(USTs are "slightly weaker/flatter from overnight on light volume/activity")while WE slept; a general sense of 'sellers remorse' AND a rates (view gets)RESET

Good morning … what if a PAUSE is ‘bearish’ and HIKES are bullish?

What has transpired over the past couple weeks surely must make someone else consider these possibilities, no?

IF the Fed were to be done AND presumed to be cutting rates next, with inflation — sticky or not — about where it is now, might that not HURT more than it might help?

Are we TOO trusting in policy makers of all shapes and sizes and sides of the aisle with the current trajectory as simply enough?

LAST week we had a couple central banks come back from pauses with HIKES — SURPRISE! This week the FOMC pulled out ‘hawkish PAUSE’ from the playbook as the PBoC EASED and the ECB HIKED … surprise all around.

If you don’t think they are confused, then WE aren’t payin’ attention.

I mean to say I’m certain they BELIEVE they aren’t wrong and know exactly what they are doing BUT perhaps it is, as Barclays notes below — IT is more about growth than rates … let’s see how then earnings develop over the next several quarters and see IF Mike Wilson is more right than not…for NOW, though, I’ll stay in my bond lane…

And in that lane is still a DAILY triangulated look at 10yy which have very little in way of signal from MOMENTUM (stochastics, bottom panel) so we’re likely to look ahead TO a holiday long weekend where POSITIONS are squared and I’ll make an effort to run thru bigger picture WEEKLY visuals over the weekend. Preliminary glance shows momentum becoming somewhat more oversold — not yet suggesting a roll over — as yields there too continue to triangulate.

For NOW … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are slightly weaker/flatter from overnight on light volume/activity, risk and FX markets (save JPY -0.5%) consolidating after no action from the BoJ and concerns about a bank reserve liquidity drain soothed (see RRP comments above from Rates & Econ). Global stocks are still on track for the best week since March with Asian markets boosted by bets on a comprehensive stimulus package for the Chinese economy (SHCOMP +0.6%, HIS +1.1%), while European indexes are buoyant (DAX +0.3% and FTSE 100 +0.2%). EGBs are bull-flattening with decent peripheral outperformance (BTP 10s -6bps). UST 2s10s is 3bps flatter, spreads slightly tighter, while S&P futures are showing +1.5pts here at 7am. Mind the Fedspeak today as Waller will break silence post-June meeting at 07:45est.

… From a technical perspective, the sense of seller’s remorse was a bit more palpable across the UST complex yesterday on further digestion of the Fed’s acknowledgement of the ‘fine-tuning’ policy phase. In the process, the 3.85% yield level rejection in UST 10s looks technically significant should it survive the weekly close, as was the rally in bonds through a short-term bear trend-line in place since the April 6th yield lows. Both indications mark potential double-top patterns from the May range highs. Similarly, both 5y and 7y yield benchmarks have traced out bullish 3-day trading patterns (indecision’ dojis followed by ‘inverted hammer’ candles) with daily RSI and stochastic momentum indices suggesting scope for bullish divergence (attached).

… and for some MORE of the news you can use » IGMs Press Picks for today (16 JUNE) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

First up on GROWTH > rates,

Barclays: More about growth than rates Hawkish central banks haven't move the needle for the equity market. With the bulk of rates hikes done, earnings is what matters now, and so far so good. Dislocation under the hood is a headache for investors. Value/Growth vs. rates relationship has broken, and Cyclicals look too high vs. PMI, albeit not vs. earnings.

But wait, that cannot ALWAYS be true … take for example, this on RATES — marching (somewhat)higher off of April’s lows into the debt ceiling drama DID bring out some buying

Goldilocks: TIC Data: Foreign Official Investors Net Purchase US Treasuries

Based on our valuation-adjusted estimates of preliminary data from the US Treasury, foreign investors net purchased long-term US securities again in April. In greater detail, foreign investors net purchased long-term US Treasuries, agency securities, and corporate bonds, while they net sold US equities. Official investors were responsible for a majority of the net inflows in April, driving net inflows into long-term Treasuries.

At the country-level, Japan was the largest net buyer of long-term Treasuries in April, while the UK was the largest net seller on our valuation-adjusted estimates…

That was THEN and this is now and as far as YESTERDAYS ReSALE TALES data goes, a few words from ‘our sponsors’

BMO: Retail Sales higher; Claims remain elevated FirstTRUST: Retail Sales Rose 0.3% in May GS: Retail Sales Edge Up in May; Manufacturing Surveys Above Expectations; Import Prices Decline; Initial Claims Remain Noisy

…Following today’s import price data, we raised our May core and headline PCE inflation estimates by 1bp each to +0.32% (mom) and +0.13%, corresponding to year-over-year rates of +4.64% and +3.87%, respectively…

Wells: Don't Let a Surprise Gain in Retail Sales Make You Lose Control

We get one of the fun economic statistics today. US Michigan consumer sentiment data offers the always humorous breakdown between Republicans and Democrats (sadly only for headline sentiment—a breakdown of inflation expectations is not provided). These two groups report that they are living in different economies. To be fair, regional divergence in the US has increased, but the sentiment split is mainly about partisan bias. Obviously, people say one thing in surveys and act totally differently in reality.

The Bank of Japan meeting decided on another month of masterful inactivity. The Bank of Japan is very good at masterful inactivity, having perfected the policy over many years. There is an expectation of a higher range for 10-year bond yields at some point, but the timing of that is being pushed later and later.

The Bank of England inflation expectations survey is due, ahead of the policy decision next week. Consumer inflation expectations are strongly influenced by high frequency purchases—and fuel prices have been coming down after the Competition Authority expressed interest in profit-led inflation in that area.

Markets are bombarded with ECB speakers after yesterday’s rate decision. The ECB policy auto-pilot light is still illuminated, though some economic warning lights are now also starting to flash red.

What does ALL this mean? Not much BUT … Well, one firm domiciled over in the UK with a rather large presence in / around CT offers,

The June FOMC clearly set a hawkish bias for higher rates in the next two quarters for the Fed. In addition, Powell elongated the duration of the tightening cycle by slowing the pace yet increasing the expected level of terminal rates, which caused markets to remove almost all the cuts priced for 2023 and reduce the number of cuts in 2024.

Given the most recent FOMC meeting and the ongoing resilience of the economy, we take a step back and re-evaluate our opinions on the Fed, the economy and inflation. In turn we re-evaluate our US rates views, reset our interest rate forecasts, and update our approach to the US rates market in the coming weeks and months. We still see weakness ahead for the economy and inflation, which would justify lower yields and steeper curves, but acknowledge that the road ahead can be choppy and the cost of holding those longs isn’t low.

… As Powell admitted, there is little clarity looking ahead. Indeed, their prior forecasts for the funds rate as projected in the dot plot does not have the best track record (Chart 2 following page).

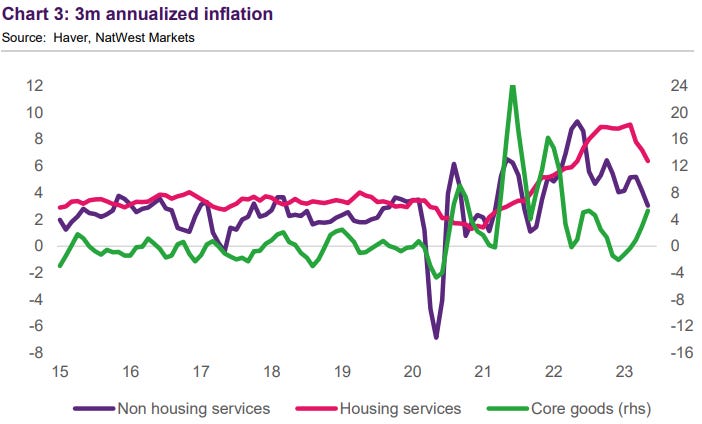

… The key here going forward will be inflation. Similarly, there are signs of slowing in inflation, with the 3m annualized rates both housing services and non-housing services (Chart 3 following page). Indeed, excluding the used cars component, the prior core CPI would have shown a +0.256% increase instead of +0.436%, and alternative data already suggest softening in used car prices, which is likely to be reflected in next CPI reports. Similarly, it is well known that most of the shelter measures in CPI (OER/rents) have significant lags to what goes in new rentals and the measure will likely continue showing a deceleration (core services ex rents, a measure preferred by Powell, has been at ~0.2% mom for the past 3 months).

… Putting all this together, despite riding the market roller-coaster over the last quarter, we will still approach the market with a buy-dips/bullish bias. Our current market bias is one where we favor the 3-5yr sector of the curve, with a steepening direction on the curve. However, given the shift in our approach, we will stop out of these views if the market prices in July fully and moves to pricing in better than even odds of a hike in in either September or November (our model puts this presently at 4.50% in 3yr notes - reminder our initial 3yr average entry was 4.45%)…

More over the weekend but … THAT is all for now. Off to the day job…