Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this abbreviated note…

Sending this now as I’ll be outta pocket tomorrow, returning to full spammation capabilities Friday morning …

I would like to take a moment and offer a couple things which helped define the day which just passed. First, jobs …

… Somewhat more …

ZH: ADP Reports Biggest Disappointment In Job Gains In 2 Years In February

… and then there was SERVICES …

ZH: US Services Sector Surveys Beat Expectations In February As Jobs & New Orders Jump

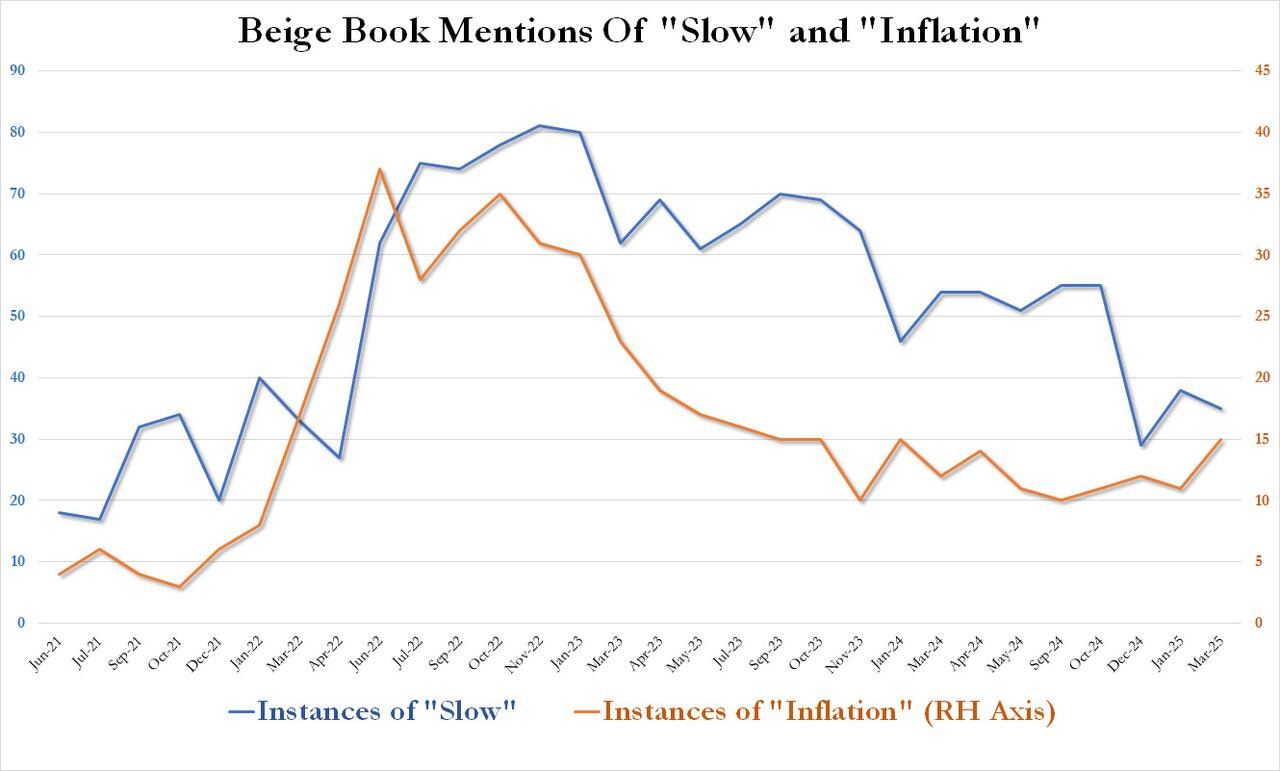

This all followed up by a heaping dose of … BEIGE …

ZH: Beige Book: Economic Activity, Employment And Prices Rose Since January, Economic Expectations Are "Optimistic"

… Confirming that contraray to conventional wisdom the economic picture improved notably since January, the latest February Beige Book saw just 2 mentions of recessions, down sharply from 6 two months prior. But more notably, while mentions of "slow" extended their decline to 35 from 38, mentions of inflation rose to a two year high of 15, up from 11 last month...

... suggesting that the US economy - while hardly on fire as it was during the hyperinflationary period of Biden's admin - continues to chug along and is hardly collapsing as so many Trump foes would like to see.

… and this all incorporated into price action by days end resulting in …

ZH: Stocks & Bond Yields Jump As Trump 'Eases' Tariff Tensions, Germany Goes Nuts

…Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

Another day, another set of tariff news and VIEWS. Here’s one …

ABNAmro: China - More US tariffs, more support | Insights newsletter

US raises China tariffs by another 10%; Beijing again retaliates immediately and targeted. Tariffs implemented still fit with base case assumptions, but more may come. Stepping up of support confirmed in annual work report to National People’s Congress. We also see upside risks to our 2025 growth forecasts despite tariffs.

… Here’s another such note and view on tariffs AND visual context on length of his speech cuz, you know, THAT is really important (?) …

On Tuesday evening, following implementation of new tariffs on Canada, Mexico, and China, President Trump delivered his first address to a joint session of Congress in his second term. In our view, the speech had few new policy details and no reassurances that markets were seeking on tariffs.

…FIGURE 3. Length of presidents' annual addresses to Congress (1964-present)

… so, somewhat LONG speech last night and the view is a more bearish take, counter TO what markets priced in (early, at least) …

Same shop with an update on services …

Barclays: February service PMIs: Still resilient, for now

The ISM services PMI strengthened in February, staying well within the range seen for some time. As such, in our view, this downplays indicators that markets had been interpreting as signs of weakness. These readings do not reflect any potential softening after March's tariffs on Canada and Mexico.

There is a notable divergence in the market at the moment between the massive selloff in German bonds and the bid for the front-end of the US Treasury market. This dynamic was made all the more striking by the fact that ISM Services unexpectedly increased and was accompanied by the strongest employment component since December 2021. The push toward higher German yields was a fiscal story, following proposed sweeping fiscal reforms that would lead to hundreds of billions of euros in spending for defense and infrastructure. One could argue that it is long overdue for Germany to ease its self-imposed fiscal constraints. Regardless of one’s stance on the timing of the shift, the economic and issuance implications are being interpreted as especially bond bearish for the Bund market. There is nothing that necessitates the US Treasury market following suit toward higher long-end rates, although the absence of a meaningful sympathy move does warrant highlighting….

Pending macroeconomic impacts from tariffs look larger than we had embedded in our base case. The Trump administration has taken the trade war to a new level by imposing a 25% tariff on Mexico and Canada and an additional 10% on China.

The situation remains fluid. Much will depend on whether these new tariffs prove temporary or are toned down. But even if they are ultimately removed, we anticipate lasting damage to global economic activity.

What’s more, this does not preclude further escalation in the near term, via an extension of the geographical scope of tariffs – with the EU in the firing line – or through retaliation from trading partners.

We outline four tariff scenarios as a device to help quantify the potential economic implications for the US, Mexico, China and the eurozone.

The initial market reaction to the latest tariff announcements has been relatively muted. But we see scope for the pricing-in of substantially greater impacts the longer tariffs stay in effect. This implies MXN, CAD and CNH weakness, lower US real yields, higher US inflation expectations and a flatter UST curve.

France (re)sent an update after I hit send and had several new trades, one specifically caught my attention …

BNP: Quant Trades of the Week: Six new trades: Short USD, rates and equity RVs [RESEND]

KEY MESSAGES Market themes

December’s tightening in US financial conditions may weigh on hard data releases near term, our modeling suggests. But the subsequent loosening implies strengthening economic data in the coming months.

Overlaying with short-term mis-pricings, we prefer taking selective short USD positions versus the NZD and MXN. We are still neutral on risk but consider high-beta FX oversold given tariff risks.

US rates look overbought, particularly the UST 10y vs Bund. We enter pay positions in MXN and receive ZAR vs US.

In equities, we focus on RV trades, favouring defensive sector RV in Europe and positioning for sector seasonality in the US.

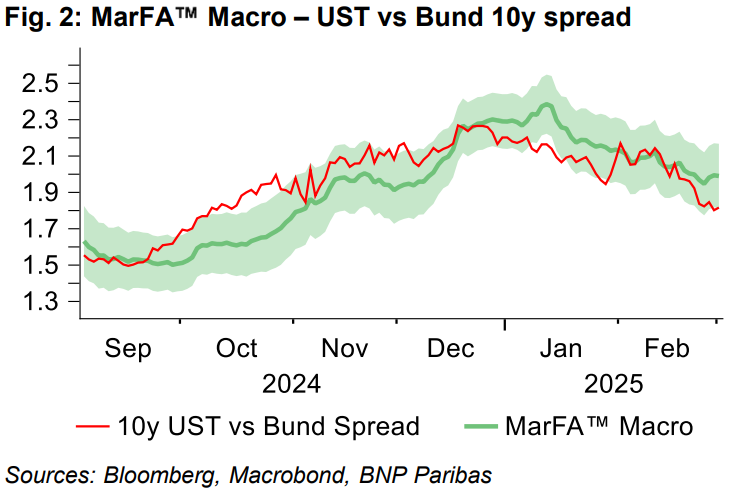

…Trade ideas: Rates Initiating UST vs Bund widener: US rates have continued to outperform their European counterparts and the broader global rates complex. UST 10y and USD 10y are now 22bp (-3.6 z-scores) and 18bp (-2.9 z-scores) below their MarFA Macro fair values, while the Bund and EUR 10y are just 5bp (-0.8 z-scores) and 6bp (-0.8 z-scores) below their respective fair values. We believe this creates an asymmetry and an attractive entry point for UST vs Bund 10y spread wideners.

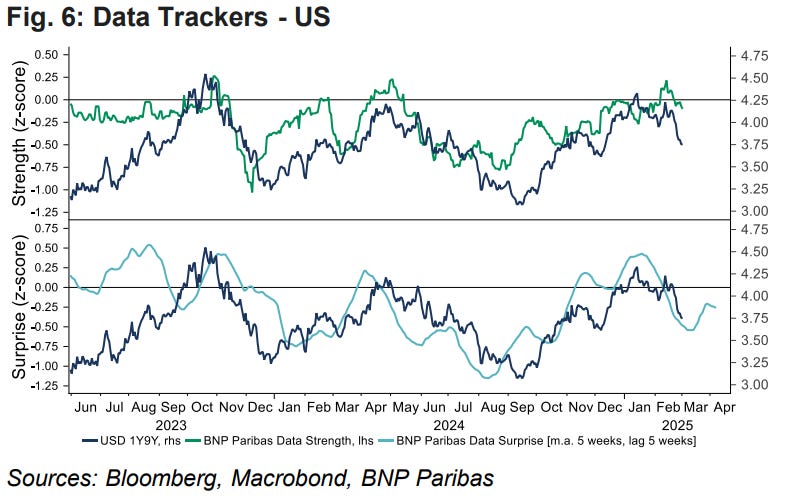

We also think European rates could find support this week due to the slowdown in EGB supply (see European rates: The long and short of it, dated 28 February). On the US data side, 1y9y forwards correlate reasonably well with US data strength, which remains supported, and lagging US data surprises that recently have pointed to mild recovery. Furthermore, our FCI-hard data projections also imply an improving data trend…

Our immediate reaction to the German news around fiscal spending was to add a short Bund trade to our macro portfolio with a target of 3%. This is at the upper end of our indicative Bund yield range (2.70-3.10%) in the event of a regime shift in German fiscal policy. We see the magnitude of the announced fiscal package as justifying this. In this publication we are officially revising our Bund yield forecast to 3% and explain the contributions of each sub-component to this figure.

With Bund/ESTR having already moved quite a lot, most of the upside from here lies in term premia, especially if we also take into account the indicative 800bn defense package announced by the European Commission. The front-end is a bit less clear-cut. When it comes to the ECB decisions in 2025, we still think tariffs will be a major factor, but following the magnitude of the fiscal announcements by Germany and the Commission, the market might be reluctant to price a trough significantly below neutral. Beyond 2025 though, we see upside risks in market pricing of r*. For reference, Holston-Laubach-Williams (HLW) estimates of r* increased by more than 100bp following German reunification.

… MORE on services …

Wells Fargo: Service Sector Pushes Through Policy Uncertainty in February

Summary The ISM Services Index signaled a pickup in activity in February, improving to 53.5 and putting some further distance between it and its manufacturing counterpart. While policy changes seemed to have limited bearing last month on the components feeding into the composite index, concerns over tariffs already appear to be seeping into prices.

…finally from Dr. Bond Vigilante, a question …

Yardeni: Are Tariffs Inflationary Or Deflationary? Are They Really ‘A Beautiful Thing?’

Until recently, the message from the bond market has been that tariffs are deflationary because they depress global economic activity. As Warren Buffett recently observed, they are a tax that consumers, importers, and/or exporters pay. It is widely presumed that tariff increases have a transitory, one-shot, price-rising impact.

Indeed, on Sunday, US Treasury Secretary Scott Bessent predicted that the Chinese "will eat any tariffs that go on." On Tuesday, the Trump 2.0 tariff on China was raised from 10% to 20%. It's unlikely that Canadians and Mexicans will eat the 25% tariff imposed under Trump 2.0 on Tuesday; rather, US consumers will. Recognizing this, on Wednesday the White House announced a one-month tariff exemption for automakers.

We've been forecasting that the 10-year US Treasury bond yield should range between 4.25% and 4.75% this year (chart). It fell slightly below that range in recent days during the tariff turmoil. Now it is back at 4.28%. The comparable TIPS yield has fallen recently on weaker-than-expected US economic data.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

There are adjustment costs associated with changing trade policy and changing the size of the government sector, and the immediate question for markets is how big the short-term pain will be.

The impact on markets and the economy depends entirely on how long the 25% tariffs on Canada and Mexico are in place. If they are removed tomorrow or later this week, then the impact on the economy will be small. If they continue for months, then the negative impact will be more significant, especially to the auto sector.

The bigger risk to markets is sentiment. We are already seeing consumer sentiment and corporate sentiment being impacted, see charts below. If policy uncertainty persists, consumers and firms may begin to hold back spending decisions. Combined with DOGE-driven layoffs, this will put upward pressure on the unemployment rate.

From a Fed perspective, the biggest problem is that tariffs increase prices and hence inflation. That is why a trade war, by definition, is a stagflation shock: Higher prices and lower sales. If tariffs on Canada and Mexico continue for several months, then the Fed will focus on the rising unemployment rate and start cutting rates soon.

The biggest downside risk is that policy uncertainty could create a sudden stop in the economy where consumers stop buying cars, stop going to restaurants, and stop going on vacation, and companies stop hiring and stop doing capex. The employment report on Friday will be stale. The key indicator to watch over the coming weeks is jobless claims, which come out every Thursday at 8:30 am ET.

Source: Conference Board, Bloomberg, Apollo Chief Economist

Source: Conference Board, Haver Analytics, Apollo Chief Economist

Source: Business Roundtable; NFIB; Federal Reserve Bank of Philadelphia, Dallas, New York, Kansas and Richmond; Apollo Chief Economist

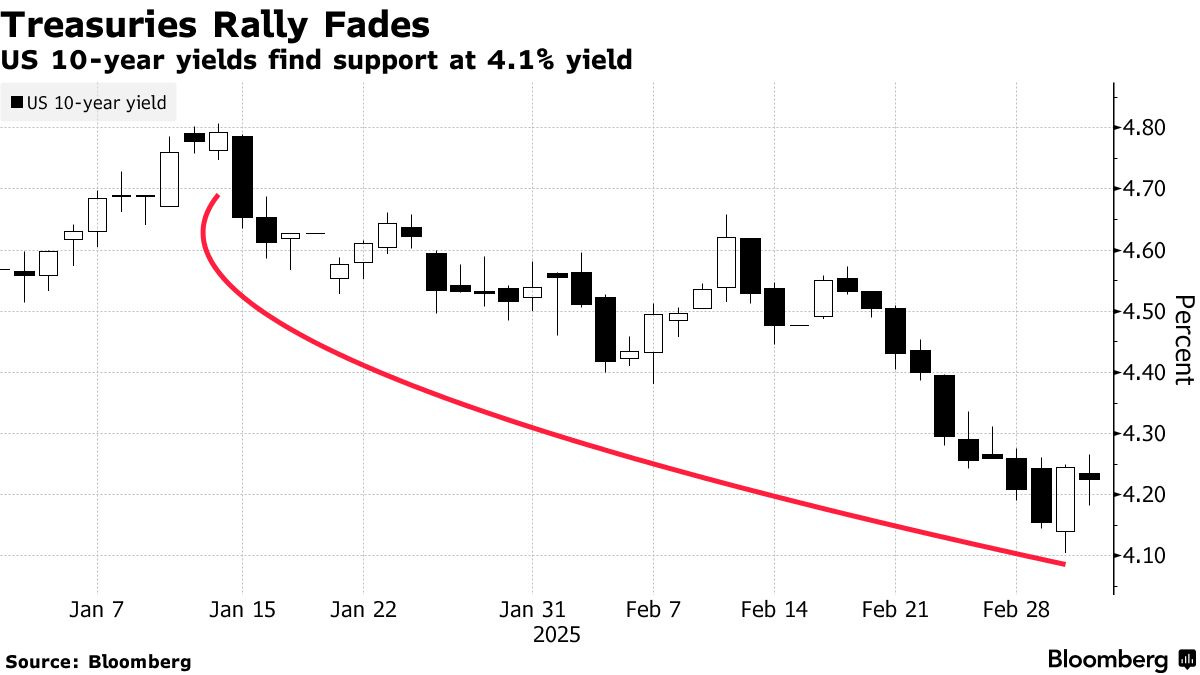

Bloomberg on record futures trade …

Bloomberg: Record Trade in 10-Year Futures Casts Shadow Over Treasury Rally

(Bloomberg) -- A huge block trade seen Tuesday in US Treasury futures was the largest of its kind since 2013, and it may serve as a signal that the recent bond market rally is hitting a wall.

A single trader appears to have sold 78,000 contracts of benchmark June Treasury 10-year futures on Tuesday morning, London time — equivalent to a $5 million bet on each basis point change in the 10-year yield.

Buying and selling in futures markets is anonymous, making it hard to identify the firms involved and the exact details of the transaction. But the time and pricing when the block took place suggests the trader doesn’t expect yields to continue to move lower, as they have over the past two months.

The CME said it was the largest block seen in the Treasury 10-year futures market since January 2013. A similar bet on 10-year notes themselves would have required a roughly $6 billion trade, according to Bloomberg calculations.

The huge transaction comes after a recent rally in Treasuries that has sent 10-year yields from around 4.8% down to as low as 4.1% Tuesday..

Over the past few weeks, there has been a barrage of bullish and now profitable in-the-money call options targeting lower 10-year yields. Some analysts suggested that Tuesday’s big block may have represented a player in the markets taking profits on some of these earlier trades.

“TY call buying seen over the last two weeks may be getting monetized/hedged,” Citi strategists Ed Acton said in a note on Wednesday morning, referencing the trade.

After the big transaction on Tuesday morning, trading in the June contract was choppy. By the end of the day in New York, open interest in the contract fell by roughly 117,000, indicating an overall decline in bets on Treasury notes, according to CME data released on Wednesday.

Yields on 10-year bonds rose roughly 9 basis points to end Tuesday at 4.24%. Those moves flipped the block trade from a roughly $5 million loss at one point to a $45 million paper profit.

From largest trade ever TO … Bernanke …

Bloomberg: Bernanke Says Recent Price Surge May Impact Inflation Control

… “I think in some ways the inflation (surge) has made inflation control a little harder going forward because, you know, firms will maybe find it easier to raise prices, you may see less consumer resistance, people might become more sensitive to inflation and their expectations may adjust,” he said…

… With hindsight, a better communications strategy might have been for the Fed to say that the baseline forecast envisioned transitory inflation but to emphasize more strongly that other outcomes were possible, and if they occurred, to outline in general terms the way that policymakers would expect to respond.

The same strategy could have been used to illustrate in advance the conditions under which quantitative easing would be ended at about the same time, Bernanke said.

From Wolf of Wall …

WolfST: Is This the Beginning of the Second Wave of Inflation?

Companies can’t pass on those higher prices? What a bummer. But if they can without losing sales, it’s off to the races. See 2021/2022.

Finally, you say VIGILANTES and I slow down to read … at least 2x …

ZH: Bond Vigilantes Blow Up German Bond Market After "Whatever It Takes" Fiscal Package

… THAT is all for now. Back IN the inbox Friday morning …