As we cycle forward and are entering today we’re now UP 25bps on the day after being down 100bps. 3 steps forward and a step back,

NOTE — momentum (stochastics, bottom panel) has crossed bearishly SO some further upside for 2yy would / could very well be a pause that refreshes. CPI up shortly will help shape price action (and narratives, then, to follow).

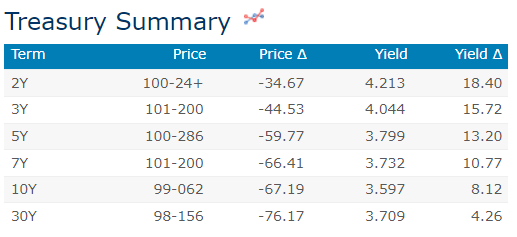

… here is a snapshot OF USTs as of 708a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are lower and the curve has bear flattened ahead of CPI this morning. DXY is higher (+0.2%) and front WTI futures are lower (-2.1%). Asian stocks were all lower (Japan and Korea leading down), EU and UK share markets are mixed/higher while ES futures are showing +0.6% here at 7:22am. Our overnight US rates flows saw a 1-way bear flattening early in Asian hours before a sharp reversal to bull steepening into the London crossover. Our flows saw better real$ buying in the long-end amid fragile liquidity conditions and explosive volumes (5-6x ave). Once into London hours and the bull steepening reversed with better selling at the 5y point from real$. Later amid some position-squaring some selling in the 10y-20y sector was noted with real$ the dominant players during London's AM hours. Overnight Treasury volume looks about 175% of average with 5yrs (230%) seeing the highest relative average turnover this morning.

… and for some MORE of the news you can use » IGMs Press Picks for today (14 MAR) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some VIEWS you might be able to use. Global Wall St SAYS:

Financial markets were waiting for today’s US consumer price inflation data with unseemly enthusiasm, but now have become completely distracted by last week’s bank failures. In the real world, the cost of living (for which consumer price inflation is a very poor proxy) probably matters more to people.

Will bank runs impact future inflation? They could. Aside from the fictional housing price data and energy prices, US inflation is mainly about profit margin expansion. That reverses if consumers stop believing price increases are fair, or if consumer demand falls. If banks tighten lending standards, the loss of credit will reduce consumer demand. After such a long period of catastrophically negative real wages, US consumers have used credit card borrowing to maintain living standards. Higher interest rates do little to deter this borrowing. Tighter lending standards stop it abruptly…

While Paul makes a very interesting point about what MAY happen, an early morning REID through is feeling quit confident of what is forecasted to happen,

… Overall, I came out of yesterday even more convinced of our long-standing H2 2023 US hard landing view but with absolutely no idea at the moment what the Fed and ECB are going to do at their meetings over the next week and even beyond. I always thought that with inflation where it was, that central banks would keep hiking until they broke something, which was especially likely with the yield curve so inverted. Now they have broken something, is that enough for a pause? Much will depend on whether markets and contagion risk can calm quickly enough. If the FOMC meeting was today I strongly suspect they wouldn't hike but a week is a long time in these markets. For the recession call it's simpler. As per last month's chart book we were just "Waiting for the lag" (link here). It's fair to say that the lag has well and truly arrived and it’s unlikely now that a key part of our macro story, namely lending standards, are going to get looser given all that's gone on. So no change to our very bearish year end 2023 credit spread targets through all this crisis…

Now depending on ones call for things to get incrementally worse, SOME out there believe in the ‘Fed put’ — now more than ever. Case in point and ironically so, from Dr. Ed BOND VIGILANTE Yardeni,

Did the Fed just guarantee every bank deposit in America? That's really not the Fed's job; it's up to the FDIC to insure deposits up to a maximum of $250,000. By law, the Fed's job is to keep unemployment and inflation down.

…More than 90% of SVB's deposits were not insured by the FDIC. Depositors were spooked when the bank revealed that it had to sell some of its bonds at a loss of $1.8 billion to raise cash. FDIC data show that during Q2-2022, deposits totaled $17.9 billion with $7.4 trillion insured and the remaining $10.5 trillion uninsured (chart).

To reduce the risk of additional bank runs by uninsured depositors (and mitigate the adverse consequences if they do happen), the Fed issued a press releaseon Sunday titled “Federal Reserve Board announces it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors.”

That certainly sounds like a guarantee to protect all depositors!

… Our conclusion is that the Fed Put is back. This time, it’s aimed at stabilizing the banking system, which should also stabilize the financial markets. Under the circumstances, the Fed may pass on a rate hike at the FOMC meeting next week. Or if it goes with a 25bps rate hike to 4.75%-5.00%, it might use the SVB debacle as proof that the federal funds rate then would be restrictive enough and opt to hold it there for a while.

Isn’t that ironic, dontcha think? Now, getting back TO a rather large German institution where another analyst — a fan favorite — is attempting to seize the day and use as a teaching moment,

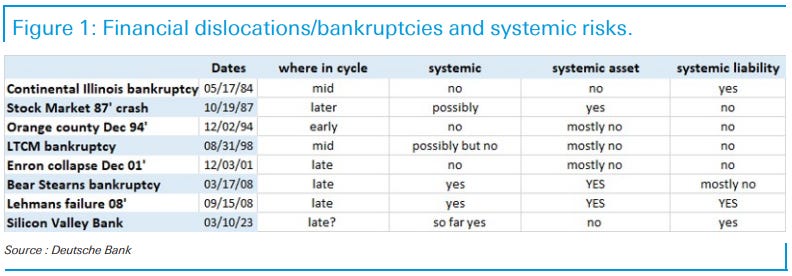

The Tables below provide a comparison for how the latest events surrounding Silicon Valley Bank (SVB) compare with other experiences of financial dislocation in the last four decades. The Tables below look at the financial market experience (Fed funds, US 2y and 10y yields, US equities, currencies and vol) surrounding the 1984 Continental Illinois, 1994 Orange county, 1998 LTCM and then Enron collapse, and two of the most influential events of the Great Financial Crisis in 2008.

Figure 1 looks at these financial bankruptcies, when they occurred within in the business cycle, and whether there were systemic risks stemming from the asset side, or, whether it was the liability side and runs on the bank that fostered the system-wide risk.

The Funds rate data shows that a year after the financial event, funds were lower in all events outside the 1987 stock market collapse, and the Orange County problems.

As per the funds rate, the 2y yield follows a pattern of being typically far below its level within 3m of the crisis, and, in the following year.

This also applies to the 10y yield, suggesting that bond rallies around these crises regularly lead to substantially lower yields across the curve.

In the 3m aftermath of past financial 'events', the yield curve has not consistently steepened or flattened, but it has tended to steepen a year after the crisis. Presumably this steepening would be even more in prospect in this cycle given the unique pre-existing curve inversion in this cycle, whereby the curve has sent an unusually negative growth signal in this crisis.

Normally T. bond Vol is highly elevated a month into the crisis and then stays high in the next month, before collapsing within a 3m period.

For equities the tendency has been to go into the crisis with considerable weakness, as the financial crises develops, and on balance be up over the next 1 and 3 months. The 2008 crisis is typically the exception to this rule. In any event, equities performance within 3m, is rarely bleak relative to its pre-crisis performance. Equity vol within 3mths moderates somewhat…

From history lesson TO the Oscars? Yeah, I know, everyone seems to fancy this analogy … DB

Over the weekend, the Fed, Treasury and FDIC stepped in forcefully to stem the risk of bank runs with the joint creation of the Bank Term Funding Program (BTFP). This program will offer one year loans backed by Treasury capital to a variety of institutions against qualifying assets valued at par (for more details see here).

These developments raise substantial uncertainty about the extent and timing of further rate increases by the Fed. We have often argued that identifying the terminal rate that is “sufficiently restrictive” is a learning process. Recent events suggest that the lags of monetary policy may be alive and well and there is likely to be substantial tightening yet to come.

In light of these events, we have for now maintained our expectation for a 25bp hike at the March meeting but see this as a close call. While in real-time risk management could argue for pausing (more details in the note), we also know that the markets and macro backdrop can shift quickly. We will finalize our view on the March FOMC outcome after observing this week’s developments.

That said, tighter financial conditions and risks to financial stability argue that “sufficiently restrictive” may be coming into view and that the terminal rate could be materially lower. We now peg the peak fed funds rate at 5.125% (versus our previous forecast of 5.625%). In contrast to the substantial uncertainty about the Fed outlook, recent events have strengthened our conviction for at least a moderate recession beginning by year end, if not sooner.

In as far as updated FED CALLS — yesterday it was Goldilocks and today it’s CSFB and Barclays and Wells (so far, but it’s early).

CSFB: The Fed finds a victim and shortens the hiking cycle

The FDIC guarantee of all deposits at the banks it has taken over combined with the Federal Reserve’s new Bank Term Funding Program allowing banks to pledge Treasuries at par for funding should contain deposit flight contagion.

However, this could take time and uncertainty could remain high over the next week or so. This argues for the FOMC to pause rather than hike at its March 22 meeting. Following through with a hike next week likely requires bank funding to stabilize convincingly this week.

If the Fed does pause next week, we would still expect 25bp hikes in May and June. The dot plot is likely to shift higher with the median dot for 2023 rising to 5.375%.

Bank failures should accelerate the pace of transmission of Fed tightening to the economy. Bank deposit and lending rates are likely to rise, and credit conditions are likely to tighten further.

Nonetheless, we judge it important that these failures came mainly from losses on financial positions, not from defaults on loans. They do not necessarily serve as an early warning of a rapid rise in credit stress in the non-bank sector.

… However, the stress of the past several days will probably limit future hikes to 25bps – because it is likely to accelerate the transmission of the policy tightening that has already taken place. Bank deposit and lending rates are likely to rise, and lending conditions are likely to tighten somewhat.

With financial stability concerns moving to the forefront, we adjust our call to assume no hike at the upcoming FOMC meeting, justified by risk management considerations. We think the peak dot will be at 5.1% in 2023, for similar reasons. The March decision remains fluid, and our views will evolve with market developments.

The failures of Silicon Valley Bank and Signature Bank have injected a great deal of uncertainty into the economic outlook. We lean toward a "pause" in the Fed's rate hiking cycle at the March 22 FOMC meeting.

… Systemic Areas of Concern

Although there are idiosyncratic elements of the current situation, there are also some systemic elements as well. According to the FDIC, the deposits of the commercial banking system in the United States are currently equivalent to more than 80% of the system's assets, the highest ratio in more than 30 years (Figure 3). However, the percentage of deposits that are insured has fallen to only about 50% of system assets. Therefore, it is easy to see why policymakers would be concerned about other banks experiencing significant deposit outflows (i.e., bank runs) such as experienced by Silicon Valley Bank

Fortunately, the commercial banking system is rather liquid with cash, predominantly in the form of deposits at the Federal Reserve, accounting for 14% of the system's assets at present (Figure 4)…

…For now, we lean toward a "pause" occurring at the March 22 FOMC meeting, meaning no rate hike. We do not think CPI data for February, which will be released on March 14, will be a major determinant of whether the FOMC hikes rates at its next meeting. Ultimately, we believe monetary policymakers will only be able to tighten further if financial markets and the banking system show signs of stabilization. Assuming financial markets stabilize, then upcoming CPI data will be more relevant for the monetary policy outlook beyond the March 22 FOMC meeting. Given how rapidly developments have occurred in recent days, we doubt the FOMC has reached a consensus on how to handle its upcoming meeting, which remains nine days away. Monetary policymakers will be monitoring developments closely in the days ahead, and so will we.

The Fed Likely Considers Rate Cuts and the Halt of QT as Financial Turmoil Continues

We expect a 25bp rate cut and a halt of balance sheet reduction in March while a new lending facility is possible.

… Also, the fact that other banks are facing a serious bank run risk suggests an increasing risk of over-tightening by the Fed, which also supports a rate cut in the near term. As we argued, the cumulative rate hikes are disproportionately reducing the supply of credit through bank loans relative to financial market conditions (for more details please refer to Higher Fed Funds Rate May Spur Deeper Recession , 3 March 2023) (Fig. 2 ). The lagged impact of past rate hikes could now materialize in a draconian way. We believe a tightening of financial conditions through bank loans could potentially steer the economy into a recession starting in H2 2023. However, the process might be accelerating, potentially moving forward a recession and exerting disinflationary pressures with some lag. At this point, the Fed could become more forward-looking in a sense that it might put more weight on the inflation outlook as opposed to waiting for realized inflation to come down materially. In this regard, although we expect a solid 0.4% m-o-m core CPI inflation in the February CPI report on Tuesday 14 March (for more details on our CPI forecast, please refer to our February CPI Preview , 9 March 2023), we think financial stability risks are quickly becoming a dominating factor for monetary policy.

All of these FED calls in mind, ultimately they are attempting to answer a similar question. In short, Saravelos of DB,

The market is sending a consistent message today: it fears that a US recession is about to start. We are now pricing in Fed cuts rather than hikes, the yield curve is bull steepening sharply, commodities and equities are down with cyclicals under-performing. This is all consistent with an imminent US recession. Without taking a strong view on whether this will indeed happen, it is worth making three observations.

First, a systemic financial event is not a necessary condition for recessionary dynamics…

Second, the dollar is behaving extremely unusually, down against the vast majority of G10 and EM currencies despite a recession priced in…

Third, the correlation breakdown between risk appetite and the dollar will put pressure on portfolio construction if sustained…

Finally, for us ‘visual learners’ a suggestion from Dr. Copper ‘bout where rates are headed — from BBG,

… The copper/gold ratio shows there’s wide agreement that it’s become harder for the Fed to fight inflation with rates in the wake of Silicon Valley Bank's failure.

The ratio, which takes the price of copper divided by the price of gold, is usually a good indicator of expected real interest rates, as one commodity is pro-cyclical and the other is seen as a hedge against inflation.

Right now, the fact that the ratio between the two has dropped makes sense, because the policy path has become more complex. Raise rates too much, and something in the financial system might break with bank failures the result. Raise too little, and inflation becomes very hard to control.

A week ago, traders were leaning towards a 50 basis point hike at the Federal Reserve's March meeting. By late yesterday, many (including Goldman Sachs) were doubting whether they'd hike at all.

As always, though, such cross-asset relationships should be treated with a pinch of salt, as market-internal fundamentals make the signal noisy. Right now, for instance, copper’s fate is much more tied to China’s perceived post-lockdown strength than to global growth.

For some further contextualizing visuals, John Authers’ latest

… It also led to the sharpest one-day tightening in financial conditions, according to the Bloomberg index which takes a number of factors into account, outside of the Lehman and Covid crises:

To an extent, this can almost be viewed as mission accomplished for the Federal Reserve. The problem for the last few months has been that financial conditions have eased, on optimistic projections that the Fed will be cutting rates soon, and this has undermined its fight against inflation…

Another visual which caught MY eyes also caught eye of global director of research at MS who offers out some of the

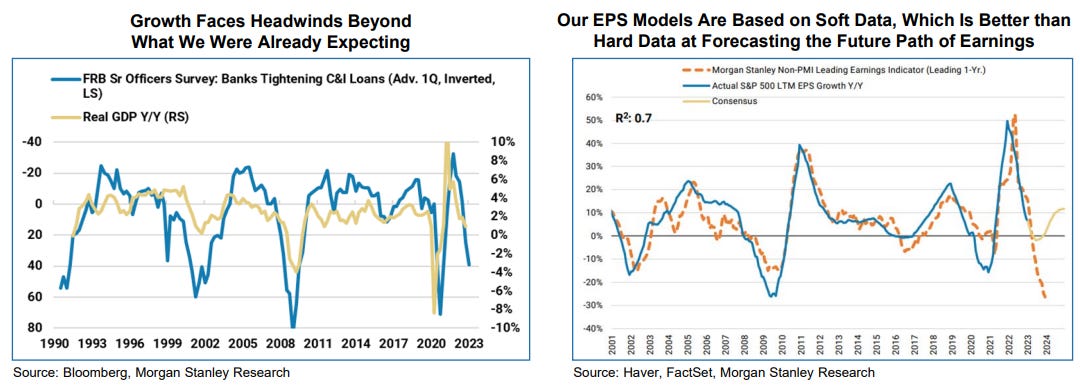

(1) US Rates Strategy: Financial conditions are affected more by rates volatility than by the Fed’s terminal rate.

(3) US Equity Strategy: Prospect for potentially tighter credit supports our view that earnings growth estimates are too high.

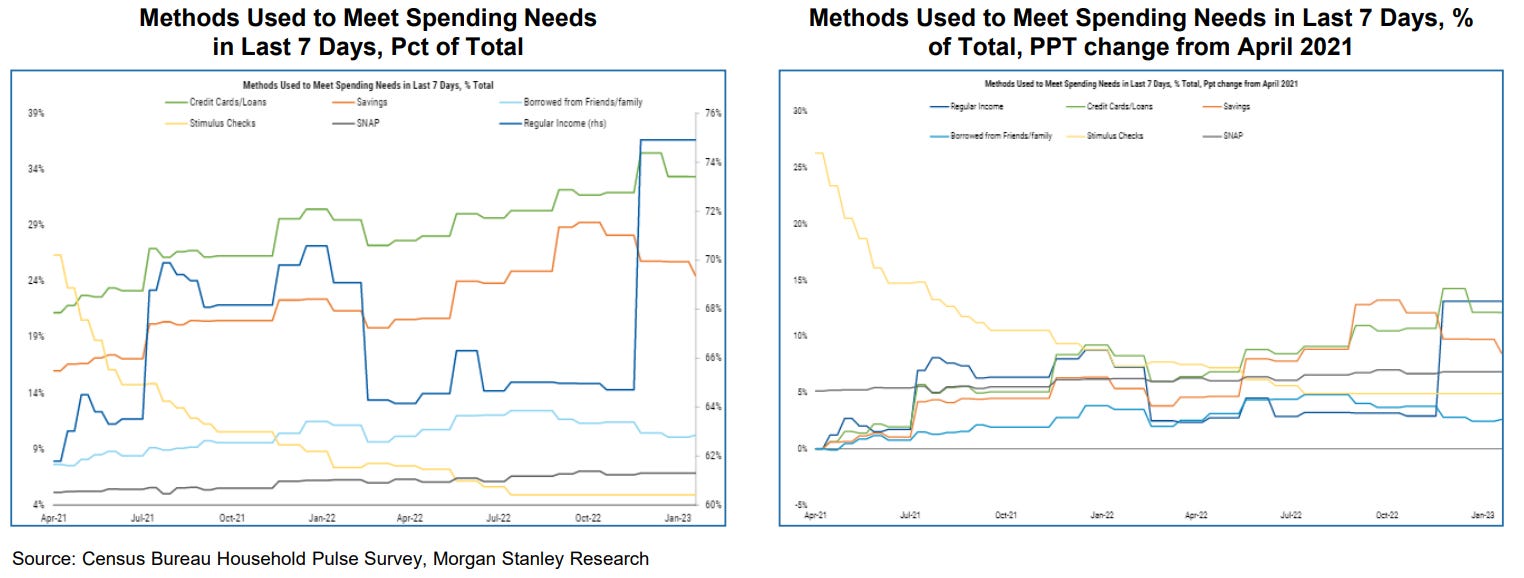

(4) US Economics: Consumption has been resilient but shifts in how consumers fund spending may augur a slowdown.

Aggregate consumption has remained resilient, but our US Economists have been monitoring which sources of income consumers have relied on to meet their spending needs over the past two years, and they find evidence that consumption is set to soften in coming quarters. Across all income brackets, as Covid-related support fades, reliance on excess savings has dwindled as consumers shift more heavily towards traditional means such as labor compensation. Usage of credit cards has risen across the board, indicating that it is not only subprime borrowers tapping into their line of credit to fund spending. Our team continues to expect spending to slow, bottoming in 2Q23 with an outright decline in real PCE on a Q/Q annualized basis, before beginning a slow rebound in the back half of the year. Even so, they expect PCE to remain below potential through 2024.