Good morning … that saying about how, IF you want less of something, you increase taxes and conversely, if you want MORE of something,

Reuters: Morning Bid: Beijing tries new ways to lift moribund markets The Times: China slashes share trading tax to boost market confidence ZeroHedge: Beijing Unleashes 'National Team' To Rescue Chinese Stocks

US equity futures are cheering (leaning marginally into the GREEN) for the moment while UK is closed for holiday, the waning hours of summertime clearly impacting markets and volumes are light, as one might expect. While this may persist early in the week, we’ll all be on much higher alert as the week comes to an end (shortly AFTER the NFP report Friday morning as the Hamptons Hedge goes into effect ahead of the 3d Labor Day weekend).

Before we get THERE we’ve got to deal with high / rising rates which, at the moment, persist without upsetting the equity apple cart — 5yy DAILY for example,

Momentum (stochastics, bottom panel) remain overSOLD and yet there’s no buying urgency evident. TIME at a price could resolve the momentum extreme. Zooming OUT a touch, and looking at a (log scaled)MONTHLY view,

… the longer term trend is clearly broken, momentum is overSOLD and yields are approaching what appears to be next significant ‘line in the sand’ up nearer 5.00%.

The pendulum ALWAYS swings further than you think reasonable and we’ll just continue to monitor data, Fedspeak and equity markets and for the moment, remember … Remain calm, all is well

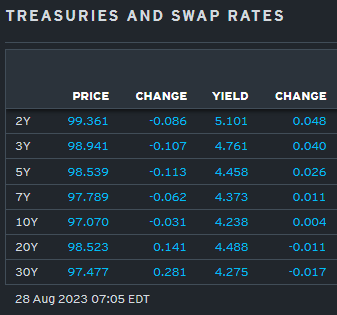

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are mixed with the curve pivoting flatter around little-changed intermediates ahead of back-back (and upsized) Treasury auctions in 2's and 5's. UK trading was closed today, DXY is UNCHD while front WTI futures are little-changed too. Asian stocks paced higher by Chinese shares after steps to support the markets were announced by Beijing (links above), EU share markets are all higher (SX5E +0.5%) while ES futures are showing +0.12% here at 6:40am. Our overnight US rates flows were unavailable while overnight volume was too with London out.

… This weekly chart of the Treasury 20+-year ETF, TLT's, shows TLT prices still near major support (91.85) derived from its move lows while medium-term (weekly, lower panel) momentum remains 'oversold' and looking ripe in set-up for a new momentum Buy signal. We spied a bullish trend reversal last week in 5-year Treasuries (Evening Star in yields) but 5yr yields remain pinned near their major range support area of 4.45%- so no joy there yet. One thought is that Tuesday's or Wednesday's post-Tsy-supply closes might offer further clues whether rates benchmarks will hold their major range supports or break up through- as 10yr real rates did a few weeks back. Either way, the thought that duration is 'too late to sell and too early to buy' resonates from a tactical perspective. So we're waiting and watching to see if our bond-friendly hunch (in)formed last week will get any traction off these major support levels...

From some of the news to some of THE VIEWS you might be able to use… here’s SOME MORE of what Global Wall St is sayin’ and these are in addition TOwhat were noted over the weekend…

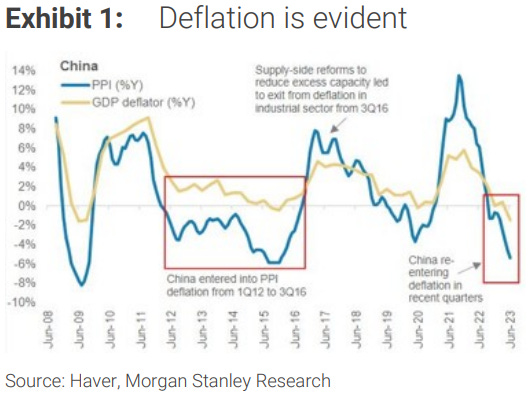

Goldilocks - China: Both Industrial profits and revenue declined sequentially in July (news out overnight … )

Bottom line: China's industrial profits and revenue contracted by 5.7% yoy and 1.1% yoy, respectively, in July, narrower than the -8.4% yoy and -2.7% yoy in June. In sequential terms, industrial profits fell 5.4% sa non-annualized in July (vs. +5.3% in June), and revenue fell 0.1% sa non-annualized (vs. -0.4% in June). Overall profit margins edged down in July with both upstream and downstream profit margins slightly lower on a 12-month average basis.

… Taken together, we expect foreign-born labor force growth to add 40k workers per month more than trend. This could add an incremental 500k workers over the next three quarters above trend levels and meaningfully dent the jobs-workers gap. Overall job growth is slowing but remains above our 75k/month estimate for the breakeven rate needed to stabilize the unemployment rate over the medium term. However, the foreign-born labor force rebound implies a breakeven rate as much as 50k/month higher.

MS - The Weekly Worldview: Eyes Still on China (forbetter or worse…and hey, we still HOPE for best export — DEFLATION — to help Fed, fiscal authorities — WIN battle ‘gainst the flation)

China's faltering growth is a key story right now. The global implications are different than at the beginning of the year.

… Now the world has changed, and Chinese growth has slumped with no recovery apparent so far. The global implications, however, are somewhat asymmetric. Because we are seeing the weakness show through to the industrial sector and especially capex spending, we cannot assume that the rest of the world will be as insulated as in the first quarter. Although we have recently marked down our view for Chinese economic growth, we still think a lost decade can be avoided. Nevertheless, with Chinese inflation turning negative, the prospect of China exporting disinflation is being discussed.

MS - Sunday Start | What's Next in Global Macro: AI: The Long and Short of It (speaking of DISINFLATION, but turning ones focus TO AI … a few words)

The topic of artificial intelligence (AI) is still top of mind in markets, in particular among equity investors, who have to sort the winners from the losers and decide how to trade the theme (see the Morgan Stanley AI Guidebook). The macro topics of employment, inflation, and interest rates are relevant to the theme as well. Over time, we will learn how AI gets deployed, in which industries, and over what time horizon the benefits are realized…

… But surely, across the various applications, there will be some net increase in meaningful and measurable productivity, allowing the economy to produce more at lower cost. The result eventually would be a disinflationary impulse. For now, the Fed is working on bringing inflation down through restrictive monetary policy—AI or not. And since the productivity gains will only play out over time, we can think about the period after the Fed has restored price stability. Will inflation fall back below target? Only until the Fed sees the disinflation happening, and then it will want to ease policy to take up the slack created by a more-productive economy.

While the disinflation from rising productivity should first lead to lower policy rates, over time, if productivity gains are large and sustained, we should actually see higher policy rates. The greater productivity is, the greater the incentive to invest. To keep the economy in equilibrium with rising productivity takes higher interest rates. And if the higher productivity growth is expected to last for some time, the higher rates should be reflected across the entire yield curve. Further, because the higher rates would be driven by fundamentals and not inflation, the entire real yield curve should rise. But, instead of seeing higher real rates as a negative for equities, faster productivity growth means that both earnings and real rates can rise in tandem—a shift in a correlation that many in markets have become used to.

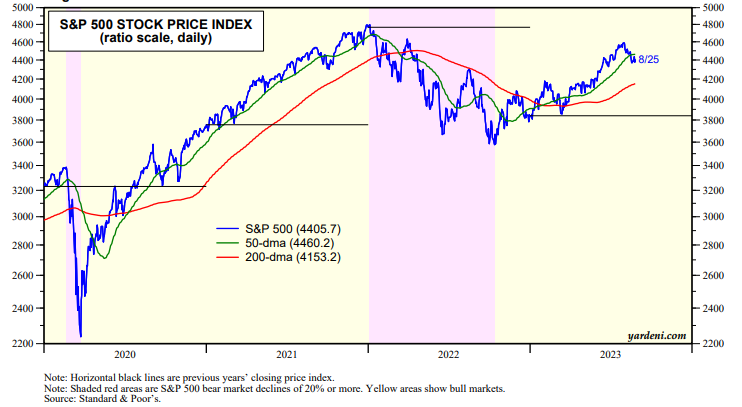

The S&P 500 has fluctuated around its 50-day moving average recently as the 10-year Treasury bond yield has done the same around 4.25%, which was last year's high on October 24 (chart). Sentiment is bearish in the bond market. It's less bullish in the stock market than it was during July.

Fed Chair Jerome Powell's Jackson Hole speech on Friday was hawkish. He avoided any mention of lowering interest rates. Instead, he said that the policy options were either high-for-longer or higher-for-longer interest rates. Interestingly the bond market didn't freak out but remained around 4.25% with the TIPS yield backing off a bit from 2.00% (chart). The stock market also didn't react much to Powell's hawkishness…

AND for those of us who are visual learners, a few last items

Bloomberg’s 5 things to know (ASIA — with EZ out, note visual still makes one feel like traders clinging to bets for rate CUTS)

Federal Reserve Chairman Jerome Powell resolutely kept the goalposts right where they were with his Jackson Hole speech. That leaves the bond market bracing for more volatility. Investors mostly look to be hanging on to their bets that the central bank’s tightening cycle will cause the US economy to crack all too soon, to spur policymakers to make the traditionally swift shift to rate cuts within half a year of calling a halt to hikes.

Swaps contracts did move to price in stronger odds for one more cash-rate increase this year, but further out they stuck with their estimation that the cash rate in a year’s time will be about 50 basis points lower than it will be six months from now. That’s a gap that’s been evident ever since the March banking crisis, even as the Fed kept raising and traders were forced to reverse their bets that the tightening cycle was done. At some stage, the tightening cycle will end, but things are set up for plenty of turmoil before that happens. There could be even greater volatility afterwards, though, because that is when those wagers on a rapid pivot are likely to face their greatest test.

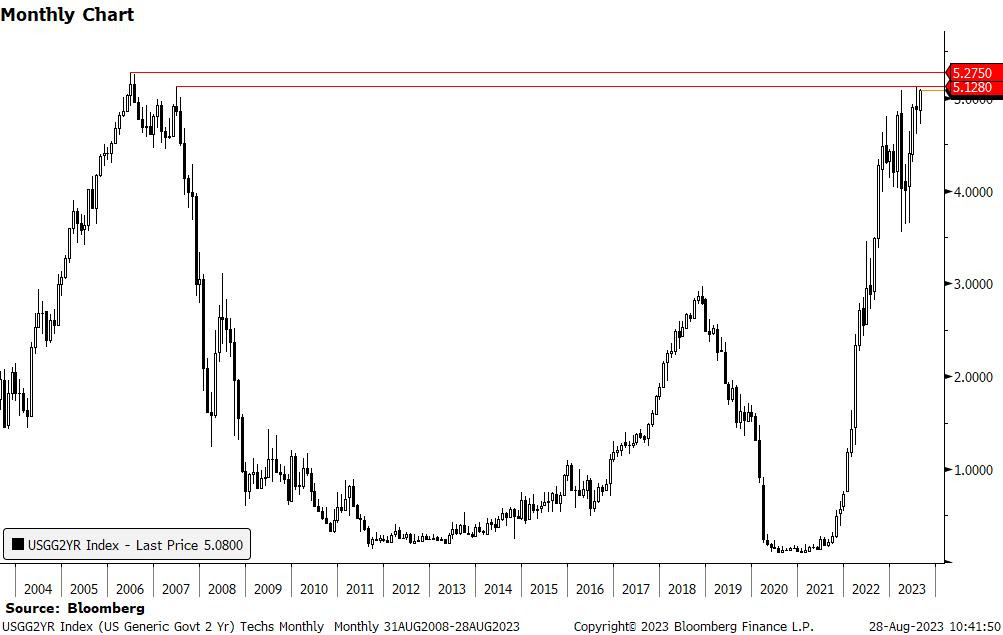

US 2y yields: Yields closed just shy of very strong resistance at 5.0801%-5.1280% (March 2023 high, 2023 high, 2007 high) on Friday. However, with no surprises at Jackson Hole, we are of the opinion that we are likely to see a break higher, with US 2y auctions today a potential catalyst.

Given the significance of the resistance level, however, we prefer to wait for a monthly close above to confirm a break. IF we do see this, then we think yields could continue higher, with subsequent resistance at 5.2750% (2006 high).

Animal house, The Jerk, Stripes, etc. They sure don't make comedies like they once did do they? But didn't have Jackass back then (or Dark Brandon!) so I guess it all balances out.

i was just citing a JERK reference this weekend and Thing 2 (20) and Thing 3 (14) looked at me with blank stares ... had NO idea who Steve Martin is. I'm doing it wrong ...

Animal house, The Jerk, Stripes, etc. They sure don't make comedies like they once did do they? But didn't have Jackass back then (or Dark Brandon!) so I guess it all balances out.

i was just citing a JERK reference this weekend and Thing 2 (20) and Thing 3 (14) looked at me with blank stares ... had NO idea who Steve Martin is. I'm doing it wrong ...