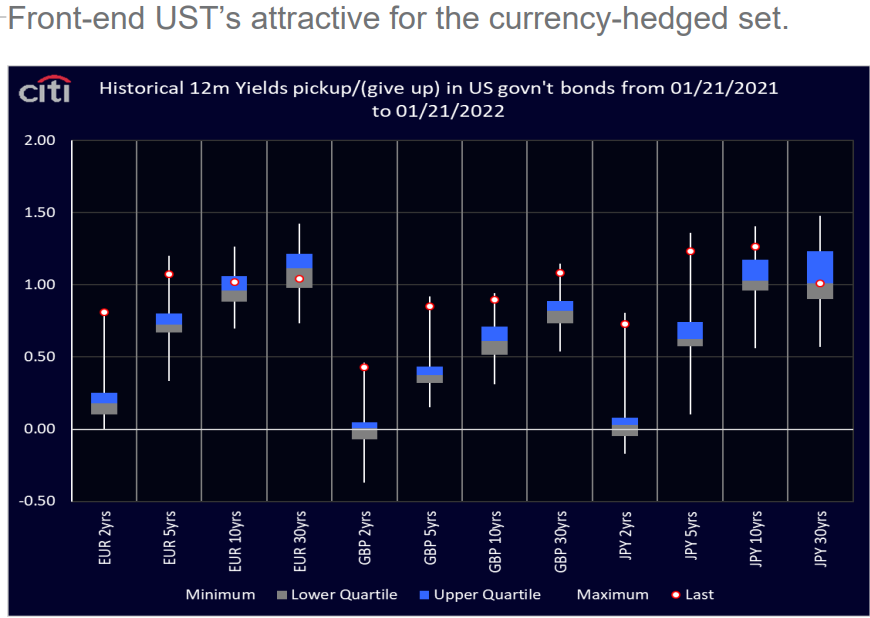

Here are IGMs Press Picks for today (24th Jan) for a few of the important links to press helping explain why stocks are weak on heals of Friday’s poor close and ahead of TODAYS $54bb (-2bb) 2yr AUCTION (which is ‘attractive for the currency-hedged set’.

Here’s what happened overnight, or as they put it,

Treasuries are mixed, off of their earlier highs, and the curve has pivoted flatter around a little-changed 4yr point. DXY is higher (+0.25%) while front WTI futures are little changed (see attachment). Asian stocks were mixed in Japan and China but lower elsewhere, EU and UK share markets are all deep in the red (SX5E -2%, SX7E -1.85%) while ES futures are showing -0.2% here at 6:55am. Our overnight US rates flows saw subdued flows during Asian hours (fast$ sold the long-end, Asian real$ a net buyer of intermediates) after a brief rally on word of Biden's recall of Ukraine families and threat of troop deployments. The geo-politically-driven bid for USTs persisted into London with the fingerprints of a large 10y receiver evident (in futures at least). Overnight Treasury volume was pretty solid at ~150% of average with 3yrs (227%) seeing the highest relative average turnover among benchmarks ahead of this afternoon's 2-yr Tsy auction.

AND a few links from same shop,

US News: Shifts within the bond market are removing a key pillar of support for Wall Street's more speculative bets WSJ The Fed may need to actually sell some of its bonds this time around BBG Inflation poses risk of faster, less predictable Fed rate increases WSJ US food supply is under pressure- from plants to store shelves WSJ Fauci: US Omicron outbreak 'going in the right direction' BBG Biden weighs sending thousands of troops to eastern Europe and Baltics NYT The US and UK embassies order withdrawals from UkraineFT CFTC: USD net longs bets slide to lowest since September 2021 RTRS US investors shun FX-hedged ETF's despite out-sized returns FT

… FX-hedged, matched-maturity yield picks into USTs: On a year-long lookback basis... front-end USTs look very attractive for the currency-hedged set out of EUR, GBP and JPY...

some CHARTS caught my eyes,

Chart of the DAY: What are the implications of elevated levels of margin -- S&P 500 vs Margin Debt

ASC: What Do Stock Market Bulls Have Left (hint, see picture of BONDS)

Barclays: Macro House View Weekly: On the brink - Rate hikes for the Fed and the BoE seem imminent, even as they confront a softening in activity. ALSO CHECK OUT LATEST ON ‘Earl’ — Blue Drum: Riding the storm … We increase our 2022 price forecasts by $5/b to $85/b and $82/b for Brent and WTI, respectively.

Sellside observations (most HATE bonds (haters gonna hate) then there's HIMCO and GMO; a few TRADE IDEAS, too many FOMC PRE-CAPS and victory laps and ... WORDLE?)

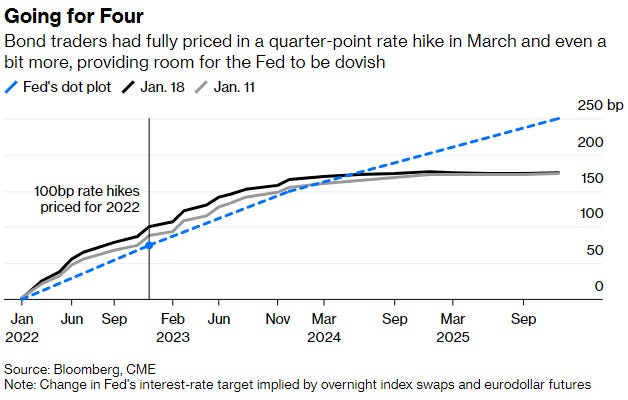

In closing, a Bloomberg VIEW (Chappatta), a good reminder

Sanguine credit markets and a nudge from President Biden to deal with inflation will keep the central bank on track to raise interest rates starting in March.

… And yet bond traders used the sharp move higher in interest rates to push the envelope. At one point last week, 100 basis points of rate increases were priced in for 2022, with bets mounting that the central bank could lift the fed funds rate by 50 basis points in March. That kind of increase hasn’t happened since 2000 but was championed by billionaire investor Bill Ackman as a way for the Fed to “restore its credibility.” Days later, Bank of America Corp. strategists led by Michael Hartnett called policy makers “hysterically behind the curve” and argued they should boost rates by 50 basis points at this coming meeting.

A half-point rate increase this week absolutely won’t happen, and it almost certainly won’t in March, either.

If anything, these splashy hawkish calls are a boon to the Fed because they give Powell and his colleagues more room to be dovish by comparison. The policy statement this week might say something like raising the fed funds rate “may soon be warranted,” setting up a quarter-point move in March. That’s a far cry from the type of panic that Ackman and Hartnett suggest — and yet, just a month ago, only Fed Governor Christopher Waller was explicitly pointing to a likely March liftoff.

Whether sticking to the charted course will cause a stock-market bounce is far from certain, however …

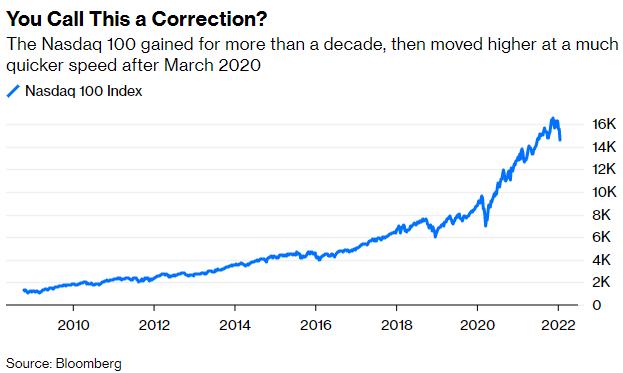

… Whether this latest drop counts as “significant” depends on whom you ask. I tend to agree with my Bloomberg Opinion colleague John Authers, who scoffed at saying the Nasdaq 100 is in the midst of a “correction” just because it fell more than 10% from its peak. This latest turbulence came after a ferocious nearly nonstop rally.

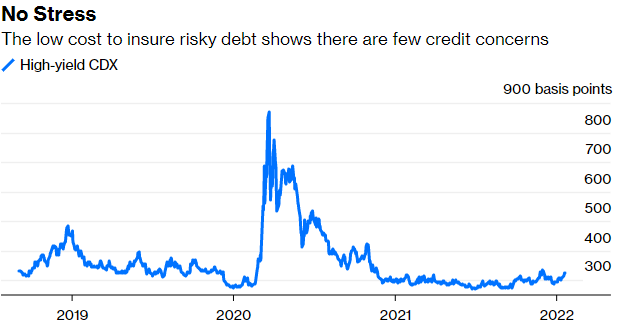

…Most important, credit markets are showing little sign of panic

… Even as the share prices of Netflix Inc. and Peloton Interactive Inc. have plunged, there has been relatively little spillover to the broader corporate-bond market. Markit’s North America high-yield CDX index, which measures the premium demanded by investors to protect against debt defaults, stood at about 321 basis points at the end of last week. By comparison, it reached as high as 485 basis points at the end of 2018, around the time that Powell was forced to abruptly pivot from raising rates to eventually cutting them. On March 23, 2020, the day that the Fed unveiled its emergency credit facilities, the high-yield CDX index peaked at 871 basis points.

… The credit market is quite possibly the most important indicator to watch for an indication that the Fed’s more hawkish rhetoric is adding strain to the financial system that would cause policy makers to back off. For now, Goldman Sachs Group Inc.’s financial conditions index remains more accommodative than any pre-pandemic period and is little changed from October. That’s a clear go-ahead for the central bank to proceed as planned.

I’ll leave you with a look at 2yy WEEKLY ahead of this afternoons featured liquidity event.

Interesting level to pause (which may refresh, esp on FX hedged basis)?

That’s all for now. Have a great start to your day and week. Get those 2yr auction bids in early and often!