Sellside observations (Jan 15th, 2022)

rates, macro econ, Fed and other CBs with a touch of equity views and more...read this and remember, "Lets be careful out there"

HERE are a few words from our Global Wall Street ‘sponsors’ as the dust settles.

I’ve taken the liberty to compile THESE research notes / thoughts to consider before the holiday-shortened week just ahead as ALL US EQUITY markets will be closed on Monday, January 17th in observance of Martin Luther King Jr. Day., and oh, yeah, BOND markets, too).

THIS PDF is a compilation of ‘views’ and ideas. Gotta read as many of them so as we can pick out the good vs the bad.

I will keep my views to myself … I will continue to let prices speak for themselves and here’s a WEEKLY visual of 20yy (since reintroduction), for example, given the ‘liquidity event’ in the week ahead.

I’ve noted a prior instance when 20yy momo was overSOLD (so, cheap up near 2.40%) and while not yet showing ANY signs of rolling over bullishly, a concession ahead of this weeks liquidity event might be worth a look. Daily and hourly charts avail, just reach out and ask…

Global Wall Street are — as always — out sellin’ a narrative hard and fast and I’ve COBBLED TOGETHER THIS PDF as a sort of ‘cliff notes’ version for the rates PM, macro trader and those other degenerate research junkies, highlighting notes that have hit inbox over the course of the week — up until late last night. I have not yet had time to read them all … ZH is good, don’t get me wrong. I like all the rest of the context.

I’m doing this for ME so as to stay marginally attached to a rates market labor force (how am I counted — this coming weeks claims data is for next NFP survey week) because after doing this for the better part of 30yrs, well, I quite like ‘the game’. And quitters never win and winners never quit.

Making NO mistake, that is just what it is. A GAME. Some play chess, some play poker, others get paid to make guesses (weathermen, economists, bond strategists) and still others get paid to run money. (OK, some do it all and my hats off to them).

Back TO matters at hand and the foundation to it all.

RATES — the wind beneath global markets wings — had a rough end to the week (but didn’t log another rough year, last week).

Maybe, just maybe, the problems in the bond market are — like all other issues in the world at the moment (prices at the pump, store shelves/inventories/ReSale TALES) related to SUPPLY and BOTTLENECKS.

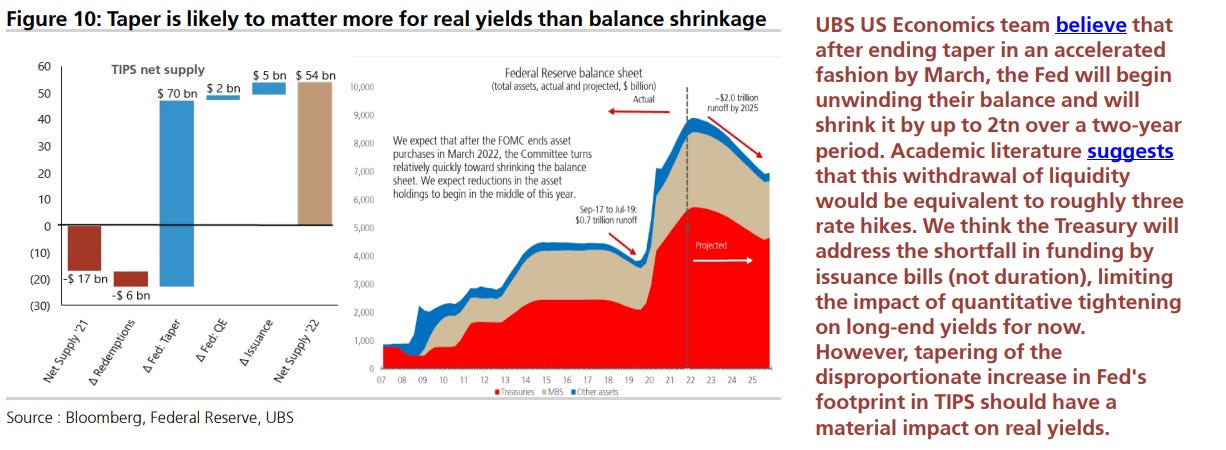

For somewhat more on the mismatch which has every bond bear salivating (supply / demand mismatch) see GS note (mentioned below) which, generally speaking, can be summarized by this one visual from JPM (via ZH tweet of GLOBAL QE)

Or THESE — not mentioned by ZH — but you’ll find them all HERE (with context)

Balance sheet shrinkflation clearly on the brain.

The following sellside observations are time / date stamped to the best of my ability and in alphabetical order. THESE WORDS are far from gospel BUT a cross section of what it is they are sellin’.

An alternative title for this post COULD have been,

source: "Marketing B.S. Detector" (and all of Global Wall Street).

HERE with a large grain of salt, I’ll reiterate that I’ve NO idea WHY I’m doing this.

It has always been a learning (for me) experience as well as time saving effort (for you) and the contents of THIS PDF are for information ONLY.

NOT views I share but rather something for us all to read / refer back to in-between wildcard games this weekend AND ahead of global markets open (HERE for 2022 holiday calendar post) Sunday evening (economic calendars will be forthcoming)

A few things which caught MY EYES over the course of the week:

GS: US Treasury Demand in 2022 … Taking all this together, the net rates market impact of the supply/demand mix remains somewhat in flux. If Treasury forgoes upcoming cuts to coupon supply in light of an earlier runoff baseline, levered funds could potentially become the marginal buyer of USTs. The concession needed, particularly on balance sheet intensive cash assets like USTs, will therefore likely rise—which could pose a headwind for swap spreads as well as duration more broadly. Alternatively, if the Treasury pursues a more bills focused approach in raising additional public financing, the rates market impact of the supply/demand shifts would be much more benign.

In other words, not even GOVERNMENT SACHS knows but that doesn’t seem to have slowed down ANY calls for higher rates and/or the bear flattener…

There are a few charts / words on (closed end)bond fund LIQUIDITY,

McClellan’s weekly Chart In Focus: Bond CEF A-D Line Showing Liquidity Problems … Most who hear this message about the current divergence between the SP500 and the Bond CEF A-D Line won’t believe in it, because these bond CEFs are interest rate sensitive contaminants to the proper A-D data. This is actually fine with me that they don’t believe in it.

Bucking the trend of 2018 analogs generally speaking, McClellan went full 2007 / 08 FLASHBACK CHART (HERE)

{kind=link}

And what would a 3rd week in January be without modifications to year ahead outlooks before any of the ink has even dried. For the latest, see

MS: More Tightening Than You Think …

4 hikes (March, June, Sept and DEC), QT announced in JULY (beginning in 2mo) to max caps of $50bb USTs / $30bb MBS by Sept (and 2 more hikes in 2023). With all this, raise RATE FCASTS UP now seeing 10yy @ 2.20% in 2Q22 and 2.30% by 4Q. This is NOT WITHOUT CONSEQUENCE — Stock Jockey in chief sees S&P DOWN 10-20% in H1 (base case target 4400) which is also associated with ‘modestly wider credit spreads and WIDER MBS spreads, too. Leaving one / all wondering what kind of widening will take for something (else) to break…

Now MSs WEEKLY rates and global macro strategy DOES warrant further inspection, asking and answering,

Are Government Bonds a Buy? Not yet. The repricing of duration to start 2022 signals risk of higher yields ahead, instead of a gift for those with excess cash. Too many central banks are on the move or sending signals, rendering traditional cross-market valuation metrics less reliable. Seasonality also favors patience.

They talk at length about how FX - hedged yields may NOT be all we think AND talk directly TO one case for range-bound bond market or a defacto yield cap (EZ and JGB yields)…In the end, they

… maintain UST 5s30s curve flatteners, and 2s5s curve steepeners vs. long 30y UST…

And there’s MORE … MUCH, much more.

Dare to explore — THIS PDF — as you wait for HIMCOs Q4 note to drop and the games to start!

Enjoy long-weekend ahead. Hopefully the storm forecasts are as good as many rate forecasts in years past…and remember … on this day back in 1981,