Good evening and I hope y’all had as nice a weekend as I did.

Thing 1 making tackles (on special teams), honored for his 4 years of playing and service TO the WPI football team, honored (again 4th year in a row) with 2022 All-Academic honors in his conference and so, we honored ALL his achievements — including his job offer to be accepted first thing Monday morning — with what was an overall outstanding weekend … save for the loss TO MIT…

That is a wrap!!

All the brag aside — sorry NOT sorry — HERE are just a few observations from Global Wall Street and FI / macro research departments OUT Friday … That extra day gave some — Morgan Stanley — the time needed to cobble together some 2023 year ahead outlooks. Please NOTE

All Downhill From Here? A week that started with a wall of worry that the Federal Reserve’s ever-higher rates path meant endless pain for bonds ended instead with an epic rally. The trigger was the first serious downside surprise for inflation in a long time. Headline annual CPI came in under the weakest survey estimate, something that hasn’t happened since late 2020. That brought enormous relief across assets, especially after Federal Reserve Bank of Philadelphia President Patrick Harker said he expects the pace of hikes to slow.

Investors were already facing a messier — though potentially more hopeful — outlook for bonds as the world’s most aggressive and synchronized monetary policy tightening in 40 years enters a new, less monolithic phase. The International Monetary Fund underscored optimism a global policy pivot is coming when Managing Director Kristalina Georgieva said inflation may be close to a peak, even though she also warned it could stay stubbornly elevated. The ECB meantime offered reassurance euro area lenders can handle a spike in interest rates, saying the benefit to earnings would alleviate the hit to capital ratios.

Just when the market was resigning itself to the idea that the much-awaited yield peak would go on receding, it may instead have arrived with a very loud bang…

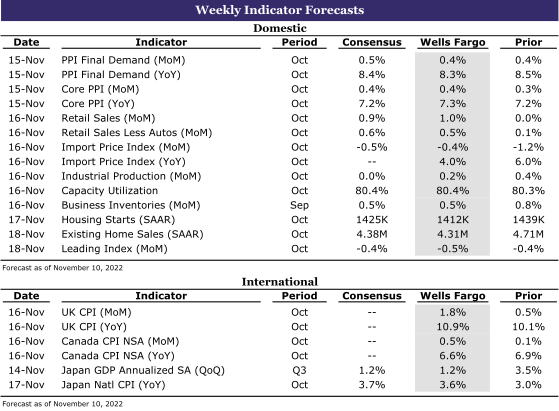

Moving on then TO the week ahead AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,