I will editorialize lots less today than usual given festivities of the weekend (‘Thing 3’ turned FOUR-teen yesterday and tailgate for the big game about to start!!

That said, lets jump right in … first a couple pictures of the ‘damage’ in the (long)bond market last week … first a DAILY,

… you can clearly see the goalposts and TLINES are needing to be redrawn. Next time I’ll do it with a pencil with an eraser — you know, the kind you never see on a golf course!!

Here’s a WEEKLY look for some further perspective,

It does appear that bearish momentum (stochastics, bottom panel have only just crossed SO … 6 more weeks of ‘winter’?)

Moving right along TO a few sellside observations from Global Wall Street’s narrative creation machine. Things I noticed will cobbling THIStogether, stocks overvalued vs bonds (ARGUS), firms turning NEUTRAL USTs from short (Barclays, TD) and some getting stopped OUT of positions while looking to buy dips (BMO).

Theres more. MUCH much more … have at ITbefore your pregame tailgate gets going.

In addition to some of THESE VIEWS, a few other links which may be of interest.

Wolf Street: CPI Just Got Revised Higher for October through December. The Revisions Take a Bite out of “Disinflation” Hoopla

For MORE along these very same lines,

ZH: Disinflation Trades To Soon Hit The Rocks As Prices Stay Sticky

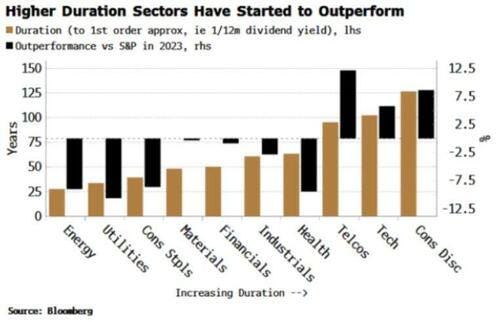

…This year, higher-duration sectors, such as tech, telcos and consumer discretionary have led stocks’ advance, while low-duration ones such as energy and utilities have underperformed. This is a reversal of the trend from late 2021, where investors started to shun high-duration stocks as inflation began to rise rapidly.

…Investors re-embracing higher-duration stocks is a signal they are also embracing the disinflationary narrative, one endorsed by the Fed and priced in to inflation swaps…

… The bigger trend of lower-duration sectors outperforming – encapsulated in the energy vs tech stock rotation – is likely to re-assert itself sooner rather than later, taking the market lower with it.

Yardeni on CPI: January's CPI Is Coming. Run For The Hills?

On CHINA data being far more consequential than Japanese,

ZH: China Data More Consequential For Global Markets Than BOJ

… Moreover, capital outflow has decreased markedly from China, which will also significantly improve domestic liquidity conditions.

It has been easy to jump the gun with China, but it looks like it’s back as a global economic driver.

This has implications for global demand and supply, but one of the most direct G7 beneficiaries is likely to be Europe.

Camp Kotok (which I’ve not yet been invited TO although former colleagues of mine have attended), notes,

… While there is a short-run tradeoff between unemployment and inflation, it has not been observed in the long run. In 1967 and 1968, Friedman and Phelps asserted that the Phillips curve was only applicable in the short run and that, in the long run, inflationary policies would not decrease unemployment. Friedman then correctly predicted that in the 1973–75 recession, both inflation and unemployment would increase. In the 2010s, the slope of the Phillips curve appears to have declined and there has been controversy over the usefulness of the Phillips curve in predicting inflation. A 2022 study found that the slope of the Phillips curve is small and was small even during the early 1980s. Nonetheless, the Phillips curve remains the primary framework for understanding and forecasting inflation used in central banks.

…The chart below breaks down the weekly AAII bullish (top) and bearish (middle) percent readings, along with the spread between the data series shown in the bottom panel (Bull-Bear Index).

Bullish sentiment has been trending higher since the start of the year, lifting the bullish percent from 20.5% at the beginning of the year to 37.5% as of Thursday, February 9. While this has been a welcomed improvement, the most recent reading is only back to its long-term average (green dotted line at 37.5%)…

… In conclusion, bears finally appear to be hibernating as bullish sentiment improves. Historically, the end of prolonged periods of bearish sentiment has usually led to above-average market returns over the next twelve months. While sentiment is clearly not a science and is often best utilized as a contrarian indicator, the recent transition toward improving optimism suggests investors are becoming more confident with the latest recovery in stocks, something absent from prior recovery periods in 2022.

Last link from the intertubes and one with some Super Sunday implications — for stocks (because, you know, nobody ever does this kinda research ‘bout bonds)

Moving on then TO the week ahead AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

I hope you enjoy your tailgate as much as I plan to enjoy ours here and doing so fresh on heels of celebrating ‘Thing 3’s “FOUR!”-teenth birday at Swing Loose indoor golf center yesterday … here he is with 3 of his buddies — ‘Thing 3’ is the awkward looking teen boy,

THAT is all for now. Enjoy whatever is left of YOUR weekend AND the big game and for now …