Good morning … Um, where to begin? Setting aside what COULD be viewed as choas within BoE as they hiked rates 50bps TO 2.25% (FIVE BOE OFFICIALS VOTE FOR 50BP HIKE; 3 FOR 75; 1 FOR 25, full schtick HERE), I’ll stay in my lane, focus on message continues to eminate from the worlds CB — the US Federal Reserve — where just yesterday, JPOW SAID,

… If we want to set ourselves up for another period of very strong labor market, we have got to get inflation behind us. I wish there were a painless way to do that. There isn't.

JPOW at his news conference via Yahoo.com HERE. It’s NOT hype it’s just our reality. Sooner we come to grips with the facts of what the Fed can and is willing to do to, you know, impact DEMAND curve, the better off (prepared) we might be … The LONG BOND thinks IT is the solution, trading back ‘down’ to June peaks,

DAILY momentum having crossed (bullishly) is worth noting but for now, here is a snapshot OF USTs as of 712a:

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT The Treasury curve has pivoted further flatter around a little-changed 10yr benchmark amid a cannonade of central bank rate hikes and Japan's first FX intervention since 1998. DXY is higher (+0.35%) while front WTI ftures are too (+1%). Asian stocks fell following NY's late swoon yesterday, EU and UK share markets are mostly lower (SX5E -0.85%) and ES futures are modestly lower (-0.13%) here at 7:15am. Our overnight US rates flows saw Asian real$ selling in the front end and solid 2-way activity in the long-end. In London's AM hours, the desk noted all the trading concentrated in the front end ahead of the BOE decision. They also mentioned ongoing demand for long-end real rates as a theme there (see attachments). Overnight Treasury volume was very solid overall (~175% of average) with 2's (267%) seeing the highest relative average turnover among benchmarks, matching our flows.

… The Treasury 20+ year ETF, TLT's, is showing hints this morning of a new tactical rebound in motion with daily momentum (lower panel ) now flipping in favor of a looming rebound in prices amid evidence of triple Bullish divergence (lower lows in price since late August , higher lows in momentum)- an oft-reliable trend reversal set- up . 30yr Treasuries (not shown) also show a similar bull set-up after being chronically 'oversold' since late August.

… and for some MORE of the news you can use » IGMs Press Picks for today (22 Sep) to help weed thru the noise (some of which can be found over here at Finviz).

We’ve reached that part of the programming where I’ll bring forward a couple / few things — sellside or widely available on the intertubes (ZH, etc) which, in my former institutional FI role, might have some funTERtainment value…

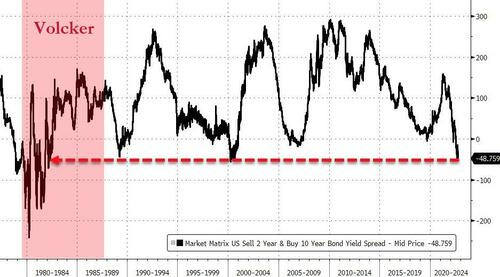

… The 2s10s curve hit -52bps intraday, very close its most inverted since 1982 (during Volcker)...

HERE is one from BBG putting some context to Fed forecast of 4.4% URATE which, they (economists) say will be equivalent to losing of 1 million jobs

The FOMC dust is still settling but there is no doubt this was a hawkish meeting. The new dot plot shows a terminal rate of about 4.6% in 2023, higher than an already-hawkish market was pricing. The latest projections also included lower growth forecasts and higher estimates on inflation. But a key figure from today’s meeting was Fed’s view on unemployment, which was ratcheted up to 4.4% from 3.9% in June.

That would amount to job losses of more than 1 million, assuming no change in the size of the labor force, according to economists. That’s a hard one to swallow for markets as it suggests the chances for a “soft landing” have greatly diminished. And most policy makers understand that. A jump to 4.4% in the unemployment rate from the current 3.6% level would meet the so-called “Sahm Rule” for identifying the start of a recession, according to Bloomberg Economics’ Anna Wong, who thinks it’s actually more likely that jobless rate would have to go to 5% to slay the inflation dragon.

Fed and related things aside, an important note from a large UK-based bank,

Central clearing comes to Treasuries Last week, the SEC released a proposal that would expand central clearing in Treasury cash and repo markets. Our preliminary reading is that these changes will reduce market risk and expand intermediation capacity but with higher transactions costs. But who pays is uncertain.

In OTHER news which has flown by underneath the radar screen for obvious reasons,

ZH: Nobody Has Traded 10Y Japanese Govt Bonds For 2 Days!

ZH: Yentervention! Japan, BOJ Enter FX Market With "Bold Action", Send USDJPY Tumbling

And a large GERMAN Bank weighs in this morning on how THAT is expected to go,

JPY intervention - unlikely to work The Japanese authorities intervened in the FX market a few hours ago to strengthen the yen. While this may help reduce some speculative positioning over the next few days, we are highly doubtful this will work in turning the yen trend …

… 3. Intervention has not worked in the past. The Japanese authorities have historically defended USD/JPY from below rather than above (chart 1). There is only one period of sizeable JPY buying operations in late 1997 and 1998. The first two saw new highs in USDJPY reached within a month; the last one in June “worked” but only because the LTCM crisis quickly followed.

Finally, one from the CHARTS department and the shop formerly known as (and perhaps again in the future) 1stBOS

* Going into the FOMC meeting this evening, rates markets are delicately poised around key technical levels, with the 10yr US Bond Yield oscillating around its prior 2022 high at 3.50%, US 2yr Bond Yields at our “measured triangle objective” at 3.905/4.00% and US 10yr Real Yields also at major support at their 2018 high at 1.17%.

* Our view is not to chase yields higher for now, with the latest push higher in yields for all 3 of these markets occurring on slower momentum compared to earlier this year, which has historically occurred around important peaks in yields.

* Furthermore, we believe a hawkish outcome would likely trigger a sharp move lower in US 10yr inflation expectations, which are close to confirming a major top, as well as trigger further curve flattening, both of which should limit the upside potential for long-end nominal yields. In contrast, an outcome in line with market expectations could trigger a reversion in US 10s back into their range, which could result in an important false breakout.

* Our view for European Fixed Income is very similar; German 10yr Bond Yields are testing major support between 1.895/93% and 2.00/2.045%, which we expect to cap, with a flattening bias still our higher conviction view.

* For these reasons, we reiterate our neutral stance on government bonds on a 3-6 month horizon from a technical perspective at this point in time.