… Mr. Powell suggested Fed officials were moving into a new phase of policy tightening in which they would try to judge just how high rates need to rise. “My colleagues and I do not want to overtighten because…cutting rates is not something we want to do soon,” he said. “That’s why we’re slowing down and going to try to find our way to what that right level is.”

AND while USTs are steady to a touch FLATTER this morning, 2yrs were shot out of a cannon, dropping MORE THAN 10bps on the session (and nearly 20bps range from cheap to rich…)

Momentum is STRETCHED (overBOUGHT) and today seems to be a day where markets are collectively catching up with themselves…

Clearly lower front-end rates (JPOW puttin’ PAID to idea of a PIVOT) gave markets this (false)sense of security … But then, there’s this …

Something surely going to ‘break’ and the Fed would like to seem … aware (rather than complicit)? Is it too late? I do NOT know — CPI coming up just as the FOMC meeting kicks off and this is certainly NOT to be dismissed. Shall we call it a nil - nil DRAW between HawkNADO and PIVOT’istas?

… here is a snapshot OF USTs as of 705a:

… HEREis what another shop says be behind the price action overnight…Morning commentary titled, “Asymmetry of Tradability”

… Overnight flows Despite little net change in 10-year rates overnight, volumes in Treasuries were impressive with cash trading at 154% of the 10-day moving average. 5s were the most active issue with a 39% marketshare and 10s took second most with 26%. The front-end was particularly active with a 25% allocation as 2s and 3s received 14% and 11%, respectively. 7s garnered 6%, 20s were very quiet with just 1%, and 30s rounded out the curve with a 4% allocation.

… and for some MORE of the news you can use » IGMs Press Picks for today (1 DEC) to help weed thru the noise (some of which can be found over here at Finviz).

Right TO Global Wall Street and the narrative machine that never sleeps.

… And while we'll get an update to those forecasts at the December meeting, which will likely show an uptick in that terminal rate projection, it will be below 5%, as Powell's comments clearly hammered the terminal rate back under 5%.

Powell also said Fed officials will be looking for “significant positive” real rates across the yield curve, among other asset classes, to assess how restrictive monetary policy is.

While the Fed chair discussed monetary policy, he talked extensively about the labor market, saying there are some early signs of a slowdown and that a “softish” landing is still possible. He said officials are concerned that workers may soon start demanding higher wages, which could have a more troubling impact on inflation.

And despite Powell’s saying that history has taught him "loosening policy prematurely would be a mistake" and that the Fed is going to stay the course until its job is done, stocks exploded when he echoed Brainard saying that "If you are waiting for inflation to go down, it's very difficult not to overtighten." …

… the rally in risk assets continued, and the S&P 500 is now up by more than +14% in total return terms over October and November. That’s the best performance for the index over two calendar months since late 2020, although there remain plenty of doubts about how durable this is and whether this is just another bear market rally. Meanwhile, the prospect of a downshift from the Fed saw Treasuries (+2.8%) put in their best monthly performance since March 2020, back when the pandemic started and the Fed cut rates back to the zero lower bound…

… In spite of the cross-asset rally in November, it’s still worth noting that there’s plenty of pessimism in markets at the minute. For instance, the 2s10s curve that’s inverted prior to all of the last 10 US recessions is now inverted by -71bps, which is the lowest monthly close since September 1981. In addition, the Fed’s preferred curve of the near-term forward spread (measured by the 18m forward 3m yield minus the spot 3m yield) inverted in November for the first time in this cycle so far, and ended the month at -41bps.

… Sovereign Bonds: Fresh hopes that we might have seen the worst of inflation supported sovereign bonds this month, with Treasuries (+2.8%) seeing their best performance since March 2020. Gilts (+2.9%) outperformed in November as they continued to recover from the turmoil following the mini-budget, but they remain one of the worst YTD performers, having lost -21.6% since the start of the year.

US Federal Reserve Chair Powell's speechwriter signalled a slowing in the pace of monetary policy tightening. The adults on the FOMC had already told markets this was coming, but markets rallied anyway. Powell did try to reverse one of the June policy errors—the core PCE deflator (rather than consumer price inflation) is once again the inflation target to watch.

Coincidentally the October core PCE deflator is due today. The data is likely to show US consumers in October were spending faster than their real incomes were growing—the gap being made up by credit cards and reduced savings. Anecdotal evidence suggested a more significant slowdown in spending in recent weeks—it is not clear if the October data will capture that.

The UN's International Labor Organization issued a report suggesting that for the first time this century global real wage growth would be negative. This is led by weak pay bargaining power in developed economies. While nominal wage growth is too high for central bank inflation targets, weak pay bargaining suggests this will moderate as inflation falls.

South Korea's November exports fell 14% y/y. Demand for goods is clearly softening and manufacturing is likely to underperform services over the coming year.

Whether or not he — JPOW — said anything new didn’t seem to matter as it seemed to propel markets … think MOON SHOT (via Yardeni)

Fed Chair Jerome Powell was a bit less hawkish today. He said he still thinks there is a "path to a soft or softish" landing for the economy. He also suggested that the next hike in the federal funds rate on December 14 is likely to be 50bps rather than 75bps. So stock prices exploded to the upside. The DJIA soared more than 735 points, or 2.2%. The S&P 500 rose 3.1%. The Nasdaq shot up 4.4% …

… This morning, the Federal Reserve's latest Beige Book, which sums up economic anecdotes from the central bank's dozen regional banks across the country, showed that there is growing evidence of moderating inflation: "The pace of price increases slowed on balance, reflecting a combination of improvements in supply chains and weakening demand."

The S&P 500 jumped above its 200-day moving average today (chart).

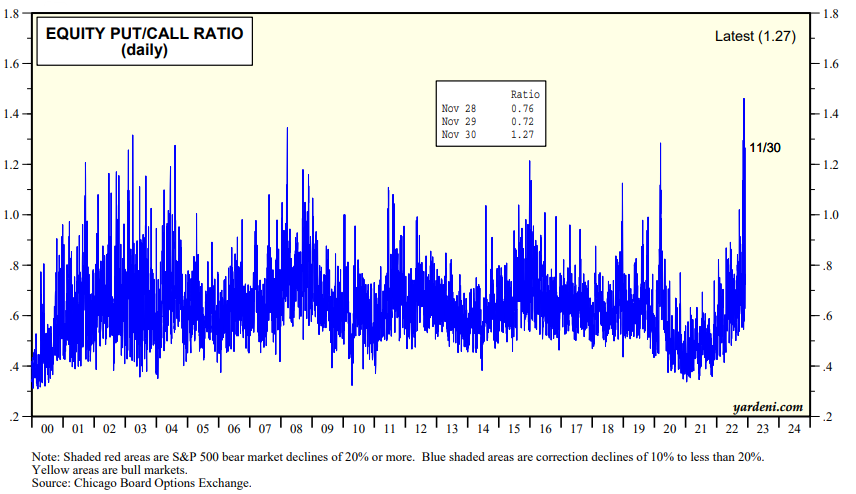

There was some really good news today for the bulls from a contrarian perspective. Investors Intelligence Bull/Bear Ratio remained depressed at 1.22 this past week and the equity put/call ratio jumped to 1.27 as put buying soared (charts).

All we want for Christmas is a rocket ship for Santa. Our yearend target is still 4305 for the S&P 500. That looked too high yesterday...but not too high today.

For somewhat MORE on PRICING and specifically from DataTrek (Colas)

… Two-year Treasury yields fell by 14 basis points, to 4.34 percent, very near 1-month lows (4.33 pct on November 10th). These have now been relatively stable since mid-October, right when the current US equity market rally began. As we have mentioned in prior reports, stable 2-year yields are the prerequisite for a sustainable move higher.

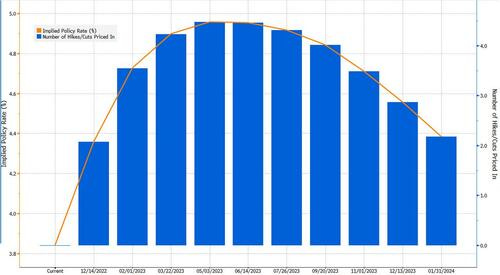

Fed Funds Futures odds for upcoming FOMC rate decisions shifted towards the dovish end of their recent spectrum of probabilities:

Odds for a 50 basis point increase at the upcoming December 14th meeting rose to 75 percent, from 66 pct yesterday. They were 76 percent a week ago. The odds for a 75 bp bump in December fell today, to 25 percent from 34 pct yesterday. A week ago, they were 24 percent.

Futures now give either a 25 or 50 basis point rate increase at the February 1st, 2023 meeting fairly even odds, at 44/46 percent. Those odds for just 25 bp are materially higher than yesterday (33 pct) or a week ago (36 pct).

The chances that Fed Funds see +5.0 percent next year have diminished. Until today, that had been this market’s default assumption – the outcome with the highest probability of occurring. Now, 4.75 – 5.00 percent Fed Funds show the highest odds for every meeting through Q3 2023.

By year end 2023, Futures are putting highest odds on Fed Funds at either 4.25 – 2.50 percent (27 pct probability) or 4.50 – 4.75 percent (29 pct odds). Both are higher than both yesterday and a week ago. This implies a greater likelihood that the Fed will be cutting rates by Q4 2023.

Takeaway: as much as Chair Powell is trying to contain investors’ animal spirits by talking about persistently high interest rates, markets are rejecting that message. Instead, they are looking through his rhetoric and think they see the inflection point for monetary policy. That is a reasonably set up for a continued stock market rally, just as it was from June to August. Against that bullish assessment, however, let’s remember that the CBOE VIX Index still has a 20.X handle today. Every time we’ve seen that level this year, rallies have fizzled. Don’t get us wrong – we’d love to see a year-end rally. Even still, lightening up as the VIX drops below 20 (which seems all but inevitable given today’s news and market reaction) seems prudent to us.

AND … I’m exhausted and I didn’t really even do that much. TOMORROW, though, I’ve have to be in NYC and will cap the evening and week off with a holiday party SO there will be NO update in the morning. I’d expect to have a few moments to hunt / gather and reflect on the week that was as well as offer a few thoughts / LINKS for the week that will be … Thank you in advance for understanding and IF you’d like a refund, kindly reach out. But for now … THAT is all for now. Off to the day job…