(USTs are lower / flatter on light volumes given May Day holiday closing much of EZ)while WE slept; biz cycle in 15 charts (OR just one); sell in May...

Good morning … Is THISthe end OR just the end of the beginning?

Dunno BUT I’m moving along and noting a MONTHLY look at 10yy looks POSITIVE (ie LOWER yields),

Monthly momentum (stochastics, bottom panel) remain in a clear downtrend and we’re at / breaking a TLINE (albeit only a couple of data points) as we triangulate … and thiis is where / how we begin the month of May …

… here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower and curve flatter amid the May Day holidays and after an embattled US bank was seized and sold to a banking giant over the weekend. DXY is higher (+0.17%) and front WTI futures are lower (-2.15%). Asian stocks that were open mostly rallied (NKY +0.92%), European exchanges were closed while ES futures are showing UNCHD here at 7am. Our overnight US rates flows were unavailable and overnight Treasury volume was ~50% of average amid the holiday closures.

… and for some MORE of the news you can use » IGMs Press Picks for today (2 APR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

First up, Goldilocks on debt limit with a most funtertaining look at cost of insuring against a US default …

… Some corners of the financial market have begun to reflect debt limit-related risks. The Treasury bills curve appears to imply risk of disruption in June, July, and October. However, implied equity volatility shows little debt limit effect. This may change once the Treasury announces a specific deadline for Congress to raise the debt limit.

While we expect markets to reflect greater debt limit risk as the deadline nears, we do not expect the Treasury to be forced to delay any scheduled payments. Our base case for resolution of the debt limit is that Congress will raise it on the day of the deadline, plus or minus one day. There is clearly a chance that Congress fails to raise the debt limit by the deadline and some payments are delayed, but if this occurs we would expect a lapse to be brief given the potential political consequences of a longer standoff.

Ultimately, we expect the debt limit to be resolved through a deal that pushes the next debt limit deadline into 2025 and caps discretionary spending. However, the spending restraint from these caps would likely be more modest than the recent House-passed bill.

I’m sure it’s nothing … Moving right along to a more WORDLY view from the top MSs econ dept, Seth Carpenter,

Ahead of next week's FOMC meeting, market pricing is in line with our view of a 25bp hike, but getting the communication right will be tricky.

… While banking conditions have stabilized since the March meeting, the implication of tighter credit conditions is still uncertain. Powell will likely reiterate that the banking turmoil tightens credit conditions, with an implication that the Fed can hike less than it would otherwise. But the tightening does not fundamentally change the outlook. I am of the view that there is downside risk of a sharper contraction because of tighter credit conditions, but with a bit of luck the fall in demand for loans as the economy slows will be close enough to the tightening supply to leave the door open for a soft landing.

The eye of a storm is surrounded by the eyewall, the most powerful and unpredictable part. Now that the eye potentially has passed, markets may still face turbulence. Hold tight to safe havens, including US Treasuries and the USD.

… We maintain UST 2s30s steepeners, 5s30s steepeners, and long 5y UST outright

Finally, a few words on equities … First, from one of the more popular stock jockey’s out there … MSs Mike Wilson,

Investors' belief in a 2H EPS recovery is growing amid a stronger than expected reporting season. Meanwhile, the recent leading macro data have slowed further. We recommend owning high operational efficiency and earnings stability stories and offer related screens in today's note.

And then another few words from a rather large British shop,

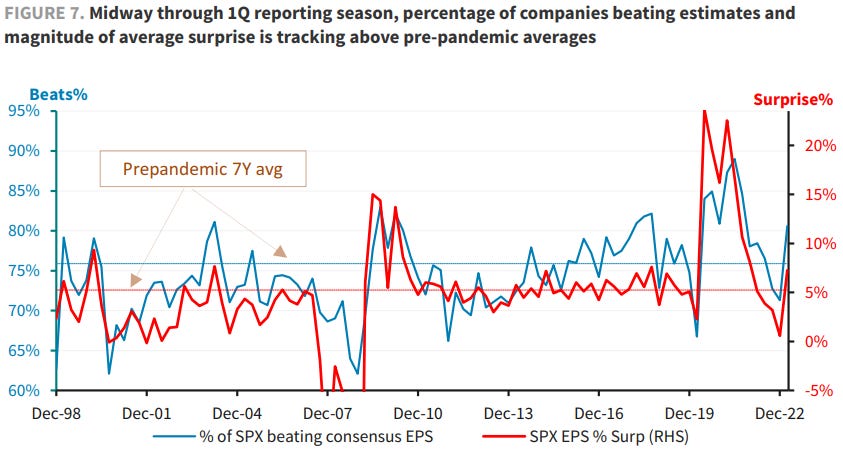

Midway through 1Q earnings, it seems negative revisions for the current quarter overshot the mark. Breadth and depth of surprise has improved sequentially but are being delivered against a very low bar, and margin pressures remain front and center. Beat-and-raises from mega-cap Internet are underpinning SPX forward EPS.

A final work on STOCKS for those who like to visualize data and are of the mindset one has to sell in may,

This adage is based on the observation that the best six months for the stock market has historically been November through April.

So how significant is the variance in performance between the best six and worst six calendar months?

Very.

The following chart illustrates the performance of the S&P 500 during the calendar months of November through April (orange line) and the performance of the S&P 500 during the calendar months of May through October (blue line).

The difference in performance is noteworthy.

With significant headwinds (e.g., relatively high inflation / interest rates, war, economic concerns, etc.), there is now an added headwind — seasonality.

Finally, a couple macro tourist links / visuals to keep in mind. First up from Raoul Pal,

Raoul Paul, interesting dude who put ALL of his money (his words) into Crypto at the peak of that bubble, all so he could learn how crypto "trades" (his words). If only Keith @Hedyeye could've told the audience that Raoul was "full of shit" in the moment, rather than a yr later. Crypto had TOO many similarities to dot.com bubble for my taste. Anyone else remember Pets.com?!? Or was it Chewy.com LOL!

Raoul Paul, interesting dude who put ALL of his money (his words) into Crypto at the peak of that bubble, all so he could learn how crypto "trades" (his words). If only Keith @Hedyeye could've told the audience that Raoul was "full of shit" in the moment, rather than a yr later. Crypto had TOO many similarities to dot.com bubble for my taste. Anyone else remember Pets.com?!? Or was it Chewy.com LOL!

I give Pal lotta credit ... throwing lotta stuff up against wall and willing to take hit ... but most def agree with regards TO bitc