Rolling With Inflation Was a Winning Move in 2021

Cam Crise (aka Macro Man) of BBG out with some non-predictions...

I LOVE predictions about the future (of markets and global macro) and cannot help but think about them as Yogi Berra (It’s tough to make predictions, especially about the future) and so, as one of BBGS own Mr Macro grades his 2021 predictions (#3, #6 are clearly most interesting to ME), here are his grades of his NOT predictions - 2021 - for your dining and dancing pleasure. I’ve attempted to add some visuals best I could but without Terminal, well, I’m still figuring out my way

Rolling With Inflation Was a Winning Move in 2021

(Bloomberg) -- While financial markets are still moving with sufficient vigor to merit the attention of portfolio managers and traders, for many this year is pretty much already in the bag. As such, focus is shifting toward 2022, and catering to that attention is a veritable mountain of outlooks detailing what will (and won’t) happen next year. For credibility’s sake, however, it’s an important and useful exercise to assess how one’s past predictions have come to fruition. As a reminder, it’s a long-standing tradition of this column to make non-predictions -- forecasting what won’t happen in the year ahead. So before looking ahead to 2022 on Wednesday, let’s grade this column’s outlook for 2021:

Non-prediction 1: Inflation will NOT stay under the radar. The entire thematic backbone of last year’s outlook was dominated by inflation; while this may seem obvious in retrospect, it’s worth recalling that the consensus forecast a year ago expected headline CPI to be 2% and core PCE inflation 1.7% by the end of this year. Last year’s outlook noted that “it’s an interesting question of what would happen if pent-up demand meets constrained supply” -- that’s pretty much the economic story of 2021 in a nutshell. While the pace of inflation handily exceeded what I thought was likely, this one is a pretty clear and obvious HIT.

Non-prediction 2: Fed QE will NOT stay at the current size for the entire year. Again, this is one that seems obvious in retrospect, and it’s easy to forget that 12 months ago a number of economists thought that the Fed wouldn’t hike rates until 2024. A tapering this year was by no means clear at the end of 2020, even if the degree of accommodation already seemed excessive given the recovery in financial markets (which are, after all, the transmission mechanism of QE.) Regardless, the Fed tapered, and then they accelerated the pace of that tapering. Another clear HIT.

Non-prediction 3: U.S. 60/40 will NOT outperform the rest of the world. It seemed so obvious: Under-appreciated inflation pressures forcing an acceleration of the policy normalization timetable -- could there be a worse recipe for U.S. financial assets? Yes, as it turns out. Rampant earnings growth proved sufficient to propel U.S. equities to another year of outperformance versus the rest of the world. Meanwhile U.S. aggregate fixed income barely underperformed the likes of Europe in local currency terms. Add in a much stronger dollar, and betting on the rest of the world was a glaring MISS.

<SIDEBAR, 60/40 … NOT dead yet>

Non-prediction 4: Tesla will NOT close 2021 with a positive share price return. For better or for worse, Tesla is more of a religion than an investment proposition, and it was probably foolhardy to hazard a forecast in the realm of financial theology. The thesis was essentially that the stock was ludicrously valued and that its entry into the S&P 500 represented some sort of “ring the bell” moment marking a top. While some of the company’s most notable supporters have seen their fortunes wane in 2021, I underestimated the clout of zealots with option-trading accounts. MISS.

Non-prediction 5: European banks will NOT fall again in 2021. The euro-zone banks index, the SX7E, has had a torrid time of things over the past decade-plus, registering seven annual losses against just four gains from the end of 2009 though last year. Financial repression explains some of this shoddy performance, given the negative yields that avail across the high-quality euro-zone sovereign universe. The thinking was that the ECB’s tiering program would mitigate some of the more pernicious impacts of QE, thus allowing banks to score a rare winning year amid a backdrop of ongoing asset purchases. At the time of writing, the SX7E is up more than 31% in price terms, its best year since 2009. HIT.

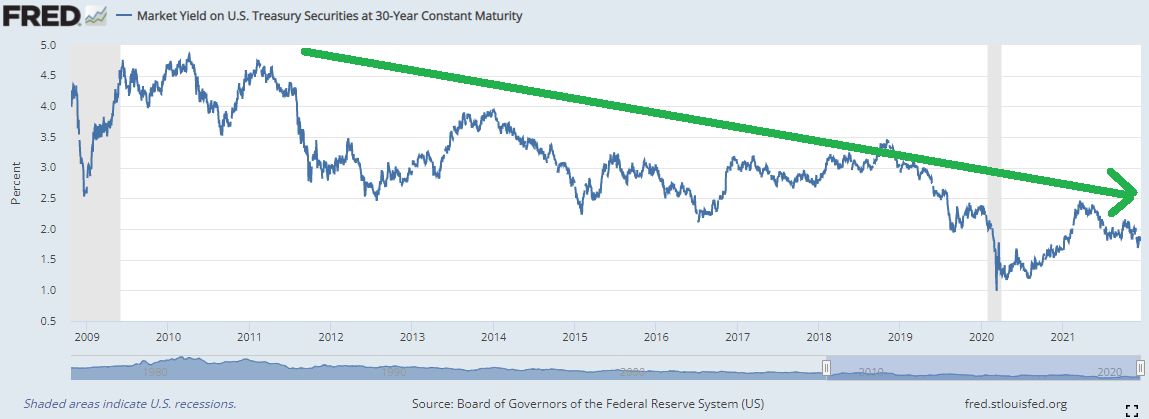

Non-prediction 6: U.S. 5s-30s will NOT close 2021 above 150 bps. A year ago steepeners were still in vogue, and if global central banks had remained relentlessly dovish against a backdrop of elevated inflation they probably still would be. Given the expectations for prices and policy cited above, however, the thinking was that yields in the belly would outperform to the topside ... and in the event that nominal growth was lower than expected, there was more room for the long end to rally. While 5s-30s traded up to a peak near 167 bps in late February, five-year yields have duly risen this year more than any other point on the benchmark curve ... and 5s-30s has flattened hard. HIT.

Non-prediction 7: USD/CNH will NOT close more than 25 big figures away from 6.53. It seems strange to read, but in the original outlook this entry refers to the expectation of broad dollar weakness for 2021. It didn’t play out that way, of course, though the dollar did drop against the yuan thanks to record trade surpluses and high PPI inflation in China. Still, the underlying premise was that the authorities wouldn’t want too much overt appreciation, instead favoring broad stability in uncertain times. That’s pretty much how things have played out, even if the market backdrop was very different from the one envisaged. HIT.

Non-prediction 8: The MOVE index will NOT end 2021 below 50. The index of fixed-income volatility spent most of the second half of last year (other than the run-up to the election) below 50, a threshold that had essentially never been breached prior to 2017. With the market sanguine on inflation and expecting little change in monetary policy this year, I suppose it was understandable why it once again traded below 50 last December. But the inflation prognosis underlying the outlook augured something of a nasty surprise, and so the call was for a normalization of rates vol. That duly materialized in February, and while the MOVE briefly dipped back below 50 in June, it’s currently trading north of 70 even after a recent dip. HIT.

If you get your big-picture theme correct, then you’d like to think that you’d nail most of your forecasts. It doesn’t always work out that way, of course, which is why Harry Hindsight seems so much smarter than Freddie Foresight. Last year’s outlook rolled the dice with inflation and nailed the big theme of the year. The hit ratio for the non-predictions as a whole was a solid 75%, the best since I’ve been doing this column for Bloomberg. But that’s in the past now; on Wednesday, we’ll have a look at what won’t happen in 2022.

For MORE of how some others on the sellside graded themselves (A+++ for rates stuff), make sure you check out THIS (hint: wathching 2s5s and 30yy)