If you were looking for BREAKING NEWS headline driving price action type stuff, well, I’ll apologize ahead of time. I wasn’t very good at that when IN a seat with more capabilities and frankly, trends, technicals and momentum were almost as important as EMOTION of the moment. You know and I don’t have to tell you that letting emotions creep in to your P&L or investment portfolio normally doesn’t work out well. Fiduciary duties require you to check emotions at the door and while the BREAKING NEWS type stuff may ultimately inform longer term thinking, let us not begin our day here together with it. For that, I’ll monitor twitter and the likes of cnbc etc, where you’ll find

I will begin here with what happened,

WHILE YOU SLEPT Treasuries are sharply higher and the curve little changed (2s30s Tsy curve UNCHD vs yesterday's 5pm) after Russia invaded Ukraine overnight. DXY is sharply higher (+1%) while front WTI futures broke above $100/bl, +8.2% here at 7am. Asian stocks were -1% to -4.7% (Nifty 50), EU and UK share markets are roughly -3% (FTSE 100) to -4.7% (DAX) and ES futures are showing -2.2% here at 7am. Our overnight US rates flows saw real$ and fast$ buying (5's to 30's) during Asian hours with some offset selling from real$ (3's and 30's) too. My London colleagues then reported an 'insane' session with 20yr benchmark underperformance (10s20s30s +3.5bp at one point earlier) noted alongside solid CB buying in the front end. Overnight Treasury volume was roughly 2x average with 20yrs (425%) seeing relatively standout turnover.

… World News: Russia attacks Ukraine WSJ Russian stocks plunge (see attachments), Ruble hits record low FT *RUSSIAN CDS PREMIUM SOARS ABOVE 750 FOR FIRST TIME SINCE 2009 (BBG) Oil rises above $100/bl for first time since 2014 FT *BRENT CRUDE HITS $105 A BARREL FOR FIRST TIME SINCE 2014 (BBG) NASDAQ 100 futures point to first bear market since March 2020 BBG World inflation shock set to worsen BBG Wheat and Corn prices surge anew as Russia 's attack threatens supplies, fertilizer prices climb further BBG Europe's energy prices soar after attack BBG NATO convenes emergency session AP China ready to soften economic blow to Russia from sanctions FT A big US chip-maker warns of tight supplies until 2027 BBG

… UST 5yrs, weekly: We'll pick on 5's as one of our few 'duration' proxies. What you can see is that in recent weeks 5yrs have respected support near 1.90%- a support derived by the summer 2019 range highs. Medium-term, weekly momentum (lower panel) is predictably deeply 'oversold' and threatening a new bull signal. Tomorrow's close may or may not confirm this emerging bullish signal. Simply, 5's appear to have plenty of bandwidth to rally further from here under the right conditions.

… And for some MORE of the news you can use » IGMs Press Picks for today (24 FEB) to help weed thru the noise (some of which can be found over here at Finviz). And please don’t forget to get those bids in for 7yr USTs early and often…recall it was only last year when 4p became the new 3p which was fully digested after last years Feb 7yr auction. Disasterous selloff provided a bit of a concession for month-end index and foreign demand… **IF** my memory serves me correctly. IF NOT, I’ll up my dosage of ginko

For even MORE, this mornings rather early morning writeup from a large German bank,

… The market reaction to these developments has been seismic, with Brent Crude oil prices surpassing $100/bbl for the first time since 2014, whilst S&P 500 futures are currently down -1.92%, on top of the index’s -1.84% decline yesterday. US Treasuries have also rallied strongly this morning as investors have moved into haven assets, with the 10yr yield down by -11.8bps to 1.873%, and gold prices have surged +1.90% to their highest level in over a year, at $1,945/oz. Otherwise overnight, the Ruble has sunk to a record low against the US dollar in the interbank trade, whilst other commodities are reacting, including aluminum which has hit a record high in London and surpassed its 2008 peak.

This morning, markets in Asia are sharing in this global risk-off move, with the Nikkei (-1.96%), the Hang Seng (-3.18%), the Shanghai Comp (-1.40%) and the CSI 300 (1.94%) all seeing major declines. Ahead of the breaking news on Ukraine, the Bank of Korea also held their policy rate at 1.25%, in line with expectations.

Even before the serious developments overnight, yesterday had already been an incredibly eventful day in markets, with the highlights including 1) that the FANG+ index has now wiped out all of 2021s gains and has lost around a quarter of its value from the November peak, 2) the S&P 500 is now down more than -10% YTD for the first time, 3) 2 year US breakevens rose a huge +20.6bps, 4) German 10 year breakevens hit decade plus highs and 5) European natural gas was up more than 10% again (and that was before the overnight developments).

Those moves yesterday came amidst a continued souring of risk sentiment given fears of a potential conflict that’s since transpired. There had been a more positive tone 24 hours ago during the European morning, but that turned shortly after the US open after news came through from Ukraine that numerous websites had suffered a distributed denial-of-service attack. That saw the S&P 500 (-1.84%) gave up its opening gains and lose ground for a 4th consecutive session. And as mentioned, for the first time so far this year, the S&P ended the day more than -10% lower on a YTD basis, which is a big turnaround from how 2022 began, having reached an all-time closing high on the first trading day. Cyclical sectors underperformed, and the FANG+ index of megacap tech stocks fell by -3.01%, marking the fourth consecutive day of declines greater than 2% for the first time since December 2018. The drop brought the index to its lowest closing level since December 2020, having now fallen by -24.97% since its all-time closing high back in early November. The Nasdaq (-2.57%) also almost wiped out its 2021 gains. For Europe the market had closed before the bulk of the losses, but with the STOXX 600 (-0.28%) closing at its lowest for 2022 as well.

In terms of the broader global impact, a significant way the events in Ukraine will affect the rest of the world is regarding inflation, and even before we saw $100/bbl oil overnight, that relentless rise in commodities showed no sign of abating yesterday. Along with European natural gas prices gaining +11.41% as mentioned, wheat futures (+3.78%) climbed to their highest since late-2012, and soybean futures (+2.45%) managed to eclipse their peak from last May, taking them to their highest levels on record. All-in-all, that sent the Bloomberg Commodity Spot Index (+0.70%) to another record high, suggesting there’ll still be significant momentum behind inflation for some time to come.

These growing fears of inflation among investors led to a further selloff in sovereign bonds on both sides of the Atlantic, although overnight the movement in Treasuries has completely reversed that. But for a sign of how acute those inflation concerns are growing, 10yr German breakevens were up +5.4bps to 1.97%, their highest closing level in over a decade, though 10yr bunds pared back moves later in the session, ending the day down -1.5bps, thanks to a decline in real yields. The pressure was even stronger across the Atlantic; the 2yr US breakeven rose a remarkable +20.6bps to 3.96%, which is its highest in Bloomberg data series going all the way back to 2004, while 5yr breakevens rose +16.7bps. Given that, yields on 10yr Treasuries were up +5.2bps to 1.99%, with breakevens up a paltry +9.5bps by comparison. So falling real yields helped prevent a US bond meltdown.

These inflationary moves seemed to be even forcing the resident doves of both the ECB and the Fed to sound a more hawkish tone despite the geopolitical turmoil, although the big question now will be how developments overnight will affect their reaction function. Fed funds futures have slashed the implied odds of a 50bp move in March to just 16%, which is the lowest in over 3 weeks before we had the CPI report. The number of 25bp hikes priced for the year as a whole has also gone down from 6.48 to 6.00, suggesting that (at least for now) investors believe this is going to make central bankers more dovish rather than hawkish as they react to the turmoil, even with inflationary pressures building.

In terms of yesterday’s central bank news, ECB Chief Economist Lane noted in an interview that there was growing confidence in medium-term inflation returning closer to the target, and if the data suggests their medium-term inflation goals were within reach, that policy would be adjusted. Unlike other previous ECB speakers, that adjustment was not couched in gradual terms. While emphasising a commitment to the exit sequence of ending net APP purchases before liftoff, Lane noted the timeline of purchases may be shorter than was expected. In line with other speakers, Lane also noted the ECB would leverage PEPP reinvestments to defend against policy fragmentation. Against that backdrop, there was a further widening in peripheral spreads, with the gap between Italian and German 10yr yields up to another recent high of 171bps, which we haven’t seen since June 2020, and the Greek spread hit 237bps, which hasn’t been seen since May 2020. Separately, President Daly of the SF Fed said a March liftoff was still on the table despite growing political risks. She also backed four Fed rate hikes this year, and left the option open for more if needed…

Sadly, events in Ukraine are turning yesterday’s armchair virologist into today’s armchair military strategist. Speculation by traders, who have acquired just enough knowledge to convince themselves that they are the modern-day Alexander the Great, does not necessarily make for rational pricing of risk.

The oil price will grab the headlines, although this is a reflection of risk pricing (neither supply nor demand has changed). Economically, the oil price today is irrelevant. The average oil price over the next three to six months is what will determine wealth transfers from oil buyers to oil sellers, and associated shifts in global spending patterns.

The other economic issue is sanctions. Sanctions to date have been economically meaningless (and, obviously, politically ineffective). Increasing sanctions could be more economically disruptive. Importantly, this is the first European war with a real-time Twitter handle. The role of social media in shaping European, UK and US public reactions to the war could be a factor in determining the strength of sanctions applied by those governments.

US initial and continuing claims numbers will get some attention. The US is revising Q4 GDP—financial markets pay less attention to data revisions than they should. There is a full pontification of global central bankers speaking.

The very idea of ‘the West’ using moral fortitude and war-gaming falling short when compared to what appears to be playing out in favor of Putin (war > Earl bid > he wins > no war > more Russian territory under control > he wins?) is very disheartening to some of this country. Who have seen this movie before (or a similar one last time some of this administration was in power — crazy coincidence, right?).

This too shall pass and sell (stocks, yields) and buy the rumor, right?

My Grandfather taught me all about appeasement and political failure. And he gave me a love of history – and an understanding of how even after such terrible mistakes, democracy eventually triumphed.

History repeats. Let’s hope not so bloodily. Democracy works. Kleptocracies don’t…

Moving along as we become students of history, some updated thoughts from GS which seem to ME to be self contradicting and only GS could get away with this type ‘analysis’ and come off seeming even MORE popular,

The Asset Market Risks of the "Slowdown That We Need"

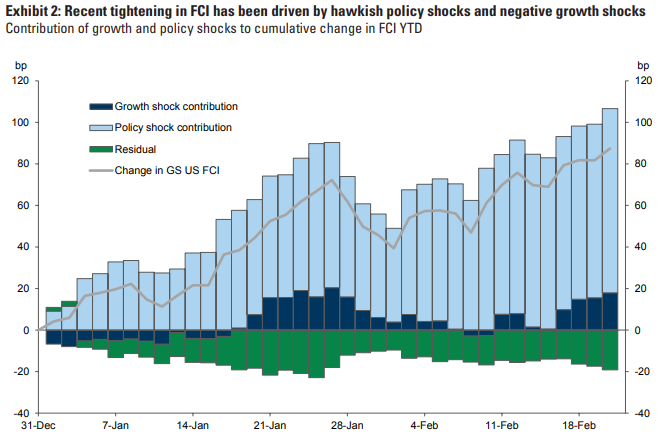

■ With wage and price inflation persistently higher than expected, growth needs to slow and financial conditions need to tighten. In our baseline forecast, a steady series of Fed hikes slows growth enough to bring inflation back towards target over the next couple years. But there is a growing risk that Fed officials will want to see a faster slowdown in output and employment growth and will act to tighten financial conditions more aggressively to slow growth to potential.

■ So far, recent tightening in financial conditions appears to have been driven more by policy than growth worries. Tighter monetary policy and negative growth shocks both work to tighten financial conditions, but the mix of the shocks matter for asset outcomes. Here we lay out the asset market implications of financial conditions tightening in the US driven by an attempt to slow growth to trend.

■ We estimate that if the Fed tries to slow growth to trend, the S&P 500 could—all else equal—fall roughly 10% from current levels, alongside a further rise in shorter-dated bond yields. In this scenario, some of this year’s more resilient areas—cyclical equities and credit—would probably see more pressure than they have so far. We could see larger declines in risk assets, and longer-dated yields might actually fall if the Fed tightened even more aggressively or the economy proved more sensitive to that tightening.

Same firm With THAT in mind, a few thoughts / links to some relatively updated TECHNICALS to help as they say, in price there is truth.

Chart of the Day: As Oil and front-end breakevens push higher, it is notable that US 30yr Inflation Breakevens are actually moving lower and have completed a relatively large top. Furthermore, weekly MACD has turned outright negative and the 55-day average has crossed below the 200-day average, which is now falling. We therefore see the medium-term risks as skewed to the downside from here, with scope for an eventual fall to 191bps, which is the “measured top objective”. We still expect 10yr Breakevens to remain relatively rangebound for now.

10yr US Bond Yields recently broke below intraday resistance at 1.905/89%, which should have triggered a small “double top” and a deeper correction lower. So far, the market has failed to follow through on this break lower, however with risk assets expected to come pressure, we expect a deeper correction lower from here, with scope for a corrective move back to 1.755/74%.

They go on to UPDATE some stops and NEW TRADES — again these were submitted yesterday afternoon so,

5yy: Our modestly unsuccessful tactical bearish view from resistance at 1.825% was negated following the break below next resistance at 1.81% and our preference is to stay tactically neutral going forwards. 10yy: Our cautious tactical bearish bias was negated following the break of resistance at 1.89%. From here, we see favorable riskreward to turn tactically bullish, with scope for resistance at 1.755/74%, with support at 2.065%, above which we would turn tactically neutral. 30yy: We finally turn tactically neutral on our successful tactical bearish bias from 2.085% following the break below resistance at 2.21%.

BUY HIGHER PRICES and SELL SAME HIGHER PRICES … Key is, as always, having DISCIPLINE trump emotions. There’s ALWAYS an opportunity it’s just in the way you see them. Have cake and eat it too? Keep your friends close and your stops closer

Hedgopia: S&P 500 Sits On Crucial Support, Breach Could Send Bears Into Panic, Which Bulls Should Like

With all that said, and thinking ‘bull’ mkt gold and ‘Earl as we study A MAP and become Ukraine experts, I can’t help but note THESE WORDS from Bloomberg overnight which again help express the idea of ‘nothing without consequence’ (high / rising ‘Earl leading to inflation fears, pricing),

… As the Ukrainecrisis adds to global inflationary pressures, the world’s safest assets risk becoming just a temporary shelter. Bonds caught a flight-to-safety bid Thursday after Vladimir Putin's special operation to “protect” the Donbas region. But the very nature of the geopolitical situation makes even relying on Treasuries -- the traditional safe haven asset -- a tricky call at the moment. The obvious market risk from an escalating conflict is a further spike in commodity prices -- exacerbating the rise in inflation at the very moment it is most feared. That increases the pressure on central bankers to act and acts as an anchor on bonds. Two-year U.S. breakeven rates -- a gauge of short-term inflation expectations -- surged to a record this week as oil rallied, in data going to 2004. That has strategists scrambling to suggest substitute havens from the old reliable gold to high dividend-yield stocks to a broad basket of commodities. There's also the option of raising cash, at least until the risk of a widening conflict passes.

The very idea of choosing CASH — a non-earning safe-haven substitute reminds ME of something I wrote / sent this past summer. Click thru to MY VIEWS for more. Here’s an excerpt of an email (with links) to an email sent July 13th, 2021 and I’ll apologize ahead of time. It was and IS meant to offend one and all!

time: 08:19:00 subj: good (bank boom, BULLard SAYS time RIGHT; NFIB optimism, PRICES off charts)morn

Good morning. Today’s PDF is updated and today you’ll find

A couple bullets and links dedicated TO the booming bank beats as well as how Yellen SEES corporations supporting her tax (what did you expect her to say). It’s also noted in today’s WSJ that BULLard says time is RIGHT TO TAPER (same script Kaplan read to us via Barrons over the weekend) and finally, you’ll note link thru to NFIB report which was released EARLY (it’s what happens when you have such good news?). Will prices feed thru to Core PCE YoY (CoTD)?

Technicals: bearish 30yy levels to watch for this afternoons liquidity event (for the bullish ones, see today’s daily pivots). ALSO note S&P is +100% from THE March 2020 lows (ChartReport) so congratulations to everyone who nailed it. CitiFX watching 30yr BREAKS breaking higher and CSFB continues to lean bearish

My Views: perhaps the most consequential MONTHLY MUSINGS (Free Willy, sorry Rush fans) ever as a call for help (and your best cartoons) which will be rewarded. It's both bearish AND bullish (ie buy the taper dip). You’ll ALSO note another look at Citi Surprise Index, the BULLard headlines and another important WSJ story of Governments Gorge on Record Debt (HIMCOs LATEST, anyone??) …