Treasuries were higher overnight with the 7-year sector outperforming. Overnight volumes were modest with cash trading at 86% of the 10-day moving-average. 5s were the most active issue, taking a 35% marketshare while 10s were a distant second at 27%. 2s and 3s combined to take 24% at 14% and 10%, respectively. 7s managed 9%, 20s 1%, and 30s just 4%. We’ve seen buying in the 10-year sector.

Treasuries are higher and the curve flatter out to 7yrs after China cut rates for a second month while ECB's Lagarde spoke about cooler inflation later this year (even after German PPI YoY% hit a record high in December). DXY is modestly higher (+0.11%) while front WTI futures are modestly lower (-0.4%). Asian stocks were mostly higher (Hang Seng +3.4%), EU and UK share markets are mixed while ES futures are +0.5% showing here at 7:20am. Our overnight US rates flows saw good Asian real$ buying in intermediates and the long-end after an Aussie employment-inspired sell-off in the early going. Overnight Treasury volume was solid during Asian hours (around 2x averages) but it cooled significantly during London trade as overnight volume was just75% of average for the night sessionwith only 2yrs (128%) seeing above average turnover this morning.

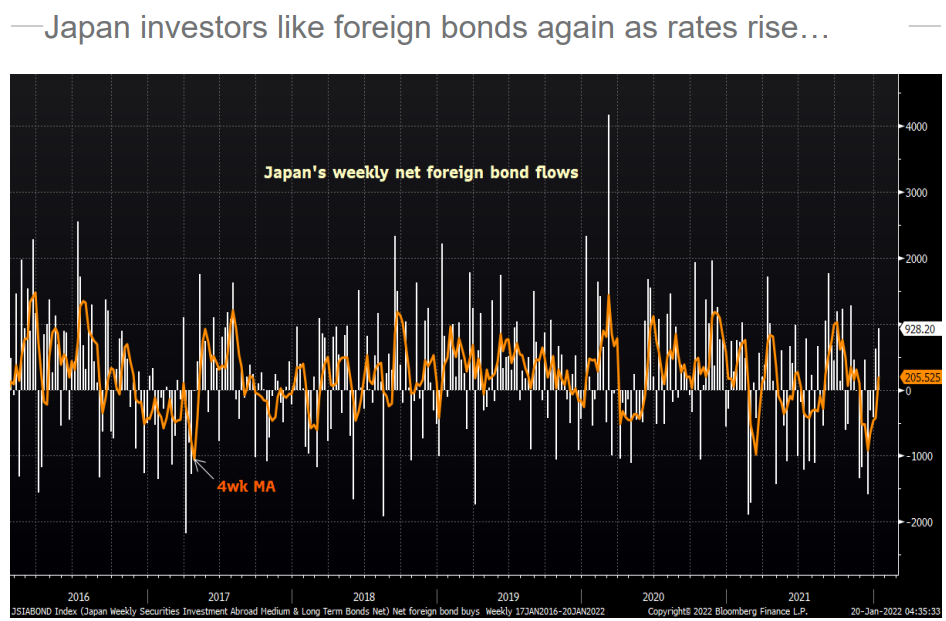

OD as he’s known, goes on to offer more than a few 2yr FWD visuals but this one of MOF flows caught my attention as it’s WEEKLY data and affirms what we saw at yesterday’s 20yr auction:

MOF net foreign bond buying: Switching gears, a look at how Yen-based investors have bought foreign bonds for a second week, pulling the 4-week moving average up sharply off its recent lows.

Links for those who’ve got permission and data ripe for interpretation … Moving on, then, to a look at THE level everyone’s been watching in 10yr futures …

Put strike expiring in mid-February has seen explosive growth

Ten-year note’s yield is approaching the strike-price level

Treasury futures dipped Thursday, edging toward a key level for options traders which could trigger the next leg higher for yields.

The front-dated 10-year contract touched 127 1/4 in early Asia trading, close to the 127 level where a wall of bearish put options has shot up in size since the start of the year. That equates to about 1.92% in benchmark yields, which slipped to around 1.85% Thursday.

…The options in question are the March 127.00 puts, where a wave of buying has lifted open interest -- the number of contracts in which traders have positions -- to 322,648 as of Tuesday’s close. That’s almost double the next-most-popular March put strike and amounts to a notional value of over $32 billion.

“There remains that monster 322k of put open interest at the 127 strike,” said Charlie McElligott, a cross-asset strategist at Nomura Securities in a note. “This level should continue to be monitored as an a potential ‘acceleration point’ on a break lower.”

…With risk also elevated in neighboring strikes above 127.00, selling U.S. 10-year futures as a hedge has the potential to lift yields above 1.95%, if not toward 2%. March options on Treasury futures expire Feb. 18.

MORE news you can use — HEREare IGMs Press Picks for today — 20 Jan. where I’d note,

Moving away from CHINA (for just a moment), and with all of this in mind and considering the current hysteria driving global macro — hikes, Fed, taper/tightening, QT, curvature, SUPPLY > demand, etc — a few words from global Wall Streets most popular ‘plumber’, Zoltan Pozsar (click LINK for graphs)

We are now at a stage where banks are more interested in making loans than buying securities – and that should have the back-end of the Treasury market concerned. Bank of America’s CFO noted that now that loan demand is back, the bank prioritizes “spending” reserves on loan growth as opposed to securities – in fact, during the fourth quarter the bank’s loan book expanded by $51 billion after no growth during the first three quarters of 2021, and added only $14 billion after averaging $100 billion of purchases during the first three quarter of 2021.

The small, $14 billion increase in the bank’s securities portfolio came from a $14 billion decline in the MBS portfolio and a $30 billion increase in Treasuries. The increase in Treasuries was recorded in the AFS book, and as noted by the CFO, reflected the purchase of Treasury securities swapped to a floating rate. Our interpretation of this is that Bank of America continued its habit of buying Treasuries in the 5- to 15-year segment of the curve (see chart on last page), which is in contrast to J.P. Morgan buying the front-end last quarter (see here).

The quarter-end spot and average reserve balances of Bank of America also suggest that our method to proxy the bank’s deployment of liquidity works (see here): chart 5 shows a late-quarter surge in the bank’s reserve balances (flat average reserve balances during the quarter, followed by a sharp spike at quarter-end, which was also mirrored by a surge in reserve balances at the Richmond Fed during December following a period of declining balances during October and November). Reserve balances at the Richmond Fed plummeted by $75 billion during the first two weeks of this year, and this decline corresponds with a pickup in large banks’ purchases of Treasuries and MBS as per the Fed’s weekly H.8 release. That’s the positive bit of news.

The negative is that QE is done, QT is coming, reserve balances at the Richmond Fed are at the lower-end of their recent range (not much left to spend), and loans will now compete with securities to absorb those excess reserves (more to spend on with less to spend). J.P. Morgan – as per Jeremy Barnum’s comments last week – “is still being quite cautious about […] buying duration”, and so it’s legitimate to worry about who will buy all the long-term Treasuries (and at what spread to OIS) once the Fed starts QT (see charts on last page).

Our view that bank portfolios will easily absorb U.S. Treasury issuance amid plenty of excess liquidity and slow loan growth is changing now that loan growth is back and QT is approaching. But unlike in 2019, we’re not concerned about funding but swap spreads – a topic we’ll explore in a series of Dispatches next.

And b ack TO CHINA, making the point with some additional PBoC input, Morgan Stanley reminds us WHO really is in charge of global macro these days,

The PBoC sent a loud and clear pro-growth messagewith a rate cut and an unequivocal statement. While January credit growth may remain sluggish, we expect TSF growth to pick up in 1Q, as LGSB issuance and infrastructure project launch is accelerating.

China has been very slowly loosening monetary policy as its property sector suffers from a downturn, whereas the Fed has made a big hawkish shift in recent months, the net result of which has been a large shift in yield differentials between the two countries. Typically, we would think of such yield shifts as having an instant impact on the exchange rate between two countries, but as this chart shows, such yield shifts often precede a move in USDCNY exchange rate. That’s likely because the level of the CNY is as much a political one as one determined by markets, with the Chinese government having a large say in the level its sets the currency at. The problem is that it's hard to take advantage of the leading nature of the relationship when it moves in this direction, because the higher level of interest rates in China means shorting the currency will result in negative carry for most investors.

Have a great start to your messy commute Thursday AND in closing, why 127 10yr futures strikes may not matter, OR perhaps be a shorter term distraction (or trading motivation?) from investing.com