Good morning … Bonds ‘round the world BID and USTs lagging as RBA hiked policy rates 25bp to 3.60%, a 10th straight hike since May last year. However, the RBA noted slowing consumer spending and said they may be nearly done tightening- which sparked a 14bp rally in Aussie 3yrs this morning RTRS

As you can see, trading at 4.58% is very near by some ‘support’ (4.68/70%) AND at the same time as we’re approaching ‘support’, momentum (stochastics, bottom panel) have crossed bullishly (ie lower rates) … Interesting timing as it would seem counter-intuitive just ahead of JPOW and THEN supply for a rally to begin in earnest … (economic) haters’ gonna hate or perhaps they think they know WHAT ever it is JPOW about to say (and the economy is ‘bout to do…)

… There’s some ‘good’ news from the FRBNY … Global Supply Chain Pressure Index (GSCPI) is DOWN

Estimates for February 2023

Global supply chain pressures decreased considerably in February and are now below the historical average.

There were significant downward contributions by the majority of the factors, with the largest negative contribution from European Area delivery times.

The GSCPI’s recent movements suggest that global supply chain conditions have returned to normal after experiencing temporary setbacks around the turn of the year.

Latest Update February 2023

For somewhat MORE on this GSCPI,

WolfStreet: Global Supply Chain Pressure Index Drops Below Average for First Time since Aug. 2019, after Horrendous Spikes

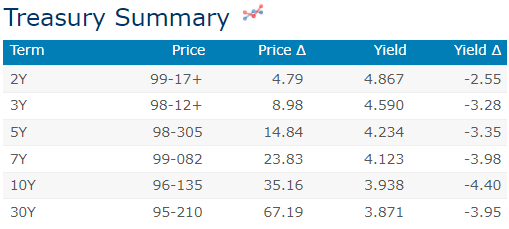

AND … here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher and underperforming the snap-back rallies in EGB's, Gilts and Aussie bonds (see link above) this morning ahead of Powell's Senate testimony at 10am. The yield curve is little-changed. DXY is little changed (+0.07% at 6:30am) while front WTI futures are modestly lower (-0.45%). Asian stocks saw weakness in China-linked exchanges but strength elsewhere, EU and UK share markets are little-changed while ES futures are showing +0.2% here at 6:30am. Our overnight US rates flows saw muted activity during Asian hours with some better selling in intermediates noted from fast$. In London's AM hours the desk saw on-balance selling too but in unremarkable sizes, apparently. Overnight Treasury volume was ~90% of average with relatively high average turnover seen in 3's (127%) and in 7's (121%)…

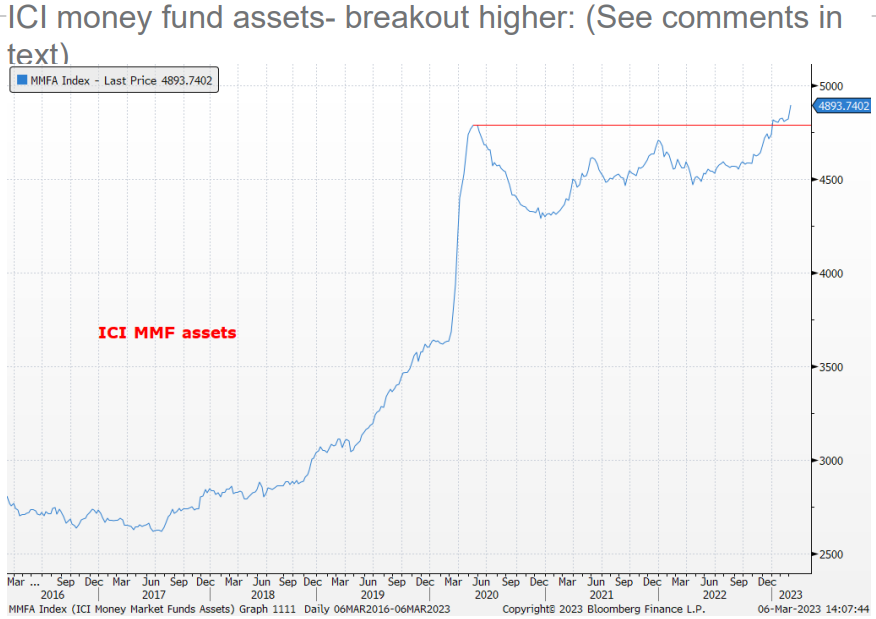

… Our third attachment shows the recent breakout to a new historic high in ICI money fund asset

… and for some MORE of the news you can use » IGMs Press Picks for today (07 MAR— and STILL SPORTING THAT NEW LOOK!!) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

In the case you hadn’t heard … JPOW (NOT an economist) speaking at 10a (to a bunch more who are NOT economists). UBSs Paul Donovan,

In the US today, a non-economist will attempt to explain to a collection of non-economists the extraordinary complexity of an economy undergoing dramatic structural change. The questioning will be mainly partisan point scoring. The question Fed Chair Powell needs to be asked is “what do you think you are doing?”. Powell has yet to explain how raising rates will tackle profit-led inflation. Pursuing higher unemployment seems an ineffective response…

With JPOW (today/tomorrow) in mind, a large German bank offers this,

After the Great Financial Crisis, the market (as per Figure 1), went through a long period where the response to the Fed Chair's semi annual testimony was tepid, until the market sprang to life on the day of the last two testimonies. This has given hope of an outsized reaction to Powell this time around, which is prone to be disappointed because Powell does not have crucial data to hand to give the market a firm steer before the next FOMC meeting. In general it should be expected that the Fed Chair will not try to guide the market away from its more hawkish bent following the NFP and CPI data, and, if there is a tone it is more likely to be hawkish than dovish, not least in his attempts to parry the mounting criticism that the Fed has fallen behind the inflation curve again. How the Chair answers questions on whether 50bp will be considered at the next meeting; on how tight he regards financial conditions to achieve inflation goals; the extent to which recent Q1 data represents a sustainable rejuvenation of activity; and, pointers to any current and future improvement in core services ex housing inflation trends, are some obvious possible avenues to vol creation. In the final analysis, it is doubtful that the Fed Chair changes the current proclivity to sell notes and bonds across the curve on price upticks, which in turn is prone to err mildly USD positive.

JPOW today / tomorrow aside, we’ve got NFP on Friday and a note from ING asking,

February US jobs report preview – was January a fluke? Half a million jobs were added according the the January employment report, yet the raw data suggests it was more a case of warm weather reducing the ususal seasonal firings with favourable seasonal adjustments providing an additional boost. February is likely to revert to the 200k trend with downside risks for coming months as lay-offs rise

… Longer terms things are more challenging

The outlook is deteriorating though. Job lay-off announcements are rising sharply with outplacement firm Challenger, Gray & Christmas reporting that lay-offs rose 440% YoY in January. The data is volatile, but if we take a 3M average of the annual rate we see that such big increases in lay-offs do typically result in employment growth eventually turning negative – the chart has employment on the right-hand scale inverted (orange line) so a movement higher implies weakening.

Challenger lay-offs and monthly changes in payrolls YoY%

… Lending conditions and higher borrowing costs will turn the screws on struggling companies

Compounding the problems is the fact we are also now seeing banks tighten their lending standards dramatically, meaning that not only is the cost of borrowing becoming more of an issue, but so too is access to borrowing. Companies and households that are already struggling will find themselves in an increasingly precarious position, especially with the Federal Reserve’s semi-annual monetary policy report emphasising that "a period of below trend growth and some softening of labor market conditions" is required to ensure inflation returns to 2%.

Banks tightening lending standards runs the risk of sharply higher unemployment

Source: Macrobond, ING

The chart above suggests that following such a sharp tightening of lending standards the unemployment rate has a tendency to climb around 9 months later. So, while for now there is optimism on the jobs market that is fueling expectations of interest rate increases, we see a clear risk that this environment changes over the summer months and our call for rate cuts before year-end starts to become more mainstream.

Then there’s this from a rather large French bank (a note for your inner PUT-SPREAD’er’er)

Hedging a hot print and higher rates: In a scenario of materially higher front-end rates, we would expect to see equities trade lower, led by Growth indices.

“History never repeats itself, but it does often rhyme.” - Mark Twain

Something we’re often asked is which era in history is most like this one. Perhaps the obvious answer is the 1970s, given the energy shock and high inflation. Others have pointed to the late-90s and early-2000s, when the dot com bubble burst and big tech valuations fell substantially. Or maybe it’s more like the 1960s, another era where policymakers moved to fine-tune economies amidst low unemployment, but where inflation got increasingly out of control.

This is not simply an abstract historical question. The lessons of history and how past situations were dealt with can play a key role in understanding the economy and markets today. For instance, we are experiencing the fastest monetary tightening in a generation, in large part because central banks are desperately trying to avoid a repeat of the 1970s experience. And after the Covid-19 pandemic, governments pursued the biggest stimulus packages in peacetime history, in part because they were trying to avoid a repeat of the sluggish post-2008 recovery.

Amidst all these events, there are also some longer-term trends running through the decades. The biggest is the relatively continuous slowdown in growth over time, which has been far more sluggish since 2008 than it was over the previous half-century.

Given that the lessons of history (or perceived lessons) exert a strong force over the present, we run through the decades of recent history, starting with the 1960s and ending up with our own time. Throughout, we focus on the differences and similarities between those situations and what we face today, and see if any lessons are applicable for our own time.

… With all this happening, it can be hard to make predictions. But there are several lessons and observations from history above that do seem appropriate to our own time:

1. Unlike previous inflationary episodes, there has been no attempt today to use fiscal policy as a stabilisation tool to slow the economy and reduce inflation. So if monetary policy struggles to do the job, or there is resistance to further rate hikes (e.g. from mortgage holders), then more of the burden could fall on fiscal policy. 2. Historically, reducing inflation has needed real policy rates in positive territory. As in the 1970s, it will be difficult to get a grip on the situation if the real cost of funds is negative. 3. When deficits have been run at unsustainable levels and debt interest payments are rising, there is usually pressure to get them under control again. Given the current debt trajectory across much of the advanced economies, at some point we could be in store for this again. 4. In an environment of very low unemployment like today, policymakers have more space to focus on other issues, like climate change. But if unemployment becomes a serious issue again, that space will diminish. We have already seen environmental goals de-prioritised in the short term because of the desire to protect consumers and businesses from high energy prices. 5. At the geopolitical level, international tensions can continue for a long time without any formal conflict. For instance, the Cold War did not see a direct outbreak of fighting between the US and the Soviet Union, even if there were “proxy” conflicts such as the Vietnam War where each backed a different side. Today, we have already seen a trade war between the US and China since the late-2010s, and whilst it is certainly possible that tensions remain high for some years and decades, it is entirely plausible for this to continue without a military element.

Finally, something that becomes apparent across the decades is how growth is trending down and debt is trending up. That's a big problem, since higher growth is what ultimately drives living standards and means we are wealthier today than previous generations. It also makes it harder to solve other problems, like the demographic challenge of ageing populations, or inequality, since a growing economic pie makes redistribution easier. At the same time, higher debt means that the major economies are more vulnerable in the event of a shock, particularly in an environment of rising interest rates as is happening today.

This question of growth and its interaction with debt is the biggest long-term macro conundrum. How it's resolved will ultimately be one of the biggest influences on how we write about future decades.

Given the large German bank focus on history, worth also noting some analysis on the BoJ as there’s some lessons for US all to learn. To whit, an early morning REID

DB Research has just released a Special Report on Japan, arguing that the country is on its way to 2% inflation. This is a once-in-a-generation regime shift, and our baseline is that the Bank of Japan’s yield curve control will be withdrawn by mid-year and that interest rates will be taken back into positive territory (+10bps) by next year. Once the transition to 2% inflation is complete, we expect the BoJ will have to increase rates to 2% accompanied by a QT programme of around 35tn yen/year. We also discuss the implications for monetary policy, along with the impact for bonds, equities and FX. See the full report here***

The last thing from this very same large German bank I’ll note today (I promise) may very well be the most important and ultimately the most important one … Given the dream of home ownership as it currently stands with regards to high / rising (?) interest rates,

Mortgage rates sustained at two-decade highs are taking their toll on housing market activity and prices. The US downturn is now more substantial as the decline in existing home sales has gone further and is now deeper than in 2007-10. However prices have only just erased year-overyear gains, and existing home inventory remains very modest on a historical comparison. Nevertheless the continued record low in Univ. of Michigan homebuyer sentiment and housing affordability measures suggest further weakness is ahead.

AND … THAT is all for now. Off to the day job…have a great start and hope this all helps as you plan your (HH, 3yr auction) trades and TRADE your (HH, 3yr auction) PLANS!