Oct. BoE asset sales are due to begin the following day.

Same shop on a stocks VIEW, diving a touch deeper, shedding some further light

U.S. Equity Insights: The 3Q22 vs FY23 Disconnect Equities rallied last week despite a bad CPI print and rising rates. The Value-driven rally leaves aggregate valuations even more vulnerable to an expected growth slowdown. Initial 3Q earnings were better than feared but on lowered numbers as revisions accelerated. Yet, FY23 EPS estimates remain surprisingly intact.

Fade This Bear Rally...

NOT a stock guy (although somewhat MORE attached now than before) and SO, moving along to the idea / notion of what we think the FOMC is thinking … on heels of Friday’s WSJ story (75bps NOV but maybe only 50bps in DEC?), WFC offers

…In our view, the most important aspect of the November 2 FOMC meeting will be how the post-meeting statement and press conference frame policy considerations ahead. The FOMC could begin to stress the cumulative effect of tightening, which could signal that it is preparing to shift to a slower pace of rate hikes in the meetings ahead. Indeed, we are starting to hear more caution slip into the remarks of some Fed speakers.

Along with our estimates for key inflation and jobs data to soften ahead of the December meeting, the more cautionary notes we are beginning to hear from some policymakers leads us to expect that the November meeting may very well deliver the last 75-bps hike this cycle, and that the Fed is likely to step down to "only" a 50 bps hike in its final meeting of the year.

Perhaps STOCKS simply reacting to the idea // HOPE for December? For more, turn now to MSs stock jockey in chief,

A Good Start as Stocks Rally in the Face of Doubt and Higher Rates Last week's tactical bullish call was met with doubt from clients, which means there is still upside as we transition from Fire to Ice—falling inflation expectations can lead to lower rates and higher stock prices in the absence of capitulation from companies on 2023 EPS guidance.

… Looking at the past few recessions and major drawdowns in NTM EPS forecasts, one can see the market didn't "pre-trade" the large scale earnings cuts. However, this time around it does appear as if it has. In fact, Exhibit 3 shows the current level of the S&P 500 is implying a drop toward $200 for NTM EPS versus the current $234. What's missing from this chart, of course, is the massive move higher in rates which means the relationship in this chart may be broken. Nevertheless, 3500 on the S&P 500 has discounted a lot of bad news, and until NTM EPS really comes down, it's going to be hard for that level to break decisively.

NOT a stock guy but if I were I’d continue to read this guys views and this weeks warmup incl a section on, “RATES, SEASONALS AND EARNINGS REVISIONS”

Equities markets look to have a strong bias toward the idea that surely, by now, the worst is over. The S&P 500 index has bounced back twice after dipping below 3,600 — a level it tested back in mid-June. The VIX fear gauge is elevated, hovering around the 30 level that tends to signal bears in the ascendant, but then hedging for further declines in the S&P has fallen out of fashion.

That could signal that all the doom and gloom has been priced in, or it could be more about investors starting to decide cash — which now provides some actual interest payments — is a better hedge these days. Treasuries traders meantime are sending the MOVE gauge of bond volatility close to pandemic-era highs. The relatively more elevated levels for the VIX’s bond-market peer add to the air of 2008 redux, when bond angst burst higher well before equities got hammered.

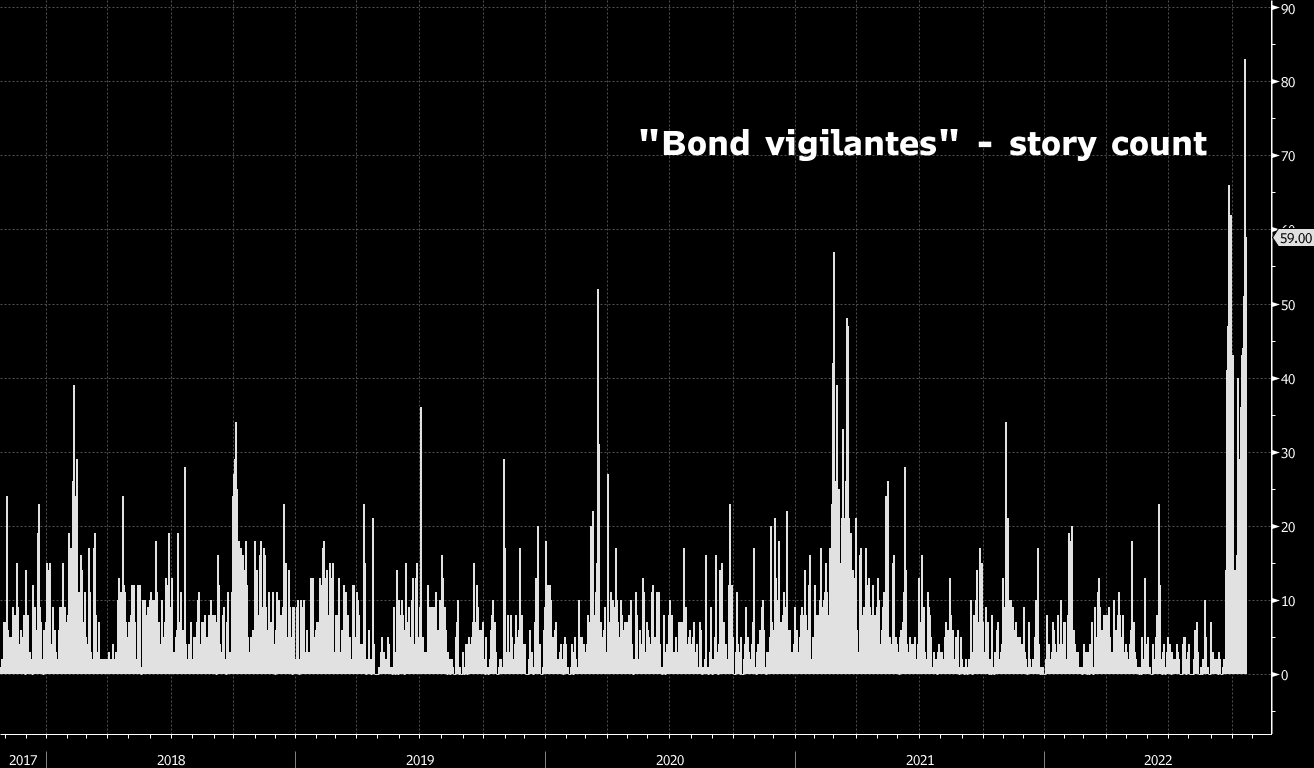

AND … yep you guessed it. From stocks back to BONDS as the world continues to turn and I try and get back in swing of things with my head on a swivel. THIS from BBG specifically the part on the BOND VIGALANTES being back (at least via SEARCH)

"Bond vigilantes" are back. Well, not exactly. But mentions of the term in news stories is back big time, as this chart shows. Ever since the UK’s mini-budget on Sept. 23, use of the term has been at the highest level in years.

The narrative is that investors were willing to lend to rich governments on the cheap after the Great Financial Crisis, and now with inflation roaring back, they're pushing against fiscal profligacy. No more free money.

Let's unpack this for a minute. It's true that inflation is very high basically everywhere in the entire world. And it's also true that, all things equal, expansionary fiscal policies (tax cuts, spending increases, etc.) would probably worsen inflation. Because at a time of scarce resources (of all kinds) increasing aggregate demand would only worsen the crunch, driving prices even higher.

It's also true that higher inflation, or higher expected inflation, would provoke more of a response among central banks, whose mission at this point is to counteract any inflationary pressures.

So it's true that any expansionary fiscal policy would likely lead to higher yields on government bonds. But it's important to get the logical sequencing right. The issue is not decreased investor willingness to "lend" per se. But rather the domestic central bank's expected response. A government bond market is, more or less, a giant prediction market on the actions of the central bank. When traders expect more rate hikes over the course of the next 10 years, the 10-year yield rises and so on.

There are a few reasons why this is important. For one thing, not all increased "borrowing" is going to have this same inflationary impulse. Tax cuts for Bill Gates or Elon Musk would probably have almost no impact on the economy, other than making them richer. Whereas checks to middle class households would probably increase demand in some manner. Secondly, and perhaps more importantly, the big question for governments here is not necessarily whether leadership has the credibility and support of the market, but specifically whether there's alignment between fiscal authorities and the central bank. This will play out differently in different countries, but it's worth watching as a theme, with the UK being perhaps the first example.

While I do WISH I could say it’s great to be back to ‘the grind’, as that saying goes, beggars can’t be choosers (?) and SO … it’s Monday FUNday and with that, just and as always, another episode of how the world turns (thanks, Felix for sending / pointing this one out)