As a card-carryin’ TRANSITORIAN early on, believe me when I say I DO sympathize. I’ve been there but just long ago … coming to realize just how powerful were the consequences OF elections.

Off THAT soapbox, HEREis where you’ll find links thru to exactly what it wasJPOW SAID (go ahead and watch the video if you missed it.

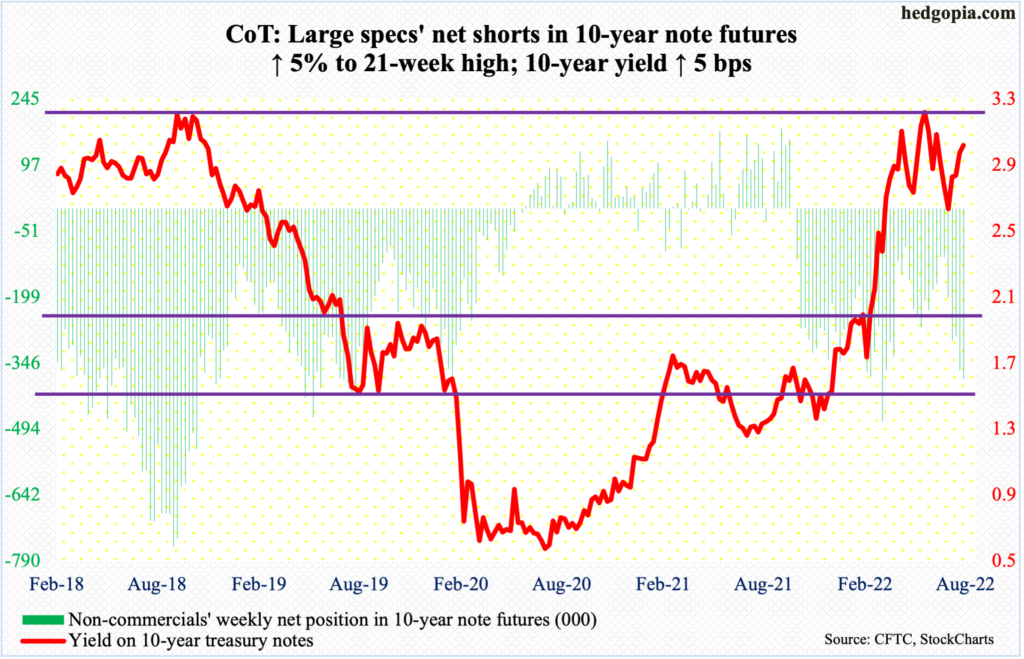

Here’s a look at 2yy, WEEKLY, for some context

Ok, then. Room to run … for somewhat more techAmental look at where they MIGHT GO …

They are all my favorite and you’ll find some trade ideas / convictions reiterated (2s10s flatteners seem to be everywhere and a few have updated rates forecasts (NWM for example).

… 2. Negative real wages will squeeze consumer demand.

This is another narrative that's still repeated regularly on financial news networks. This view is very backward looking, and ignores the fact real wages rose by 0.5% m/m in July. This was the first monthly increase since September 2021, and the largest gain since Dec'20.

Real wages will almost certainly rise again in August, given the fact that the CPI on track to contract by 0.1% m/m. With consumers spending less on gasoline, discretionary spending - and real spending - is set to accelerate.

Although nominal spending underwhelmed in July, rising by just 0.1% m/m, real spending increased by 0.2% which still puts real consumption on track to be up 2.5% in Q3. This would be the fastest growth rate since Q4.

On top of that, net exports are likely to be very additive to GDP in the third quarter. The goods trade balance narrowed by $9.5bn in July, and it has now fully reversed the Nov-March widening. We estimate that real imports declined by 2.1% m/m last month, while real exports rose by 3%. If both stay at their current levels through Sep, trade will add 2%-3% to Q3 GDP. Net, we still expect GDP to expand by more than 3% in the third quarter…

I dunno. This shop is one of those I respect quite a bit. Perhaps my brain is still in summer mode and, well, I’m not swayed…yet.

Here are a few other items // things // links from the intertubes

We estimate that debt cancellation alone will cost up to $519 billion, with about 75% of the benefit accruing to households making $88,000 or less. Loan forbearance will cost another $16 billion. The new income-driven repayment (IDR) program would cost another $70 billion, increasing the total plan cost to $605 billion under strict “static” assumptions. However, depending on future IDR program details to be released and potential behavioral (i.e., “non-static”) changes, total plan costs could exceed $1 trillion.

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Finally, beginning this short summer-ending note with a visual I’ve gotta end with one. Here’s a look at what Friday’s market would be IF it were a scented candle

… THAT is all for now. Off to enjoy the remainder of the weekend and the last nuggets of summertime. And while I’m ‘off’ Monday and Tuesday, regular updates may be somewhat less regular…

{kind=link}