(USTs are higher, steeper following UK, Ger and BoJ all on solid (~250% avg) volumes)while WE slept; BoJ TWEAKS, illustrated; US econ DEFIES laws of gravity;

Good morning … Traveling yesterday, what did I miss?

Fed jacked rates (but it was a dovish hike, you know, the LAST one ever), equities streak continued while bonds … well, not so much (although SHOULDa / coulda been a concession for 7yr auction — but wasn’t) and by days end, stocks winning streak ended.

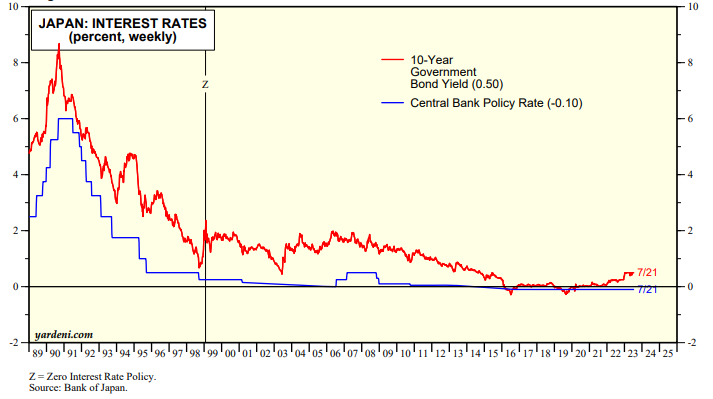

Not really a big deal (see Yardeni comment below — the BULL deserves a rest (double entendre or is it just me)?

BoJ YCC a BIG deal or a BIG nothing burger? MY view is that it continues to be a BIG deal and worth watching — they led us down the rabbit hole of negative rates, YCC (save for the Fed 1942 - 1951 — see FRB Chicago HERE for more) and modern day central planning will continue to be watching every move. And listening to every word (Jackson Hole coming…)

BUT be that is it may, one might NOT be able to tell by looking at US markets in the early going here … SO here’s an unprofessional view of 10yy JGBs via TradingView

I’m sure it’s nothing … and hey, how ‘bout that momentum — moving TO quite oversold on a daily basis … over to you, Mrs. Watanabe?

BOJ left rates unchanged but decided “to conduct yield curve control with greater flexibility, regarding the upper and lower bounds of the range as references, not as rigid limits”. BOJ produced chart to explain how tdhe 10 year yield could now move up to 1% and that their outlook for CPI had increased for this year (although not future years) while firms’ inflation expectations had shot up:

Nikkei: BOJ tweaks policy to allow 10-year yields to rise past 0.5% - Central bank offers to buy long-term JGBs at 1.0% every business day.

**ZH: Stocks Dump, Yields & Yen Spike On Regurgitated Trial Balloon BOJ "Will Discuss" Tweaking Yield Curve Control**

ZH: Tailing 7Y Auction Prices At A Record High Yield ZH: Fed Hikes Rates By 25bps As Expected, Stays Data Dependent WolfST: Fed Hikes by 25 Basis Points, to 5.5% Top of Range, Highest since 2001, More Rate Hikes on the Table. QT Continues

… let’s get back to work get this note back ON the rails … and so, here is a snapshot OF USTs as of 711a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are higher and the curve is steeper this morning, following curve steepening moves in the UK and Germany this morning. The details from this morning's BOJ meeting are linked above, DXY is lower (-0.15%) while front WTI futures are too (-0.4%). Asian stocks saw a sharp rally in China-linked benchmarks but a modest downturn in the Nikkei (-0.4%), EU and UK share markets are mixed while ES futures are showing +0.4% here at 7am. Our overnight US rates flows an initial downturn in prices during early Japan hours before a rally into the London open. We saw better buying throughout the Asian session (real$ in 5's - 30's) on very elevated volumes (~400% of ave). In London's AM hours, it was more real$ buying in the belly to the long-end with fast$ a better seller in 5's and 7yrs. Volumes during London hours were actually below-average despite the surge in volume during Tokyo time. Overnight Treasury volume was very, very solid though at ~250% of ave.

… as our first chart attachment of Tsy 30yrs illustrates, above the 4.045% support level there may be little support for bonds until 4.345% or another 30bp above this nearby support. Indeed, it took only three November trading sessions to rally from 4.345% to 4.045% so the idea is/was that above 4.045%... there could be a possible 30bp air-pocket to next-support. Bonds have collected themselves this morning after the BOJ meeting outcome and they remain just a hair below this 'last' range support at 4.045%. Today's week-end close could be telling and perhaps the good news for bonds (near-term at least) is that Monday's month-end is a backdrop and probable short-term crutch for bonds. Regardless, big test here for bonds, we think.

Surprisingly, my TradingView of bonds looks very similar!! … WATCHING the big test and for some MORE of the news you can use » IGMs Press Picks for today (28 July) to help weed thru the noise (some of which can be found over here at Finviz).

From some of the news to some of THE VIEWS you might be able to use… here’s a taste of what Global Wall St is sayin’ …

The advance estimate put Q2 GDP growth at 2.4% q/q saar, surpassing expectations. The surprise likely reflects this morning's stronger-than-expected June estimates of international goods trade. Much as expected, the estimates point to resilient private final demand in Q2, reinforced by resurgent nonresidential investment.

BNP US GDP: Consumption slows as Bidenomics props up investment

The headline Q2 GDP print topped estimates, rising 2.4% (annualized q/q). The report featured sharp deterioration in consumer demand and a pickup in investment growth, which resulted in little change in the pace of growth in final sales.

The business sector strength seems to be driven by the implementation of the CHIPS and Inflation Reduction Act laws. Investment in equipment rebounded sharply, while structures investment continued to expand at a robust pace.

Construction spending in the manufacturing sector has surged in the industries involved in computer, electronics and electrical manufacturing, accounting for much of the recent strength in nonresidential construction and business investment.

The BoJ has made minor changes to the operating policy of the YCC. It left the range for its long-term interest rate operations unchanged at +/-0.5%, but will allow it to exceed 0.5% to some extent depending on market developments. Reflecting this mandate, a fixed-rate operation will be offered at 1.0%. The BoJ does not accept that this correction is an inflation fight, but it seems to be wary of the risk of uncontrolled yen depreciation. The aim should be to stabilize the exchange rate by giving market participants the expectation that if overseas interest rates rise sharply or the yen weakens, the yen interest rate could also rise…

… We still expect the central bank to revert to a "back to basics" approach during the first half of Kazuo Ueda's tenure as Governor, with its "yield curve control" (YCC) framework and "inflation-overshooting commitment" to be scrapped at some point so as to allow for a renewed focus on (1) targeting of short-end interest rates and (2) forward guidance.

That said, we also envisage maintenance of the current QQE-YCC framework at least the time being, believing that any substantial adjustments will need to wait until after the conclusion of the BOJ's "broad-perspective review" and are thus unlikely to come before around mid-2024 at the earliest. There is of course a possibility that some policy settings could be tweaked prior to then with a view to alleviating adverse side effects, but we would expect any such adjustments to stop short of relegating the Quantitative and Qualitative Easing (QQE) moniker to the history books.

We still believe that an eventual exit from YCC will require either (1) a sufficient conviction that inflation is set to remain at adequately high levels or (2) a clearer argument that current ultra-accommodative monetary policy settings are impacting negatively on the economy's fundamentals and thereby making it harder rather than easier to achieve sustainable and stable +2% inflation.

… It was originally another great day for the fictitious soft-landing ETF yesterday until markets started to break down around 6pm London time last night after a softish 7-year Treasury auction and more importantly, a report from Nikkei suggesting the BoJ would discuss tweaks to YCC at this morning's meeting, something they've followed through on as we'll see immediately below. This turned an +8bps sell-off in 10yr US yields into a +13.1bps one by the close and turned the S&P 500 from a +0.7% gain to a -0.64% loss, with the NASDAQ moving from c.+1.3% to -0.22% over the same 3 hour late session period. It all overshadowed a relatively dovish ECB meeting, within the context of the expected +25bps hike, after which European yields moved notably lower for the day (e.g. 2yr bunds -5.1bps).

So the last international hold out on ultra low yields has turned with the BoJ tweaking it's YCC policy in the last couple of hours. In a slightly complicated message the BoJ kept their target for 10yr JGBs at 0% but effectively widened the band to +1% from 0.5% even if they've kept the original bands as reference points. It confused me a bit this early in the morning but they won't be able to defend 0.5% now absent a macro development that structurally lowers yields. 10yr JGBs have increased +12bps as we type to 0.56bps, their highest since 2014 and all other things being equal this should continue to creep up in the days and weeks to come and removes an anchor for global yields. It's going to be an interesting press conference just after we go to print.

Initially, the Japanese yen strangely fell on the news to 141 but now trades +0.6% higher at 138.6. Elsewhere the Nikkei (-2.24%) is sharply lower with the KOSPI (-0.26%) also trading in the red. Chinese stocks are bucking the trend with the CSI (+1.79%) leading gains followed by the Shanghai Composite (+1.38%) and the Hang Seng (+0.89%). US stock futures are edging slightly higher with those tied to the S&P 500 +0.18%. Meanwhile, yields on 10yr USTs (+3.01bps) are at 4.02% as we go to press.

Coming back to Japan, Tokyo’s consumer price index (CPI) rose +3.2% y/y in July (v/s +2.9% expected). This is the 14th consecutive month that the inflation rate in the capital came in above the BOJ’s 2% target. At the same time, core inflation (excluding fresh food) advanced +3.0% y/y in July, higher than Bloomberg estimates of +2.9% but lower than prior month’s reading of 3.2%. More surprising was the core-core inflation (excluding fresh food and energy) which climbed to +4.0% y/y in July (v/s +3.7% expected, +3.8% in June) and provided more justification for the move today. Elsewhere, Australia’s retail sales sharply declined by -0.8% m/m in June, recording its biggest decline this year, versus expectations of a flat outcome…

… Looking at the details, the BOJ has maintained a 10-year JGB yield target of around 0 percent and a tolerable band of around ±0.5 percentage points, but has raised the rate for fixed-rate purchase operations every business day from +0.5 percent to +1.0 percent. Considering the level immediately before the MPM was around +0.5 percent, we think this is effectively akin to a rate hike. However, we surmise the BOJ decided to adopt this asymmetric scheme with the target maintained at around 0 percent because it did not want the market to interpret it as the start of full-blown tightening. In a recent interview, Deputy Governor Shinichi Uchida defined rate hiking as raising the short-term policy rate, including terminating the negative interest rate policy (NIRP) (Nikkei, July 7). Our main scenario for YCC adjustment was for the BOJ to shorten the target maturity, with widening the tolerable band a secondary scenario. While today's YCC adjustment is close to the latter, it still differs in essence …

… The Bank of Japan has practiced masterful inactivity in policymaking for aeons. Today, something happened. The details of yield curve control are not that interesting—the net result is a moderate tightening of policy. BoJ Governor Ueda was supposed to be improving the clarity of communication, but the tightening came as a surprise to markets …

… Weighing on the stock market was a rise in the 10-year US Treasury bond yield back over 4.00%. Some observers said that happened because Q2's real GDP growth rate of 2.4% (saar) was more than expected, raising the odds of more Fed tightening. That doesn't make sense since that was the latest number shown by the Atlanta Fed's GDPNow tracking model. Today's yield backup might have been a delayed response to Wednesday's hike in the federal funds rate. In addition, the Bank of Japan might widen its yield curve control bands tomorrow (chart).

Boy oh boy does all this BULL need a rest …

I digress, for those who are visual learners like myself,

… US 10yr Bond Yields are only seen setting a yield top below 3.70/3.675%

US 10yr Bond Yields stay rangebound after holding key support from their 4.085% YTD high from March, but then also key resistance from the 55- and 200-day averages and late June low at 3.70/675%.

Only below 3.675% would see a yield top established. If confirmed though we would look for this to clear the way for a rally to 3.58% initially, and eventually back below 3.40%.

Above 4.085% on a closing basis would be seen to mark an important bearish break for a move back to test long-term support in the 4.27/4.40% zone – the high of 2022, the 78.6% retracement of the 2007/2020 fall in yields and the “neckline” to the 2006/2007 yield top.

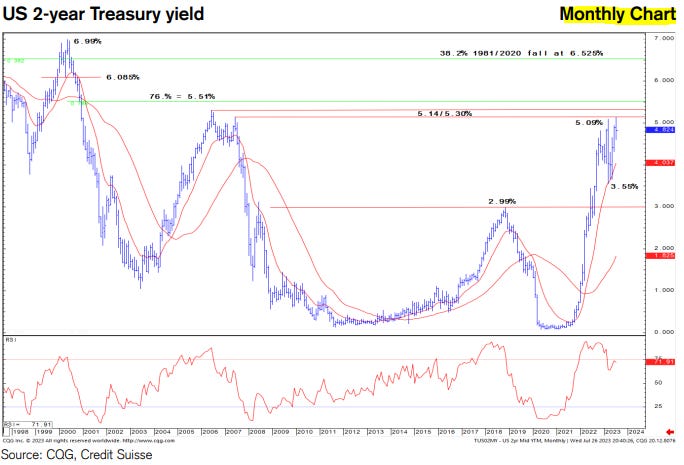

US 2yr Bond Yields are holding major support at the 5.14/5.30% key highs of 2006 and 2007

…Whilst 4.73% holds on a closing basis though there can remain the risk for a fresh look at the 5.14/5.30% support. Only above 5.30% though would be seen as a major break higher, clearing the way for a test of the 78.6% retracement of the 2000/2020 fall in yields at 5.50/5.51%…

Disinflation is speeding up and growth is holding in, but sticky wage growth and high-cost inventories stand between the S&P 500 and a sustainable margin recovery. We think consensus continues to underestimate negative operating leverage and its drag on earnings growth, especially for SPX ex-Tech and into 2024.

AND after a long WINNING streak, we get ONE day in a row where the markets stumbled and investors now be like,

Thanks for your continue patience with travel schedule and spammation SHOULD return to somewhat normal basis … THAT is all for now. Off to the day job…C U this weekend…

In no way shape or form does the US 10 yr look like it's been subject to YCC of late; I mean no WAY could any leviathan sized org be trying to keep the 10 yr at or below 4%, NO WAY MAN!

Lacy just did a great interview on Wealthion; found it helpful to've read the Hoisington Q2 report first. Thanks for that link Steve that's always a MUST read!

In no way shape or form does the US 10 yr look like it's been subject to YCC of late; I mean no WAY could any leviathan sized org be trying to keep the 10 yr at or below 4%, NO WAY MAN!

Lacy just did a great interview on Wealthion; found it helpful to've read the Hoisington Q2 report first. Thanks for that link Steve that's always a MUST read!