As we BOND together in / around CPI and then this afternoons liquidity event … here is a snapshot OF USTs as of 705a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are aggressively mixed ahead of CPI and after a 'surprise,' -10bp cut in China's 7-day RRP rate. On the other hand, UK 2yr yields rose above their fall Mini-Budget highs (see attachment) after strong UK labor market data. DXY is lower (-0.35%) while front WTI futures have rebounded higher (+2%). Asian stocks were higher (Nikkei closed >33k for first time in 33yrs), EU and UK share markets are mixed and little-changed while ES futures are showing +0.1% here at 6:40am. Our overnight US rates flows saw some fast$ selling in intermediates during Asian hours but volumes then were very weak at around 50% of ave. In London's AM hours some selling/paying in Tsys was seen after the UK data but prices held firm despite that. Our volume sheet suggests around 125% of average volume overnight despite the very weak volumes reported by Asian colleagues…

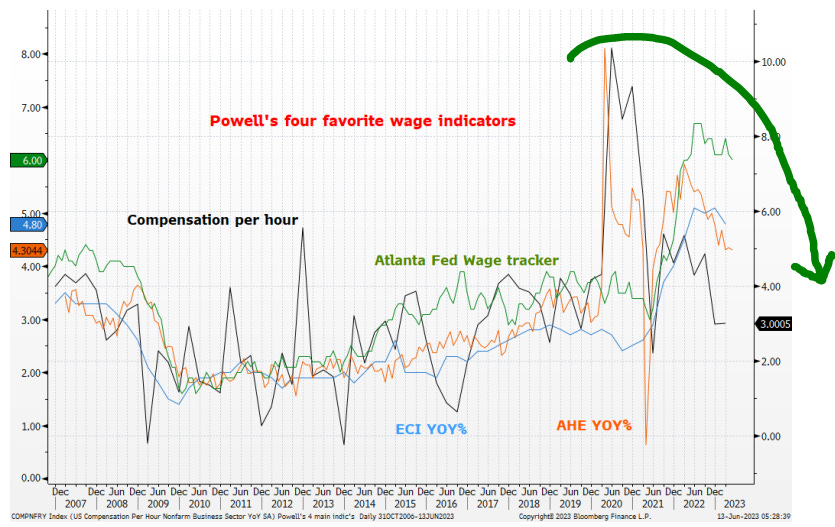

…Our last attachment this morning offers an updated look at Powell's four favorite wage indicators: ECI YoY%, AHE YoY%, Atlanta Fed's wage tracker and compensation/hour.

… and for some MORE of the news you can use » IGMs Press Picks for today (13 JUNE) to help weed thru the noise (some of which can be found over here at Finviz). Before heading there, from press picks on CHINA

From some of the news to some of THE VIEWS you might be able to use… here’s what Global Wall St is sayin’ …

As you’d imagine there are a few additional CPI precaps.

UBS Lower inflation for most? Headline US May consumer price inflation is expected to be close to 4% y/y. It is worth remembering that this is not news to parts of the US—areas like New York and Los Angeles have seen the headline inflation rates collapse this year, and are already experiencing sub-4% inflation. This rapid disinflation argues against the inevitability of price stickiness.

The core consumer price measure is likely to be supported by the fictitious owners’ equivalent rent, and volatile used car prices. Any US household that owns its own home but is not buying a used car has a cost of living experience below that of consumer price inflation. It thus has more spending power. This covers almost two thirds of US households…

And a large German bank strategerist notes the FX moves in response,

DB - A different asymmetric response to a CPI surprise

For recent CPI releases over the past year, we have tended to have a bigger negative USD reaction to soft CPI, than positive USD reaction to an upside surprise…

This same firm ALSO attempts to skate to where the puck is gonna be,

It's been some time since we got used to deal with uncertainty around CPI releases, and the May print should be no different. We currently see inflation risks tilted to the downside over the medium term. Private quits rate (our preferred labor market slack indicator) suggests further deceleration in wages, which would indicate further downside on core services ex shelter. Forward-looking indicators suggest significant deceleration in rent inflation over the next months. Our macro models signal significant richening in USD breakevens as manufacturing/services input prices survey data declined meaningfully. As for tomorrow's print, using our ex energy inflation breakeven estimates (see here), we note consensus headline and core forecasts would seem to imply strong food inflation figures. Overall, given our model input, we see 5y breakeven as the best point to express a bearish view on USD inflation.

This same shop moves beyond today’s CPI and tomorrows FOMC and, incorporating all of these and more, offers

… The broad contours of the forecasts are little changed since our prior update. We continue to expect the UST curve to steepen, with lower front-end yields driven by recession and Fed rate cuts. We now forecast 10y UST at 3.35% at year-end, slightly lower than previously, as we anticipate long-end yields will initially drop as recession nears. From there we project a rebound on various factors boosting term premia, bringing the 10y to 3.6% at the end of 2024….

With the US CPI in mind, it’s worth pausing a moment and looking to the FAR East where China CUT rates overnight,

GS: PBOC cuts OMO rate by 10bps; MLF rate and LPR cuts could soon follow

Bottom line: The PBOC cut the OMO reverse repo rate by 10bps from 2.0% to 1.9% this morning (June 13th). This move could suggest the start of additional monetary policy easing. We expect the PBOC to cut the 1-year MLF rate and LPR rate by 10bps as well on June 15th and 20th, respectively, but now think the 25bp RRR cut that we had previously forecast for June is likely to be delivered in Q3 instead (historically the PBOC has almost never cut policy rate and RRR in the same month). There could be another RRR or policy interest rate cut in Q4, depending on the economic outcome over the next several months. Sluggish activity growth, potentially weak credit extensions, and low confidence are the reasons behind this cut, in our view. The RMB depreciated by around 0.3% in response to this interest rate cut, but amidst the backdrop of weakening exports, we expect the central bank to prioritize growth and show a higher tolerance for currency depreciation.

Exhibit 1: The PBOC cut the OMO 7-day reverse repo rate by 10bps

Firm points their analysis back home and from cutting rates to another IDEA — not suggestion — it asks,

■ Lowering inflation to 2% is likely to take a while, and the last leg of the journey might prove the hardest. This has led some to ask whether the Fed couldn’t spare itself the trouble and raise its inflation target. After all, many economists came to see 2% as too low last cycle because it left monetary policy too little room to maneuver in an economy with a lower real neutral rate. And if raising it opportunistically is unacceptable, what about in the 2024-2025 framework review?

■ We doubt that the FOMC will raise its inflation target, for three reasons. First, Fed leaders have expressed doubts about whether they have the right to raise the target without Congressional signoff. Second, the Fed’s decision to take raising the target off the table in its last framework review—even though that was arguably the most straightforward solution to the problem of reduced monetary policy space—suggests that there is a strong institutional reluctance to raise the target. Third, the recent inflation surge and the return of supply shocks have weakened the normative case for a higher target at least a bit by making some of the risks look more serious, especially the risk that inflation might be more volatile when it is high enough to be noticed.

■ A current and a former Fed official recently raised the possibility of changing the 2% target to a range centered on 2%, such as 1.5-2.5%. Fed officials rejected this idea in the last framework review because they worried that implying 1.5% is good enough could make the low neutral rate problem worse, but a range would have the virtue of honestly acknowledging the limited control of inflation that any central bank can have, and officials could reconsider in the next framework review.

■ In short, we think the FOMC is likely to maintain its 2% target. That said, if core PCE inflation falls to 2.5% this cycle, we doubt that the FOMC would have much appetite for any further hawkish policy moves that might risk causing a recession just to get the rest of the way to 2%.

I would personally seriously doubt the Fed angling to move this particular goalpost as it would risk any chance of EVER having (had?) credibility.

That aside, looking at some ‘analysis’ from a large French bank in a large monthly package or themes and notes,

BNP USD rates: Tactically bearish as Fed ‘skips’ in June

Fed to skip in June, hike by 25bp in July: Data remained strong, with the May payroll print exceeding estimates (actual: 339k, estimate: 190k) and the 3-month moving average ticking higher. Meanwhile, wage and price inflation remain resilient, with core CPI still expected to print above 5% this month. Despite ISM data surprising lower and the signal from corporate profits and SLOOS clearly recessionary, we revised up our Q2 and Q3 GDP forecasts while still expecting a shallow recession in late Q3 2023.

The May FOMC minutes showed a split between “some” expecting further hikes and "several" seeing a pause. The likely compromise of a skip at the June meeting, with a lean towards more tightening in July, was reinforced by other Fed officials. As the near-term economic outlook is therefore strong and Fed officials remain hawkish, we expect a ‘hawkish hold’ in June, with a 25bp hike in July (terminal rate at 5.5%). We continue to expect rate cuts starting in March 2024, with 175bp of cuts in 2024.

US rates to grind higher near term, and bull steepen into H2 2023: As the economy is withstanding elevated policy rates, we revise up our US yield forecasts. We expect rates to peak this quarter (Q2) with the 2y yield at 4.7% and the 10y yield at 3.9% (2s10s: -80bp). Once our economic outlook materialises, market focus should shift to potential Fed easing and rate cuts, triggering a rally in the 2y to 4.05% by the end of the year that continues into cuts in 2024. Meanwhile, we expect the 10y yield to stay elevated at 3.85% as we do not expect the Fed to signal cutting the zero lower bound as it normally does (2s10s: -20bp).

… Post-debt ceiling liquidity drain to push funding costs higher: With the debt ceiling out of the way, we expect the Treasury to rebuild its cash balance (TGA) back to ~USD600bn by September, leading to a liquidity (or liquidity adjacent) drain of ~USD800bn (reserves + RRP). We expect the Treasury to rely primarily on T-bills, and see net T-bill issuance into September reaching ~USD850bn.

For money market funds (MMF) to rotate out of the reverse repo facility, they will need to see T-bills and repo cheapen above swaps, while the curve will need to steepen enough for them to term-out. We expect 60% of the total USD800bn drain to come from a decline in the RRP facility (~USD500bn) and the rest from reserves (~USD300bn) into September. Banks will still be faced with a considerable drain of reserves that may need to be met with higher deposit rates, increased borrowing in repo from MMFs, increased BTFP/discount window usage, or FHLB cash advances. We expect the liquidity drain to increase EFFR-IOER by 2-3bp into Q3. The massive T-bill issuance and increase in repo volumes is likely to push SOFR-RRP as much as 5bp higher into Q3 (SOFR-RRP: +6bp), and possibly 3bp more into Q4….

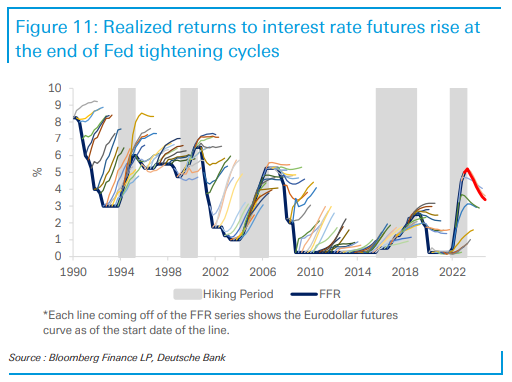

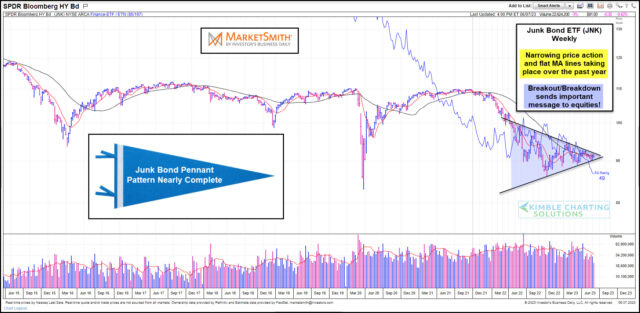

AND for those of us who are visually motivated and learners,

Kimble: Junk Bonds “Pennant Pattern” Nears Critical Point For Investors!

… Should Junk Bonds breakout to the upside, they send a positive message to stocks!

And another couple things to consider ahead of CPI,

ZH: Near-Term Inflation Expectations Tumble To 2-Year Low As Economic Outlook Worsens: NY Fed

Finally, maybe all these academics need only stop and look at the prices at the pump … and so, a look at ‘Earl

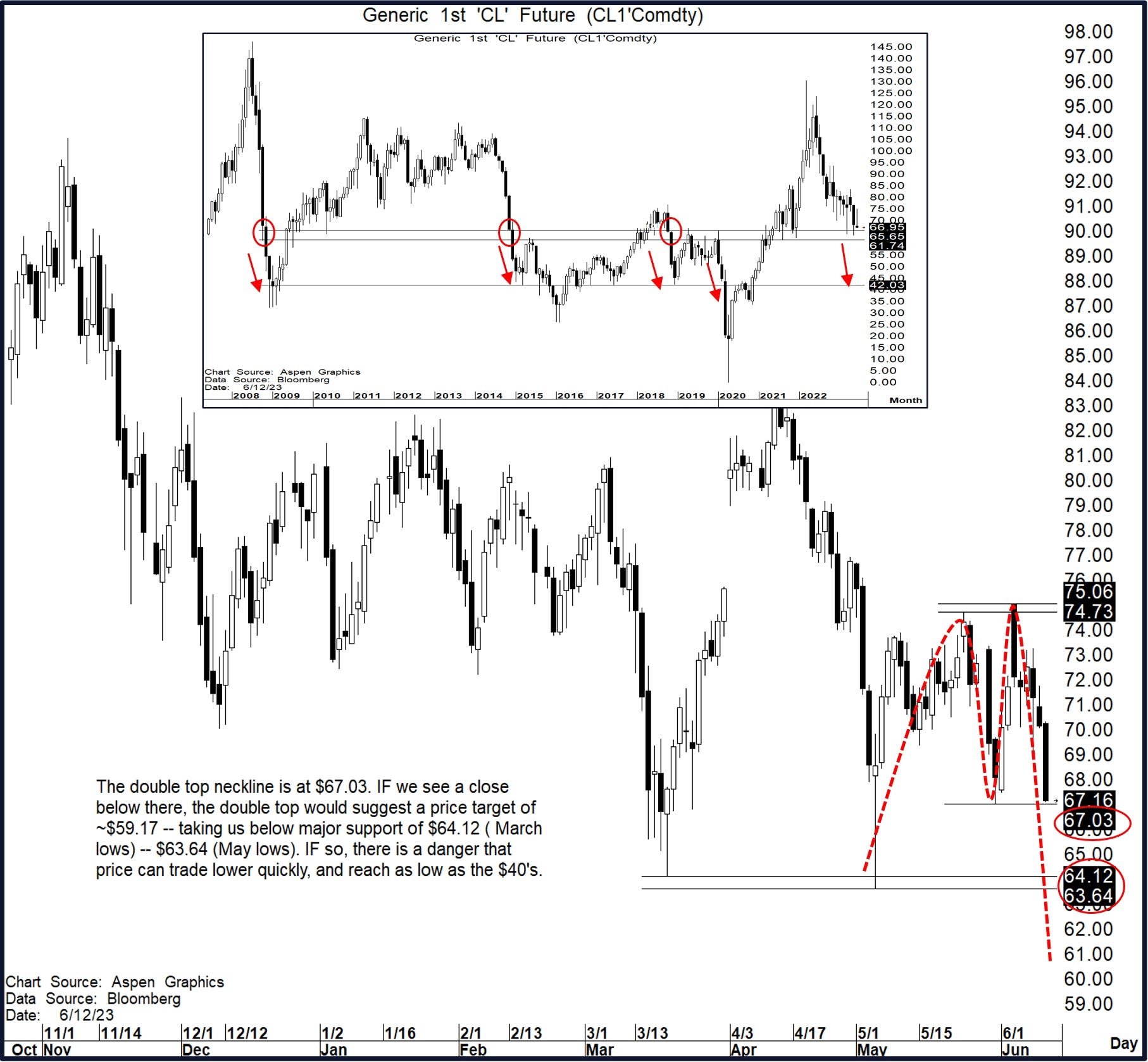

CitiFX Chart of the (yester)Day: Dangling on the edge

WTI: There is a potential double top IF price closes below the double top neckline at $67.03.

IF we see a close below there, the double top would suggest a price target of ~$59.17 -- taking us below major support between $64.12 (March lows) -- $63.64 (May lows).

IF so, the monthly chart suggests there is a danger that price can trade lower quickly, and reach as low as the $40's.

Double top could bring us below major pivot point

AND this brings me right back to a question / hashtag above.