Good morning … CASH bond market set to open about 30min before NFP and so I’ll jump right TO what a couple fan fav shops saying just BEFORE NFP … you know …

… WHILE YOU SLEPT We're waiting for our Treasury pricing screens to populate but DXY is slightly higher (+0.1%) with ES futures little changed amid market closures for holiday in Asia and Europe ahead of today's US employment event and our early close here.

… MORNING MUSINGS Ed wrote this in his wrap-up yesterday: "Technically speaking, the second consecutive daily ‘hammer’ pattern seen in 2s and the noncommittal flattening in 2s10s back below the 200dma (-51bps) likely speaks to some tactical exhaustion with CPI data expected to be quite firm next week." Indeed, our first attachment shows Treasury 2yr yields and their recent unwillingness to open or close a session below the 3.77% area despite five intraday forays below the level since mid-March. It's a predictably similar story with the 1y1y OIS rate which, for now, seems to run out of rally thrust below 3.00% (next attachment). At the other end of the curve, 30yrs Treasury yields (next attachment) have inched closer to their potentially key range resistance area (~3.50%) too.

So US rates market benchmarks appear to be going into NFP and CPI with a relatively unstable overall positioning set-up. All our medium and long-term momentum studies still guide quite bullishly while shorter-term studies, and the recent price action that reflects it, indicate an increasingly 1-sided, and long, tactical posturing. Indeed, here's RPM's David Bieber yesterday on SOFR positioning: "Fast 1mth positioning flipping into longs across all packs but large structural shorts held in medium term setup" and on Treasury positioning: "a long build with flows balanced between short covering ($7m) / new long risk ($13m) with positioning flipping long in fast, medium and legacy." The whole idea here is to not chase prices higher here and instead to duck back into the weeds in the hope/expectation that better long entry levels should be seen in the coming sessions... That's how we read the tea leaves right now.

Our next attachment this morning updates the 3mo-10y Tsy curve which is now at inversion levels not seen in decades. This curve is naturally a close cousin to Powell's 3m versus 18mo forward 3mo rate curve; sending the very same message/recession warning. Our last attachment updates the Citi economic surprise hard and soft data sub-indexes. As you know, we're finally starting to see some below-expectations prints in the hard data which hints of the two time series coming more back into line up ahead- after a largely one-way string of hard data beats since last summer...

We'll leave it there with little/nothing new to go on this morning with the data screens blank and the e-mail in-box [pleasingly] empty this morning. We'll have a post-NFP wrap late morning before heading off to dye some eggs. Good luck today.

For MORE just ahead of the NFP, some words from THE best in the business …

Treasuries were unchanged overnight. Not ‘unchanged’ insofar as yields held a tight range in otherwise listless trading as investors sought trading direction in an uncertain market; no, unchanged because Tokyo and London were both closed for Good Friday. As we alternate between our BLS and SIFMA voodoo dolls, it also isn’t wasted on us that there is no settlement of trades conducted today until the world is back online next week. This is an ideal backdrop for an outsized response to any detail of this morning’s payrolls release that doesn’t confirm with market expectations. As we’ve observed in the past, the headline jobs number is easy to dismiss as old information in the case of an upside surprise; after all, hiring decisions associated with March’s NFP-survey week were unlikely to be impacted by the regional banking sector turmoil. For evidence of fallout, investors will need the patience required to wait for the bulk of Q2’s data for a better understanding of the ultimate ramifications. On the other hand, a downside disappointment will speak to the prevailing concerns that the labor market was already weakening before the events of mid-March…

… For this week’s focus on the fundamentals, let us not forget the simmering uncertainty in the financial sector. In terms of the relative containment of the turmoil, responses to our second special question ranged from 1 to 5, with a mean and median reply of 3. We’ll characterize this as a cautious optimism that the worst is behind the market in terms of banking sector volatility, with some acknowledgment of the risk that the Fed’s macroprudential tools will not be sufficient to contain a larger crisis. One of the main macro questions at the moment is what the uncertainty is worth in terms of tightening and how that may influence Powell’s decision making. The most common response to question 2b was 50 bp with 49%, followed by 25 bp that took 23% of responses. 75 bp was offered 16% of the time, while 100 bp and 100+ bp took 8% and 4%, respectively. As a rough approximation of what the bank failures have been worth, we’re comfortable with a weighting between one and two quarter point hikes.

The topic of Japanese demand will continue to attract attention, and the median response to our final special question was 3 in terms of the relative importance of the new Japanese fiscal year to the US rates outlook. There was certainly a divergence of opinion with replies ranging from 1 to 5, and especially as the first auctions in the new Japanese fiscal year loom, we’ll be eager to see the extent to which renewed demand from Tokyo will benefit Treasuries in the coming months…

… and for some of the news you can use head over here TO Finviz where something from BBG (via ZH) caught MY eyes

Authored by Simon White, Bloomberg macro strategist,

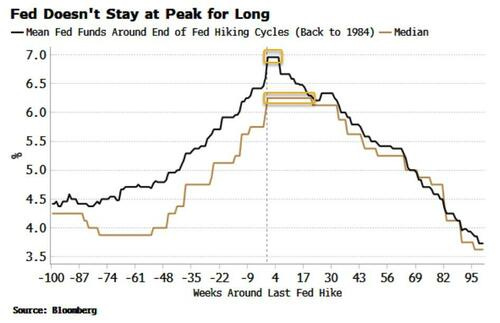

The Fed could be cutting rates sooner than expected given the historically short period between the last rate hike and the first rate cut.

“Higher for longer” is a neat phrase, but it rarely plays out like that in practice.

Rapid rises in borrowing costs invariably lead to something going wrong, which typically has to be put right by cutting rates.

In fact, the median time between the last Fed hike and the first cut is only four months, while the average time is only six weeks.

Some will say “this time is different” and such caveats should always be noted. But this argument is generally applied incorrectly. One should anchor one’s view with the long-term picture, and then tweak it using today’s information. “This time is different” thinking is an inversion of this, starting with the current outlook and then seeing if agrees with the historical outlook.

In a sign of how quickly things can turn, it wasn’t long ago when the market was pricing in several more Fed rate hikes. Suggesting a pause or an early cut back then was somewhat heretical. But fast-forward to today, in the wake of the SVB failure, and the market barely sees a 50% chance of another hike, while pricing in a cut of more than 25 basis points by September.

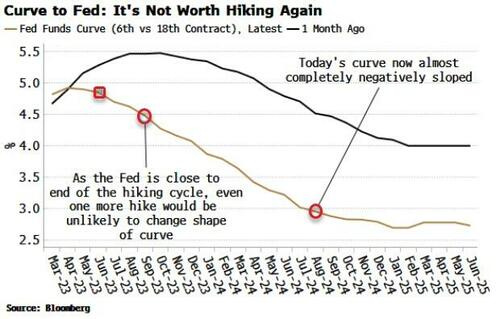

Things could change again of course, but there is a lower cost-benefit for the Fed in hiking again while the short-term interest-rate curve (STIR) is so inverted.

As we saw in this cycle, the curve barely responded to the Fed’s hawkish message. Yet with the central bank now close to the end of its rate-hiking cycle, the curve is even less likely to react to another hike. The curve would remain inverted, and become even more so if the market were to deem the hike would do more harm than good to the economy.

Thus another hike would risk only more downside, while the curve would do little to transmit its inflation-cooling effect. So it’s lose-lose situation.

I still lean towards this Fed hiking cycle being over, with the first cut coming as early as June.

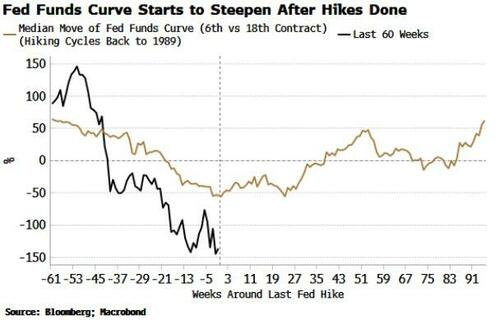

What we need to watch now is the latter part of the STIR curve. Once the Fed has stopped hiking, that typically starts to steepen.

We could see come giveback in short-term yields in the coming days as they are very oversold, but the prospect of a renewed upward trend is looking increasingly distant.

I’ll have something over weekend AFTER all the data dust settles. I’ll wish you all well as you plan your NFP trades and TRADE your NFP plans.