Marc doesn’t touch on FDIC and BBG story which I think is of yuuuge importance and so, another day another shocking / NOT shocking development from central planners,

ZH: US Studies How To Guarantee All $18 Trillion In US Bank Deposits

HEREis the BBG story cited in ZH and here’s updated visual of 10yy with TLINE touched and momentum crossing BEARISHLY now,

AND similar story exists on 20yy which IS up for auction today,

… here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower and the curve is flatter as risk-on conditions (SX7E +4.8%) dominated overnight. DXY is little changed while front WTI futures are higher (+1.1%), Asian stocks were higher (Japan out on holiday), EU and UK share markets are all in the green (SX5E +1.7%) while ES futures are showing +0.6% here at 7am. Our overnight US rates flows saw thin and listless dealings with Japan out with London's activity mixed and largely concentrated in the front-end. Later on, some real$ selling emerged in intermediates as the curve flattened while going into the NY crossover some back-end buying emerged. Overnight Treasury volume was ~40% of the recently elevated average volume.

… and for some MORE of the news you can use » IGMs Press Picks for today (21 MAR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

We think the case for EURUSD appreciation remains intact. We favour owning topside convexity. We stay bullish JPY spot and vol and positioned accordingly.

We see less scope for a rally in core European rates markets than we do in other regions.

Risks of a pause from the FOMC are high, but predicated on stabilisation of financial markets, we still expect a 25bp hike this week.

Developed economies have had three waves of inflation since the pandemic: transitory inflation for durable goods; commodity inflation; and finally profit margin-led inflation.

Profit margin-led inflation is not caused by a supply-demand imbalance. Profit margin-led inflation is when some companies spin a story that convinces customers that price increases are "fair," when in fact they disguise profit margin expansion.

Technically, companies are able to use stories to reduce their customer's price elasticity of demand.

Raising rates to reduce demand will eventually squeeze profit margin-led inflation, but it is a crude and unnecessarily destructive policy approach. Convincing consumers not to passively accept the price increases is a potentially faster and less destructive way of reversing profit margin-led inflation. Social media might have a role to play in this process.

… The leap up in US retailers’ profits as a share of GDP is exactly what is expected in a profit-margin inflation episode. For over a decade, pricing power was moderate, and the amount of profit retailers took was fairly steady. But in the second quarter of 2021, as the economy reopened, US retailers were able to persuade consumers to accept far higher prices. At the same time, retailers were able to keep down wage costs, and so profit margins exploded.

ln as far as the Fed goes, a large German bank offers a,

We offer reflections on this week's FOMC meeting and related client questions in the form of Q&A. To summarize, the Fed will hike 25bp, the SEP will be released as planned, a pause in rate hikes would not be accompanied by a pause in QT, the new Bank Term Funding Program is not QE, and our bias remains towards a steeper curve this year on recession and Fed rate cuts.

… Regardless of outcome, this meeting will be the biggest surprise vs. expectations this cycle (Figure 1).

Continuing on from this very same operation BUT a different desk, the early morning MONTHLY reid CHARTS,

Last Thursday (March 16th) marked the first anniversary of the Fed’s hiking cycle and this week's FOMC will help determine if they continue hiking into year two. On the eve of that first hike a year ago, markets were expecting Fed Funds to be just under 2% at this point, which itself was well above the 0.9% expected at the start of 2022. As we show in this chart book, the 450bps hikes so far is comfortably the most aggressive first year since the 1980 cycle. Only that and the 1973 cycle have been more aggressive in year one.

In this chart book we look at a variety of financial and economic indicators to show how they've been impacted by this year-long hiking cycle and compare their path to previous hiking cycles.

Of all the hiking cycles of the last 70yrs, this one has seen the weakest US growth, one of the largest declines in US housing and manufacturing activity, the worst S&P 500 performance, and one of the most inverted yield curves. After the recent banking crisis, 10 and 2yr yield moves are now around average at this point. Market based financial conditions are now tighter than where they were a year ago even though pre-SVB, less than 2 weeks ago, they were close to the loosest they'd been over the last 12 months.

We point out how something always breaks in a Fed hiking cycle and this cycle is starting to prove this assumption correct. As we articulated in last month's chart book, we are now"Waiting for the Lag" of one of the most aggressive first year hiking cycles in history. We're starting to see the financial market impact, with a high risk that this will confirm our long-standing US recession forecast for H2 2023. History suggests we should fasten our seatbelts in year two, whether the Fed keep hiking or not.

… We have seen big moves over the last 12 months….. And last 2 weeks!!

… The Fed’s tightening is having an impact… after surging during the pandemic, we’ve now seen the money supply begin to contract again, which never happened during the 1970s

And finally, from the firms Ivory Tower unit … those with more letters after their name than I’ve got in mine,

(Credit) Crunching the numbers: A bank lending shock and recession risks

Recent events have triggered a deluge of questions about how a shock to bank lending could impact the economic outlook. In this piece, we attempt to quantify the potential impact of a tightening in bank lending conditions on the economic outlook.

In past work, we have emphasized that measures of financial conditions should account for more than just high-frequency asset price movements. In particular, we have shown that our broad FCI, which includes measures of bank lending conditions and perceptions of credit conditions, is more highly correlated with future growth developments (see “5.1% is necessary, but is it ‘sufficiently restrictive’?”). These metrics had also tightened more significantly into this year, raising the prospect of a recession.

Given the significant uncertainty about how events will evolve and how sustained any tightening of financial conditions will ultimately be, we consider a few scenarios. A more modest tightening of bank lending conditions could subtract roughly 0.5pp from growth in the coming quarters, while a shock that pushes bank lending conditions towards historical tightness could easily subtract more than one percentage point.

Either way, we see the potential for this shock to be associated with a broader tightening of financial conditions that will meaningfully slow growth at a time when recession risks were already elevated. As a result, recent events strengthen our conviction that a recession remains the most likely outcome for the economy over the next year.

Moving along thru the inbox full of narratives AND THIS from GUGG,

It is never a good time for a bank run, but it is an especially bad time when the Federal Reserve is fighting inflation. While it’s true that Silicon Valley Bank (SVB) was an outlier in terms of the mismatch between its highly run-prone funding base and longer-duration asset composition, a close look at trends among FDIC-insured banks over the past 15 years shows that what happened at SVB is indicative of a system-wide phenomenon. With this context, we can see that the easing of terms on the Fed’s discount window and the creation of a new Bank Term Funding Program (BTFP) were not just a forceful response to the SVB bank run, but also a way to address possible similar scenarios that may play out across the banking system. Meanwhile, the weekend news of UBS’s takeover of Credit Suisse and the announcement of daily auctions through the Fed’s dollar swap lines with foreign central banks should help to calm fears of a wider global conflagration. We expect to see a lot of volatility in and around the next several Federal Open Market Committee meetings—we expect another quarter point hike this week—and are also looking further down the road to the debt limit battle that looms this summer. That’s because when it is resolved Treasury will need to issue hundreds of billions of dollars in T-bills to replenish its depleted cash balance. As all of this plays out, investors will be well served by being appropriately vigilant in their security selection, duration positioning, and asset allocation decisions.

FDIC story then justified? All this is funny ‘til it’s NOT funny.

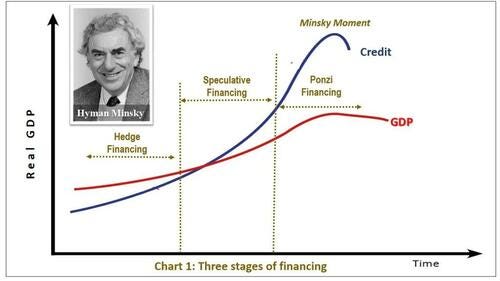

Speaking of NOT FUNNY … JPMs Kolanovic,

ZH: Kolanovic Sees Growing Odds Of A "Minsky Moment In Markets"

… Enter Marko Kolanovic again, who in his latest note not only quotes Lenin (the infamous "There are-decades where nothing happens; and there are weeks where decades happen” which pops out like clockwork every time the FRA-OIS spread hits 50bps), but - having completely forgotten about his 0DTE doomsday thesis from just 4 weeks back - has now escalated the doom and gloom rhetoric to conclude that virtually everything that is now happening is bearish and that "the possibility of a Minsky moment in markets and geopolitics has increased."

Translation: having tried to pinpoint the market's weakest link one month ago - and failing - and having had nothing at all to say about what would have a fare more devastating impact on market psychology and the economy, the cascading failure of major banks (as described here weeks ago), Marko is now just shotgunning it and hoping that something sticks to the wall, so that he can then point to it and say: "look, I was right." Here is the choice excerpt from his latest note:

A lot has happened in the past week. The bailout of several US banks did not manage to calm markets, which consumed another large bank in Europe. In a Trichet-like moment, the ECB increased rates by 50bps. The Fed is facing a difficult task on Wednesday, but it is likely already past the point of no return – a soft landing now looks unlikely, with the airplane in a tailspin (lack of market confidence) and engines about to turn off (bank lending). China brokered a Middle East deal, and there is a presidential visit to Russia this week. “There are decades where nothing happens; and there are weeks where decades happen”— Lenin.

The possibility of a Minsky moment in markets and geopolitics has increased. Even if central bankers successfully contain contagion, credit conditions look set to tighten more rapidly because of pressure from both markets and regulators. We stay neutral duration in the US and Europe amid cross-winds, favoring 10s/30s steepeners as an asymmetric way to position for an eventual Fed pause.

Cracks are beginning to emerge in US credit fundamentals, and Euro credit spreads will likely continue to widen unless we see meaningful policy intervention. The historical template for FX during widening credit spreads is for USD strength, coupled with relative safe-FX (USD, CHF, JPY) strength vs. highbeta. We see little change in oil fundamentals and keep our price forecasts unchanged for now, while financial stress and macro uncertainty have boosted safe haven demand for gold and silver.

There is a famous saying about a broken clock that is right twice a day... and yet, when it comes to Marko's track record the past two years don't even show that: starting in January for all of 2022, the JPM strategist was telling clients to buy the dip, yet every time a new and bigger dip emerged. Marko then flip-flopped in late September, and turned bullish which as we said at the time, marked the market bottom...

In as far as the bond market volatility, I’m told it’s been stunning on the front-lines and taking a step back, Bloomberg notes,

… Markets look a lot calmer as Tuesday gets going in Asia, but investors will be on the lookout for any fresh signs of further shocks. The moves that ripped across markets over the past week or so have few precedents, and the ones that do exist simply heighten the sense that things have reached a breaking point or 10.

Just look at the readings from the so-called fear gauge for the Treasuries market — ICE’s BofA MOVE Index of implied volatility. It touched levels only previously seen in the lead-up to the 2008 crisis and during the actual meltdown, and in 1998 during the collapse of Long-Term Capital Management. The Federal Reserve’s hiking cycle is obviously playing a role in helping to send Treasuries jumping around all over the place. Whatever the central bank decides on interest rates, investors will be hoping it can craft a message that manages to avoid setting off further turmoil.

What do do / think / say ‘bout it all? Well, a desk at a large British operation sums it up,

Don't be a hero Wild swings in bond markets, weekend bank rescues, and a Fed meeting all make for a volatile week, despite the CS merger announcement yesterday. While we feel the bond rally is excessive, for the first time ever in the GMT, we recommend staying in cash until more clarity emerges.

AND a live look in at global central planners ahead of whatever they are cookin’ up this coming weekend …

REMINDER — no update tomorrow due to travels. Should you desire a refund, please reach out to our refund department and otherwise, I’ll say thanks in advance for your patience.… THAT is all for now. Off to the day job…

Even by your high standards that was an epic note. Safe travels man!