JPM inboxed this earlier this morning so I thought I’d share. I’ve no opinion on it (complete untruth — see very bottom for quick comment on title of the report — but think about it — IF reflation endgame is being written about, what then comes NEXT), other than it being something else to read / consider in-between football games …

The superheroes on the cover have all contributed in their own way to a reflating world: higher nominal growth, higher wages, higher prices and rising asset prices. While the COVID recession was deeper, the global recovery is on track to eliminate spare capacity at a much faster pace than after prior recessions. Global inflation is close to the highest level in 20 years, driven by surging goods prices and changing consumption patterns due to COVID, the inability of a just-in-time corporate sector to respond, soaring government debt1 , monetary policy that dwarfs anything seen after the Global Financial Crisis a decade ago, and energy policies which reduce the supply of thermal energy much faster than they reduce demand.

… Bottom line: the Fed is now facing the largest challenge yet to its “transitory” description of inflation dynamics. We agree that goods price inflation will roll over, in which case CPI and PCE measures will as well. But we believe that wages and commodity prices will remain high since their supply/demand curves have shifted.

The executive summary includes a WHATS NEXT for stocks which everyone knows is dependent on REALZ,

… While the Fed is expected to raise policy rates next year and slow the pace of its asset purchases, we think the most important question to ask is this: what is the Fed’s endgame, positive real rates or just real rates of around zero? We believe it’s the latter. As illustrated on the left, the Fed now uses an approach which yields much lower equilibrium real policy rates. Most of the reason for this decline: aging demographics, slower trend growth and income inequality which offset the rise of government debt3 . As a result, maybe real yields crawl back to zero at some point, but that’s as far as we could see them going in the US or Europe. Also, while the Fed is expected to scale back its asset purchases, our economists still expect another $1 trillion in developed market central bank balance sheet expansion through December of next year.

Suggesting the Fed desires a ZERO REAL rate is, in my view, a big ask and as we all know, nothing can / will happen without some other form of consequence. Thankfully, CONTEXT offered — global central banks will continue to GROW balance sheet — SO it’s not as if the Fed is the sole punch-bowl operator. We just like to jump to that conclusion, whenever it’s convenient.

That in mind, some general BULLETS to consider

Be prepared for intermittent selloffs, since market internals are less favorable than they were last spring:

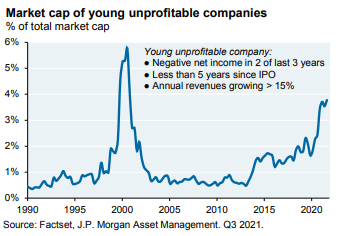

Young and unprofitable companies make up the largest share of market cap since 1999; Bridgewater estimates $200 bn in “YUC” supply in 2022 from primary/secondary issuance and insider lockups expiring

There were a lot of highly valued, crowded-trade stocks which fell by 35% or more in 2021, which is unusual for a year when market returns were ~25%; another development we have not seen since the late 1990’s

A rising number of companies are now more sensitive to changes in liquidity conditions and monetary policy than their counterparts that are more sensitive to changing economic growth

There’s a high concentration of S&P 500 market cap and total return that is reliant on a handful of stocks; excluding the top 5 stocks, the NASDAQ was actually down 20% through mid-December

Signs of weakness in momentum/liquidity plays (fintech, renewable energy, IPOs and SPACs)

… and HERE is link to the entire the latest 46pg report from JPM

So as one reads and absorbs this all, consider that if reflation endgame is near, what is on the other side? DE/DIS-inflation? Clearly not this weeks business but perhaps some food for thought especially for your inner, more strategically minded portfolio.