Good morning. Before I begin, I’d like to copy / paste something from Alfs MacroCompass because it’s relevant today on two fronts. Yesterday he said

Actually, before we jump right in. If you are struggling to keep up with all the good macro newsletters out there, I get you. But the guys at Harkster.com have a handy solution: they created a fantastic newsletter aggregator that allows you to keep track of the ones you like, and find brand new ones to read. I am using Harkster myself, and you can also check out which macro newsletters I am reading!

Back to it: do you know what’s the biggest market cap asset class in the world? Equities? No. Bonds? No, try again.

The real estate market is by far the biggest asset class in the world: summing up residential and commercial real estate with agricultural land, at the end of 2020 the estimated market value of the global real estate market was at $326 trillion or about 40% bigger than the global bond and equities markets combined!

Great minds think alike (OR fools never differ)? Please apply to any / all concerned — Alf, Harkster.com (and those who’ve requested MY presence - thank you!!

Onwards and upwards.

Stocks STEADY off recent lows and marginally better bid, bonds underwhelmed (waiting for whatever shoe will drop next). CNBC,

BREAKING: Mortgage applications drop to lowest level in over 2 years … “Higher mortgage rates have quickly shut off refinances, with activity down in six of the first seven weeks of 2022,” said Joel Kan, MBA’s associate vice president of economic and industry forecasting…

Hmmm … higher rates (and, um, prices), lead to lower applications? Who’d a thunk. For somewhat more competent read thru, see this from Calculated Risk and also,

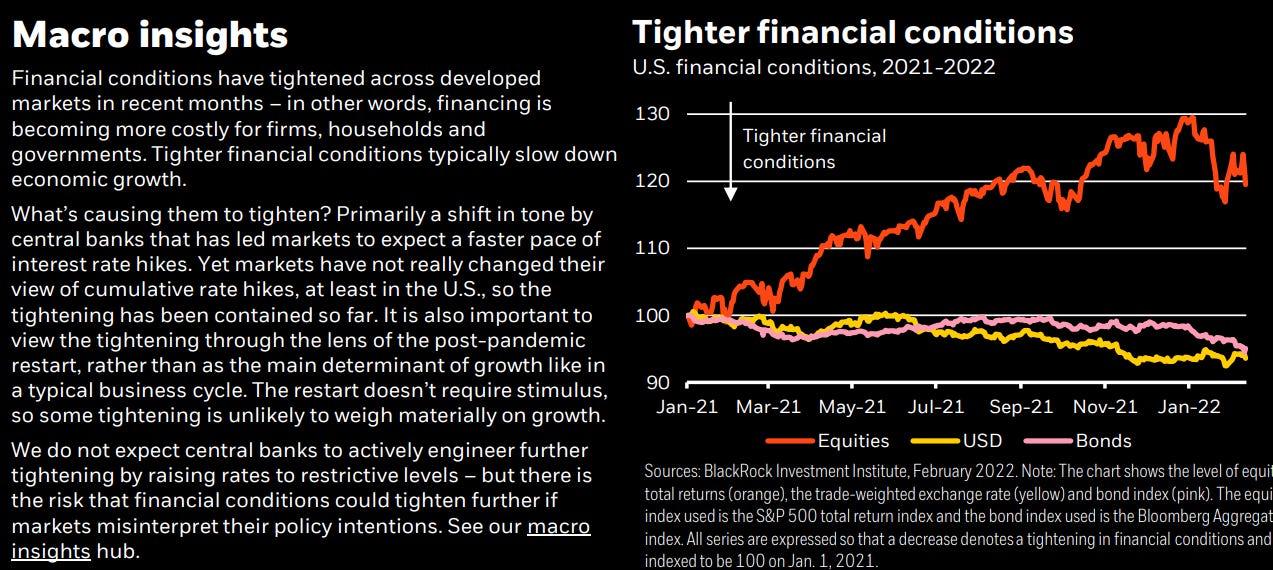

Or don’t … With stocks on verge of bearish H&S (Yes, pundit, we all see it. -@mnkahn), credit on the (widening)move and some saying in all this, Confusion yields opportunity (BlackRock — liking stocks, generally speaking, see WEEKLY — PDF HERE) where they note,

We up our strategic overweight to developed market (DM) equities, but near term elevated geopolitical tensions keep our tactical shopping basket on hold.

Equities retreated as investors took renewed fright over the military stand-off involving Ukraine, helping pull down short-term bond yields from recent peaks.

The market’s focus this week will be on PCE inflation, the Fed’s inflation target, for clues on the timing and magnitude of coming rate hikes.

They ALSO detail somewhat TIGHTER financial conditions

More on financial conditions in a bit … for NOW, though, here’s what happened overnight … this from THE best in biz and a morning update, “Only 33 bp to Go…”

…Overnight Flows Treasuries were weaker overnight with the 2-year sector leading the selloff. 2s/10s flattened to 33.4 bp and 5s/30s slipped to 35.5 bp. Overnight volumes were modest with cash trading at 67% of the 10-day moving-average. 5s were the most active issue, taking a 34% marketshare. 3s were second at 22% while 10s took 21%. 2s managed 15%, 7s 5%, 20s <1%, and 30s 3%. We’ve seen selling in 2s, 3s, and 5s.

…5s – The new high yield print in 5s is 1.983% which is immediate support before a handle change along with an unfilled opening gap from 1.992% to 2.020%. 2.236% is a local yield high from May of that year that is support before 2.25%. The previous range top at 1.79% will now be resistance beyond the 1.728% 21-day moving average. Momentum in the form of stochastics have crossed bullishly and are now pulling back from oversold with room to run, so from this perspective a bullish lean resonates. The volume bulge centered around 1.62% will be a hurdle in a larger rally along with the 40-day moving average of 1.576%.

And for some MORE of the news you can use » IGMs Press Picks for today (23 FEB) to help weed thru the noise (some of which can be found over here at Finviz).

TODAY: Mortgage Apps @ 7a (no bueno — see above) THEN 5yr auction @ 1p. Bids in early and often, please. Here’s 1.80% yield level (RED LINE)in some context … long-term and short:

In terms of the big, bad Russia and sanctions being announced by politicians as they victory-lap with each other, showing their solidarity and reiterate their own moral fortitude. A few words of context (and snark) from UBSs Paul Donovan (yea, THAT one),

Some have described sanctions against Russia as "more aggressive". This is difficult to argue for the macroeconomic impact. Germany closed a pipeline that was not open. Japan banned sovereign debt issuance that does not take place. The US pledged to stop the Russian government accessing international finance they do not really need. The UK has focused on threatening to do more in the future. Financial market reactions are more about fear of future action than pricing in current action.

The oil price spike does increase inflation pressures in the near term. It does not stop inflation falling later this year (it is the change in the oil price, not the level, that matters for inflation). However, the increase in the oil price is a de-facto tax on oil-consuming economies—which threatens to reduce economic activity in non-energy sectors…

Here’s a feel-good story of the day via Goldilocks,

Karma’s a b!tch, ain’t it? High and rising price of ‘Earl, consequently, is also a b!tch for most of ‘Merica and so, on $100 ‘Earl, this from BBG

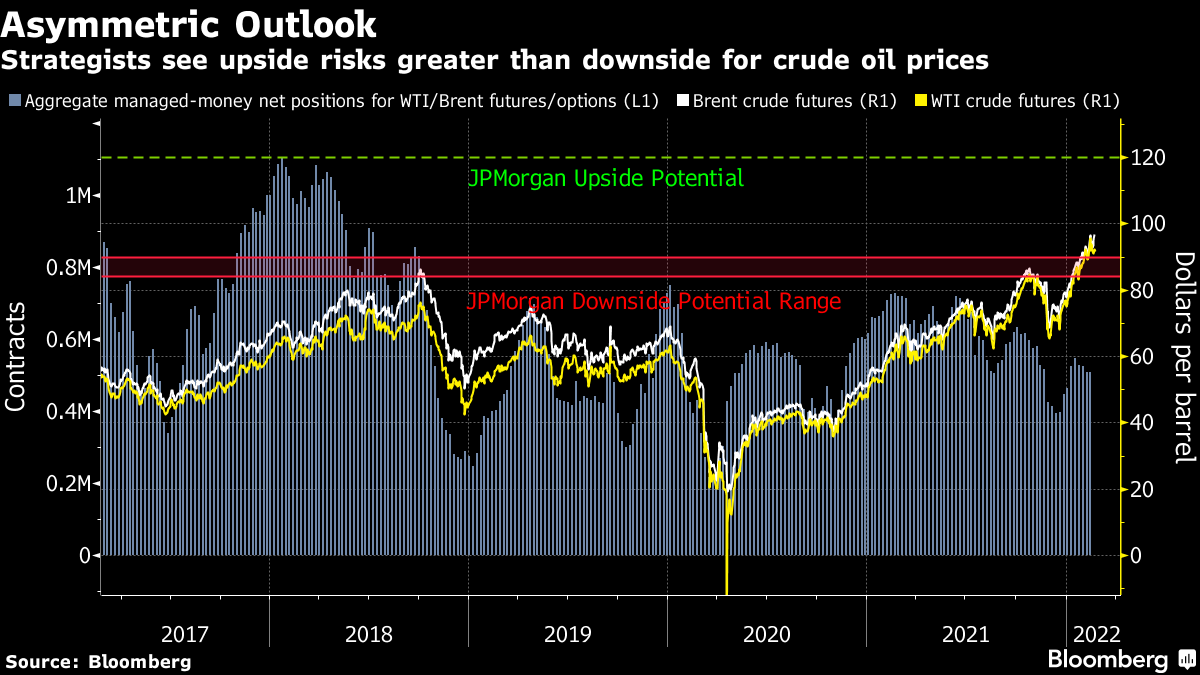

Oil is firmly in the market spotlight, caught in a tug-of-war between Russia and Iran as the key $100-per-barrel level looms for the first time since 2014. But supply is so tight that the risks look asymmetric, with more potential upside than downside, according to strategists. The upside risk is sadly obvious, the potential for escalating conflict in Ukraine, while the downside risk is the more optimistic potential for increased supply from Iran should a nuclear deal be reached. Iran was one of OPEC’s biggest crude producers and many traders expect it will be able to boost daily exports by about 1 million barrels within just a matter of months if sanctions are lifted. But key OPEC+ members look wedded to a strategy of gradually raising production and see no need to be more aggressive, which means the market can still remain tight. JPMorgan suggests oil could easily hit $120 a barrel on a worsening of the situation in Ukraine but would find a floor of between $84-$90 a barrel even with an Iran deal. So far traders remain agnostic with a gauge of bullish bets on oil futures well below last year's highs. But a move through $100 would likely trigger some momentum trades, suggesting bullish interest is likely to pick up.

AND this more simply, from investing.com for us visual learners,

Meanwhile, a nice and simple map from Stratfor via @PriapusIQ (here),