Good morning … what did I miss? This is just ONE thing … and THE most important to me — rates MOVES over past week or so nothing short of breathtaking …

U.S. long bond: full reversion scenario. Not a forecast.

It’s this sort of move I was referring to Wednesday HERE — March CHEAPS are now in rear view mirror and I’ll break out crayons and sharpener over the weekend BUT once stocks really start to embrace this AND rates / prices get (even MORE)oversold, and exactly NOBODY wants to buy USTs (duration supply heading our way — these current moves could very well be a concession for one of most unloved reFUNdings in recent memory?

Now this is NOT to say this is IT — the move is DONE — and for some context as to WHY prices have moved — well, economy doing less bad than forecast, the USAs credit rating was downgraded (“arbitrary” or not) and there is MORE issuance on the horizon. On THAT note,

… For the US the confusing thing is how much of the budget deficit increase of late is due to delayed tax receipts (due to winter storms) and how much is due to genuine stealth fiscal easing. It still feels like the former to me but that's not to say that the weak US fiscal situation isn't unparalleled in non-recessionary or non-crises times. Also there’s no denying that tax receipts are lower and interest costs higher at the moment so the increased issuance in the next few months is real. As such treasuries are making room for the extra supply. We’ll wait and see if it triggers any issues anywhere.

On a similar vein, back in March there were some who suggested that the straw that broke the camel's back in the SVB downfall was possibly the Powell hawkish testimony to Congress earlier that week. So can any of us say with any certainty that the last of the market shocks from higher rates are behind us?

… The renewed rates sell-off got an extra push with US data releases on the day that pointed to further resilience of the US labour market and upward price pressure in the US economy. In this context, it's put a laser focus on the market's favourite random number generator, namely payrolls later today. Our economists expect +175k (vs +200k expected by consensus), with the unemployment rate to remain steady at 3.6%. You can read their full preview here. …

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries mixed with the curve pivoting notably flatter (2s30s -5.5bp) around a little-changed 20yr point ahead of NFP. DXY is little changed while front WTI futures are +0.65% and nearing key range resistance near $82.36 again. Asian stocks were mixed/higher, EU and UK share markets are mixed while ES futures are showing +0.25% here at 6:45am. Our overnight US rates flows saw a dearth of curve stop-outs and some dip-buying in the long-end that have contributed to this morning's twist flatter in curve. Fast$ was also better seller in the belly/intermediates according to the desk. Overnight Treasury volume was about average across the curve…

… As for duration, our next attachment of Treasury 5yr yields shows how they're approaching support derived by their March move highs (4.37%) with daily momentum (lower panel) still guiding bearishly.

10's and 30's have already cleared their March move highs with Treasury 30yrs now inching closer to their November move highs near 4.34%, their presumed next-support. We'd expect pretty solid support for 30yrs between that 4.34% level and their move high from October at 4.42%...

… and for some MORE of the news you can use head TO Harkster (app HERE for example) AND Finviz too…

From some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ and think’ ‘bout …

Before jumping in TO the inbox, I’m going to skip ALL the NFP precaps and victory laps as anything offered over the weekend likely to have all the redrawn TLINES and newly minted narratives which take the day’s print into consideration.

That said,

ZH: July Jobs Preview: Hot Print Sends Yields Soaring, Puts September Hike In Play

AND as I go thru inbox — saving a few things I missed for weekend consumption, here are a few items which I think are worth sharing for consideration ahead of todays NFP …

(BFW) A $10 Million Options Play Targets 5-Year at 4.20% by Month End 2023-08-03 16:29:06.727 GMT

By Edward Bolingbroke (Bloomberg) -- One standout flow in Treasury options over Thursday’s US session has been the build-up of a bullish position in 5-year tenor targeting a yield drop to around 4.20% within three weeks. Premium paid so far is up to around $10 million for the upside play. * All session 25,000 Treasury September 106.75 calls bought at 27 ticks, says London trader * Strike price correlates to around 4.20% 5-year yields vs. current 4.29%; open interest in the strike sits at 11,629; suggests that activity Thursday has been a new position rather than a short cover * Five-year yields are cheaper by around 5bp on the day, topping through 4.31% in early session * Some information comes from rates traders familiar with the transactions, who asked not to be identified because they are not authorized to speak publicly

The larger-than-expected US Treasury issuance announcement have pushed US yields broadly higher, with the curve bear steepening. According to our MarFA™ Macro framework, US rates now look oversold by about 26bp (2.6 z-scores), 25bp (2.5 z-scores) and 21bp (2.1 z-scores) for the 30y, 20y and 10y USD swap tenors. The 10y UST bond also looks oversold by about 23bp (2.2 z-scores).

Going into August, which typically sees rates rally due to seasonal factors and following an extended rates sell-off, we favour adding a tactical long UST 10y position, targeting 3.92%.

We also acknowledge near-term risks in the coming weeks such as NFP data (this Friday), CPI (next Wednesday) and the US Treasury 10y and 30y auctions (next Wednesday and Thursday, respectively) as potential catalysts for further upside in US yields.

For the next 17 months, the US government can comfortably make payments as the Congressional agreement suspends its borrowing constraint until January 2025. The real question is whether the market can absorb such heavy issuance without spurring a surge in yields, and with it the government’s funding cost.

… For the next 17 months, the US government can comfortably make payments as the Congressional agreement suspends its borrowing constraint until January 2025. The real question is whether the market can absorb such heavy issuance without spurring a surge in yields, and with it the government’s funding cost. There are reasons to think that existing demand for US treasuries will be enough to maintain an orderly market:

If the government debt is funded by issuing T-bills, the liquidity sitting in the Fed’s reverse repo facility and commercial bank deposits will help anchor yields. Some US$2.07trn sits in the Fed’s RRP facility and the Fed is paying interest on reserve balances at 5.4%. If new issuance causes T-bill yields to rise much above 5.4%, US money market funds will tend to move money they have parked at the Fed out to buy US T-bills. The same thing could happen to commercial bank deposits, as deposit rates are lower than interest on reserves and T-bill yields. Therefore, there is likely to be enough liquidity at the short end of the curve to meet the coming supply.

If the government chooses to raise funds using longer-dated treasuries, investors should buy them. On a risk- adjusted basis, the real yield offered by US treasuries is attractive relative to the return earned by the average US firm (the economy-wide corporate return on invested capital) and the equity earnings yield. This situation will tend to put downward pressure on long-term treasury yields, especially if concerns about US economic growth again come to weigh on investor sentiment (see Buy Or Fade The US Equity Rally?). In the view of Will Denyer and I, there is a high chance such a shift will occur due to the lagged effect of higher interest rates impacting demand (see It Is Too Soon To Call A Soft Landing).

Looking ahead, Fitch’s concern about a fiscal deterioration in the next three years will likely come to pass. Using Gavekal’s trusty “four quadrants” framework to think about future scenarios, US budget deficits should widen in the two most likely outcomes, namely an inflationary boom (as expected by Louis Gave and Anatole Kaletsky) and a disinflationary bust (as still expected by Will and I). When the government receives less and spends more, less is taken away from the private sector and more is spent on goods and services supplied by firms. This aids business profits in the near term (see War, Recession And… Today). However, further deficit widening will raise long-term debt sustainability concerns if no fiscal action is taken (see The Three Prices: An Update On US Treasury Yields).

Still, none of this is likely to affect the status of US treasuries as a “risk-free” asset in the near term, however oxymoronic that may sound.

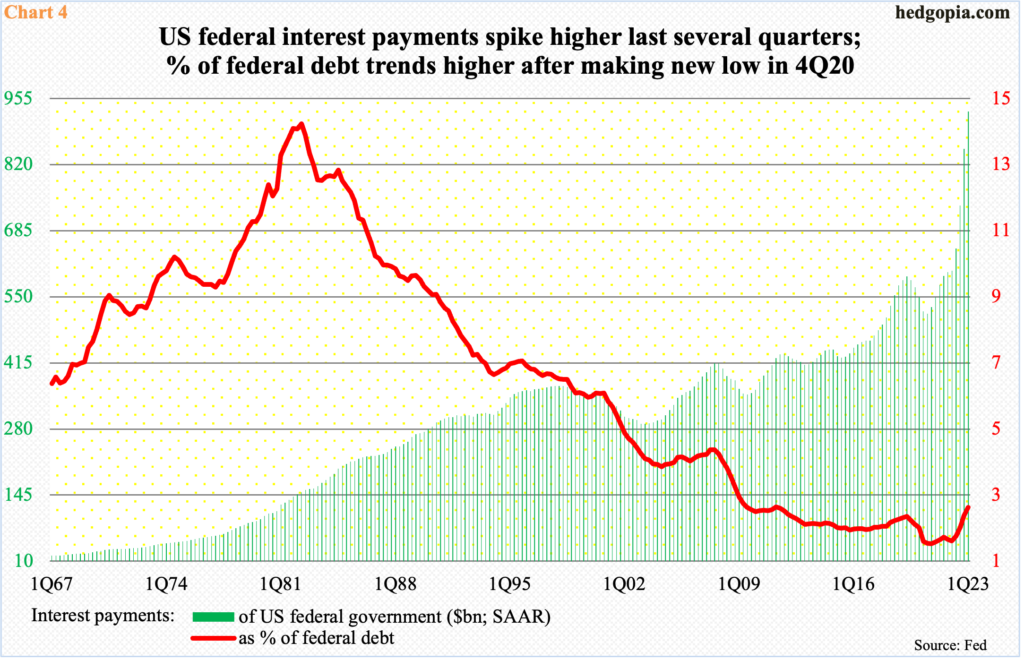

Hedgopia: Rates, Budget Deficit, Treasury Debt Issuance And Federal Interest Payments – All Rising

Interest rates on both the short and long end have gone up meaningfully. The federal government sits on nearly $33 trillion in debt, and the budget deficit is on the rise even though the economy is growing. This only means persistently rising interest payments.

… Rates have now risen to potentially matter. In the March quarter, annualized federal interest payments were $928.9 billion; six quarters before that, they were under $600 billion. In the March quarter, payments as a percent of debt, which can be treated as effective interest rate, comprised three percent, up from 1.9 percent in 4Q20 (Chart 4).

Rising rates in combination with rising budget deficit and rising issuance of debt can prove to be ill-fated. It is too soon to say if the chicken has come home to roost, but it is also the truth that the current fiscal trajectory is not headed in the direction and will only deteriorate, making the system more prone to shocks.

ZeroHEDGE: Usage Of Fed's Emergency Bailout Facility Hits New High; Money-Market Inflows Continue

US Money Market funds saw a third straight week of inflows ($29 billion this past week) to a new record high of $5.15 trillion...

AND here are some charts which I missed AND which, in context and benefit of hindsight may still be instructive,

AllStarCharts: Will Rising Rates Lead to a Stock Market Bloodbath?

It’s no longer a matter of whether rates will fall later this year. It’s now more a question of how fast they will rise.

A sharp increase in yields would no doubt apply pressure to growth sectors and, by extension, the major US indexes. We’re already witnessing a correction as the Nasdaq 100 has retreated roughly 3.5% over the past two weeks.

But it’s essential to put the current state of the markets into perspective.

The long-duration bond ETF $TLT is printing fresh 9-month lows just weeks after the tech sector ETF $XLK posted a new all-time high.

XLK carved out a significant bottom the last time TLT traded at these levels – quite a different picture from today.

The chart highlights the central relationship between stocks and bonds. Equities have ripped higher in an environment where interest rates have chopped sideways.

10yr US Bond Yields have surged higher following the surprise ratings downgrade in the US for a clear break to new highs for the year above 4.085% and we look for a retest of long-term support at a cluster of levels at 4.27/4.405%, including the 2022 yield high. Whilst we would look for an attempt to hold 4.405%, a closing break higher would be seen to clear the way for a further rise in yields to 4.50%, then 4.72%.

Of further and even more concern are 10yr US Real Yields, as if a sustained move above the key 1.82% high of 2022 were to be seen this would be seen to mark a large and worrying bearish continuation pattern to warn of a more sustained move higher in Real Yields and “risky” assets more generally…

…and we already look for the S&P 500 to correct lower with daily and weekly momentum divergences now in place and we see scope for a potential fall now towards support at 4,325/4,302…

…with the VIX also seen on the cusp of confirming a “double bottom” base.

Tactical indicators also point to a correction lower, with the percentage of S&P 500 stocks above their medium-term average having moved to an overbought condition and with “retail” sentiment having been seen to rise to what we see as a “typical” extreme.

Nasdaq 100 has also been capped at key price resistance and we look for a break of the uptrend from March and a correction lower.

Please note the House View has US Equities as least preferred on a 12-month horizon.

Both US High Yield and Investment Grade credit spreads have held major areas of resistance and we look for the near-term risk to turn wider.

…Chart of the Day: 10yr US Bond Yields have surged higher post the surprise US ratings downgradefor a move to a clear new high for the year and we look for a retest of long-term support in the broad 4.27%/4.405% zone – the 2022 yield high, the 78.6% retracement of the 2007/2020 yield fall and the “neckline” to the 2006/2007 yield top. Whilst we would look for an attempt to hold below the upper end of this range, underlying momentum is seen strong and a direct break and weekly closing break above 4.405% would suggest the yield rise can extend further with next support seen at 4.495/4.505%, through which can see support next at 4.72%.

US 10yr Real Yields have similarly surged higher but for now remain capped at their YTD and 2022 yield highs at 1.82/1.825%. A weekly close above here is needed to see the broader range resolved higher to warn of a further significant rise in yields

US 30yr Bond Yields are see on course to test long-term support at 4.42/4.46%.

… Whilst we would look for fresh buyers to show at 4.42/4.46%, should weakness directly extend and a weekly closing break higher be seen this would suggest we can see a further rise in yields to test the series of yield highs posted in 2008, 2009, 2010 and 2011 at 4.80/4.86%.

Resistance is seen at 4.21% initially, the 4.15%, which we look to try and hold. Below 4.085% though is needed to ease the threat of a further sell-off, clearing the way for a recovery back to resistance next at 4.00/3.985%.

The 2s10s US bond curve has steepened sharply, but with a close above -74bps seen needed to clear the way for a move back to the -41.5/-39.5bps highs….

Finally something(s) I TWEETED while traveling for work yesterday.

I have been surprised how low US long-term rates have remained in light of structural changes that are likely to lead to higher levels of long-term inflation including de-globalization, higher defense costs, the energy transition, growing entitlements, and the greater bargaining power of workers. As a result, I would be very surprised if we don’t find ourselves in a world with persistent ~3% inflation. From a supply/demand perspective, long-term Treasurys (T) also look overbought. With $32 trillion of debt and large deficits as far as the eye can see and higher refi rates, an increasing supply of T is assured. When you couple new issuance with QT, it is hard to imagine how the market absorbs such a large increase in supply without materially higher rates. I have also been puzzled as to why the

hasn’t been financing our government in the longer part of the curve in light of materially lower long-term rates. This does not look like prudent term management in my opinion. Then consider China’s (and other countries’) desire to decouple financially from the US, YCC ending in Japan increasing the relative appeal of Yen bonds vs. T for the largest foreign owner of T, and growing concerns about US governance, fiscal responsibility, and political divisiveness recently referenced in Fitch’s downgrade. So if long-term inflation is 3% instead of 2% and history holds, then we could see the 30-year T yield = 3% + 0.5% (the real rate) + 2% (term premium) or 5.5%, and it can happen soon. There are many times in history where the bond market reprices the long end of the curve in a matter of weeks, and this seems like one of those times. That’s why we are short in size the 30-year T — first as a hedge on the impact of higher LT rates on stocks, and second because we believe it is a high probability standalone bet. There are few macro investments that still offer reasonably probable asymmetric payoffs and this is one of them. The best hedges are the ones you would invest in anyway even if you didn’t need the hedge. This fits that bill, and also I think we need the hedge.

And I then offered some VISUAL CONTEXT from a different angle,

Kimble: Breakout By 10-Year Yields Suggesting Upside Target of 6% Yields?

Interest rates remain in the spotlight with investors watching every economic data release and wondering when the Federal Reserve will stop raising rates.

Well, one way to gauge this environment is to watch the 10-Year US Treasury bond yield. And as you guessed, it’s been heading higher for a while now.

And today’s long-term “quarterly” chart highlights ahistoric Fibonacci breakout resistance level at (1).

The 10-year yield is testing the 23% Fibonacci retracement level right now. This is a HUGE test for yields continues.

And should the 10-year breakout and close the quarter above (1) it would open up the potential for yields to move to the next Fibonacci target around 6%. There’s a lot at stake here for consumers and bond traders! Stay tuned!

Hope to have time and somewhat MORE over the weekend as the data dust settles and NEW narratives are formed but … THAT is all for now. Off to the day job…

Didn't the BoE have to kneecap their 10 yr at 4% back in Oct, to otherwise prevent a continued yield spike and potential pension meltdowns? Extra-awesome charts, especially the Long-Term ones. As a CA employee nearing accelerated retirement (my mind and body can't handle the ever-tightening screws of working for WOKELAND much longer), I have the utmost faith in CalPERS, I'm sure nothing like that could happen out here. *sarcasm* Actually I do apologize for I'm sure we're at the top of Brandon's future bailout priorities. I was a different person in 1990 when I got my Gov job. Now I'd like to find my side-hustle niche post Gov retirement. Or I'll go be a $18 an hr min wage employee at my local ACE Hardware. I really don't know jack about home repair so may as well learn something useful & get paid too, right? Sorry to babble, I return to work for my last 11 months Sunday, to (semi) retire at the ripe old age of 53. I'm taking the $$$ and running. I do apologize. I tip my hat to all you all who make a real living out there in the market SharkTank. Hell of a ride ain't it! About time to Ramble On I'd say! Thanks!

Ps-If you're ever in the Sacramento area in the next 11 months I'd love to buy you a drink Steve. Or better yet, partake in sharing a pre-rolled with you :)! About a yr from now that offer stands, but up in Reno. I'm retreating to the Eastern Sierras to turtle up for my last stand. And try and ski my brains out. I've at least gotta land the 360 before I'm too brittle! Thanks again everyone!

Didn't the BoE have to kneecap their 10 yr at 4% back in Oct, to otherwise prevent a continued yield spike and potential pension meltdowns? Extra-awesome charts, especially the Long-Term ones. As a CA employee nearing accelerated retirement (my mind and body can't handle the ever-tightening screws of working for WOKELAND much longer), I have the utmost faith in CalPERS, I'm sure nothing like that could happen out here. *sarcasm* Actually I do apologize for I'm sure we're at the top of Brandon's future bailout priorities. I was a different person in 1990 when I got my Gov job. Now I'd like to find my side-hustle niche post Gov retirement. Or I'll go be a $18 an hr min wage employee at my local ACE Hardware. I really don't know jack about home repair so may as well learn something useful & get paid too, right? Sorry to babble, I return to work for my last 11 months Sunday, to (semi) retire at the ripe old age of 53. I'm taking the $$$ and running. I do apologize. I tip my hat to all you all who make a real living out there in the market SharkTank. Hell of a ride ain't it! About time to Ramble On I'd say! Thanks!

Ps-If you're ever in the Sacramento area in the next 11 months I'd love to buy you a drink Steve. Or better yet, partake in sharing a pre-rolled with you :)! About a yr from now that offer stands, but up in Reno. I'm retreating to the Eastern Sierras to turtle up for my last stand. And try and ski my brains out. I've at least gotta land the 360 before I'm too brittle! Thanks again everyone!